What Is The Difference Between Asset Allocation And Diversification?

Alright, let’s cut right to it. If you hang around the investment world long enough, you’ll hear the same old debate, framed like a prizefight: Is it better to nail your overall asset allocation – the big-picture mix of stocks, bonds, etc. Or are you better off focusing on picking the next winning asset class? stock – security selection?

What Is The Difference Between Asset allocation vs Diversification?

For nearly thirty years, I’ve sat across the table listening to smart people tie themselves in knots over this. The financial media loves the drama of stock picking. It’s exciting. It makes for great stories. But let me tell you something I’ve seen time and time again:

Focusing only on picking winners while ignoring your portfolio’s fundamental structure is like meticulously choosing the tires for a car with a faulty engine. It might feel good for a bit, but you’re not getting where you need to go safely.

The truth? It’s not an either/or game. It never was. The real magic – or lack thereof – happens in how these two critical pieces, allocation and selection, work together.

Forget the generic advice for a minute. Let’s talk about what I’ve actually seen move the needle for investors over the long haul, the mistakes people keep making informed asset allocation decisions, and maybe a couple of things you won’t hear in a standard finance class.

TLDR; What Is The Difference Between Asset Allocation vs Diversification?

- The asset allocation vs. stock selection debate is the wrong lens. Your portfolio’s success depends on how well these elements work together. Allocation sets your risk foundation and controls volatility, especially in different asset classes.

- Selection tunes performance, especially when costs and discipline matter.

- Ignore the 90% myth, personalize your mix using tools like the “Sleep Test.” And avoid behavioral traps like recency bias or performance chasing.

- Simplicity, structure, and emotional discipline win over time.

I vividly remember a client back in the late 90s who abandoned his carefully crafted financial plan to chase the latest tech stocks. Despite our regular discussions about long-term strategy, he couldn’t resist the allure of doubling his money in months rather than years. By 2002, his portfolio had lost over 70% of its value, while more disciplined investors recovered much faster. The most painful part wasn’t just the financial loss, but watching him postpone retirement by five years. He forgot the blueprint.

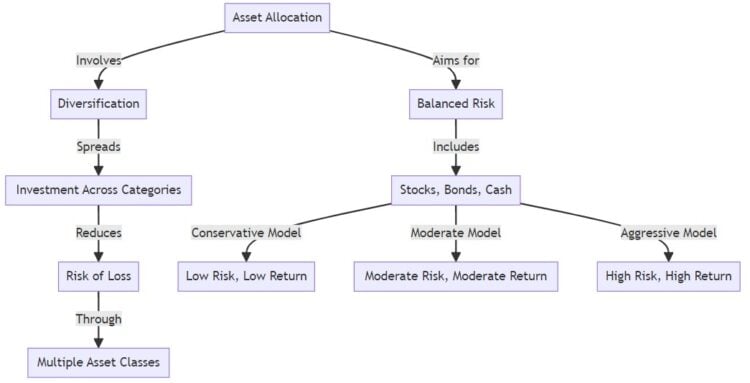

Asset Allocation: Your Financial Shock Absorbers

Think of asset allocation less like a rigid formula and more like the foundation and shock absorbers on your financial vehicle. Before you obsess over the horsepower (security selection), you need a structure that can handle the bumps in the road.

It’s the strategic decision about how much of your capital you’ll expose to different types of economic engines – the growth potential (and volatility) of stocks, the relative stability (but interest rate sensitivity_) of bonds, maybe real estate, cash reserves.

Why is this the first, most crucial step? Because it’s the primary dial controlling your portfolio’s overall risk exposure.

I’ve seen more investors bail out at the worst possible time – crystallizing losses. Not because their individual stocks were bad, but because their overall allocation was far too aggressive for their actual stomach. They hit a bump, the shock absorbers weren’t right for them, and they swerved off the road.

Getting this broad mix aligned with your real risk tolerance (we’ll get to how to really figure that out), your time horizon, and what you’re actually trying to achieve. That’s what provides resilience. It’s the bedrock of diversification.

And diversification isn’t just owning lots of different things; it’s owning stocks and bonds that tend to zig when others zag. Helping to smooth out the ride and, crucially, helping you stay invested.

