“What is a good monthly retirement income” or “How much do I need to retire?” – these are questions, often clouded with uncertainty, that loom large in the minds of many pre-retirees and recent retirees.

You’ve likely arrived here seeking a precise figure, a definitive dollar amount for a comfortable retirement. But, as a retired financial planner with nearly three decades of experience, I can tell you that the answer is far from one-size-fits-all. Each person’s journey to retirement is as unique as their financial story.

Drawing from my extensive background in financial planning, I’ve assisted countless individuals in navigating the complexities of retirement income.

This experience has equipped me with real-world insights into what constitutes a ‘good‘ retirement cash flow, tailored not just to numbers but to lifestyles, aspirations, and personal circumstances.

In this article, we will explore key issues such as retirement income sources (pension funds, annuities, social secuirty benefits, 401k and IRA withdrawls), lifestyle choices, and living expenses, breaking down these concepts into understandable bites of info. We’ll discuss how factors such as inflation and geographical location impact your retirement planning as well.

I’ll guide you through understanding your retirement needs, aligning your income sources, and managing your expenses.

My goal? To provide you with the knowledge and confidence to answer the pivotal question: “What is a good monthly income for retirement?”

Quick Answers: What is a Good Monthly Retirement Income in 2026?

- Defining “Good” Retirement Income: The ideal income in retirement varies per individual, factoring in lifestyle, expenses, and personal aspirations. While general guidelines suggest targeting 70-80% of your pre-retirement income, this figure should be tailored to your unique circumstances, hinting at deeper financial nuances detailed in this article.

- Income Sources and Expense Management: It’s crucial to understand and align your income sources such as Social Security, pensions, and personal savings with your retirement expenses. This includes budgeting for healthcare, housing, leisure, and essential daily needs. We delve deeper into how to effectively manage these elements throughout your retirement.

- Geographical and Inflation Considerations: The cost of living and inflation rates are significant factors influencing your target income in retirement. These variables differ by location and over time, underscoring the need for adaptable financial strategies, which are explored in the subsequent sections of the article.

- Lifestyle and Personal Preferences: Your retirement lifestyle choices – travel, hobbies, relocation plans – play a pivotal role in determining your income needs. This article provides insights on how to align your financial planning with these personal preferences, ensuring a fulfilling retirement journey.

Wondering how these factors apply to your retirement plan? Do you have enough money to retire at age 65? Dive into the heart of the article where we unpack each aspect, offering you tailored advice and actionable strategies. Discover how to craft a retirement income that not only meets your needs but enriches your golden years

Jump To: What Is a Good Retirement Income or Average Retirement Income?

So, What is Considered a Good Monthly Retirement Income?

As a financial planner who has helped thousands of clients plan for retirement over my career, one of the most common questions I got asked is “What monthly income should I target in retirement?”

Strategic retirement planning requires careful budgeting across four key expense categories. Understanding average spending patterns for healthcare, housing, leisure, and essentials helps you allocate resources effectively and maintain a comfortable lifestyle throughout retirement. Proper planning ensures your savings stretch further and cover unexpected costs.

| Expense Categories | Average Annual Spending | Notes and Tips |

|---|---|---|

| Healthcare | Varies, often increases | Plan for more than current healthcare costs; consider Medicare coverage and supplemental plans. |

| Housing | Depends on location | Costs can vary greatly by state and lifestyle choices; consider downsizing or relocating to a more affordable area. |

| Leisure Activities | Personal discretion | Allocate funds for hobbies, travel, and other activities to ensure a fulfilling retirement. |

| Essentials | Based on lifestyle | Includes groceries, utilities, and other daily necessities. |

Start building your retirement budget today by categorizing your expected expenses and adjusting allocations based on your priorities and lifestyle goals.

As I mentioned earlier, there is no one-size-fits-all answer, as many personal factors influence your ideal income target. However, I will provide you with my professional experience, researched guidelines, and expert planning perspectives to help you in setting a monthly retirement budget tailored to your needs.

- Are you wondering if you can Live on $4,000 a Month in Retirement? Read the article and find out…

Defining a Good Monthly Retirement Income For Your Unique Lifestyle

Again, desired retirement living standars varies from person to person. It’s the income that allows you to maintain your desired lifestyle and cover essential expenses without constantly worrying about finances. Rather than focusing on an arbitrary number, it’s about aligning your income with your retirement goals.

