As a financial planner with almost 3 decades of experience, I’ve seen few things cause more anxiety than the dense jargon of Social Security. The “Social Security 5-Year Rule” is a perfect example.

Clients come to me confused, worried, and unsure if they qualify for the benefits they’ve paid into their entire working lives.

The confusion is understandable because the “Social Security 5-Year Rule” isn’t one rule. It’s a term people use for three different, crucial provisions that affect you at different stages of the disability process.

I understand you may be facing mounting bills while unable to work—let’s cut through the confusion so you can take the right next steps. This guide will provide the clarity you’re looking for, breaking down each rule so you can identify exactly which one applies to your situation.

In Plain English: The “5-Year Rule” Problem

This is what it is: A confusing term people use to describe three different Social Security rules.

This is what it means to you: You might be searching for an answer to one question but finding information about another, which causes stress and confusion.

This is what you need to do: Figure out which situation below describes you best to find the “5-Year Rule” that actually applies to you.

I’ve seen Maria’s SSDI claim denied for lack of credits—then reinstated within days after filing EXR.

A Story of Two Applicants

Last month, I spoke with two people in nearly identical situations. “John,” a 53-year-old landscaper, was denied benefits because he’d been out of the workforce for six years and his “disability insurance” had lapsed. “Maria,” a 48-year-old who had been on disability before, was able to get provisional benefits started in just 21 days. The only difference? Maria understood a crucial provision called Expedited Reinstatement. These rules matter, and knowing which one applies to you can change everything.

Key Takeaways Ahead

Key Takeaways: The Three “5-Year Rules”

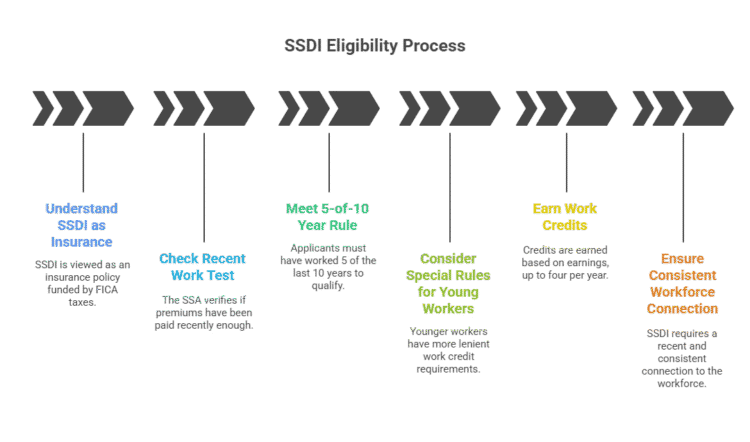

- For New Applicants (The Recent Work Test): This rule determines if you’re eligible to apply for SSDI in the first place. You generally must have worked for 5 of the last 10 years.

- For Re-Applicants (Expedited Reinstatement): This is a safety net that allows you to get back on benefits quickly if your disability returns within 5 years of stopping work.

- For Current Beneficiaries (The Work Safety Net): This refers to the 5-year (60-month) window used to track your Trial Work Period months, allowing you to test your ability to work without losing benefits.

Rule #1: The Recent Work Test – How Do You Qualify for SSDI in the First Place?

Think of Social Security Disability Insurance (SSDI) as an insurance policy you pay for with every paycheck via FICA taxes. To make a claim, your policy needs to be active.

The “Recent Work Test” is how the Social Security Administration (SSA) checks if you’ve paid your premiums recently enough to be covered.

In Plain English: The Recent Work Test

This is what it is: A test to see if you’ve worked recently enough (usually 5 of the last 10 years) to be covered by SSDI.

This is what it means to you: If you haven’t worked much in the past decade, you might not qualify for SSDI, even with a severe disability. Your work history is just as important as your medical condition.

This is what you need to do: Go to the SSA.gov website and check your official work history to see if you have enough “work credits.”

What is the “5-of-10” Year Work History Requirement?

In July 2025, I worked with “John,” a landscaper who hadn’t worked for over five years. We discovered he’d missed the 5-of-10-year work credit window, and even though his lung disease was severe, he couldn’t qualify for SSDI without backdating his Alleged Onset Date.

⚠️ Here’s a contrarian twist: some claimants find a qualifying job within the final months of that 10-year lookback, just to get covered again. They’re essentially buying insurance with a paycheck.

The SSA’s most recent actuarial report shows nearly 30% fewer approvals for applicants with gaps exceeding 5 years.

So the real question is: did you let your SSDI “insurance policy” lapse before you knew you needed it?

What if I’m Under 31? (Special Work Credit Rules)

The “5-of-10” rule primarily applies to workers aged 31 and older. The SSA has special, more lenient rules for younger workers who haven’t had as much time to build a work history:

- If you are under age 24, you may qualify with just 6 credits earned in the 3-year period before your disability began.

