I’ll never forget the chill that ran down my spine, and my soon to be client’s. October 24th, 2008. David, a sharp engineer who’d meticulously planned his retirement for years and had only just hung up his hat. He logged into his portfolio in my office.

The silence was heavy as he watched a number that represented decades of dreams and diligent saving shrink by 5%, nearly $400,000 before our very eyes.

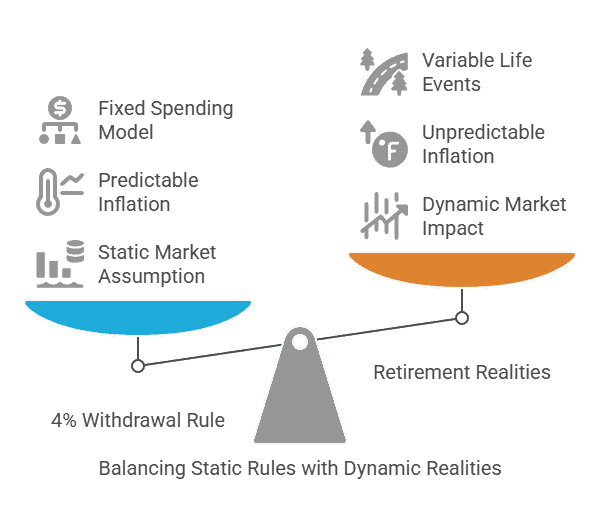

In those gut-wrenching minutes, the popular “4% withdrawal rule of thumb” he’d been relying on suddenly felt less like a financial strategy. And more like a game of Russian roulette with his future. That day crystalized a truth I’d seen play out many times: static, one-size-fits-all rules often shatter when they meet the harsh realities of the market and real life.

If you’re planning your retirement, you’ve undoubtedly encountered the 4% rule. It’s touted everywhere as the gold standard for how much you can safely withdraw from your nest egg each year.

But after 25 years on the financial front lines, I’m here to tell you that clinging to it as an unbreakable commandment can be a dangerous mistake.

It’s time for a “4% Rule 2.0,” an approach built on flexibility and real-world dynamics, not rigid theory. For some essential context on planning, you might want to first look at basic financial planning principles.

The Old 4% Withdrawal Rule: A Safe Strategy? What It Really Says

Let’s set the record straight. When financial planner Bill Bengen first published his research on safe withdrawal rates back in his 1994 study, his “4% rule” was groundbreaking. He analyzed historical market data going back to 1926 and tested various withdrawal rates over rolling 30-year retirement periods.

His conclusion? A 4% initial withdrawal, adjusted annually for inflation, had survived even the worst-case 30-year historical sequences. Notice that emphasis: worst-case. What often gets lost in translation is that in many of those historical periods, retirees could have actually withdrawn more and still been perfectly fine.

In fact, research has shown that in roughly half of Monte Carlo simulations (a common way to model portfolio outcomes), retirees strictly adhering to a 4% withdrawal actually die with more inflation-adjusted wealth than they started with. This isn’t a sign of perfect planning; it’s often a sign of underspending and an unnecessarily constrained retirement lifestyle.

Monte Carlo Retirement Savings Simulator

Explore how changing returns could affect a long-term savings plan. The simulator shows a range of modeled outcomes—not a forecast of your future account value.

Modeled Savings Outcomes

Modeled Balance Range Over Time

How to interpret this run

Assumptions used

This simulator is an educational illustration, not a prediction, probability guarantee, investment recommendation, retirement plan, or personalized financial advice.

The model uses independent monthly lognormal returns derived from the annual return and volatility assumptions. Real markets can exhibit losses, correlations, changing regimes, extreme events, prolonged inflation, changing interest rates, valuation shifts, taxes, behavioral responses, and other patterns not captured here.

Preset assumptions are illustrations only. They do not represent expected returns for a particular security, account, portfolio, investor, or future period.

The tool does not enforce IRA, workplace-plan, compensation, employer, or tax-law contribution limits. Confirm applicable limits before making retirement-account contributions.