An often-cited rule of thumb suggests aiming for 70-80% of your pre-retirement income. However, this can change based on your circumstances and expectations.

Comprehensive retirement planning requires evaluating three critical areas: understanding your spending patterns before and after retirement, analyzing all income sources to bridge any gaps, and for couples, coordinating household finances strategically. These foundational elements ensure your retirement income aligns with your lifestyle goals and protects against financial shortfalls.

| Topic | Key Points |

|---|---|

| Examine Current and Future Spending | Analyze current household expenses. Consider changes post-retirement. Account for future costs like healthcare. Include one-time expenses such as travel or home renovations. |

| Income Sources Analysis | Calculate guaranteed income from Social Security, pensions, and annuities. Compare with expenses to identify gaps. Plan for taxes and unexpected costs. |

| For Couples: Coordinating Retirement Plans | Combine incomes and consider tax implications. Account for Social Security benefits for each spouse. Adjust budget for shared expenses. Set a target income based on pre-retirement earnings, lifestyle, and location. |

Take action now: evaluate each of these three planning dimensions to create a retirement strategy tailored to your unique financial situation and goals.

Some more retirement planning articles that will be helpful for you to read today:

- Michael Ryan Money Retirement Planning Guide

- How To Plan For Retirement by The Experts

From A Financial Planner’s Perspective

- From my experience, the key to a comfortable retirement is not hitting a numerical target but aligning your income with your lifestyle and needs.

- Diversifying income sources is crucial. I recall a client who solely relied on Social Security and faced financial strain; this could have been mitigated with a more varied income plan.

- Determining your comfortable living standards is a process unique to each individual. It requires a deep dive into your personal finances, lifestyle aspirations, and a strategic approach to bridging income and expense gaps.

- Regular reviews with a financial advisor can ensure your retirement plan remains aligned with your evolving needs and goals.

Learn more about Social Security by reading these articles today:

- Social Security Survivor Benefits

- When you can expect to receive your Social Security Checks

- or are you wondering why you received extra Social Security money this month?

Determining Your Retirement Income Needs – A Client Example

As a retired financial planner, I regularly helped clients tackle this complex question. While numbers and data provide starting guidelines, arriving at your answer requires understanding your complete financial picture.

When Lauren first scheduled a consultation, retirement was just 3 years away. She was concerned whether her retirement income sources would sustain the lifestyle she hoped to maintain.

We meticulously reviewed her fixed monthly streams – Social Security benefits, a small pension, annuity payments. We estimated taxes and built a realistic budget, factoring in higher healthcare costs in the future and plans to travel more.

The initial math showed a sizable gap between essential expenses and Lauren’s reliable income. This shortfall is what needed to be supported through withdrawals from her retirement savings.

- The following article can help you if you feel you are in a similar situation Lauren was in: Are You Savings Enough?

- Learn about variable annuity pros and cons, as well as fixed annuity pros and cons here

However, sustainable withdrawal rates vary greatly based on portfolio composition, time horizon, and risk tolerance.

By diving into all aspects of Lauren’s financial situation, we tailored both an appropriate withdrawal rate and asset allocation for her investments to produce the “retirement paycheck” she required. The insight and confidence gained from this personalized plan helped Mary immensely in transitioning to a rewarding retired life.

