Imagine leaving an 8.48% return on the table last year simply because of when you invested, not what you invested in. For many, that was the reality. Are you one of them?

I’m Michael Ryan, and for almost 3 decades as a financial planner, I’ve helped folks navigate these tricky markets. This latest DALBAR QAIB report? It’s a bombshell, and it confirms what I’ve seen firsthand, Our own behavior is often our biggest enemy, or, if we play it smart, our greatest ally.

The 2024 data is stark: the average equity fund investor pocketed “just” 16.54% while the S&P 500 sailed ahead with a 25.02% return. That’s a staggering 8.48 percentage point gap. And here we are entering 2026 – the same behavioral patterns are already emerging. Will you fall into the same trap, or will you finally break the cycle?

And get this, investors were pulling money out of equity funds every single quarter of 2024,. With the biggest stampede for the exits happening right before the market decided to throw a party and surge. It’s like leaving a concert just before your favorite band plays their biggest hit.

This isn’t just a one-off bad year; DALBAR has been tracking this for decades, and the story, unfortunately, remains largely the same. But here’s the good news: understanding why this happens is the first step to fixing it.

Think you’ve got these behavioral quirks mastered? Take this quick quiz based on the report’s key findings; some of these might surprise even the most informed investors!

I’m Michael Ryan, and for over 25 years as a financial planner, I’ve seen everything from the dot-com bubble to the 2026 market shifts. This latest data? It confirms what I’ve seen firsthand: Our own behavior remains our biggest enemy, but with the right plan, it can be our greatest ally.

In this article, we’ll unpack the shocking truths from the 2025 DALBAR QAIB report, explore the costly behavioral patterns that trip us up. And most importantly, I’ll share my “Behavioral Armor™” framework – a practical system honed over years of client conversations to help you capture the returns you truly deserve.

So, are you ready to stop leaving money on the table? Read on.

The Uncomfortable Truth: What the 2025 DALBAR Report Really Says About Investor Behavior (And Why It Matters for 2026)

Think the market timing curse only hits stock pickers? The 2025 DALBAR data, as detailed in reports like Investors Missed the Best of 2024’s Market Gains, Latest DALBAR Investor Behavior Report Find, paints a much broader picture of behavioral blunders. Even in the supposedly “safer” corners of the market.

As we’ve seen, equity investors didn’t just underperform; they actively sabotaged their returns by withdrawing funds consistently throughout 2024,. Especially before significant upturns.

“Many investors captured only part of the market’s gains in 2024, missing the strongest-performing quarters. It’s a continuing pattern the data has confirmed across decades of analysis.”

Lou Harvey, DALBAR President, (DALBAR QAIB 2025 Press Release via PRNewswire)

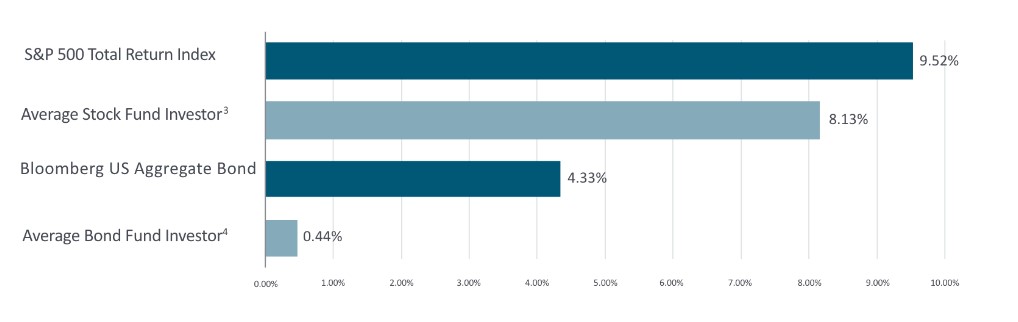

But the story takes an even more curious turn when we look at the fixed income landscape. Despite fixed income markets delivering negative returns overall, investors actually increased their contributions to bond funds in 2024. The Average Fixed Income Investor lost 1.07%, while the Bloomberg U.S. Aggregate Bond Index, a common benchmark, actually gained 1.25%. (DALBAR QAIB 2025 Report)

It’s fascinating, isn’t it?

