If you find yourself asking, “How much do I need to retire at 65?” the real question is not whether you have $500,000, $1 million, or $2 million saved. It is whether your savings can create enough reliable income after Social Security, Medicare costs, taxes, inflation, and market risk are included.

Two people can retire at 65 with the same portfolio balance and have completely different outcomes.

Because retirement readiness depends on your income gap, not just your account balance.

A practical estimate is to take your annual retirement spending, subtract Social Security, pensions, and other reliable income, then multiply the remaining income gap by 25 to 30.

For example, if your savings need to provide $40,000 per year, you may need roughly $1 million to $1.2 million saved to retire at 65.

Key Takeaways Ahead

Quick Answer: How Much Money Do You Need to Retire at 65?

A common starting point is that many retirees may need 10 to 12 times their annual income saved by age 65, but the better answer is based on your spending, guaranteed income, taxes, healthcare costs, and how long your money may need to last.

A simple retirement savings estimate looks like this:

Annual retirement spending need

minus guaranteed income

= portfolio income gap

Portfolio income gap × 25

= estimated retirement savings needed

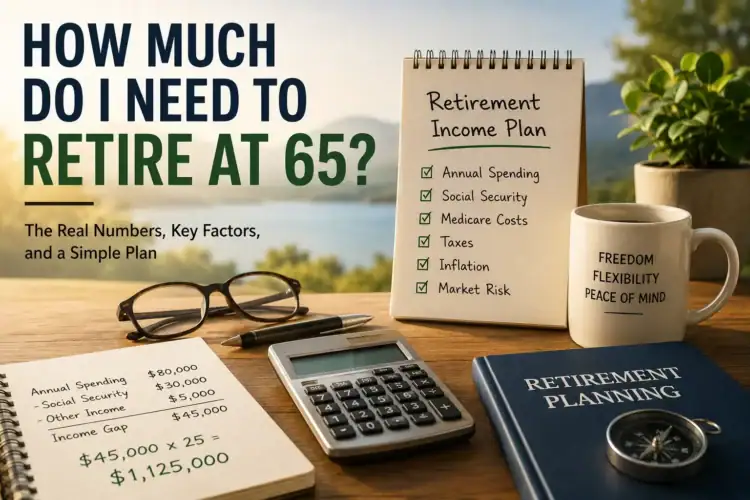

For example, if you expect to spend $80,000 per year in retirement and receive $35,000 per year from Social Security and pensions, your portfolio needs to cover the remaining $45,000 per year.

Using a 4% withdrawal guideline:

$45,000 ÷ 0.04 = $1,125,000

In that example, you may need about $1.1 million invested for retirement at 65.

But that number can be too high or too low depending on your taxes, Medicare costs, debt, home equity, life expectancy, investment risk, and whether your spending changes over time.

Why There Is No One Perfect Retirement Dollar Amount Needed For Everyone

Most retirement articles give a simple rule of thumb. The problem is that retirement is not one number. It is a cash-flow problem. That is why a broader retirement planning strategy should start with income, taxes, healthcare, and withdrawal timing. Not just a single savings target.

The better question is not:

“How much money do I need to retire?”

The better question is:

“How much income do I need my savings to create after Social Security, pensions, taxes, healthcare, inflation, and required withdrawals?”

That distinction matters because two people can both retire at 65 with $1 million and have completely different outcomes.

Two retirees can both reach age 65 with the same portfolio balance, but their retirement number can look completely different once income, debt, healthcare costs, and taxes are included.

| Retiree A: More Flexibility | Retiree B: More Pressure on Savings |

|---|---|

| No mortgage | Still has a mortgage |

| Pension income helps cover monthly expenses | No pension, so investments must do more of the work |

| Lower healthcare and prescription costs | Higher prescription drug and out-of-pocket healthcare costs |

| Modest travel and lifestyle plans | More expensive travel and lifestyle goals |

| Paid-off home reduces required monthly income | Housing costs keep the annual income need higher |

| Spouse has Social Security benefits | Adult children or family support may increase spending |

| More after-tax flexibility if savings are spread across account types | Most savings are in tax-deferred accounts, so withdrawals may increase taxable income |

Why this matters: Retiree A may need a smaller portfolio income gap because Social Security, a pension, and lower fixed expenses cover more of the budget. Retiree B may need a larger savings target because more of the retirement income must come from taxable portfolio withdrawals.