- Check out “The Michaelryanmoney.com Guide to Asset Allocation” on Michael Ryan Money.

Sample Strategic Asset Allocations

Conservative Portfolio

Lower risk, stable returns

Moderate Portfolio

Balanced risk and return

Aggressive Portfolio

Higher risk, growth potential

Q: Why is asset allocation important for my portfolio?

A: The importance of asset allocation can’t be overstated! It helps manage risk and can greatly affect your total return. A solid asset allocation strategy can keep your portfolio balanced and aligned with your investment goals, especially during market fluctuations.

Q: What’s the difference between asset allocation and security selection?

A: Asset allocation is all about how you spread your investments across various asset classes like stocks, bonds, and ETFs. Security selection, on the other hand, focuses on picking the specific securities within those asset classes. Think of it as the big picture versus the fine details!

Now, security selection. This is choosing the specific instruments within your allocated lanes. Which stocks? Which bonds? Which mutual funds or low-cost ETFs?

This is where you (or a manager) get granular, looking under the hood – analyzing companies, scrutinizing fund strategies, comparing fees (never underestimate fees!), looking for value, growth, or income.

This is the sexy part, right? The realm of active management and active asset allocation are crucial for investment success., the hunt for individual securities is essential in a well-rounded policy portfolio.alpha‘ – beating the market. And yes, skillful selection can make a meaningful difference.

I’ve worked with portfolios significantly boosted by managers who adeptly navigated specific market niches or identified truly undervalued companies.

But here’s the cold water, poured straight from decades of my hands on experiences: Consistently picking winners, year after year, after factoring in fees and taxes? It’s extraordinarily difficult.

The market is a brutally efficient discounting machine. Most people who try – professionals included – fail to consistently beat simple index funds over the long haul. [Most recent SPIVA report proves it one again, emphasizing the importance of asset allocation in investment strategies.

It’s not impossible, but relying solely on stock-picking genius while your overall structure is shaky is like relying on perfect driving skills in that car with the faulty engine.

That Pesky “90% Myth” – Can We Bury It Now?

You’ve heard it: “Asset allocation determines 90% of your returns!” Often cited alongside the Brinson, Hood, and Beebower studies. Let’s be clear: this statement, as commonly used, is misleading.

What those landmark studies actually showed was that the policy asset allocation explained the vast majority of the variability (the volatility, the bumpiness of the ride) of portfolio returns, particularly for large pension funds with stable policies. [Brinson study interpretation].

Think of it this way: Your allocation (say, 80% stocks) largely dictates how much your portfolio might swing up or down in any given year compared to a 40% stock mix. It sets the risk parameters. But it doesn’t solely determine your final dollar amount.

“As I often tell clients,” quoting the wisdom of Benjamin Graham, “The essence of investment management is the management of risks, not the management of returns.” When I explain this principle, I watch as the lightbulb turns on – suddenly they understand that chasing performance isn’t the path to financial security.

Benjamin Graham, The Intelligent Investor

Here’s a real-world example I’ve seen repeatedly:

Take two identical 60/40 allocations. One uses low-cost index funds. The other uses expensive ‘closet index’ mutual funds that charge 1.5% for basically hugging the benchmark. Over 20 years, that fee drag – a selection issue – creates a massive difference in the final wealth accumulated, even though the volatility driven by the 60/40 split might look similar on paper.

Allocation sets the stage, but selection (including cost control!) heavily influences the final score. They are completely intertwined.

Strategic Discipline vs. Tactical Temptation (Guess Which One Usually Wins?)

Strategic vs Tactical Asset Allocation

| Feature | Strategic Allocation | Tactical Allocation |

|---|---|---|

| Goal | Long-term wealth building aligned with financial plan | Market timing to capitalize on short-term opportunities |

| Approach | Fixed target allocations with periodic rebalancing | Flexible allocations adjusted based on market outlook |

| Rebalancing | Periodic (quarterly, annually, or when allocations drift) | Opportunistic based on market conditions and analysis |

| Activity Level | Low – mostly passive with scheduled maintenance | High – requires regular monitoring and adjustments |

| Required Skill | Lower – focuses on discipline and plan adherence | Higher – requires market analysis and timing expertise |

| Emotional Discipline | Helps avoid emotional decision-making | Requires strong discipline to avoid behavioral biases |

| Transaction Costs | Lower due to less frequent trading | Higher due to more frequent portfolio adjustments |

For the vast majority of investors I’ve worked with, the most reliable path is Strategic Asset Allocation. Set a long-term mix based on your goals and your actual risk tolerance. Implement it simply, often with low-cost, diversified index funds or ETFs. Then, crucially, rebalance periodically to stay on track.