- If you are age 24 to 31, you may qualify if you have work credits for at least half the time between age 21 and the time you become disabled.

These exceptions are critical and ensure younger individuals are not unfairly excluded from the SSDI program.

What is a work credit?

A Work Credit is the building block of your Social Security eligibility. In 2026, you earn one work credit for every $1,890 in earnings (up from $1,810 in 2025), up to a maximum of four credits per year.

This requirement ensures SSDI helps those who have a recent and consistent connection to the workforce, distinguishing it from Supplemental Security Income (SSI), which is a needs-based program.

Why Your Disability Onset Date is Critical

The date you officially claim your disability began (your Alleged Onset Date) is the starting point for the 10-year lookback period.

This date is critical because it determines your Date Last Insured (DLI). Aka the last day you are covered by the SSDI “insurance policy.” You must prove your disability began on or before your DLI to be eligible.

Special Considerations for Mental Health Conditions

It’s a difficult truth that SSDI claims for mental health conditions like severe depression, anxiety, or PTSD can be more challenging to prove. However, they absolutely qualify.

The key is demonstrating how your condition functionally limits your ability to perform work-related tasks.

The SSA reports that a significant percentage of working-age SSDI recipients have mental conditions, so you are not alone.

Success hinges on thorough medical evidence from a psychologist or psychiatrist that details your work limitations.

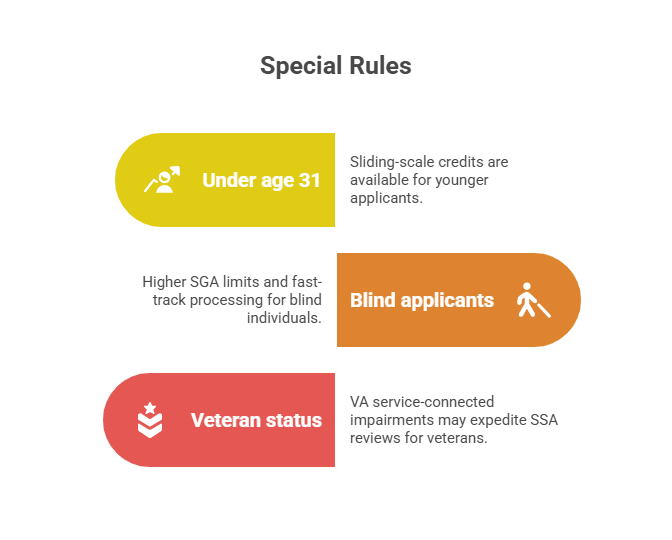

Special Rules: Under‑31, Blind, Veteran Applicants

- Under age 31: sliding-scale credits (e.g. 6 credits in 3 years if under 24)

- Blind applicants: higher SGA limits & fast-track

- Veteran status: VA service-connected impairments may earn expedited SSA reviews

Rule #2: Expedited Reinstatement (EXR) – How Can You Get Back on Benefits Fast?

Expedited reinstatement (EXR) is the rule that offers a powerful safety net for those who have improved, returned to work. But find they are unable to continue due to the same disability.

In Plain English: Expedited Reinstatement

This is what it is: A “fast pass” to get back on disability benefits if you were on them before, tried to work, and had to stop again within 5 years.

This is what it means to you: You can likely skip the long, stressful initial application process and the five-month waiting period for payment.

This is what you need to do: If this describes your situation, contact the SSA immediately and use the specific term “Expedited Reinstatement (EXR).”

Who is Eligible for Expedited Reinstatement?

You can request EXR if you meet these conditions:

- Your previous SSDI benefits ended because you were working and earning above the Substantial Gainful Activity (SGA) limit.

- You are unable to work again due to the same or a related medical condition.

- You make the request within 5 years (60 months) from the month your benefits stopped.

A Client’s Story: Maria’s “Tactical Reset”

In April 2025, “Maria,” a former client, returned to her job only to find her spine flaring up again two years later. Because we filed for Expedited Reinstatement (EXR) within the five-year deadline, she skipped the five-month waiting period and started receiving provisional benefits within 21 days. EXR isn’t just a safety net—it’s a tactical reset button. Many advocates don’t even mention provisional benefits, but that early support can mean paying rent instead of going into debt. Under an updated POMS rule, EXR now allows up to six provisional months even if earnings exceed SGA in some cases—an allowance absent from other guides.

What Are the Benefits of Using EXR?

The advantages are significant:

- No New Application: You do not have to fill out a full, new disability application.

- Skip the Waiting Period: You bypass the standard five-month waiting period for new applicants.

- Provisional Benefits: You can receive up to six months of temporary benefits while the SSA reviews your case to confirm your disability still meets their rules.

Rule #3: The Work “Safety Net” – How Can You Try Working While on SSDI?

The SSA provides work incentives to encourage beneficiaries to test their ability to work without immediately losing their benefits. This is where the third “5-year” concept comes into play.