Results are accumulation estimates only. They do not model retirement withdrawals, Social Security, pensions, health expenses, required minimum distributions, taxes, longevity, sequence risk during retirement, or changes in asset allocation.

Why Does the Four Percent Withdrawal Rule of Thumb Often Break Down

So why does a rule designed for the worst-case scenario often feel inadequate or break down for today’s retirees?

Sequence-of-Return Risk is a Monster:

This is the danger of experiencing poor market returns in the first few years of your retirement. If your portfolio takes a big hit early on while you’re simultaneously drawing income, it dramatically increases the odds of running out of money later.

That 2008 crisis David experienced? Prime example. The 4% rule is static; it doesn’t inherently adjust for these brutal early hits.

Inflation Isn’t Always Tame:

The original rule assumes steady, predictable inflation adjustments. But as we’ve seen in recent years, inflation can spike unexpectedly and significantly. A 9.1% inflation rate, like in June 2022, can decimate the purchasing power of a fixed withdrawal far faster than a gentle 2-3% average.

Over a 25 or 30-year retirement, even “average” inflation can nearly double your spending needs. Ignoring this insidious creep is like planning a cross-country road trip with only half the gas you need. Your plan needs to protect your savings from inflation.

Life Isn’t a Straight Line: A rigid rule collapses the moment reality bends.

The 4% rule is a mathematical model. Your life isn’t.

Unexpected expenses, changing health needs, or even opportunities for joyful spending (like helping with a grandchild’s education) don’t fit neatly into a fixed percentage.

The takeaway here isn’t that Bengen’s research was flawed – it was pivotal. But the oversimplified application of it as a rigid, never-exceed ceiling is where the trouble starts. It can be a useful floor for discussion, a starting point, but it’s rarely the optimal, final answer.

Retirement Withdrawal & Allocation Modeler

Explore the trade-off between initial portfolio withdrawals, stock exposure, retirement length, and your ability to reduce spending after difficult markets.

Your Modeled Trade-Off

Michael’s Perspective

What matters most in this combination

Stress-test question

Beyond Rigidity: Adaptive Strategies for a Real-World Retirement Income

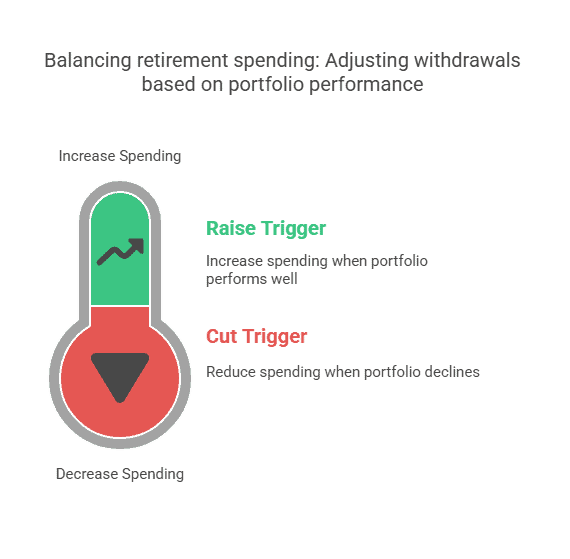

The good news is that smarter, more flexible approaches have evolved. These “guardrail” or dynamic strategies acknowledge market volatility and allow for adjustments, giving you a much better chance of weathering storms and even enjoying some of the market’s bounty.

The Kitces Guardrail Upgrade: Permission to Spend, Framework to Protect)

Michael Kitces, a leading voice in retirement research whose work I frequently shared with clients, has done extensive work on “guardrail” strategies.

Think of it like this: you set an initial withdrawal rate (perhaps even a bit higher than 4%, say 5%, if your portfolio is well-positioned and you have some flexibility). Then you establish “guardrails.”

Contrarian insight A 5 % initial withdrawal tied to remaining balance (not initial) survived every 40-year period since 1926 in a new WCU simulation.