This imposes a discipline: you systematically sell a bit of what’s done well (selling high) and buy a bit more of what’s lagged (buying low). It feels wrong sometimes. It often works beautifully over time.

Then there’s the siren song of Tactical Asset Allocation. Making short-term shifts based on market forecasts – “Let’s get out of stocks now,” “Time to load up on energy!” Sounds smart. Feels proactive.

Frankly, in 25+ years advising real people, I’ve seen tactical timing destroy more wealth than almost any other strategy. Why?

Because our human brains aren’t wired for it. We chase heat (recency bias), get scared at bottoms (loss aversion), and think we can predict the unpredictable.

You have to be right twice – when to get out and when to get back in. Almost nobody does that consistently. I can count on one hand the number of people I know who’ve added real value through tactical calls over decades. AND I WAS A PROFESSIONAL!! For most, it’s a recipe for whipsaws and regret.

Q: What’s tactical asset allocation and how does it differ from strategic asset allocation?

A: Tactical asset allocation is a more flexible approach where you adjust your portfolio allocation based on short-term market conditions. Strategic asset allocation is more about setting a long-term policy portfolio and sticking to it. Both have their place in portfolio management, depending on your investment style.

Getting Your Own Allocation Right (Throw Out the Simplistic Rules)

So, how do you land your right mix? First, please ignore simplistic rules like ‘100 minus your age’ for stock allocation. That’s outdated advice from a different era.

I’ve had risk-averse 40-year-olds who needed less stock exposure than financially secure 75-year-olds with pensions and long time horizons for legacy goals. It must be personalized.

Here’s a framework that gets closer to reality:

The ‘Sleep Test’ (My Version):

Forget the questionnaires for a moment. Determine your proposed stock allocation (say, 60%).

- Now, vividly imagine the market drops 30% over the next few months. Your 60% stock portion takes a big hit.

- Write down – physically write down – exactly how you would feel and what specific action you would take.

- Would you panic sell? Would you nervously check quotes daily?

- Or would you think, “Okay, this is uncomfortable, but it’s part of the plan – maybe time to rebalance”?

- Be brutally honest. If your written reaction involves panic or abandoning the plan, your proposed stock allocation is too high for you, regardless of your age or what a calculator says.

- We dial it back until your honest written reaction aligns with sticking to the strategy.

- Link to Michael Ryan Money article on Risk Tolerance

Risk Tolerance Assessment Tool

1. What is your investment time horizon?

2. How would you react if your portfolio suddenly lost 20% of its value?

3. Which statement best describes your investment goal?

4. How much financial cushion (emergency savings) do you have?

Suggested Asset Allocation Range:

Important Note:

This tool provides a conceptual starting point only and is not financial advice. Your ideal asset allocation depends on many factors beyond this simple quiz. Consider working with a financial advisor to develop a personalized investment strategy that accounts for your complete financial situation.

For a more comprehensive assessment:

Try Vanguard’s Investor QuestionnaireTime Horizon – Really Define It:

Not just “long-term.” For which goal?

Money needed in 5 years for college has a very different time horizon than money for retirement in 25 years.

You might even have different allocations for different goals.

Goals – Get Specific:

“Make money” isn’t a goal. “Generate $5,000/month income in retirement starting 2040” is.

Specific goals allow you to work backward to the required return and acceptable risk.

Your Whole Picture:

Your allocation doesn’t exist in a vacuum.

Job stability, pensions, real estate equity, debt levels – they all influence how much investment risk you can and should take.

Investment statement depicting asset allocation diversification

Document your decision.

An Investment Policy Statement (IPS) sounds formal, but it’s just your roadmap. Write down your target allocation, why you chose it, and your rebalancing rules. It’s your anchor against emotional decisions later.