We see panic selling in stocks, but then this almost blind faith in bonds, even when the data’s screaming caution. It tells us our emotions are pulling strings across our entire portfolio. An area I explore in my overview of the financial planning process.

I often saw clients misinterpret bond market movements, and the QAIB data shows this is widespread. One client, let’s call him “Cautious Carl,” was so worried about stock volatility that he shifted a large chunk to bond funds right when they were tanking, thinking he was playing it safe. He effectively bought high and locked in losses. Missing the eventual equity rebound he was scared of in the first place.

Classic case of trying to dodge raindrops and ending up in a hailstorm, wouldn’t you agree?

What This Means for You Entering 2026

Here’s the reality check: We’re now at the threshold of 2026, and the investment landscape is shifting. The S&P 500 posted a 13% total return through most of 2025, continuing its impressive multi-year run (26.3% in 2023, 25% in 2024). Yet history – and DALBAR’s research – tells us that average investors are likely capturing only a fraction of these gains.

Three critical investing trends shaping 2026:

Active ETF Revolution:

The investment industry is experiencing a structural shift. Active mutual funds continue bleeding assets while active ETFs are seeing explosive growth. If you’re still in old-school mutual funds making panic-driven switches, you’re paying higher fees AND sabotaging your returns through bad timing. The vehicle matters less than the behavior.

AI and Market Concentration:

Much of 2024-2025’s returns came from a handful of mega-cap tech stocks. Many investors chased these names at peaks or fled at dips – classic FOMO and panic. The question for 2026: Will you chase the next hot sector or stick to a diversified, disciplined approach?

The “Guess Right Ratio” Hit 25%:

In 2024, DALBAR found investors timed their buy/sell decisions correctly only 25% of the time. That means they were wrong three out of four times. As we head into 2026 with ongoing uncertainty around interest rates, elections, and geopolitics – do you really think you’ll suddenly get better at timing? Or is it time for a different strategy?

Alright, DALBAR lays out the ‘what’ pretty clearly. But the multi-million dollar question is ‘why’? What’s happening between our ears that leads to these costly detours?

Why do investors underperform?

The Psychology of the Gap: Why We Consistently Shoot Ourselves in the Financial Foot

If we all know “buy low, sell high” is the mantra, why does the data show we’re masters of the opposite? It’s not that we’re not smart; it’s that we’re human! Our brains are wired for survival in the savanna, not navigating Wall Street’s digital stampedes.

Several cognitive traps and behavioral biases are at play:

Recency Bias:

This is the tendency to give too much weight to recent events, making us believe current trends will continue indefinitely. When markets are down, “Recency Rick” (a client archetype I see often!) gets convinced they’ll stay down, leading to selling at the bottom.

The 2024 equity outflows right before surges? Classic Recency Bias in action. So, the market sneezes, and we immediately assume it’s got terminal pneumonia. Sound familiar?

Loss Aversion:

Psychologically, losses hurt about twice as much as equivalent gains feel good. This makes us overly cautious after experiencing a loss, often causing investors to sell to “stop the pain.” Even if it’s the worst long-term decision.

It’s like touching a hot stove. You’re not keen to go near it again, even if the next stove is perfectly safe and full of delicious food.

Overconfidence Bias:

Some folks believe they have a special knack for predicting market moves. They might get lucky once or twice, reinforcing this belief, but consistently timing the market is virtually impossible. The data proves it.

Are you a market wizard or just riding a lucky wave that’s about to crash?