Key Factors Influencing Retirement Income Requirements

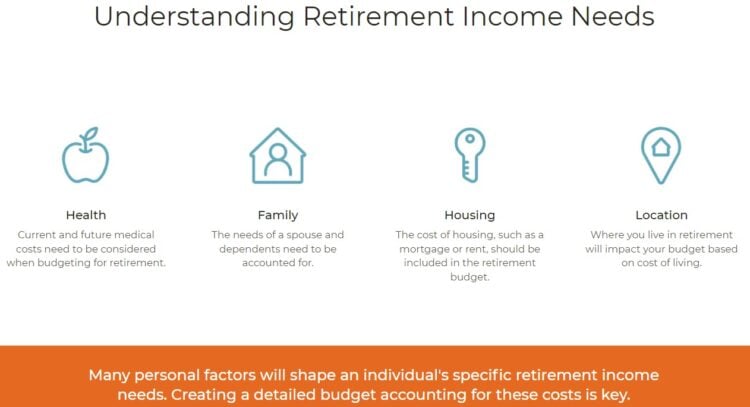

As I touched upon a little earlier, several factors affecting your retirement income requirements. These include your health, family situation, housing choices, and location. For instance, living in an expensive city might require a larger income compared to retiring in a more affordable region. Additionally, as we consider these factors, it’s important to acknowledge the looming baby boomer retirement crisis, which could strain social security systems and necessitate larger personal savings.

Building a realistic retirement budget requires detailed analysis of your current spending patterns and thoughtful projections about how expenses will evolve. By tracking actual costs, anticipating shifts in major expense categories, and accounting for both one-time outlays and discretionary priorities, you create a comprehensive financial roadmap that supports your retirement lifestyle while protecting against unexpected shortfalls.

| Topic | Key Points |

|---|---|

| Build a Detailed Picture of Current Costs | Thoroughly record all household spending over 3-6 months. Categorize every expense. Be comprehensive as it informs your future budget. |

| Project How Expenses Might Shift | Expect some costs to decrease (commuting, work wardrobes). Plan for higher health insurance premiums and aging-related expenses. Consider early retirement travel. |

| Account for Large Future Outlays | Factor in big-ticket expenses (vehicle, home repairs, vacation properties, medical procedures). Leave room for surprises. |

| Understand Impact of Relocating | Research expenses in potential lower-cost retirement areas. Regional differences affect your budget. |

| Pinpoint Discretionary Priorities | Identify important discretionary categories (hobbies, entertainment, charitable causes, family gifts, inheritance). Quantify and incorporate into your budget. |

Complete your budget analysis now by documenting current spending patterns and projecting realistic monthly income needs—this foundation determines whether your retirement savings will sustain your desired lifestyle.

Retirement income needs depend on several key factors:

- Current income – We already discussed trying to replaceme 70-80% of your current pre-retirement income. For example, a couple earning $100,000 per year would aim for $70- $80,000 annual stream of income. This benchmark accounts for assumed decreased expenses and taxes in retirement.

- Desired retirement lifestyle – Your desired activities, travel plans, and hobbies impact income needs. Budgeting for your envisioned lifestyle is crucial.

- Healthcare costs in retirement – Healthcare expenses are likely to rise significantly as you age. Budgeting an extra $300,000+ in retirement per couple is realistic.

- Inflation – This erodes purchasing power over a 30-year retirement timeframe. Budget for at least 3% annual inflation.

- Location – Where you live and any plans to relocate affect expenses. Research costs in regions you are considering.

What Are Some Reasonable Assumptions When Planning For Retirement?

Making reasonable assumptions is crucial when retirement planning:

- Life Expectancy – Assume at least age 90, especially for married couples. Plan for longer if you have longevity genes.

- Healthcare – Budget significantly more than current costs, potentially $300,000+ in retirement per couple.

- Protect Against Inflation – Estimate at least a 3% annual inflation minimum. Higher rates increase lifetime costs drastically.

- Investment Returns – Target approximately 6% average annual return overall, with some lower and higher years.

- Social Security – Assume benefits start between ages 67-70 for maximized payments. Do not rely solely on it.

- Pensions – If applicable, estimate payments conservatively given potential plan changes.

- Retirement Age – Earlier retirement such as at age 62 means more required income years and less time to save. Have adequate assets.

Building in conservative assumptions creates wiggle room for upside surprises. Discuss assumptions with your ad

Michael’s Advice: Plan Conservatively

In my experience, it’s better to be pleasantly surprised than caught off-guard. Plan for higher expenses, lower income, and higher inflation. That way, if you find at 80 you have more money than expected, it’s a welcome scenario. Always err on the side of caution.

Plan For Retirement Calculator: Will I have Enough For Retirement?

Doing The Math For Your Retirement Income Needs: The Power of Planning Estimating your income needs in retirement involves analyzing your anticipated expenses, factoring in inflation, and assessing potential income sources.