And revisit it! At least annually, or when major life events happen. A plan set at 35 often needs tweaking by 45 or 55.

Danger Zones: Where Good Intentions Meet Bad Outcomes

Experience teaches you where the landmines are hidden. Here are common traps I’ve seen derail even smart investors:

The ‘Diworsification’ Trap:

Owning 20 different mutual funds doesn’t automatically mean you’re diversified. I’ve looked under the hood of portfolios like this only to find massive overlap – they all held the same big US tech stocks!

True diversification means owning assets with low correlation – things that don’t always move in lockstep (like maybe stocks and high-quality bonds and some international exposure). It’s about the mix, not just the number of holdings.

The Concentration Hangover:

You let that winning stock or sector ride until it dominates your portfolio. It feels great on the way up. It’s devastating on the way down.

Remember those tech darlings of the late 90s? Many people saw years of gains evaporate because they fell in love with their winners and abandoned allocation discipline.

Rebalancing forces you to take profits and manage risk. It’s hard emotionally, vital financially. Use bands (e.g., rebalance if any class deviates +/- 5% from target) to enforce discipline.

Chasing Performance (Recency Bias):

Our brains are wired to expect the recent past to continue. When stocks soar, people want more stocks. When bonds do well, they pile into bonds. This almost always leads to buying high and selling low.

Sticking to your strategic allocation, even when it feels uncomfortable, is the antidote.

Ignoring Taxes in Taxable Accounts:

Rebalancing is crucial, but doing it smartly matters. Sometimes letting a winner run a bit longer to qualify for lower long-term capital gains tax rates makes sense. Actively harvesting losses to offset gains can add real value.

Don’t just blindly rebalance by percentages in your taxable accounts; think about the after-tax impact. This is an area where good advice often pays for itself.

The Myth of ‘Safe’ Bonds:

Bonds are generally safer than stocks, yes. But they aren’t risk-free. Rising interest rates crush the value of existing bonds (as we saw recently). And holding only “safe,” low-yielding bonds long-term guarantees you lose purchasing power to inflation, highlighting the importance of asset allocation.

Sometimes, what feels safe is actually introducing a different kind of risk.

The Bottom Line: It’s About Structure, Strategy, and Sticking To It

Let’s land the plane. Forget the endless “Allocation vs. Selection” debate. It’s the wrong frame for understanding the importance of asset allocation.

- Allocation is Your Foundation & Risk Control:

It sets the stage, dictates the likely volatility, provides diversification. Get this right for you first. - Selection is Execution & Refinement:

It happens within your allocation. Smart choices here (often low-cost, diversified funds, especially for core holdings) matter for minimizing drag and capturing market returns effectively. Bad choices or high costs can sink even a good plan. - Behavior is Everything:

Your biggest enemy isn’t the market; it’s likely the reflection in the mirror. Managing your own fear, greed, and impatience is paramount. A good allocation you can stick with is infinitely better than a “perfect” one you abandon mid-crisis. - Personalize Relentlessly:

Use frameworks like the ‘Sleep Test’. Ignore generic rules. Dig deep into your own situation. - Embrace Simplicity:

Complexity rarely equals better returns, but it almost always equals higher fees or confusion. A simple, strategic allocation implemented well is incredibly powerful.

Successful investing isn’t about predicting the future or finding hidden gems (though that’s nice when it happens). It’s about building a robust structure tailored to your life (asset allocation), implementing it intelligently (security selection & cost control), and then having the discipline and emotional fortitude to let it work over the long haul.

Do that, and you’ll likely be miles ahead of those still chasing headlines and hot tips.

Key Factors in Asset Allocation Decisions

- Your genuine risk tolerance (emotional & financial)

- Your investment time horizon

- Your specific financial goals

- Your short-term liquidity needs

- Your tax situation and implications

- Your existing investment portfolio

- Your employment stability and income sources

- Your retirement income needs

- Your estate planning considerations

- Your comfort with different asset classes

Click items to check them off as you consider each factor in your planning process.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Investing involves risk, including the potential loss of principal. Consult with a qualified financial professional before making investment decisions based on your specific circumstances.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.