Upside Guardrail (Raise Trigger):

If strong market returns cause your actual withdrawal rate (your annual spending divided by your current portfolio value) to drop significantly below your initial target (e.g., it falls from 5% to 4%), you give yourself a “raise” – increasing your spending by, say, 10%.

Downside Guardrail (Cut Trigger):

Conversely, if poor market returns cause your withdrawal rate to spike above a certain threshold (e.g., it rises from 5% to 6%), you implement a spending cut – perhaps by forgoing an inflation adjustment for the year or reducing discretionary spending by 10%.

A 2015 client ignored a downside trigger, refused a 10 % cut, and is now on a 6 % unsustainable path. This illustrates discipline costs less than regret. What happens if the market tanks year one? You cut early, not late.

Guardrails can increase failure risk if discretionary cuts never materialize. Kitces even warns that ignoring the downside trigger turns the rule into 2019’s “spend-through-the-floor” fiasco.

Guardrails aren’t shackles; they’re speed bumps for your spending.

Spend bravely when markets smile, tighten belts when they snarl.

When my client David, the engineer I mentioned earlier, adopted this guardrail approach after the 2008 shock, it transformed his outlook. He started with a more conservative withdrawal but, by 2014, after a significant market rebound, his guardrails allowed him to increase his spending to 5.6% of his then-larger portfolio.

He had a clear framework that gave him permission to enjoy the good years while providing a disciplined plan for tougher times. It replaced white-knuckle hope with confident action.

The Guyton-Klinger Dynamic Throttle: Cruise Control with Lane Assist)

Another sophisticated approach comes from Jonathan Guyton and William Klinger. Their model is a bit more complex but offers even more refined adjustments. It typically starts with a higher initial withdrawal rate (often in the 5-5.6% range) but builds in several rules:

- Withdrawal Rule:

Spending is adjusted annually for inflation. - Capital Preservation Rule:

If the portfolio has a negative return for the year, the next year’s withdrawal is frozen (no inflation adjustment). - Prosperity Rule:

If the current withdrawal rate drops to more than 20% below the initial rate due to strong portfolio growth, the withdrawal is increased by 10%. - Progressive Cutting Rule:

If the current withdrawal rate rises to more than 20% above the initial rate, the withdrawal is cut by 10%.

This dynamic throttle acts like an advanced cruise control system for your retirement income, automatically adjusting to real-world market conditions.

It’s particularly appealing for retirees who are comfortable with a bit more complexity in exchange for potentially higher sustainable income.

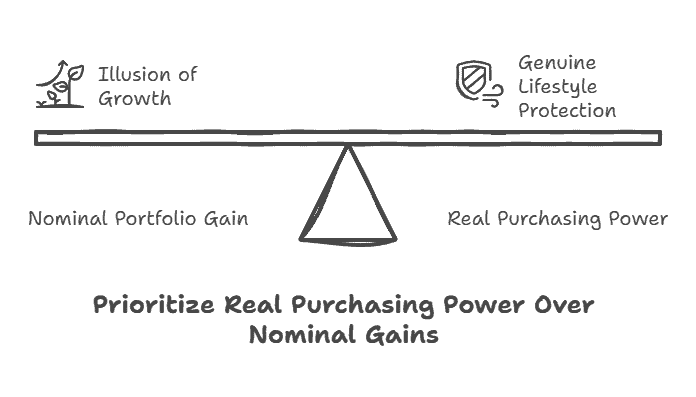

My “Inflation Collar” Twist: Ensuring Real Purchasing Power)

Over the years, working with clients, I developed a slight modification I often applied to guardrail strategies, particularly during periods of volatile inflation. I call it the “Inflation Collar.”

Even if the portfolio was up and a “raise” was triggered by the guardrails, we would only increase actual dollar spending if two conditions were met: The portfolio’s real return (that’s after accounting for inflation) was positive for the year. The current Consumer Price Index (CPI) was below a certain threshold, say 3%.

Why the collar?

Because I saw too many instances where a nominal portfolio gain was actually a loss in real purchasing power if inflation was raging. For instance, in 2021, David’s account was up a healthy 14% in real terms, and CPI was around 2%; he comfortably took a 5% spending raise.