Same portfolio balance. Very different retirement readiness. That is why the real question is not just how much you have saved, but how much income your savings must safely produce.

The Retirement Number Formula

A practical way to estimate how much you need to retire at 65 is:

Step 1: Estimate annual retirement spending

Step 2: Subtract Social Security and pensions

Step 3: Calculate the annual income gap

Step 4: Multiply the gap by 25 to 30

Example Retirement Number Calculation

| Retirement Planning Item | Example Amount |

|---|---|

| Desired annual retirement spending | $80,000 |

| Estimated Social Security income | $30,000 |

| Pension or other guaranteed income | $5,000 |

| Annual portfolio income needed | $45,000 |

| Savings needed using 4% rule | $1,125,000 |

| Savings needed using 3.5% rule | $1,285,714 |

The 4% rule suggests that a retiree may start by withdrawing about 4% of their portfolio in the first year of retirement, then adjust withdrawals over time. But it is not a guarantee. It is a planning guideline.

- The 4% guideline comes from historical retirement withdrawal research, but it should be treated as a planning estimate rather than a promise.

- For a deeper look at the assumptions and limits behind this estimate, see my guide to the 4% withdrawal rule of thumb.

Plain-English Version

Your retirement savings do not need to replace your entire paycheck. They need to replace the part of your spending that Social Security, pensions, annuities, rental income, or other reliable income sources do not cover.

Why Retiring at 65 Is Different From Retiring at 67 or 70

Age 65 feels like the traditional retirement age because it is tied to Medicare eligibility. But 65 is not the same as full retirement age for Social Security for many retirees.

Social Security full retirement age depends on your birth year. The Social Security Administration says full retirement age is between 66 and 67, and your retirement benefit generally increases the longer you wait to claim, up to age 70. The Social Security Administration explains that full retirement age is between 66 and 67, and that retirement benefits are higher the longer you wait to apply, up to age 70.

That creates an important planning issue:

Retiring at 65 does not automatically mean claiming Social Security at 65.

Before choosing a claiming age, compare how your monthly benefit changes based on when to take Social Security benefits.

You might retire from work at 65 but delay Social Security to receive a larger monthly benefit later. That can be helpful if you have enough savings to cover the income gap in the meantime.

Why This Matters

If you retire at 65 and claim Social Security before full retirement age, your m0onthly benefit may be permanently reduced. If you delay benefits, your savings may need to cover more of your spending for a few years, but your future guaranteed income may be higher.

This is why your retirement number depends not only on your savings balance, but also on your Social Security claiming strategy.

The 5 Key Questions to Answer Before Retiring at 65

Before you ask, “Do I have enough saved?” walk through these five questions. Your retirement number depends less on your account balance and more on how much income your savings must safely create.

Spending Need − Guaranteed Income = Portfolio Income Gap

Portfolio Income Gap × 25 to 30 = Estimated Savings Needed

Your retirement number is not a single magic savings target. It is the result of five moving parts: spending, guaranteed income, portfolio withdrawals, taxes, and time.

Considering retirement before 59½? Your account-access plan matters as much as your savings total. The Rule of 55 may allow qualifying withdrawals from an employer retirement plan after a properly timed separation from service, but rolling that money into an IRA first can eliminate this particular early-access option.

How Much Will You Spend Each Year in Retirement?

Start with your current spending, not your current income. If you are not sure what a realistic retirement budget looks like, start by estimating a good monthly retirement income based on your housing, healthcare, taxes, travel, and basic living expenses.

Many people estimate retirement needs based on salary, but salary includes things you may not need in retirement, such as:

- Payroll taxes

- Retirement plan contributions

- Commuting costs

- Work clothes

- Professional expenses

But retirement can also add costs, such as:

- Travel

- Hobbies

- Healthcare

- Home repairs

- Helping family

- Long-term care planning

A useful first estimate is:

Current annual spending

- minus work-related expenses

+ plus new retirement expenses

= estimated retirement spending

How Will Taxes Affect Your Retirement Income?

