Deciding when to start collecting your Social Security retirement benefits is one of the most consequential financial choices you will ever make.

After guiding hundreds of clients through this labyrinth, I’ve seen how the right decision can add tens of thousands of dollars to your lifetime income, while a hasty choice can lead to lasting regret.

The internet is filled with myths and one-size-fits-all advice. My goal here is different.

I’m going to give you the same in-depth, personalized framework I used with my clients, grounded in decades of experience and aligned with official guidance from the Social Security Administration (SSA). We’ll move beyond generic formulas to focus on what truly matters: your unique personal factors.

Step 1: Understand the Three Key Ages Of Social Security Income (62, FRA, and 70)

Your entire claiming decision revolves around three milestone ages. The choice you make sets your base benefit for life, only adjusted by annual Cost-of-Living Adjustments (COLAs).

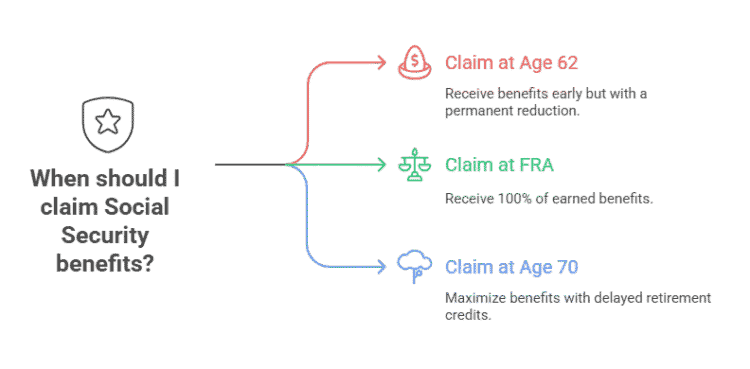

Claiming at Age 62 (The Earliest Option):

You can start receiving checks as early as age 62, but your monthly benefit will be permanently reduced by up to 30% compared to what you’d get at your Full Retirement Age.

Claiming at Full Retirement Age (FRA):

This is the age at which you are entitled to 100% of your earned benefit. Your FRA is between 66 and 67, depending on the year you were born.

Claiming at Age 70 (The Maximum Option):

For every year you delay claiming past your FRA, you earn delayed retirement credits that increase your benefit by about 8% per year. By waiting until age 70, your monthly check will be 24-32% larger than your FRA benefit.

Social Security Claiming-Age Comparison Engine

Compare claiming ages using your own Social Security estimates, calculate simple crossover ages, and identify household issues that the dollar comparison alone cannot answer.

Social Security Comparison Results

Cumulative benefit comparison

| Planning age | Claim at 62 | Claim at FRA | Claim at 70 | Highest in this simple comparison |

|---|

Pairwise crossover estimates

Decision factors the math does not settle

Questions to resolve before filing

Official verification

Did You Receive Extra Money From Social Security This Month?

Step 2: Get Your Personal Social Security Benefit Estimate

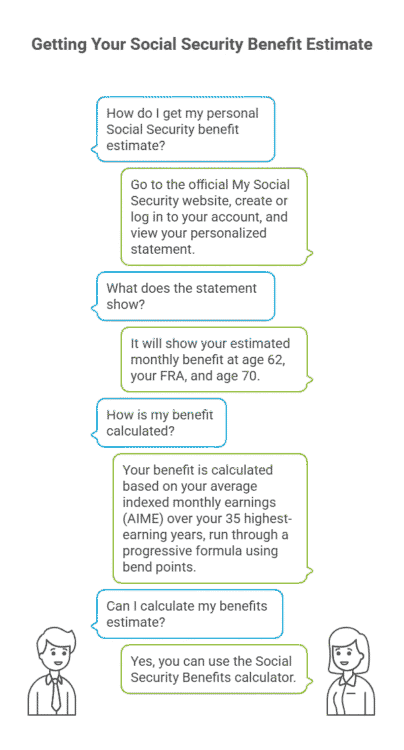

Before you can make a decision, you need your numbers. The Social Security Administration provides an indispensable tool for this.

- Go to the official My Social Security website.

- Create or log in to your account.

- View your personalized statement.

It will show your estimated monthly benefit at age 62, your FRA, and age 70.

The Social Security Benefit Statement is the foundation of your entire analysis.

Your benefit is calculated based on your average indexed monthly earnings (AIME) over your 35 highest-earning years, run through a progressive formula using bend points.

While the math is complex, your statement gives you the final, actionable numbers.

You can use the Social Security Benefits calculator to determine your benefits estimate

Step 3: Find Your “Break-Even” Age

The break-even analysis is a critical calculation. It answers the question: “How long do I have to live for the higher payments from delaying to make up for the years of payments I gave up?“

For most people, the break-even age is typically between 78 and 82.

If you live past this age, delaying your claim results in a higher total lifetime benefit.