Herd Mentality (FOMO):

Fear Of Missing Out, or FOMO, drives investors to pile into “hot” investments when they’re already peaking (buying high). Often fueled by media hype or seeing others get rich quick. I had a client, “FOMO Fiona,” who jumped into a trendy tech stock at its absolute peak in 2021, only to see it crash.

The herd might feel safe, but it often stampedes off a cliff.

Let’s be real, fighting these urges is tough. But recognizing these behavioral biases, as highlighted by the field of behavioral finance, is the crucial first step. These aren’t character flaws; they’re human tendencies we need to build defenses against.

The Unshakeable Case for Patience: How “Time In the Market” Builds Real Wealth

If trying to dance in and out of the market is a losing game, what’s the winning strategy? It’s simpler (and more powerful) than you think.

People think ‘buy and hold’ is boring. I think it’s brilliant. It’s like planting a tree. The real growth happens slowly, steadily, when you’re not constantly digging it up to see if the roots are okay.

The magic of compounding interest, where your returns start earning their own returns, only truly works its wonders over extended periods.

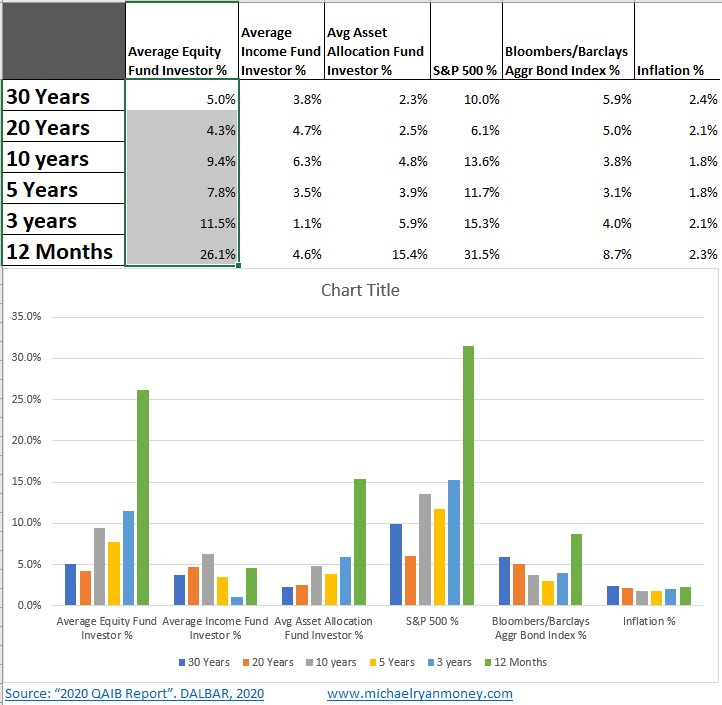

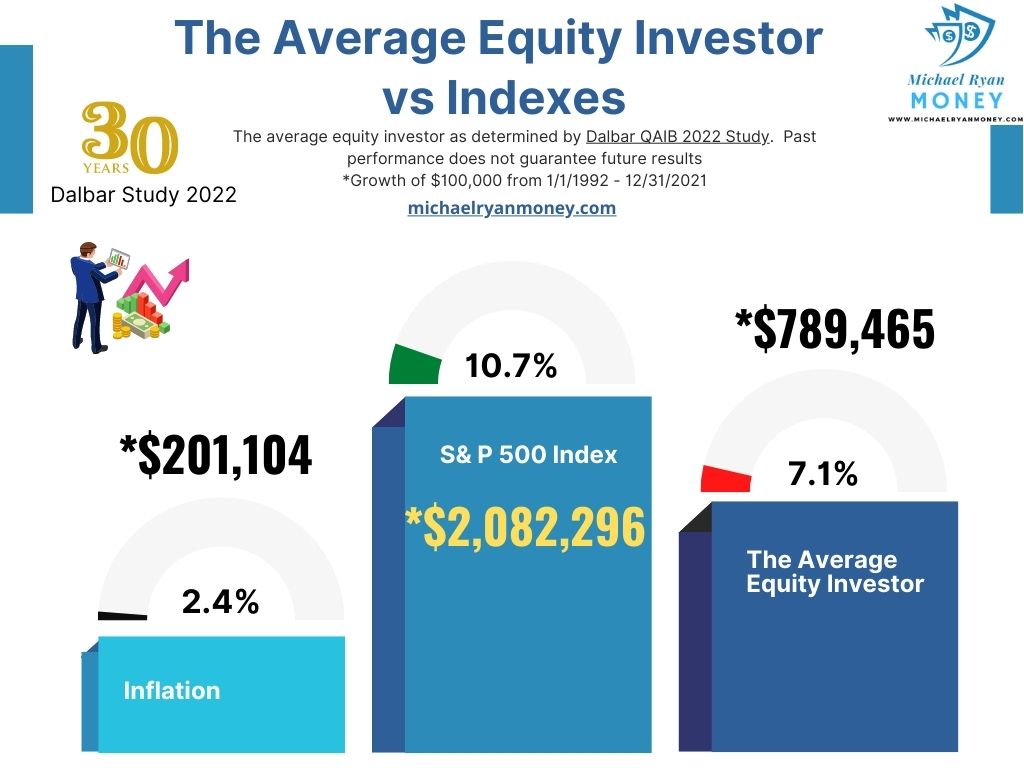

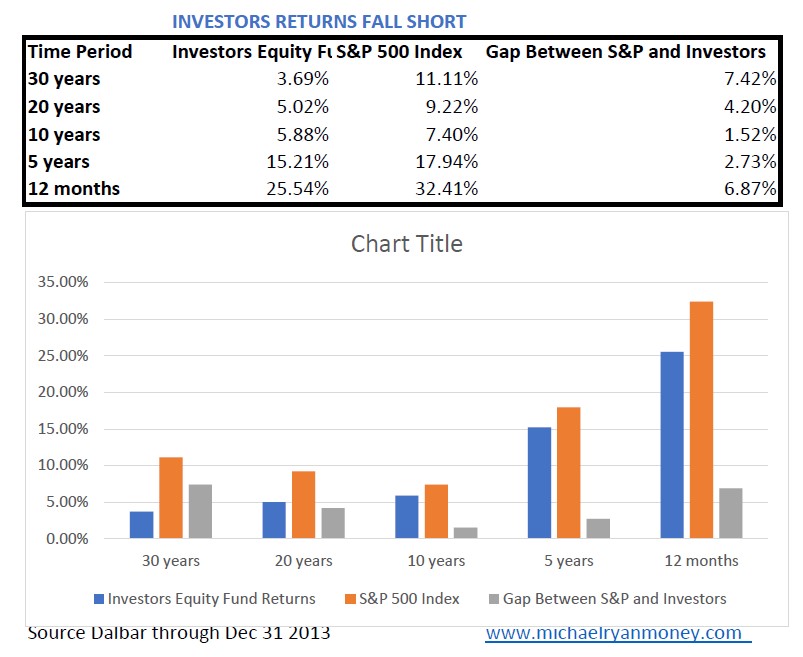

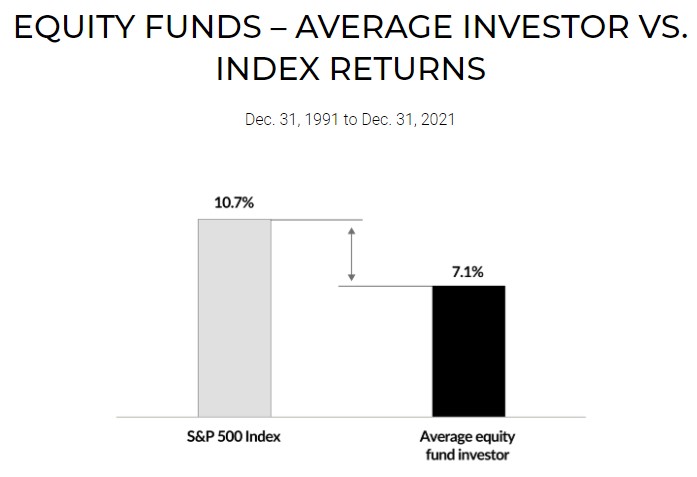

Consider this: DALBAR’s data shows that over the 30 years ending in 2024, the average equity fund investor earned an annualized 10.00%. The S&P 500? 10.92%. (Hartford Funds citing DALBAR). That near 1% difference annually, compounded over three decades, is a fortune left on the table.