This is where many retirement estimates are too simple.

A retiree with $1 million in a Traditional IRA does not have the same after-tax spending power as a retiree with $1 million in a Roth IRA or taxable brokerage account.

Expert wording:

Tax-deferred retirement accounts create ordinary income when withdrawals are taken.

Plain-English wording:

If most of your money is in a Traditional IRA or 401(k), you may owe income taxes when you use that money.

That matters because taxes reduce the amount of portfolio income you actually keep.

How Long Does Your Money Need to Last?

Retiring at 65 could mean funding 25, 30, or even 35 years of retirement. A retirement savings target is only useful if you also test how long your money may last under different withdrawal rates, inflation assumptions, and market conditions.

That is why your retirement savings number must account for:

- Inflation

- Investment returns

- Market downturns

- Healthcare costs

- Longevity

- Spousal income needs

- Long-term care risk

The goal is not just to retire at 65. The goal is to stay retired.

How Much Should You Have Saved by Age 65?

Here are rough savings targets based on how much annual income your portfolio needs to provide.

| Annual Income Needed From Savings | Approximate Savings Needed at 4% | Approximate Savings Needed at 3.5% |

|---|---|---|

| $20,000 | $500,000 | $571,429 |

| $30,000 | $750,000 | $857,143 |

| $40,000 | $1,000,000 | $1,142,857 |

| $50,000 | $1,250,000 | $1,428,571 |

| $60,000 | $1,500,000 | $1,714,286 |

| $80,000 | $2,000,000 | $2,285,714 |

| $100,000 | $2,500,000 | $2,857,143 |

How to Read This Table

The first column is not your total retirement spending. It is the amount your savings need to provide after Social Security, pensions, annuities, or other reliable income are counted.

For example, if you want to spend $90,000 per year and expect $40,000 from Social Security and pensions, your savings need to provide $50,000 per year. That points to roughly $1.25 million to $1.43 million, depending on the withdrawal rate used.

Why the Range Matters

The 4% column assumes a higher starting withdrawal rate. The 3.5% column gives more room for uncertainty, longer life expectancy, lower future returns, or a more cautious retirement plan. As a retired financial planner, guess which one I suggested my clients follow…

- If you retire at 65 with a short life expectancy, low spending, and guaranteed income, a higher withdrawal rate may be reasonable.

- If you retire at 65 with a long family history of longevity, high healthcare costs, and most of your income coming from investments, a lower withdrawal rate may be safer.

What Changes the Answer For You?

Your retirement savings number changes based on several major factors.

Your Social Security Claiming Age

Claiming early may reduce your monthly benefit. Delaying may increase it up to age 70. That changes how much retirement income your portfolio needs to provide.

Your Medicare Costs

Medicare begins at age 65 for most people, but it is not free. CMS announced that the standard Medicare Part B monthly premium is $202.90 in 2026, with higher-income retirees potentially paying income-related monthly adjustment amounts.

- Higher-income retirees should also understand how Medicare calculates IRMAA premium surcharges, because extra retirement income can increase Medicare Part B and Part D costs.

- If your income is near a Medicare surcharge threshold, review the current IRMAA brackets and Medicare surcharges before taking large IRA withdrawals or Roth conversions.

That matters because Medicare premiums, Part D drug costs, Medigap or Medicare Advantage costs, deductibles, and out-of-pocket expenses can materially affect your retirement budget.

Your Income Tax Mix

Your account types matter:

A $1 million Traditional IRA may not give you the same after-tax retirement income as a $1 million Roth IRA, taxable brokerage account, or HSA.

- Traditional IRA / 401(k): Withdrawals are generally taxable as ordinary income, which can affect your tax bracket, Social Security taxation, and Medicare IRMAA.

- Roth IRA: Qualified withdrawals are generally tax-free, giving retirees more flexibility when managing taxable income.

- Taxable brokerage account: Interest, dividends, and capital gains may be taxed differently, so timing and asset location can matter.