But in 2022, even if his portfolio had eked out a small nominal gain, with CPI hitting 8%, the “Inflation Collar” would have denied a spending increase. This ensured that any spending “raises” were based on genuine growth in what his money could buy. Not just a higher number on his statement while his actual lifestyle was being eroded.

It’s a small tweak, but it provided crucial protection and clarity during those unexpected inflationary surges.

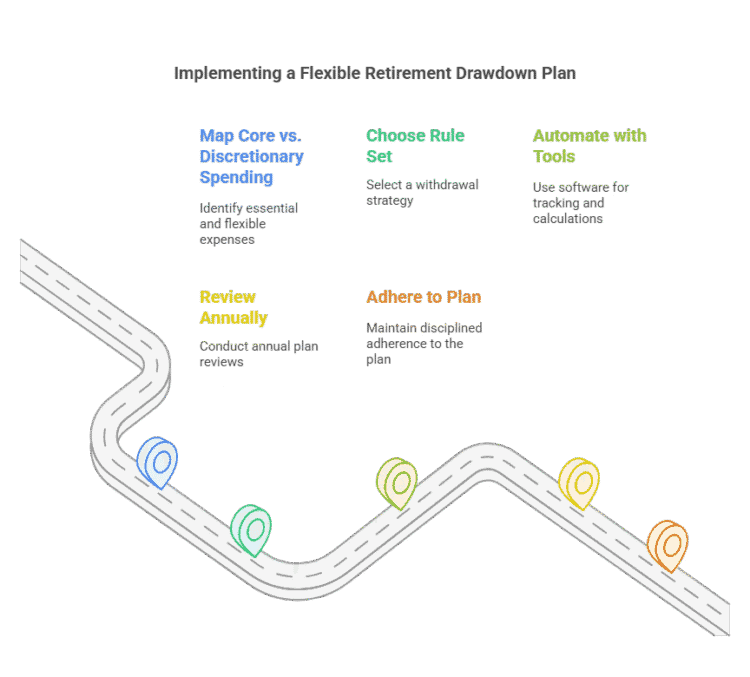

Putting A Flexible Retirement Drawdown into Practice: Your Action Plan

Adopting a more flexible withdrawal strategy isn’t just theory; it requires a practical plan. Here’s how I guided clients:

- Map Your Core vs. Discretionary Spending: Understand what’s non-negotiable (housing, food, healthcare, taxes) versus what’s flexible (travel, hobbies, dining out). This helps you identify where cuts can be made if a downside guardrail is triggered. Knowing your annual income needs is the first step.

- Choose Your Rule Set: Review the concepts – Kitces Guardrails, Guyton-Klinger, or perhaps incorporating an “Inflation Collar.” Which one resonates with your risk tolerance and desire for simplicity versus active management?

- Automate (or Semi-Automate) with Tools: Use a detailed spreadsheet or specialized retirement income software to track your portfolio, calculate your current withdrawal rate annually, and flag when guardrail triggers are hit. Don’t rely on memory or guesswork.

- Review Annually, or After Major Market Moves: Schedule a dedicated review at least once a year to apply your chosen rules. Be prepared to act sooner if a significant market event occurs (e.g., a 15-20% portfolio drawdown).

The key is disciplined adherence to your pre-set plan.

The Bottom Line: Flexibility Beats Fear in Retirement Income-Sustainability Planning

Rigid rules like a strict interpretation of the 4% rule might offer a false sense of security. But they often crumble when faced with the unpredictable nature of markets and life. Flexible, adaptive strategies like guardrails give you a much more resilient framework.

They provide both the permission to responsibly enjoy your wealth when times are good and a clear, pre-agreed playbook for making necessary adjustments when markets are challenging.

For most people I’ve worked with, that proactive approach beats white-knuckle hope and fear every single time. It’s about building a retirement income plan that bends, so it doesn’t break. Understanding concepts like asset allocation vs. diversification is also key to building that resilient portfolio.

When stocks soar, adjust. When bonds sag, adjust. When inflation bites, adjust.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.