If you’re an investor, you’ve seen the letters “SIPC” on your brokerage statements. Most people see it and think, “Great, my money is insured,” and move on. They treat it like a label on a food package. Reassuring, but not worth reading the fine print.

After nearly 30 years as a financial planner, I can tell you that assuming you understand SIPC insurance is one of the most dangerous mistakes an investor can make.

- SIPC coverage is not instant.

- It’s not a guarantee against market loss.

- It’s not a solution for fraud.

But SIPC coverage IS the bedrock of our financial system.

People think they understand it, but the reality is no one knows how it plays out until a crisis hits. I was there on the phone with terrified clients, during the 2008 financial crisis. That experience taught me that SIPC protection isn’t just a talking point; it’s the foundation of investor confidence.

Let’s pull back the curtain and look at how Securities Investor Protection Corporation (SIPC) really works.

📌 Key Takeaway

SIPC protects you from custodial risk, the risk of your broker failing. Not market risk. If you buy a stock and its price goes down, that’s your risk to bear. If you own 100 shares of that stock and your broker goes bankrupt and the shares vanish, that’s when SIPC steps in.

A Planner’s View: Why SIPC Became My Clients’ Most Important Safety Net in 2008

I’ll never forget the fall of 2008. The markets were in freefall, Lehman Brothers had just collapsed, and the word “bankruptcy” was on every news channel. My phone rang off the hook with clients asking the same panicked question: “Michael, is it all gone?“

Amid the chaos, my most important job was to be a source of calm and clarity.

I’d often use the analogy of a sturdy umbrella in a hurricane. “Your investment decisions are your own” I’d explain:

“SIPC is the umbrella that protects you if the building holding your assets, the brokerage firm itself, collapses.“

This simple idea, that their specific stocks and cash were protected from the failure of the firm holding them, was the single most powerful tool I had to keep people from making panicked decisions. It gave clients the confidence to weather the 2008 financial crisis.

That experience cemented my belief that understanding SIPC isn’t just financial literacy; it’s financial self-defense.

Want more insights on managing your finances with a unique perspective that only I can provide? Sign up for a complimentary newsletter below!

What SIPC Insurance Actually Covers (and Its Limits)

The Securities Investor Protection Corporation (SIPC) is a non-profit, member-funded organization created by Congress under the Securities Investor Protection Act of 1970. Its mission is to protect investors from losing their cash and securities if their brokerage firm fails.

What SIPC Covers (Up to $500,000 per customer):

- Stocks and Bonds: The core of your portfolio.

- Mutual Funds & ETFs: Your diversified fund holdings are protected.

- Cash Balances: Cash held in your brokerage account, waiting to be invested or from a recent sale, is covered up to a $250,000 sub-limit within the $500,000 total.

- Certificates of Deposit (CDs): If held at the brokerage firm.

- Unauthorized Trading: SIPC protection extends to cases where your cash or securities are stolen through unauthorized transactions by the firm.

The $500,000 Promise: The SIPC Umbrella and What’s Actually Shielded

The SIPC’s $500,000 promise covers the building blocks of your portfolio. The actual securities listed on your statement. This includes your stocks, bonds, mutual funds, and ETFs.

It also covers the cash sitting in your brokerage account meant for investment, but with a crucial nuance: that cash is only protected up to a $250,000 sub-limit within the overall $500k.

I had a client in Q2 2025 who sold a commercial property and parked $400,000 cash in his brokerage account, planning to deploy it gradually into dividend stocks. I immediately suggested moving $150,000 to a high-yield savings account at his bank. Why? If his broker failed overnight, only $250,000 of that cash would be SIPC-protected. The other $150,000? Gone. And here’s what most investors don’t know: In September 2025, SIPC’s Board voted to reinstitute member assessments for the first time in years, effective April 2026. Translation? They’re concerned about their reserve levels. That’s not panic-inducing, but it is a signal that the protection fund isn’t infinite.

This is a blind spot for even savvy investors.

- Does SIPC cover you if your broker makes a bad trade? No.

- Does it cover you if they go bankrupt and your 100 shares of Apple simply aren’t there anymore? That’s the exact scenario it was built for.

If you are a more visual and audio learner, consider watching this quick YouTube video on how SIPC works:

The Fine Print: What SIPC Does Not Cover (Market Loss, Fraud, Crypto)

SIPC doesn’t insure you against bad decisions, it insures you against bad custodians. Its limitations are critical to understand:

- Market Losses: If your investments lose value, that is your risk. SIPC will not reimburse you.

