Have you ever wondered if $4,000 a month is the magic number for a worry-free retirement? Do you think think that you can live on $4,00 a month in retirement? It’s a burning question on the minds of many soon-to-be retirees.

Imagine a life where you can kick back, relax, and not stress about money.Sounds pretty good, right? But can this monthly sum truly unlock the door to your golden years?

If you’re thinking of retiring on an income of $4,000 per month, you’ve likely wondered. Can this income truly cover my living costs? Between soaring rent prices, mounting grocery bills, debt payments, and other daily expenses, making ends meet on that $48,000 annual salary may seem impossible some months.

Will you constantly be stressed about money? Do you need to radically downsize your lifestyle? Or can smart budgeting actually allow you to live comfortably on $4,000 per month while still pursuing your goals?

As a financial expert, I’ve guided countless clients through this exact situation. And the truth is, whether $4,000 per month is “enough” comes down to your unique circumstances and priorities. Factors like your:

- Housing costs (rent, mortgage, etc.)

- Transportation needs and costs

- Essential expenses (utilities, insurance, minimum debt payments)

- Financial goals (emergency fund, retirement, etc.)

- Location and lifestyle

All play a major role in determining if a $4,000 monthly budget is workable or wildly insufficient for your situation.

In this guide, I’ll break down the realistic math and tradeoffs of living on around $4,000 per month. You’ll learn money-saving strategies to stretch this income further, need-to-know budgeting tips, and how to still allow room for fun and savings – without living like a penniless monk.

By the end, you’ll have an honest, experienced perspective on if a $48,000 salary can genuinely cover your expenses and provide your desired quality of living. Or whether you may need to adjust your housing, transportation, discretionary spending, and other major costs to make it work.

Let’s dive in and answer the burning question on your mind: Can I actually live on and retire comfortably on $4,000 per month?

In this article, we’ll unravel the mystery and discover how to retire comfortably on a budget.

Key Takeaways: Is $4,000 a Month Enough to Retire On?

- Is $4,000 per month enough to retire on? The answer is it depends. This amount could be sufficient for a comfortable retirement for many, but it’s essential to consider individual cost of living, expected lifestyle, and other personal financial factors. Stay tuned as we unpack the complexities of this seemingly straightforward question.

- Variability in cost of living across different locations can drastically affect how far your $4,000 can stretch. Whether you’re eyeing a cozy suburban home or an urban apartment, understanding regional financial climates is crucial.

- The impact of inflation rates on your retirement funds cannot be overstated. Grasping the concept of purchasing power over time will help you assess whether $4,000 a month will remain a viable income throughout your retirement.

- A combination of Social Security benefits, pensions, and personal savings will be the pillars of your retirement income. It’s vital to know how these sources interplay to sustain your monthly $4,000.

Quick Links: Is $4,000 a Month Enough To Live On in Retirement?

When you think about retirement planning, it’s like piecing together a puzzle. You need to fit together your living costs, income sources, and smart money management to see the whole picture. Everyone’s picture looks a little different. Some folks might need more dough, while others can make do with less

Did you know that according to a survey by the Employee Benefit Research Institute, only about 2 in 3 workers feel confident about having enough money for a comfortable retirement? That’s why it’s crucial to get the facts straight. By the end of this read, you’ll know if $4,000 per month will be your ticket to retirement bliss or if you might have to adjust your sail to reach paradise.

Wondering, what’s a good income in retirement? (read my related article!)

- According to recent stats from the U.S. Bureau of Labor Statistics, the average retired household spends about $4,622 per month or $55,464 per year (2023-2025 data).

- That’s good context for our $4,000 monthly budget question. Almost half of retirees were actually spending less than $2,000 per month.

- Only 16% were spending between $4,000 and $7,000 per month. So a $4k budget puts you in pretty good company!

Now, those are broad statistics. Your personal situation and expenses really determine if $4,000 is enough each month.