The Importance of Pre-Retirement Income Analysis: Understanding your pre-retirement earnings is the starting point for estimating your retirement needs. A common guideline suggests aiming for 70-80% of your pre-retirement compensation in retirement. This calculation takes into account reduced work-related expenses and taxes.

Understanding Retirement Expenses: Retirement doesn’t signify the end of expenses but a change in their nature. While work-related costs may decrease, healthcare, leisure activities, and travel expenses might rise. Crafting a detailed budget that encompasses all potential expenses is essential for accurate retirement goal setting.

Utilizing Retirement Income Calculators: Retirement interest income estimation tools provide a useful starting point for estimating your income needed. These online tools factor in variables like current savings, expected Social Security benefits, and projected expenses to offer an estimate. While these calculators provide insights, it’s advisable to consult financial professionals for a comprehensive analysis.

Retirement Income Comparisons – Average and Median Retirement Income Amounts

Understanding current retirement income levels helps you assess your financial readiness and set realistic goals for 2025 and 2026. The latest data from the U.S. Census Bureau and Social Security Administration reveals significant differences between median and average income, with median figures providing a clearer picture of what most retirees actually earn from combined sources including Social Security, pensions, and savings.

| Household Type | Average Income | Median Income | Data Source |

|---|---|---|---|

| Single Retiree (65+) | $83,950/year ($6,996/month) |

$54,710/year ($4,559/month) |

U.S. Census Bureau & Bureau of Labor Statistics (2025) |

| Married Couple (65+) | $100,000+/year ($8,300/month) |

$84,670/year ($7,056/month) |

U.S. Census Bureau (2023) & SoFi (2025) |

| Average Social Security Benefit | $1,976/month (2025) | Couple: ~$4,005/month | Social Security Administration (January 2025) |

| Recommended Monthly Spending | $5,000/month (average) | $50,000–$70,000/year individuals $80,000+/year couples |

CBS News & Financial Planners (2025) |

Key insight: The median income figures represent what most retirees actually earn, whereas average income is skewed higher by high earners—making the median a more reliable benchmark for retirement planning.

Individuals

- Median Monthly Income for 65-74 age group: $4,989

- Median Monthly Income over 75 years old: $3,601

- In 2026, the average monthly Social Security retirement benefit for retired workers rises to $2,071 following a 2.8% COLA adjustment from late 2025’s $2,015 average.

How does the average retirement income vary by state?

Do you remember earlier, I had mentioned that your retirement needs vary by where you live?

Average retirement income varies significantly by state, largely driven by differences in living costs. Examining averages by state provides insights into how location impacts retirement finances:

- Hawaii has the highest average retirement income at $119,004 annually. High cost of living is the key factor.

- Mississippi has the lowest average at $53,710. Much lower living expenses allow retirees to get by on less.

- In high-cost states like California, New York and Massachusetts, averages range from $90-100K.

- Low-cost states like Kansas, Tennessee and Alabama average $50-60K in retirement streams.

- Within states, urban areas usually have higher averages than rural areas due to higher costs.

- State tax policies can affect income needs. Low-tax states may offer savings.

These state-by-state differences demonstrate why national average income isn’t necessarily a good benchmark. Your specific location – and whether you’re willing to relocate – should inform your income needs. Cost of living calculation aids can provide location-adjusted estimates.

Please note that the figures provided are based on various sources and may vary depending on individual circumstances and the specific year.

Additional Considerations When Setting Your Retirement Income Goal

As a retired financial planner, I’ve witnessed first-hand the diversity of retirement planning needs.

Your income target should facilitate the retirement lifestyle you envision, whether traveling extensively, pursuing hobbies, leaving a legacy for family, or relocating to a lower-cost region.

Learn more about all of the Basic Estate Planning Documents You Need TODAY

Crunching the numbers is crucial, but your goal transcends a simple formula to instead enable the life you desire.

Tailor a Plan Aligned to Your Needs

Rather than focusing on hitting a particular dollar figure for recurring retirement income, think through your unique priorities and resources available. Think through all options, from tapping home equity, relocating, or part-time work to help bridge gaps to the lifestyle you envision.

As with Lauren’s case, the numbers are guides. Your realistic plan emerges from understanding your whole situation.