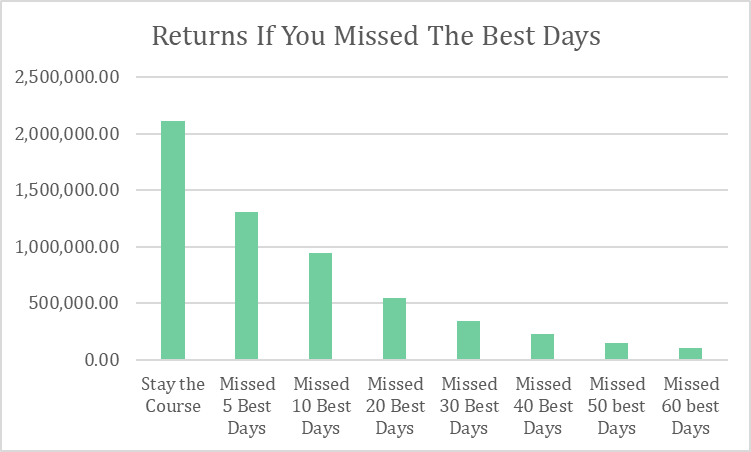

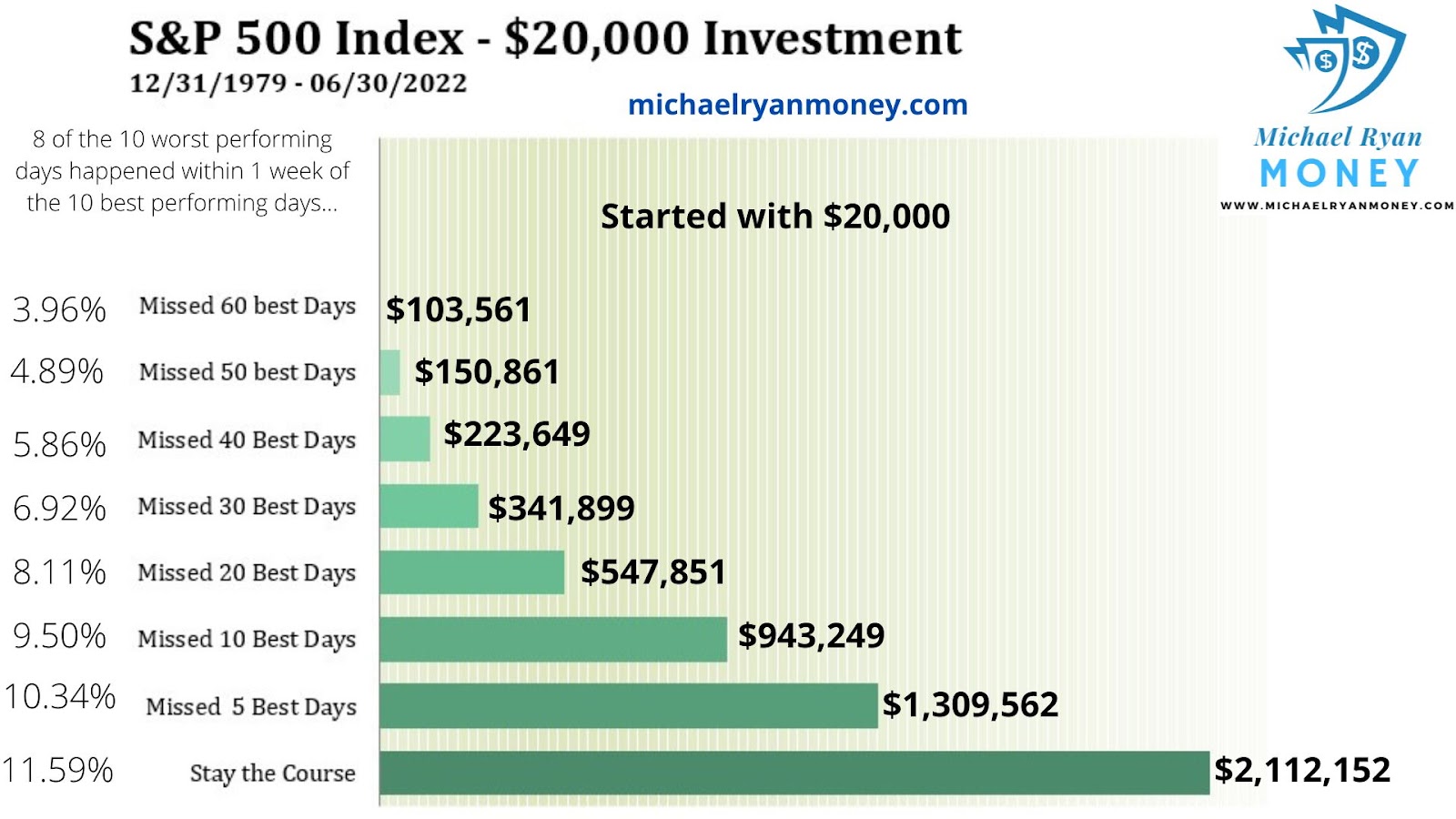

And here’s the thing: a huge chunk of the market’s long-term gains comes from just a handful of its best days. Miss those, and you’ve severely hobbled your portfolio. Studies from firms like Bank of America have shown that missing the 10 best days in the S&P 500 over a long period could have cut your overall return by more than half!

Now, let me show you something that really brings this home. I call these the ‘Accelerated Wealth Days’. Miss just a few, and you’re on the slow track. It’s these “growth spurt” days that often follow periods of uncertainty – exactly when fearful investors are sitting on the sidelines. When everyone else is running for the exits, are you brave enough to hold the door?

15 Days That Make or Break Your Decade

Missing just a few of the market’s strongest trading days can significantly erode long-term wealth accumulation, even for disciplined investors. This analysis demonstrates how staying fully invested versus missing the best market days dramatically impacts portfolio growth over a decade, with missing just 15 days reducing annual returns by 55% and cutting final portfolio value by nearly two-thirds. Understanding this timing risk underscores the importance of maintaining consistent market exposure and avoiding emotional decision-making during volatility.

| Best Market Days Missed | Annual Return | Return vs. Baseline | Portfolio Growth ($10,000) |

|---|---|---|---|

| 0 days (Fully Invested) | 7.7% | Baseline | $64,844 |

| 5 days | 5.9% | −23% | $45,000 |

| 10 days | 4.7% | −40% | $35,000 |

| 15 days | 3.5% | −55% | $25,000 |

| 20 days | 2.5% | −68% | $18,000 |

| 30 days | 1.1% | −85% | $11,000 |

The data powerfully illustrates why market timing is dangerous—adopt a buy-and-hold strategy to capture the gains of the market’s best days and maximize decade-long wealth creation.

Missing just 15 of the best days over 28 years slashes your gains by more than half-proof that time in the market, not timing, is what builds wealth.