What is the Trial Work Period (TWP)?

The Trial Work Period (TWP) allows you to test your ability to work for up to 9 months while receiving your full SSDI check.

My Boston client, “Hannah,” used up 3 TWP months teaching seasonally. Because SSDI uses a 60-month rolling window, she can try working again later without issue.

Here’s a detail others often miss: after someone reinstates benefits via EXR, a new TWP countdown begins just 24 months later, per a late 2024 SSA policy change. A crucial nuance for anyone planning a return to work.

In Plain English: The Work Safety Net

This is what it is: A 9-month “safety net” that lets you try going back to work while still receiving your full disability check, no strings attached.

This is what it means to you: You can test your ability to work without the immediate fear of losing your only source of income and your Medicare coverage.

This is what you need to do: Understand how the SSA counts these 9 months (it’s complicated) so you can use them strategically if you feel able to work again.

What Happens After the TWP? The EPE and 2026 SGA Limits

After you use your 9 TWP months, you enter a 36-month Extended Period of Eligibility (EPE).

During the EPE, you will still receive your SSDI check for any month your earnings fall below the Substantial Gainful Activity (SGA) level.

- 2026 SGA Limits:

- $1,690 per month for non-blind individuals

- $2,830 per month for blind individuals

Furthermore, your Medicare coverage continues for at least 93 months (over 7 years) after your TWP ends, even if your cash benefits stop due to work.

At a Glance: How to Compare the Three “5-Year Rules”

In June 2024, the SSA finalized a rule change that significantly helps many applicants. They have reduced the period they look at for your past relevant work (PRW) evaluation from 15 years down to 5 years. This is a major development. It means that an older, physically demanding job you did a decade ago is less likely to be used as a reason to deny your claim that you can no longer perform work. You can read about this update directly on the SSA’s official blog.

This means that older jobs you may have held are less likely to be used as a reason to deny your claim, which is a major positive development for many people applying today.

A Critical Update for 2025: The “Past Relevant Work” Rule Change

| Rule Type | Who It’s For | 2025What It Does | Key Detail for 2026 |

|---|---|---|---|

| Recent Work Test | New Applicants | Determines your initial eligibility to apply for SSDI. | You must have worked at least 5 of the last 10 years before your disability began. |

| Expedited Reinstatement (EXR) | Past Beneficiaries | Lets you restart benefits quickly without a new application. | You must apply within 5 years of when your benefits stopped due to work. |

| Trial Work Period (TWP) | Current Beneficiaries | Gives you 9 months to test your ability to work while getting full benefits. | The 9 months are tracked within a rolling 5-year (60-month) window. |

Frequently Asked Questions (FAQ) About the 5 Year Disability Rule

Does the 5-Year Rule apply to SSI?

No. The “Recent Work Test” does not apply to Supplemental Security Income (SSI). SSI is a needs-based program and is not dependent on your work history. Expedited Reinstatement rules, however, are similar for SSI.

Is it harder to qualify for SSDI with a mental health condition?

It can be more challenging because the limitations are not always as visible as physical impairments. Success depends on detailed medical records from a psychiatrist or psychologist that clearly link your symptoms to functional limitations preventing you from sustaining work.

I was denied SSDI before. Can I apply again?

Yes, you can reapply, especially if your condition has worsened or if you have new medical evidence. The recent SSA rule changes regarding past relevant work may also help your case. It is often wise to consult with a disability representative to review your denial and plan your new application.

Do I Need a Lawyer to Apply For SSDI?

While you are not required to have a lawyer, statistics show that applicants who are represented have a higher rate of approval, particularly at the appeals stages. An experienced representative can help ensure your application is complete and accurately reflects the severity of your condition.ply for SSDI?

Does military service count toward SSDI work credits?

Yes. If you served in the military, you paid Social Security taxes just like civilian employees, and you earned work credits for your service. Additionally, veterans may be able to receive expedited processing of their disability claims under certain circumstances.

I was denied SSDI before. Can I apply again?

Yes, you can reapply, especially if your condition has worsened or if you have new medical evidence. The recent SSA rule changes regarding past relevant work may also help your case. It is often wise to consult with a disability representative to review your denial and plan your new application.

What Are Your Next Steps?

Understanding these rules is the first step toward taking control of your financial future. The Social Security system is complex, but it has provisions designed to protect you.

Your most powerful move is to be proactive. Go to the official SSA.gov website and review your earnings record to confirm you meet the work history requirements. If you believe you qualify for Expedited Reinstatement, contact the SSA directly.

Ready to see where you stand? Download our free SSDI Eligibility Checklist. It’s a simple tool I developed to help you quickly assess if you meet the basic requirements before you start the application process.

- If you have other assets, it’s also critical to understand Special Needs Trust rules to ensure you don’t accidentally disqualify yourself from benefits.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.