For most retirees, housing is the biggest monthly cost—stuff like your mortgage, property taxes, insurance. Like my client Joan and her husband, who downsized when they retired to reduce housing expenses.

Healthcare is another biggie that can take a surprise bite out of budgets.

Bottom line: understand YOUR must-have expenses, run the numbers, and get professional advice. That’s the recipe for stretching $4k comfortably! Reach out if you need any personalized suggestions for mapping out a retirement budget that works.

Curious about how these factors will influence your golden years? I’ll show you strategies to maximize your retirement income and why a personalized approach is key to a financially sound retirement. Understanding the nuances I’m about to explore could make the difference between just getting by and thriving in your post-career life.

Facts, Stats, and Important Information

- Based on my decades of experience, $4,000 per month provides a reasonable income for some retirees but may not be enough for others depending on individual circumstances.

- General rule of thumb is that retirees need 70-80% of pre-retirement income to maintain their standard of living.

- Healthcare, housing, and other essential costs often increase more rapidly than overall inflation, squeezing retiree budgets.

- Investment growth and Social Security SSI provide supplementary income but shouldn’t make up more than half of spending money.

- Catch-up 401(k) contributions allow those 50+ to save more in final years before retirement.

How To Figure Out If You Can You Retire Comfortably on $4,000 Per Month

Determining if a $4,000 monthly retirement income will allow you to live comfortably requires looking at your expected expenses, income sources, savings, and overall financial situation. Here’s a step-by-step guide to help assess if $4,000 per month is enough for your retirement:

Step 1: Wants – Estimate Your Essential Monthly Expenses

The first step is calculating your essential monthly expenses that can’t be eliminated, including:

Housing – Rent/mortgage, taxes, insurance

Utilities – Electric, gas, water, internet, cable/streaming

Food – Groceries and dining out

Healthcare – Insurance premiums, out-of-pocket costs

Transportation – Car payment, gas, insurance, maintenance

Debt Payments – Minimum payments on loans, credit cards

Add up these essential “needs” to get your baseline monthly costs. For many retirees, housing, healthcare, and food make up over 60% of their essential budget.

Step 2: Needs – Factor in Discretionary Expenses

Next, estimate your discretionary spending needs each month, such as:

Travel Entertainment and leisure activities

Hobbies and memberships

Gifts and charitable contributions

Having money for these “wants” is key to maintaining your desired retirement lifestyle. A realistic discretionary budget can be 15-25% of your total spending.

Step 3: Compare to Your $4,000 Monthly Income

Now you can compare your total projected monthly expenses to a $4,000 income. As a general guideline, your essential costs should be no more than 50-60% of your income to have enough for discretionary spending and some savings.

If your essential costs alone exceed $3,000 on a $4,000 budget, meeting your needs will be very difficult without drastically cutting discretionary expenses.

Step 4: Factor in Other Income Sources

Don’t forget to include any additional income streams you expect in retirement, such as:

Social Security benefits Pension income

Withdrawals from retirement accounts

Rental property income

Part-time employment earnings

These extra sources can provide a crucial supplement to your $4,000 per month.

Step 5: Assess Your Retirement Readiness

Finally, look at your overall retirement financial readiness:

Emergency fund savings – Aim for 6-12 months’ expenses

Total retirement savings – Following the 4% withdrawal rule

Healthcare costs – Medicare premiums, supplemental insurance

Lifestyle expectations – Can you maintain your desired standard of living?

It’s critical to have a realistic, well-defined retirement income plan that accounts for all your potential sources and expenses. This will help determine if $4,000 per month, combined with other income and assets, can sustain your retirement lifestyle and goals.

What You Should Focus On When Determining Your Retirement Feasability

For many retirees, living on a fixed $4,000 monthly income (or $48,000 per year) is the reality. But can you actually retire comfortably on that amount? Do you have enough money to retire at age 65?

Income Sources and Savings

Social Security provides a pillar of an income stream for most retirees. The average monthly Social Security retirement benefit is $2,009 as of September 2025. So you are nearly halfway to your $4,000 a month retirement income goal.

