It’s one of the most frustrating feelings in finance. You deposit a check at Chase, see the money in your account, and then. BAM. Chase holds the check, and a 7-day hold appears. Your money is there, but it’s not yours to use. Plans are wrecked, bills are late, and the panic sets in.

You’re left asking: Why is Chase holding my money hostage? Is this even legal?

Here’s the deal, and it’s not what most people think.

That 7-day hold by Chasse isn’t a punishment. It’s a direct result of a banking system where a 1980s federal law, the Expedited Funds Availability Act, is forced to deal with 21st-century digital fraud. The hold is the bank’s primary defense mechanism, and understanding why it gets triggered is the key to avoiding it.

In my 30 years as a financial planner, I’ve walked countless clients through this exact situation. This guide will go beyond the generic advice and give you the unspoken truth about why holds happen and a concrete playbook for what to do next.

Key Takeaways Ahead

Interactive Calculator: Will My Check Clear Before 7 Days?

Check Fund Availability Estimator

*Estimate only, based on common rules (Reg CC). Actual holds vary due to risk factors, holidays, check details & Chase policies. Not financial advice or a guarantee.*

The ‘Why’ Behind the Chase 7 Day Wait: Regulation CC and Bank Risk

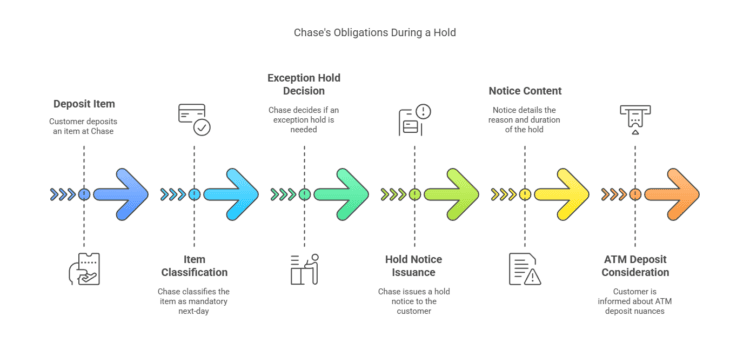

The rules for check holds are mandated by federal law, implemented via Regulation CC. This law requires banks to make a portion of your deposit available quickly. Usually the first $225 by the next business day. But it also gives them the legal authority to place an “exception hold” and delay availability for the rest of the funds when they detect certain risk factors.

Unspoken Professional Truth:

When you deposit a check, the bank doesn’t instantly know if it’s good. The bank provisionally credits your account and then begin the process of collecting the money from the check writer’s bank.

The “hold” is the legally defined window they give themselves to ensure the check clears before they let you withdraw the funds. If Chase bank releases the money and the check bounces a few days later, the bank is on the hook. The hold protects the bank, not you.

Before we go deeper, here’s what you need to know upfront:

⚡ Key Takeaways

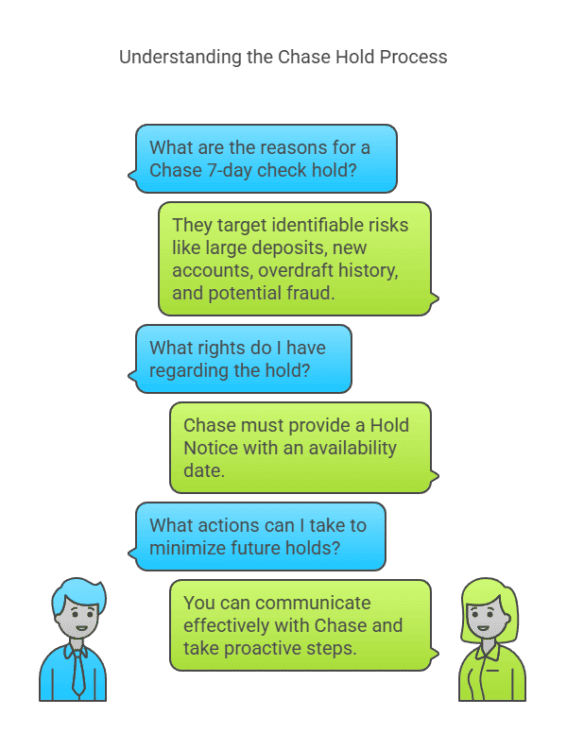

- It’s Legal and Regulated: Check holds are authorized under Federal Regulation CC to protect banks from fraud. Chase must provide you with a written notice explaining the hold and when the funds will be available.

- It’s About Risk, Not You: A 7-day hold is typically triggered by automated risk algorithms that flag your deposit based on a specific set of criteria, such as the check’s size, your account history, or the deposit method.

- Verification is a Two-Way Street: The delay isn’t just Chase. It’s the time it takes for Chase to communicate with the check writer’s bank and verify that the funds actually exist.

- You Have Options: While you often can’t force an early release, you have a clear playbook for communicating with the bank and, more importantly, for taking action to solve your immediate cash-flow problem.

The Most Common Triggers for a 7-Day “Exception Hold”

Your deposit was likely flagged for one of these specific reasons authorized under Regulation CC.

- The Large Deposit Flag (Over $5,525):

- The law allows banks to hold funds on any amount deposited in a single day that exceeds $5,525. The first $5,525 is subject to normal availability rules, but the rest can be held.

- The New Account Gauntlet (Less Than 30 Days Old):

- If your account has been open for less than 30 days, you are considered a “new customer” and the bank is legally allowed to place longer holds on your deposits. This is one of the most common reasons for a 7-day hold.