524

This table is based on S&P 500 data from 1995–2023. Returns and portfolio values are rounded for clarity. The effect is even more dramatic if you miss more days; missing 30 best days nearly wipes out all growth.

As Warren Buffett, a man who knows a thing or two about building wealth, famously said, “The only value of stock forecasters is to make fortune-tellers look good.” He also said, “Our favorite holding period is forever.”

This isn’t about being passive; it’s about being disciplined and strategic, letting time do the heavy lifting.

Michael Ryan Money’s “Behavioral Armor™”: Your 4-Step Plan to Conquer Timing Traps

Knowing isn’t doing. So how do you actually build the discipline to stay invested? This isn’t theory; this is what evolved from hundreds of conversations, seeing what actually helps real people stay the course when their gut is screaming ‘Run!’ Over my near 30 years in the trenches with clients, I’ve developed what I call the “Behavioral Armor™” system. It’s not about being smarter than the market; it’s about being smarter about yourself. It’s a proactive defense against those emotional impulses that DALBAR shows are so costly.

Let’s break it down:

Education (Know Your Enemy… and Yourself):

- Understand Market History:

Recognize that volatility is normal, and historically, markets trend upwards over the long term. Don’t let short-term dips derail a long-term plan. - Identify Your Triggers:

What news, emotions, or situations make you want to hit the panic button? Self-awareness is your first line of defense. Are you a “Recency Rick” or a “FOMO Fiona”? Be honest! - Learn About Biases:

Actively study the common behavioral biases we discussed. The more you understand them, the easier they are to spot in your own thinking.

Automation (Set It and Mostly Forget It):

- Embrace Dollar-Cost Averaging (DCA):

Invest a fixed amount of money at regular intervals, regardless of market ups and downs. This takes emotion out of the equation and ensures you buy more shares when prices are low and fewer when they’re high.

And here’s a little secret many overlook with DCA – consider front-loading your IRA contributions early in the year if you can. More time for potential growth within that tax-advantaged wrapper! - Automate Contributions:

- Set up automatic transfers from your bank account to your investment accounts every payday. This makes saving and investing a habit, not a decision you have to revisit constantly.

- Consider Auto-Rebalancing:

Set your portfolio to automatically rebalance back to your target asset allocation periodically (e.g., annually). This forces you to systematically sell high and buy low without emotional interference. Don’t make this mistake: manually tinkering too often. Let the system work. Learn more about setting up Automated Investing here.

Accountability (Your Financial ‘Battle Buddy’):

- Write Down Your Financial Plan:

Having clear, written financial goals and an investment policy statement makes it harder to deviate on a whim. Is your plan just a vague idea, or is it written in stone (or at least, in a very important document)? - Work with a Trusted Advisor:

A good financial advisor or planner acts as a behavioral coach, helping you stick to your plan during turbulent times. They’re the ones who can talk you off the ledge when you’re tempted to make an emotional move. - Find a Knowledgeable Friend or Mentor:

Discussing your investment thoughts with someone who understands long-term principles (and isn’t prone to panic themselves) can provide a valuable sounding board.

Auditing (Regular Check-ups, Not Obsessive Tinkering):

- Schedule Annual Reviews:

Review your financial plan and investment performance once a year, or when major life events occur. This is for strategic adjustments, not reactionary changes. - Limit News Consumption:

Constant exposure to market news and “expert” predictions can fuel anxiety and impulsive decisions. Focus on your long-term plan, not the daily noise. - Track Your Behavior, Not Just Returns:

Did you stick to your plan? Did you avoid emotional decisions? These are often more important metrics for long-term success than short-term performance figures.

I had a client who was a classic market timer. She’d jump in and out, always trying to catch the next wave, checking her portfolio 10 times a day, losing sleep over every headline. After a particularly bad year where she missed several key upswings, we implemented the Behavioral Armor™.