- HSA: Withdrawals can be tax-free when used for qualified medical expenses, which may help with retirement healthcare costs.

Why this matters: Retirement readiness should be measured in after-tax income, not just account balances.

A retiree with tax diversification may have more flexibility than a retiree with all savings in pre-tax accounts.

Your Required Minimum Distributions

Required minimum distributions, or RMDs, are mandatory withdrawals from many tax-deferred retirement accounts. IRS guidance says account owners generally must begin annual RMDs when they reach age 73, and the RMD is generally calculated using the prior year-end account balance divided by an IRS life expectancy factor.

- If you want the full rules, deadlines, and planning options, my guide to retirement plan distributions and RMDs explains how IRA and 401(k) withdrawals work in retirement.

- You can estimate future withdrawals with my IRA RMD calculator to see how required distributions may affect your taxable income later in retirement.

- The IRS says RMDs generally begin at age 73, and the amount is usually calculated by dividing the prior December 31 account balance by an IRS life expectancy factor.

Why RMDs exist:

Traditional IRAs and 401(k)s allow workers to delay taxes during their working years. RMDs ensure that tax-deferred money eventually becomes taxable instead of staying sheltered indefinitely.

Why this matters when retiring at age 65:

Your early retirement years may be a planning window. If you retire at 65 but RMDs do not begin until later, you may have several years to manage Roth conversions, taxable withdrawals, charitable giving strategies, and Social Security timing before required withdrawals begin.

That planning window is especially important because a Roth conversion can create an IRMAA tradeoff if the added taxable income lowers future RMDs but raises Medicare premiums today.

Your Housing Situation

A paid-off home can reduce monthly expenses. A mortgage, rent, property taxes, insurance, and maintenance can increase the amount you need saved.

Your Spending Flexibility

Some retirees can reduce travel, dining, or gifting during down markets. Others have fixed expenses that are harder to cut.

Spending flexibility can reduce retirement risk because it gives you more room to adapt when markets or inflation are unfavorable.

Why Your Retirement Number Is Really an Income Gap

Many people ask:

“Can I retire with $1 million?”

A better question is:

“How much income does my $1 million need to produce?”

Example:

Retiree A

- Needs $70,000 per year

- Receives $45,000 from Social Security and pension

- Portfolio must provide $25,000

- $25,000 × 25 = $625,000 estimated need

Retiree A may be comfortable with $1 million.

Retiree B

- Needs $120,000 per year

- Receives $30,000 from Social Security

- Portfolio must provide $90,000

- $90,000 × 25 = $2,250,000 estimated need

Retiree B may find $1 million too low.

Same portfolio. Different income gap. That is the key message I want you to walk away from with this article. This is my 30 years of experience talking. And thousands of retiree’s I have seen and worked with.

Common Mistakes I’ve Seen When Estimating Retirement Needs at 65 years Young

Common Mistake 1: Using Gross Income Instead of Spending

Why it matters:

Your paycheck is not the same as your lifestyle cost. Retirement planning should start with what you spend, not what you earn.

Better approach:

Build a retirement budget using housing, food, insurance, healthcare, transportation, taxes, travel, gifts, and emergency expenses.

Common Mistake 2: Forgetting Taxes on IRA and 401(k) Withdrawals

Why it matters:

A $60,000 withdrawal from a Traditional IRA may not give you $60,000 to spend after federal and state taxes.

Better approach:

Estimate retirement income after taxes, not before taxes.

Common Mistake 3: Assuming Medicare Covers Everything

Why it matters:

Medicare does not eliminate healthcare costs. Premiums, deductibles, copays, dental, vision, hearing, prescriptions, and long-term care may still require planning. Because Medicare generally does not solve every long-term care risk, retirees should also consider whether long-term care insurance belongs in their retirement income plan.

Better approach:

Include Medicare premiums, supplemental coverage, prescription drug costs, and out-of-pocket healthcare expenses in your retirement budget.

Common Mistake 4: Ignoring the Years Before RMDs

Why it matters:

The years between retirement and RMD age can be valuable tax-planning years. If income is temporarily lower, retirees may have room for Roth conversions or strategic IRA withdrawals.