Diversify Income Streams for Flexibility

I’ve witnessed the pitfalls of relying entirely on Social Security. Cost-of-living increases often still lag behind inflation. These payment amounts assume Social Security will remain solvent for years to come.

- Creating a diversified income stream: Combining Social Security, pensions, and personal savings.

- Implementing a dynamic withdrawal strategy: Adjusting annual withdrawals based on market performance and personal needs.

Tally projected income from Social Security payments for each spouse if married, pension payments, annuities, and withdrawals from retirement accounts. Consider part-time work to generate supplemental funds if needed. Understand tax implications on retirement income streams.

While not perfect solutions, introducing additional income streams can tremendously boost flexibility.

Seniors earning income for the “extras”

Boosting income takes research and planning. A financial advisor can assess options and integrate appropriate strategies into a cohesive plan tailored to your situation. The key is creating sufficient guaranteed income to support your retirement lifestyle.

While Social Security and traditional pensions form a foundation for retirement sources of money, today’s retirees often need additional income streams. Here are some strategies to supplement your retirement payments:

- Delay Social Security claims – Waiting until age 70 increases monthly benefits by up to 32%.

- Work part-time – Earn extra income from temp, seasonal or side jobs.

- Move to lower-cost area – Relocating can significantly reduce living expenses.

- Downsize home – Selling and downsizing frees home equity.

- Invest strategically – Stocks that pay dividends can provide steady income.

- Purchase annuities – These products generate guaranteed lifetime income.

- Withdraw judiciously – Follow the 4% rule or work with an advisor.

- Leverage home equity – A reverse mortgage converts home equity to income.

- Rent rooms – Renting a room or carriage house creates rental income.

- Lower expenses – Reducing costs frees up more of your fixed income.

- Consider longevity insurance – An annuity starting advanced age can hedge risk

How To Lower Retirement Expenses?

Living expenses are a key driver of how much income you need in retirement. Trimming costs can allow you to thrive on less:

- Housing – Downsize to a smaller home or condo. Move to a lower-cost town or state.

- Transportation – Downsize to one car. Use public transit. Walk and bike more.

- Food – Eat out less. Meal plan. Shop sales and generic brands.

- Entertainment – Limit expensive cable packages. Find free activities.

- Travel – Be selective with destinations. Use points. Take longer trips.

- Shopping – Develop a minimalist mindset. Avoid impulse purchases.

- Healthcare – Enroll in Medicare. Use preventative care. Seek generic drugs.

- Insurance – Raise deductibles. Drop unnecessary coverage.

- Debt – Pay off credit cards and loans. Avoid new debt.

- Taxes – Choose retirement-friendly states/cities.

- Gifting – Set limits for children/grandkids. Focus on time over money.

Part-time work and relocating to a LCOL area can dramatically cut costs. But also look to trim expenses in your current living situation. Sticking to a frugal budget takes discipline but pays dividends in retirement.

Expanding on Psychological Aspects of Retirement Planning

Emotions can affect how you save for retirement.

- Overconfidence: Don’t take too many risks.

- Loss Aversion: Don’t sell investments too quickly.

- Anchoring: Don’t base decisions on the past.

Common Misconceptions Simplified

- Common misconceptions about a good retirement income include thinking that it’s solely about saving money when, in reality, wise investing plays a crucial role. In retirement, aim for a good monthly income by avoiding emotional mistakes in your savings.

- For Example – Avoid Panic Selling: Don’t rush to sell when things lose value. Wait for better results. One of my clients known to panic – fully diversified their investments. It really helped them handle the ups and downs of the market better than those who didn’t.

- Additionally, some mistakenly believe that Medicare will cover all healthcare expenses in retirement, which isn’t always the case.

Conclusion: Personalized Retirement Income Planning

In summary, determining your ideal monthly retirement income is a personalized process that depends on various factors. It requires meticulous consideration of your pre-retirement earnings, expenses, inflation, and income sources. While retirement income calculators provide valuable insights, consulting with financial experts is advisable to create a comprehensive financial plan.

Remember, it’s better to be pleasantly surprised by having more money in retirement than you expected than to realize too late that you have too little. By mastering these calculations, you can embark on your retirement journey with confidence and financial security.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.