Next, you have your savings and investment portfolio that can create an income stream as well.

- Following this rule, you’d need a $1.2 million nest egg to provide $48,000 in annual retirement income.

- For the average American household nearing retirement with $107,000 saved, that $4,000 monthly budget from withdrawals would fall well short of their pre-retirement income.

How much do you have saved in your investmemnt portfolio? What would a 4% withdrawal rate provide as a monthly income for you?

Lifestyle and Living Expenses

Making Housing Costs Fit the 4K Budget

The biggest expense for most retirees is housing, which financial experts advise capping at 30% of your income. For a $4,000 monthly budget, that means keeping housing costs below $1,200.

This is very doable if you’ve downsized and have your mortgage paid off.

- According to the Harvard Joint Center for Housing Studies report, “Older mortgage-holders have median monthly housing costs of $1,470 compared to homeowners without mortgages, who pay a median of $520.“

- The report also notes that 73% of renters aged 65+ were cost burdened.

- Relocating to a lower cost-of-living area is one solution. For instance, according to Rentometer, the average rent for a 1-bedroom apartment in Pittsburgh is $1,350+. Compared to $2,150+ in Boston, MA.

Don’t Neglect Other Major Expenses Beyond Housing

Retirees need to factor in costs like:

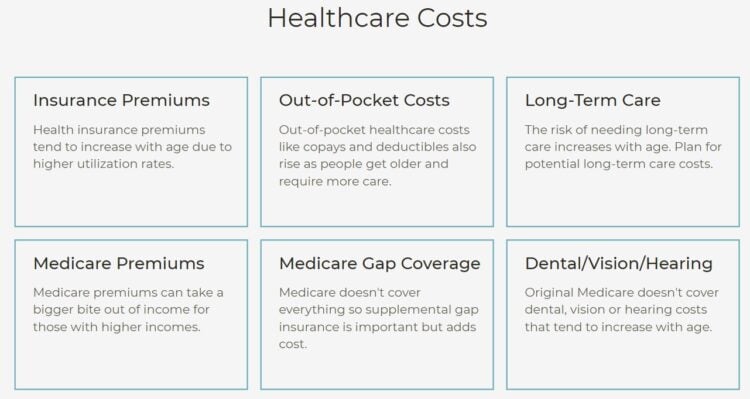

- Healthcare (premiums, copays, medications):

According to the Bureau of Labor Statistics data, households aged 65 and older spend an average of $6,814 per year on healthcare expenses. - Food (Groceries and dining out):

Households aged 65 and older spend an average of $5,555 per year on food, including both at-home and dining out expenses. 2 - Utilities/Household Operations (electric, gas, water, phone/cable):

The average annual spending on utilities and household operations for 65+ households is $4,115. - Transportation (car payment, insurance, gas, maintenance):

Households aged 65 and older spend an average of $7,292 per year on transportation costs. - Travel and leisure activities

Consulting a Financial Advisor

Given the complexities of retirement planning, consulting with a financial advisor can be invaluable. These professionals can assist in crafting a personalized plan that factors in your unique circumstances, helping you navigate the journey toward a secure retirement.

Step By Step Guide To Determining If You Can Live Comfortably On Your Retirement Income

1. Estimating Expenses: Setting Your Retirement Budget

How much will you need to maintain the lifestyle you envision in retirement? It’s time to crunch the numbers and set your retirement budget.

- Begin by totaling your current monthly costs for housing, healthcare, food, transportation, and leisure.

- Account for inflation over the years you will be retired.

- Healthcare requires particular attention as expenses often increase with age due to insurance, medications, and potential care needs.

Start by scrutinizing your current expenses and eliminating those that will disappear post-retirement, such as work-related costs or a mortgage that you expect to pay off. This exercise can reveal whether a monthly income of $4,000 will meet your needs or if adjustments are necessary.

Remember, a clear-eyed view of your anticipated living expenses and leisure costs is key to a realistic retirement budget.