If you don’t, claiming early would have been the better financial choice.

Step 4: Consider Your Personal Factors (This is The Most Important Step)

The math from the break-even analysis is just a starting point. In my 25 years of experience, the right decision always comes down to these personal factors.

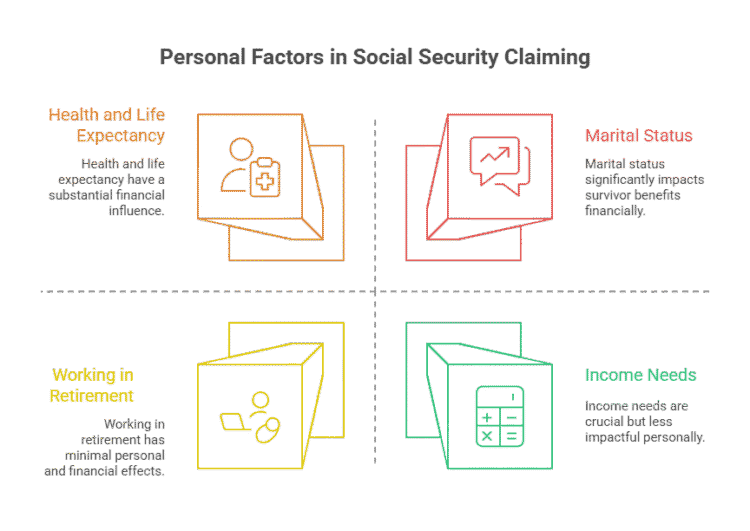

Health and Life Expectancy:

Be honest with yourself. If you have chronic health issues or a family history of shorter lifespans, claiming early is often the right call. If you are in excellent health and have longevity in your genes, delaying becomes much more powerful.

Income Needs:

Do you need the money to cover essential expenses? If you’ve been forced into an early retirement, claiming at 62 can be a crucial lifeline. If you have other income sources like a pension, an annuity, or a sufficient investment portfolio, you have the flexibility to delay.

Marital Status (Spousal & Survivor Benefits):

This is the most overlooked factor for couples. The higher earner’s decision dramatically impacts the survivor benefit for the spouse who lives longer. Often, the optimal strategy is for the higher earner to delay until 70 to maximize this potential survivor benefit, even if it means the lower earner claims earlier.

Working in Retirement:

If you claim benefits before your FRA and continue to work, your benefits can be temporarily reduced if your earnings exceed a certain annual limit.

Tax Implications:

Up to 85% of your Social Security benefits can be subject to federal income tax, depending on your “provisional income.” Delaying benefits can sometimes help you manage your tax bracket in the early years of retirement.

Step 5: Making the Final Decision on When To Start Receiving Your Social Security Income

So, should I claim Social Security at 62 or wait until 70?

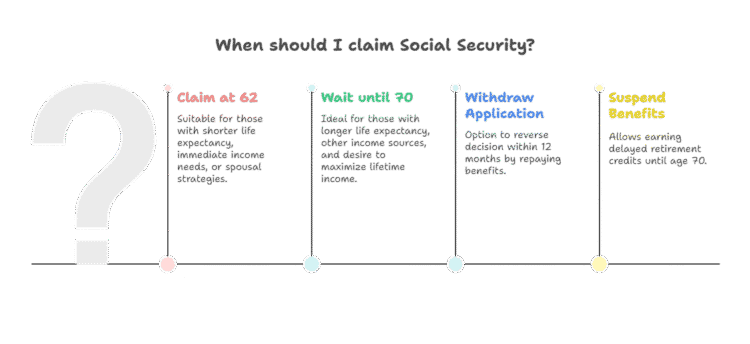

Claim at 62 if:

You have a shorter life expectancy, you need the income immediately, or it enables a crucial spousal strategy.

Wait until 70 if:

You have a longer life expectancy, you have other sources of income, and you want to maximize your inflation-protected lifetime income and the potential survivor benefit for your spouse.

What If I Change My Mind?

You have two main options if you regret your claiming decision:

- Withdraw Your Application:

You can do this only once and only within the first 12 months of claiming. You must repay all the benefits you and your family received. - Suspend Your Benefits:

Once you reach your FRA, you can voluntarily suspend your payments. You can then earn delayed retirement credits until you restart your benefits, up to age 70.

Related Reading You Might Enjoy

Now, try searching for: spousal benefits, retirement income planning, or what is a good monthly retirement income.

Final Verdict: The Best Choice is an Informed One

There is no single “right” answer for when to take Social Security. The optimal choice is the one that is made thoughtfully, based on a clear understanding of the rules and an honest assessment of your personal situation. By following these five steps, you can move from a state of anxiety to one of confidence, knowing you have made the best possible decision for your financial future.

For more, read my Comprehensive Retirement Planning Guide.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.