Better approach:

Map the years from 65 to RMD age before deciding when to claim Social Security or how much to withdraw from each account.

Common Mistake 5: Treating the 4% Rule as a Guarantee

Why it matters:

Market returns, inflation, retirement length, and spending patterns can all change the safe withdrawal amount. Your withdrawal plan should also match your asset allocation for retirees, because portfolio risk affects how much income your savings can safely support.

Better approach:

Use the 4% rule as a starting estimate, then stress-test your plan with lower returns, higher inflation, longer life expectancy, and unexpected healthcare costs.

Decision Framework to help You Decide if You Can You Retire at 65 or Not?

Retiring at 65 May Be Reasonable If:

- Your essential expenses are covered by Social Security, pensions, or conservative portfolio withdrawals

- You have a clear healthcare plan through Medicare and supplemental coverage

- You understand your tax situation

- You have emergency reserves outside retirement accounts. Those reserves matter because a strong emergency fund or cash reserve can help you avoid selling investments during a market downturn.

- Your withdrawal rate is sustainable

- You have a plan for inflation and market downturns

- You know when you will claim Social Security

- You have considered long-term care risk

- You have coordinated your plan with your spouse, if married

Retiring at 65 May Be Risky If:

- You do not know your annual spending

- Your portfolio must cover most or all expenses

- You still carry high-interest debt

- You plan to claim Social Security early only because savings are low

- You have not budgeted for Medicare and healthcare costs

- Your withdrawal rate is above 5% with little flexibility

- You have no plan for taxes on IRA or 401(k) withdrawals

- You are assuming strong investment returns to make the plan work

A Simple Retirement Readiness Worksheet

Use this worksheet to estimate your number.

Fill in each line to estimate how much you may need saved to retire at 65. The key number is your portfolio income needed — the amount your savings must provide after Social Security, pensions, and other reliable income are counted.

| Step | Question | Your Number |

|---|---|---|

| 1 | Annual retirement spending goal | |

| 2 | Expected annual Social Security | |

| 3 | Expected annual pension or annuity income | |

| 4 | Other reliable income | |

| 5 |

Portfolio income needed Step 1 − Step 2 − Step 3 − Step 4 |

|

| 6 |

Multiply by 25 for 4% estimate Step 5 × 25 |

|

| 7 |

Multiply by 28.6 for 3.5% estimate Step 5 × 28.6 |

Annual spending − Social Security − pension or annuity income − other reliable income = portfolio income needed

Portfolio income needed × 25 to 28.6 = estimated retirement savings target

Worksheet Formula

Annual spending − Social Security − pension or annuity income − other reliable income = portfolio income needed

Portfolio income needed × 25 to 28.6 = estimated retirement savings target

Example: Couple Retiring at 65

Assume a married couple wants to spend $95,000 per year in retirement.

They expect:

- $48,000 from Social Security once both claim

- No pension

- $10,000 per year from part-time consulting for the first three years

- $1.2 million in retirement and brokerage accounts

Their long-term portfolio annual income need is:

$95,000 - $48,000 = $47,000 per year

Using the 4% rule:

$47,000 ÷ 0.04 = $1,175,000

At first glance, $1.2 million may be enough. But context matters.

They still need to evaluate:

- Whether they are claiming Social Security at 65 or later

- How Medicare premiums fit into the budget

- Whether withdrawals come from Traditional IRA, Roth IRA, or brokerage accounts

- Whether future RMDs will increase taxable income

- Whether one spouse would be financially secure if the other dies

- Whether they have enough cash reserves for market downturns

The portfolio number looks close, but the retirement decision depends on income timing, taxes, healthcare, and survivor planning.

The Retirement Ripple Effect

Retiring at 65 does not only affect your paycheck. It can also affect taxes, Social Security, Medicare, Roth conversion planning, investment withdrawals, estate planning, and your spouse’s future income.

Here is the Michael Ryan Money Retirement Readiness System:

Retiring at 65 does not just change your paycheck. It can create a chain reaction across your taxable income, Social Security decision, Medicare premiums, future RMDs, and after-tax retirement income.