- Fraudulent Investments: It does not cover you if you are sold a worthless or fraudulent security. It only covers theft of your legitimate securities.

- Cryptocurrency: This is the biggest gap in modern investor protection. Digital assets like Bitcoin or Ethereum held at a brokerage are not considered securities by SIPC and have zero protection. I had a younger client in 2023 who was thrilled his brokerage app let him buy stocks and crypto in one place. He had over $50,000 in a popular altcoin.

When I explained that if the firm went under, his stocks were covered but his crypto had zero protection, the color drained from his face. He immediately moved his crypto to a dedicated hardware wallet. - Commodities, Futures, and Fixed Annuities.

SIPC vs. FDIC: Don’t Confuse the Vehicle with the Vault

This is where most people get tripped up. Confusing these two is like thinking your car insurance covers your house fire. They operate in different universes.

- The FDIC protects cash you’ve intentionally placed in a bank for safekeeping. It’s a vault.

- SIPC, on the other hand, protects the securities and cash inside your brokerage account—the investment vehicle.

| Feature | SIPC (Securities Investor Protection Corporation) | FDIC (Federal Deposit Insurance Corporation) |

|---|---|---|

| What it Protects | Securities (stocks, bonds) and cash at a brokerage firm. | Cash deposits at an insured bank. |

| Coverage Limit | $500,000 total per customer, per separate capacity. | $250,000 per depositor, per bank, per ownership category. |

| Cash Limit | Includes a $250,000 limit for cash within the $500k total. | The entire $250,000 limit is for cash. |

| Trigger Event | Brokerage firm failure/bankruptcy. | Bank failure. |

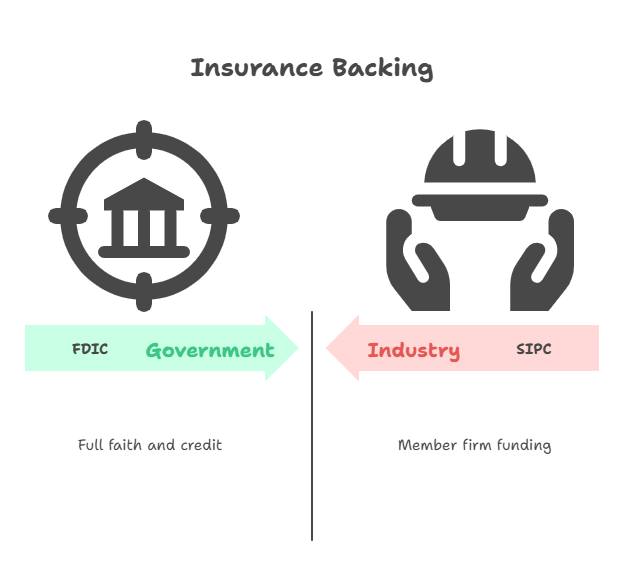

| Backed By | Funded by member brokerage firms. | Backed by the full faith and credit of the U.S. government. |

My bold prediction? By 2027, the line between these two will blur even further as fintech “super apps” push for unified insurance, creating massive confusion for consumers. For now, the key difference is the backing.

- FDIC is explicitly backed by the full faith and credit of the U.S. government.

- SIPC is a non-profit funded by its member firms, which, while robust (it has collected over $5 billion in assessments since inception), is a fundamentally different structure.

One is a government guarantee; the other is an industry-funded safety net. Do you know which one is protecting your “cash management account”? You’d better find out.

The Account Titling Strategy: How to Maximize Your SIPC Coverage

The $500,000 limit isn’t a hard ceiling; it’s a floor for the strategic investor.

This is where we move beyond basics into what I call the Account Titling Strategy for Maximum SIPC Coverage. This technique, which I implemented for dozens of high-net-worth clients, hinges on SIPC’s rule of “separate capacity.”

SIPC insures accounts based on their title, meaning different account types are insured independently, even at the same firm.

- Your Individual Brokerage Account: $500,000 coverage.

- Your Joint Account (with a spouse): $500,000 coverage.

- Your Traditional IRA: $500,000 coverage.

- Your Roth IRA: $500,000 coverage.

- A Trust Account for a Child: $500,000 coverage.

A married couple using this strategy could easily secure over $2 million in SIPC protection at the same institution. Your account title isn’t just a label. More like a multiplier for your insurance coverage.