2. Evaluating Your Sources of Retirement Income

Next, document expected retirement income from Social Security payments, pensions, and personal savings and investments. Average Social Security checks are currently around $1,950 monthly.

If your total estimated income mirrors or exceeds $4,000 monthly to offset your projected expenses, this target may be reasonable.

3. Assessing Your Finances

It’s important to factor in your nonhousing wealth, home equity, individual retirement accounts (IRAs), and employer-sponsored plans like 401(k)s. These form the backbone of your savings strategy.

- Assessing Your Personal Budget

Start by creating a comprehensive budget that breaks down your fixed and variable costs. This will give you a transparent view of where your money goes and highlight areas where you might cut back or reallocate funds. - Debt Management

Check your credit card balances, personal loans, and other financial obligations. Reducing high-interest debt can significantly improve your financial health. - Savings Strategy

Whether it’s your emergency fund or retirement accounts, consistent growth in these areas is a sign of sound financial planning.

Remember, it’s always a good idea to seek guidance from a financial advisor to ensure your retirement plan is a blueprint for a secure future

4. Understanding Savings Vs. Investing: Making the Most of Your Retirement Funds

Did you know that the way you manage your retirement funds can significantly impact your financial security in your golden years?

- Savings typically refers to putting money aside in safe, easily accessible accounts that offer low returns.

- On the other hand, investing is the process of purchasing assets with the potential for higher returns, though it comes with a greater risk.

- When planning for retirement, it’s essential to balance these two approaches to ensure you have both security and growth.

- With recent inflation and rising costs, retiring only on Social Security is tougher than ever. Having a pension or retirement savings to supplement that fixed monthly income makes a huge difference.

I remember a few years ago, I sat down with a client and calculated all of her essential living expenses. We realized if she watched her spending and made some lifestyle tweaks, $4k would be a decent monthly budget. The key is figuring out what’s essential for you.

If you’re hoping to retire soon, I suggest tracking your current expenses closely. That’ll give you a good idea of how far your retirement funds can stretch.

Also, don’t underestimate healthcare costs in retirement. Review your Medicare and insurance options – that can take a big bite out of fixed incomes.

5. Healthcare Costs in Retirement

Navigating the twilight years without a plan for healthcare costs can be like sailing into a storm without a compass. Medical expenses tend to climb as we age, and failing to account for them can greatly impact your retirement funds.

It’s crucial, then, to include healthcare as a distinct category in your retirement planning. By anticipating these costs and considering options like Medicare or a health savings account (HSA), you can ensure that your budget remains resilient against potential medical financial strains.

Key Takeaways

- Savings provide stability and low-risk growth, while investing offers the potential for higher returns.

- Aim for a diversified investment portfolio to spread risk and target consistent growth.

- Work with a financial advisor to develop a tailor-made retirement investment strategy.

- Regularly review and adjust your investment choices to align with your retirement goals.

Making Retirement Work on $4K Per Month

So how can you realistically live comfortably on just $4,000 in monthly retirement income? Here are some tips:

- Pay off your mortgage or downsize to a lower cost home

- Move to a retirement-friendly, lower cost of living area

- Maximize Social Security benefits as a couple

- Maintain an affordable, low-maintenance used vehicle

- Take advantage of senior discounts and cost-saving programs

- Seek out low-cost activities like walking, libraries, museums

- Delay receiving Social Security to increase your monthly benefit

- Have a smart withdrawal strategy to make your savings last

- Be prepared to make some sacrifices on leisure spending

While far from luxurious, it is possible for frugal retirees to enjoy their golden years comfortably on a $4,000 monthly budget. But it takes discipline, smart planning, rightsizing your housing situation, and managing your expectations.

Additional income streams from a pension, part-time work or rental property can provide more financial breathing room as well.

The key is going into retirement with a realistic, sustainable plan for stretching your modest income as far as possible. With preparation and the right money habits, an annual retirement income of $48,000 can cover your basic living expenses without too much

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.