Lifestyle creep is the subtle, ongoing increase in spending that happens when your income grows. Often without conscious decision, leading you to feel just as strapped on $100,000 as you did on $60,000.

To beat it, use the “First Slice Rule”: every time you get a raise or bonus, automatically put 50% into long-term investing, 30% into a specific savings goal, and only allow up to 20% for lifestyle upgrades. Make automation your discipline.

I once had a client Chloe, a 34-year-old marketing manager who got a $20,000 raise. Six months later, her savings rate hadn’t changed. We did a financial audit and found her old “latte factor” had evolved into a “$1,200-a-year artisanal-cheese-and-wine-subscription factor.”

This is lifestyle creep in its sneakiest form. It’s the silent wealth killer that ensures you feel just as broke on a $100,000 salary as you did on $60,000. It’s the reason so many high earners are “not rich yet.”

But what if you could turn every raise into a powerful wealth-building engine?

In this guide, I’ll show you the psychology behind why we let our spending expand and give you the actionable playbook we used to reverse Chloe’s situation and put her on the path to financial independence.

📌 Key Takeaways

- Identify the true enemy: lifestyle creep is fueled by the Hedonic Treadmill, where spending rises just to maintain happiness.

- Apply the First Slice Rule: Allocate 50% of each raise to investing, 30% to specific savings goals, and up to 20% to lifestyle upgrades.

- Automate discipline as default: Set up automated transfers so your future self gets paid before lifestyle adjustments occur.

- Here’s what people get wrong: Cutting creep doesn’t mean no enjoyment—it means spending intentionally on what brings lasting value.

What Is Lifestyle Creep (And Why Is It a Silent Wealth Killer)?

Lifestyle creep, also known as lifestyle inflation, is when your spending rises in lockstep with your income, turning “wants” into “needs” without realizing it. As defined, “Lifestyle creep is what happens when you start making more money, and your standard of living rises along with your income.

Lifestyle creep is what keeps people on the financial treadmill, unable to build wealth despite higher earnings.

Instead of sticking to your former way of life, you begin spending more—slowly, without really realizing it”. The slow creep means many high earners end up living paycheck to paycheck, unable to build financial freedom.

Why is it so hard to resist? Psychologists call it the “Hedonic Treadmill”. Humans quickly adapt to new luxuries and look for the next upgrade. Per The Decision Lab, “Our happiness levels don’t fluctuate over the long-term… eventually, your new luxury fades and that upgrade becomes your baseline”.

The real danger? According to Fidelity research, letting your spending grow by just 3% each year can cut your chances of a successful retirement in half.

📘 A Planner’s War Story: The True Cost of Keeping Up

I once had a client who bought a new BMW simply because his neighbor did. We calculated that the car payment was costing him his ability to retire two years earlier. Seeing the actual math, trading two years of freedom for his neighbor’s approval, was a brutal wake-up call.

The Psychology: Are You on the “Hedonic Treadmill”?

Why is lifestyle creep so hard to resist? It’s baked into our psychology. The core driver is a concept called the “Hedonic Treadmill“ (or hedonic adaptation).

It’s the human tendency to quickly return to a stable level of happiness despite major positive life changes. That thrill you get from a new car or a bigger apartment fades, and that new luxury quickly becomes your new normal.

To get the same happiness boost, you need another upgrade, and the cycle continues.

📊 Quick Stat

While a famous Princeton study suggested a $75,000 happiness plateau, a newer 2024 study in Economic Letters found this emotional well-being plateau may now be closer to $200,000. However, the core principle remains: at a certain point, more income and more spending do not create more day-to-day happiness.

The Long-Term Impact: A Tale of Two Savers

Let’s make this tangible. Here is a 10-year projection comparing two people who both start with a $70,000 salary and get a 4% raise each year. The only difference is how they handle lifestyle creep.

- The Creeper: Spends 5% more each year.

- The Smart Saver: Limits lifestyle spending growth to 2% per year. It’s simply delayed gratification.

| Year | The Creeper’s Net Worth | The Smart Saver’s Net Worth | The Difference |

|---|---|---|---|

| 1 | $10,500 | $12,600 | $2,100 |

| 5 | $61,500 | $82,000 | $20,500 |

| 10 | $160,000 | $235,000 | $75,000 |

As you can see, small, seemingly innocent spending increases compound into a massive wealth gap over time.

The “First Slice Rule”: My 50/30/20 Plan for Every Pay Raise

Generic advice like “make a budget” doesn’t work for new money because that money isn’t yet assigned to a job. You need a proactive plan. I call it the “First Slice Rule,” and it applies to every dollar of new, after-tax income from a raise or bonus.