The Anatomy of a Brokerage Failure: A Step-by-Step Guide

If your broker fails, the process isn’t chaos. It’s a cold, calculated legal procedure. In my career, I’ve seen it from the outside twice, with smaller firms my clients had old accounts with.

Here’s how it unfolds.

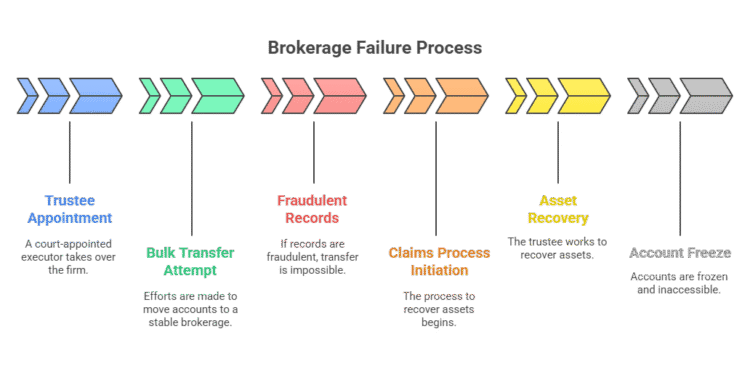

If your broker fails, don’t expect a check from SIPC in the mail the next day. The process is methodical and can take time.

- The Trigger: A firm usually gets into financial trouble and self-reports or is flagged by regulators like the SEC or FINRA

- SIPC Steps In: SIPC files an application in federal court to begin a liquidation proceeding.

- Trustee Appointed: The court appoints a trustee whose job is to recover assets.

- Account Transfer (Best-Case Scenario): In most cases, the trustee arranges a bulk transfer of customer accounts to another healthy, SIPC-member brokerage firm. This is the fastest and most common outcome. You’d simply get a notice that your account is now at a new firm.

- The Claims Process (If Assets are Missing): If a transfer isn’t possible (often due to fraud or poor records, as in the Bernie Madoff Case, you will need to file a claim. The trustee and SIPC work to recover and distribute all available property, using the SIPC fund to replace any missing cash or securities up to the coverage limits.

This process can be complex. While SIPC has an incredible track record of making investors whole, the Madoff recovery has taken over a decade, illustrating that in cases of complex fraud, patience is essential.

Are you prepared for your account to be frozen and inaccessible for weeks, or even months, while this plays out?

The Elephant in the Room: SIPC’s Limitations & 2025 Political Winds

It’s crucial to be clear-eyed about what SIPC cannot do.

- Fraud:

SIPC covers theft by your broker (i.e., they steal your shares). It does not cover you if you are sold a fraudulent investment (i.e., you are convinced to buy shares in a fake company). - Cryptocurrency:

As mentioned, this is a black hole for SIPC coverage. If your broker offers crypto trading and the firm fails, your crypto assets are not protected by SIPC. - Political Risk:

In the current political climate, all financial regulations are subject to debate. While SIPC has enjoyed broad bipartisan support for over 50 years, investors should always stay informed about potential legislative changes that could affect investor protections.

Frequently Asked Questions (Answered by Michael Ryan Money)

How do I file a SIPC claim?

If a trustee is appointed for your brokerage, they will mail a claim form to you. You can also find the form on the SIPC website. You must file it with the trustee, not SIPC.

How long does an SIPC claim take?

Most liquidations are resolved quickly via account transfers. According to SIPC, over 99% of eligible investors in completed cases have been made whole. However, if a claims process is needed, it can take several months or, in cases of extreme fraud, years.

Is SIPC insurance per account or per person?

It’s per “separate capacity,” as explained above. This means you can have multiple streams of coverage at one firm by using different account types (individual, joint, IRA, etc.).

Does SIPC cover mutual funds and ETFs?

Yes. Mutual funds and ETFs are considered securities and are protected against the failure of the brokerage firm holding them.

Final Word: SIPC as Your Financial Seatbelt

SIPC insurance is your financial seatbelt. It’s designed to protect you in a catastrophic crash. The failure of your brokerage firm. It won’t stop you from making a wrong turn and losing money in the market, but it will ensure you don’t lose everything because the vehicle itself falls apart.

Understanding how it works, its limitations, and how to strategically maximize your coverage is a hallmark of a sophisticated investor.

What to Read Next

Now that you’re an expert on account insurance, are you confident you’re with the right broker? See our comprehensive breakdown of the best platforms for your needs.

➡️ Read Our Guide: The Best Online Brokers for Beginners in 2025

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.