- “Reasonable Cause to Doubt Collectibility”:

- This is the bank’s catch-all for when something about the check or your account activity seems risky. A detailed checklist of triggers is in the FAQ below, but it can include a history of bounced checks, a check from an out-of-state bank, or even a low check number (indicating a new, unproven account).

- Repeatedly Overdrawn Account: I

- f your account has been negative for six or more business days in the last six months, the bank can place Exception Holds on your future deposits.

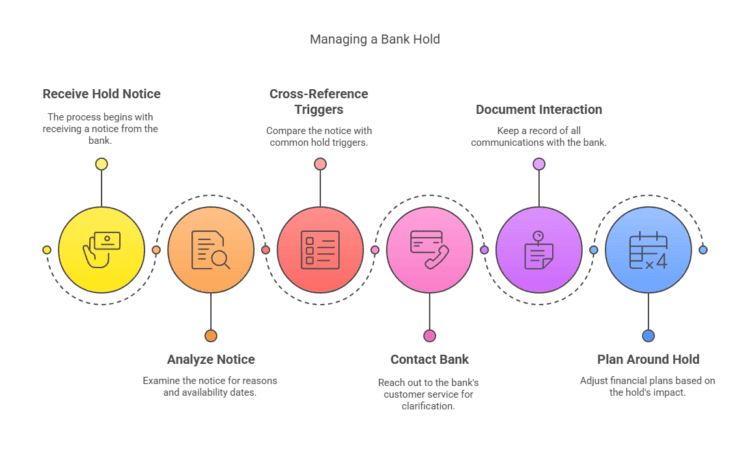

Your Action Plan: What to Do When a 7 Day Hold is Placed on Your Check

- Analyze Your Hold Notice:

- This is your most important document. It legally requires the bank to state the reason for the hold and the exact date the funds will be made available.

- Contact the Check Issuer:

- This is the most overlooked step. Explain the situation to the person or company that wrote you the check. Ask them if they can cancel the check and pay you in a different, faster way, like Zelle, a wire transfer, or even cash.

- Request a Partial Emergency Release:

- Call the bank or visit a branch. While they are unlikely to lift the entire hold, you can explain the situation and ask for a small, partial release to cover a critical payment like rent or a car payment. It’s not guaranteed, but it is always worth asking.

- “Break Glass” Option – Reputable Check-Cashing Services:

- Use this with extreme caution. Services at major grocery stores or Walmart can give you instant cash, but they charge significant fees. This should only be considered a last-resort option for a true emergency.

How to Minimize Future Bank Holds

- Go Electronic: The best way to avoid check holds is to avoid checks. Use Direct Deposit for your salary and services like Zelle for personal payments whenever possible.

- Deposit In-Person: For a large or unusual check, depositing it with a teller is better than using the mobile app. A teller can physically inspect the check and you can ask them upfront if they anticipate a hold.

- Keep Your Account Healthy: The single best way to reduce your “risk profile” is to avoid overdrafts. A clean account history makes the bank’s algorithms see you as a lower-risk customer.

💡 Get Smarter About Banking Rules & Red Flags

Receive one clear, actionable money move each week—designed to help you:

- Understand the banking rules that affect your money

- Sidestep costly fees, holds, and financial traps

- Apply proven playbooks you can use in minutes

✅ Join thousands of readers navigating the financial system.

📬 No spam. Unsubscribe anytime.

Frequent Readers Questions About Banking Holds

What exactly is Regulation CC?

Regulation CC is the rule issued by the Federal Reserve to implement the Expedited Funds Availability Act. It sets the maximum time a bank can hold your funds and requires them to disclose their policies. The Consumer Financial Protection Bureau (CFPB) provides excellent consumer guides on your rights.

Why did I get a hold on a Cashier’s Check? Aren’t they guaranteed funds?

While safer than personal checks, cashier’s checks are a major target for sophisticated counterfeit fraud. If a cashier’s check is for a large amount, from an unfamiliar source, or deposited into a new account, the bank will still place a hold to give itself time to verify its authenticity with the issuing bank.

Does depositing via Mobile App vs. Teller increase the risk of a hold?

It can. While the same rules apply, mobile deposits carry a slightly higher inherent risk because the bank cannot physically inspect the paper check for signs of alteration or fraud. For a large, important, or unusual check, depositing it in person with a teller is always the safer bet.

Master Your Money Flow

- Troubleshoot a late direct deposit – Learn the 7 reasons your electronic payment might be delayed and the exact steps to take to track it down.

- Decode the numbers on any check – Master the routing and account numbers to set up electronic payments correctly and avoid costly errors.

- Find the correct Chase routing number – Get the right routing number for your specific state to ensure your direct deposits and transfers are sent without a hitch.

Conclusion: Taking Control By Understanding the Chase Hold Process

Knowledge is power, especially when navigating bank rules. While facing a Chase 7-day check hold is undeniably frustrating, understanding the process demystifies it: By familiarizing yourself with standard practices, you can better anticipate any delays and plan accordingly. Additionally, understanding Zelle transfer durations can also help you manage your cash flow more effectively, as these transfers typically occur almost instantly for most users.

- It’s Regulated: Holds aren’t random; they follow specific Regulation CC exceptions.

- Reasons Exist: They target identifiable risks (large deposits, new accounts, overdraft history, potential fraud).

- You Have Rights: Chase must provide a Hold Notice with an availability date.

- You Have Actions: You can communicate effectively with Chase and take steps to minimize future holds.

By understanding the “why” behind the hold and knowing your rights and options, you move from feeling helpless to being an informed navigator of your finances.

Get Your Funds Faster With Chase Mobile Check Deposits

What’s your biggest takeaway from understanding Chase check holds? Share your thoughts or experiences in the comments below! Ready to explore other banking topics?

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.