Age 65 may start the retirement decision, but it also affects Medicare timing, Social Security claiming, and how soon your portfolio must provide income.

Paychecks may shrink or disappear, which changes your annual cash flow and may lower taxable income temporarily.

Savings may need to replace the income gap after Social Security, pensions, annuities, or other reliable income are counted.

Withdrawals from Traditional IRAs and 401(k)s are generally taxable, while Roth IRA and taxable brokerage withdrawals may be treated differently.

Claiming earlier may reduce your monthly benefit, while delaying may require your portfolio to cover more spending for a few years.

Higher modified adjusted gross income can increase Medicare Part B and Part D premiums through IRMAA.

Required minimum distributions can force taxable withdrawals later, which may affect taxes, Medicare premiums, and Roth conversion planning.

The final result is not just how much you withdraw, but how much income you actually keep after taxes and healthcare-related costs.

Bottom line: “How much do I need to retire at 65?” is not just a savings question. It is a retirement income planning question.

This is why “how much do I need to retire at 65?” is not just a savings question. It is a retirement income planning question.

Before retiring at 65, answer these questions:

- What will I spend each year?

- How much guaranteed income will I have?

- When will I claim Social Security?

- What will Medicare and supplemental coverage cost?

- Which accounts will I withdraw from first?

- How much of my retirement income will be taxable?

- What is my expected withdrawal rate?

- What happens if the market drops early in retirement?

- What happens if I live into my 90s?

- What happens financially if my spouse outlives me? Married couples should also review Social Security survivor benefits, because one spouse’s claiming decision can affect the income available to the surviving spouse.

- Will RMDs create future tax issues?

- Do I have a plan for long-term care?

If you can answer those questions clearly, you are much closer to knowing whether you can retire at 65.

FAQs About Retiring at 65

Can I retire at 65 with $1 million?

You may be able to retire at 65 with $1 million if your spending is moderate, you have Social Security or pension income, your healthcare costs are manageable, and your withdrawal rate is sustainable. If your portfolio must provide most of your income, $1 million may not be enough.

Is $500,000 enough to retire at 65?

$500,000 may be enough for some retirees with low expenses, strong Social Security benefits, no debt, and a modest lifestyle. Using a 4% withdrawal guideline, $500,000 provides about $20,000 per year before taxes.

How much monthly income will I need in retirement?

Many retirees start by estimating 70% to 85% of pre-retirement income, but actual spending is more important. A retiree with a paid-off home may need less. A retiree with high healthcare, travel, or housing costs may need more.

Should I claim Social Security at 65?

Not automatically. Age 65 is important for Medicare, but it may be before your Social Security full retirement age. Claiming before full retirement age can reduce your monthly benefit, while delaying can increase it up to age 70.

What is the biggest hidden cost of retiring at 65?

Healthcare and taxes are two of the biggest hidden costs. Medicare has premiums and out-of-pocket expenses, and withdrawals from Traditional IRAs and 401(k)s are generally taxable. Higher income can also affect Medicare IRMAA premiums.

What is the best age to retire?

The best age to retire depends on your savings, health, work satisfaction, Social Security strategy, healthcare coverage, spouse, taxes, and retirement goals. Age 65 works for some people, but others may benefit from working longer, retiring gradually, or delaying Social Security.

Final Answer: How Much Do You Need to Retire at 65?

A reasonable estimate is that many people need somewhere between $750,000 and $2 million or more to retire at 65, depending on spending, Social Security, pensions, taxes, healthcare, and lifestyle.

But the most useful retirement readiness formula is:

Annual spending - guaranteed income = portfolio income gap

Portfolio income gap ÷ safe withdrawal rate = retirement savings needed

- If your savings only need to produce $30,000 per year, you may need around $750,000 to $857,000.

- If your savings need to produce $60,000 per year, you may need around $1.5 million to $1.7 million.

- If your savings need to produce $100,000 per year, you may need around $2.5 million to $2.9 million.

The right number is not the biggest number you can find online. It is the amount that can support your actual spending after Social Security, Medicare, taxes, inflation, and investment risk are included.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.