Here’s the breakdown:

- 50% to Your Future Self (Invest Automatically):

Pay yourself first! This is non-negotiable. Half of your net raise goes directly into long-term, wealth-building investments.

Increase your 401(k) contribution percentage, up your automatic IRA transfer, or add to your brokerage account. - 30% to Your Next Big Goal (Save Intentionally):

Funnel this portion into a high-yield savings account for a specific, medium-term goal. This is your “fun fund” for a down payment, a vacation, or a new car paid for in cash. - 20% to Your Present Self (Spend Guilt-Free):

This is your reward. You’ve earned it. Use this 20% to upgrade your lifestyle in a way that brings you real joy. Get the better coffee, plan a nicer date night, or hire a house cleaner. It’s planned, it’s intentional, and it’s 100% guilt-free.

4 Tactical Tools to Make Your Plan Stick

A rule is only as good as your system for enforcing it. Here are the four actions I have my clients take.

Tool 1: Automate Your “First Slice” Immediately

The day you confirm your raise, log in to your payroll portal or bank account and increase your automatic transfers. Don’t let the new money even touch your checking account. This is the essence of paying yourself first.

Tool 2: Give Your Dollars a Job

Know where your money is going with a clear spending plan. This allows you to see the creep before it happens and make conscious decisions.

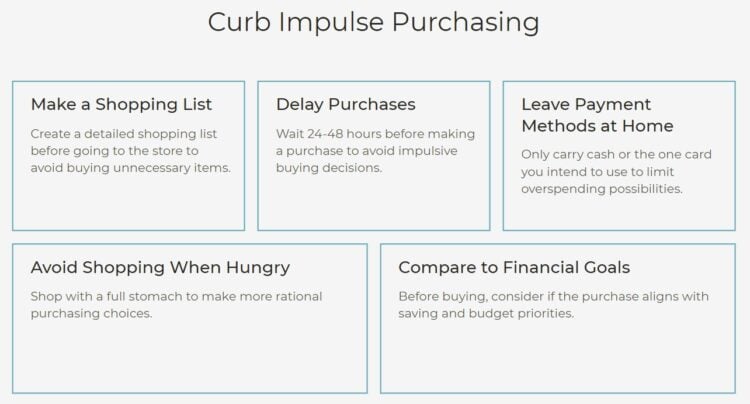

Tool 3: Implement a 72-Hour Rule for Big Purchases

For any non-essential purchase over a set amount (say, $200), put it on a list and wait 72 hours. The impulse often fades, saving you from regretful spending.

Tool 4: Schedule an Annual “Lifestyle Audit”

Once a year, review your bank and credit card statements. Are you paying for subscriptions you don’t use? Have your “wants” slowly become “needs”? This check-in is crucial for staying on track.

💡 Michael Ryan Money Tip

Automation is the cure for a lack of willpower. You will never have to decide between saving and spending if the saving has already happened. It’s the single most effective tactic my wealthiest clients use.

Your Final Takeaway: Choose Your Future

Lifestyle creep is a battle won or lost in the small decisions we make after every success. Left unchecked, it guarantees that no matter how much you earn, you’ll never feel truly wealthy.

But by implementing a clear plan like the “First Slice Rule,” you take control. You make a conscious decision to prioritize your future freedom over fleeting upgrades. This isn’t about deprivation; it’s about intentionality. It’s how you turn a simple pay raise into a legacy of financial independence.

📌 Your Anti-Creep Action Plan (TL;DR)

- Automate your future: Immediately direct at least 50% of any new income to savings/investments.

- Cap your spending: Aim to keep lifestyle spending growth at or below 2% annually.

- Pause before purchasing: Implement a 72-hour waiting period for non-essential buys over $200.

- Know your “why”: Align your spending with your long-term values, not short-term impulses.

(For more on building a robust financial life that resists lifestyle creep, I highly recommend the book “Your Money or Your Life“ from Amazon.)

Lifestyle Creep Frequently Asked Questions

How much lifestyle inflation is sustainable?

A sustainable rate is one that allows your savings rate to increase with your income. A good rule of thumb is to keep any lifestyle upgrades at less than 25% of your net raise, ensuring the other 75% goes toward building wealth.

Is it bad to reward yourself after getting a raise?

Not at all! In fact, you should. The key is to do it intentionally. The “First Slice Rule” ensures you prioritize your long-term goals first, and then carves out a specific portion of your raise for guilt-free enjoyment.

How does lifestyle creep affect my Financial Independence (FIRE) number?

It has a massive impact. For every $1,000 your annual spending increases, your target FIRE number increases by $25,000 (based on the 4% rule). Controlling lifestyle creep is the most effective way to accelerate your path to financial independence.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.