We automated her investments, set clear long-term goals, and had quarterly check-ins focused on sticking to the plan, not chasing headlines. Two years later, her portfolio was significantly healthier, but more importantly, she told me, “Michael, I finally sleep at night. I’m not stressed about the market anymore.” That’s the real win.

Which pillar of the Behavioral Armor™ do you need to strengthen first? Reflect on that as we move to the conclusion.

Frequently Asked Questions (FAQ)

Still got questions? You’re in good company. Here are some of the most common things folks ask me about market timing and staying invested:

Q: Can market timing ever work?

A: For most investors, no. Decades of data, including the 2025 DALBAR report, and my 25 years of experience, overwhelmingly show it’s a losing proposition. The odds are heavily stacked against you consistently getting it right.

It’s far more profitable to focus on what you can control: your savings rate, your asset allocation, and your own behavior. For a deeper dive on why market timing doesn’t work, check out my other article.

Q: How many best days do investors typically miss?

A: It varies, but studies often show missing just 10-20 of the market’s absolute best days over a couple of decades can slash your returns by a third, or even half! The 2025 DALBAR report showed investors missed key surges in 2024.

It’s not about many days; it’s about those critical days that often come when least expected, usually after periods of pessimism.

Q: What’s the biggest mistake investors make trying to time the market?

A: Hands down, it’s letting emotion dictate decisions. Fear makes you sell at the bottom, and greed (or FOMO) makes you buy at the top. That’s the exact opposite of the ‘buy low, sell high’ goal. The DALBAR data is a testament to this, year after year, showing a clear pattern of investors reacting emotionally rather than strategically.

Are your feelings your financial advisor?

Q: Is Dollar-Cost Averaging a good way to avoid timing mistakes? Absolutely.

A: DCA is a core part of my ‘Automation’ pillar in the Behavioral Armor™. It takes the guesswork and emotion out of deciding when to invest. By investing a consistent amount regularly, you’re buying systematically, regardless of market noise. It doesn’t guarantee a profit or protect against loss in declining markets. But it’s a fantastic discipline for long-term investors and helps mitigate the risk of investing a lump sum at the wrong time.

Your 2026 Action Plan: Stop Gambling, Start Building Wealth

So, after all the data, the stories, and the strategies, what’s the one thing to remember about building lasting wealth?

The 2025 DALBAR study isn’t just numbers; it’s a story about human nature and our relationship with money. The good news? You get to write your own ending. That 8.48% gap we talked about? That’s the cost of letting emotions or flawed timing strategies call the shots.

My clients who’ve embraced the “time In the market” philosophy and fortified themselves with Behavioral Armor™ have not only seen better returns on paper but, more importantly, they experience less stress and more confidence in their financial future. They sleep better at night. It’s not about predicting the future, but preparing for it with discipline.

Time, consistently applied, is your most powerful financial ally. Perhaps not your only ally, good planning and the right assets matter of course, but it’s the one most people underestimate and misuse.

Ready to stop gambling and start truly investing for your future?

Your 3-Step Plan to Win in 2026:

Commit to Your Behavioral Armor™ This Week: Pick one pillar – Education, Automation, Accountability, or Auditing – and implement it by January 15, 2026. Set up that automatic investment. Write down your investment policy. Schedule that meeting with an advisor. Just start.

Ignore the 2026 Noise: There will be headlines. Elections. Fed decisions. Market corrections. AI hype. Your job isn’t to predict these – it’s to stay invested through them. Remember: investors who tried timing in 2024 were wrong 75% of the time.

Measure What Matters: At the end of 2026, don’t just look at your returns. Ask yourself: Did I stick to my plan? Did I avoid emotional decisions? Did I continue investing during market dips? These behaviors are what separate wealth-builders from wealth-destroyers.

The choice is yours. You can repeat the same behavioral mistakes that cost the average investor 8.48 percentage points in 2024, or you can be different. Time in the market has beaten timing the market for decades. Will 2026 be the year you finally put this truth to work?

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.