Alright, let’s cut to the chase. You’ve got a check in your hand, and it looks like a secret code. You need to find the account and routing numbers, probably for direct deposit or to set up a payment. Mess this up, and your money could end up in limbo, or worse, in the wrong hands.

I’ve seen it happen more times than I can count in my nearly three decades as a financial planner.

The Quick Answer (But Don’t Stop Here):

Here’s a quick YouTube explainer of How To Read a Chek I put together, if you prefer a quick answer:

- Routing Number: The first 9-digit number at the bottom-left of your check. Think of it as your bank’s address (e.g., like a Chase Routing Number).

- Account Number: The second set of numbers (usually 9-12 digits) immediately to the right of the routing number. This is your unique identifier at that bank.

- Check Number: Usually in the upper-right corner and as the last set of digits at the bottom right. They should match.

Stare at a check long enough and it looks like musical notation. Except one wrong note can freeze your cash. I’m a retired planner who’s watched six-figure checks bounce over a single misplaced digit. Stick with me for five minutes; you’ll read a check like a pro, dodge the new 2026 hold limits, and sleep better knowing a fraudster can’t reroute your rent.

Ever had a payment delayed because of a misread check number?

A) Yes, it was a nightmare!

B) Nope, I’m a check wizard!

C) Not sure, that’s why I’m here!

For a deeper dive on how to physically fill out a check, see my guide on How to Write a Check or Fill Out a Check.

💡 Avoid Check Fraud & Banking Disasters

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Spot the red flags scammers exploit

- → Protect your routing & account numbers

- → Sidestep the costly mistakes I’ve seen happen

How To Read a Check: Your Check’s Anatomy Under the Microscope

Think of a check as a financial instrument with its own language. That string of numbers at the bottom? That’s the MICR (Magnetic Ink Character Recognition) line . Designed for machines, but crucial for you to understand.

Interactive Check Routing and Account Number Locator

To see exactly where these numbers are on a typical check, explore our interactive locator tool below.

Hover or click on the highlighted areas of the check to learn more:

Interactive Check Parts Explorer

Hover over or tap the fields below to learn about each part of a check.

123 Main Street

Anytown, USA 12345 Payer Information Name and address of the account holder.

101 Check Number (Top-Right) Sequential check ID. Matches MICR check number.

Order Of

💡 Found this useful? Share the insight:

🎯 Get Smarter About Banking & Money

Receive one clear, actionable money move each week—designed to help you:

- Sidestep costly banking fees & penalties

- Master check fraud prevention strategies

- Apply proven financial playbooks in minutes

✅ Join thousands of readers already protecting their wealth.

📬 No spam. Unsubscribe anytime.

Did you know:

- The average check contains 100+ numbers and codes for processing payments through banks

- Checks with mismatched account/routing numbers have double the rejection rate and delays

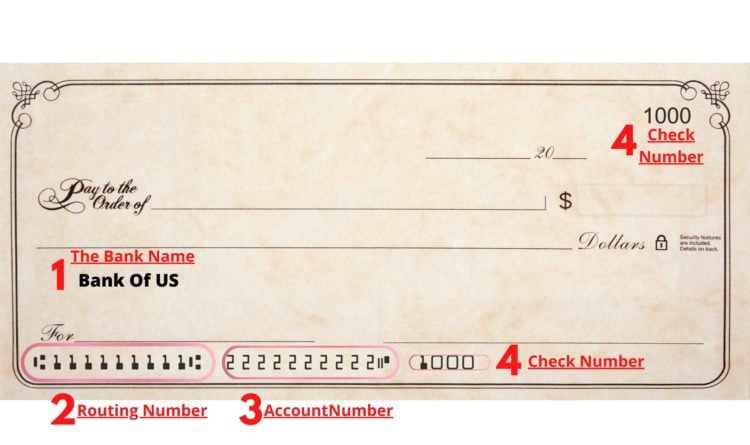

1. The Routing Number: Your Bank’s Fingerprint (Always 9 Digits)

- Where is it? Bottom-left corner. It’s always 9 digits. This is mandated by the American Bankers Association (ABA).

- What’s its job? This is the ABA Routing Transit Number (RTN). It tells other banks and the Federal Reserve which specific financial institution your account belongs to.

It’s essential for ACH transfers, direct deposits, and wire transfers. Are routing numbers always 9 digits? Yes, find out more here. - Michael Ryan Money Insider Tip:

Got multiple accounts at the same bank? They’ll likely share the same primary routing number. But if you opened accounts at different branches in different states, or if your bank merged, these can differ.

When in doubt, check your bank’s official website or a recent bank statement for the most accurate routing number, especially for setting up Chime Direct Deposit or similar services.

I had a client, Sarah (a small business owner), whose payroll for a new employee went astray for a week because she used an old routing number. A costly, frustrating mistake. - The Fractional Routing Number (The Ghost on Your Check): See that fraction in the upper-right corner, like

67-890/1234? That’s an older, manual system version of the routing number. For 99% of what you do, focus on the MICR line.

2. The Account Number: Your Personal Vault ID (Varies in Length)

- Where is it? Right after the routing number in the MICR line. The length can vary (typically 9-12 digits).

- What’s its job? This pinpoints your specific account at that bank. This is the number you guard closely. For instance, your Vanguard Account Number will be unique to you.

- Michael’s “Been There, Fixed That” Moment:

A young client, Jamal, setting up his first direct deposit, accidentally gave his check number as his account number. His first paycheck? Vanished into the digital ether for three stressful weeks.

Always double-check the order: Routing first, THEN Account. - Leading Zeros Matter! Some account numbers start with zeros. If you’re typing it into a form, include those zeros. Dropping them is a common reason direct deposits or payments get rejected.

3. The Check Number: Your Personal Transaction ID

- Where is it? Typically in two places: the upper-right corner of the check and as the last set of numbers on the MICR line.

- What’s its job? It’s a sequential number to help you (and the bank) track individual checks.

- Fraud Alert: If the check number in the top right doesn’t match the one at the end of the MICR line, that’s a massive red flag for a potentially altered or counterfeit check. Don’t accept it.

Learn more about avoiding scams in my Zelle Scams guide – similar vigilance applies.

Why This Still Matters in a Digital World (Security & Avoiding Headaches)

“Michael” you might say, “checks are dinosaurs!” And you’re partly right. But they’re still used, especially by businesses and for certain government payments. And the numbers on them are the backbone of digital payments too.

Direct Deposits & ACH:

Your employer, Social Security, the IRS – they all need your correct routing and account numbers. Get it wrong, and your money gets delayed. If you’re wondering “Why is my direct deposit late?” (Why Is My Direct Deposit Late?), incorrect numbers could be a reason.

Check Washing & Fraud:

Scammers can “wash” checks (chemically alter them) using your legitimate numbers.

I once had to help Robert, a retiree, navigate a nightmare where his stolen Social Security check was washed and cashed for thousands.

Mobile Deposits & MICR Errors:

When you snap a photo for Chase Mobile Check Deposits or Chime Mobile Check Deposit, your phone’s camera needs to clearly read that MICR line.

If it’s smudged or cropped, the deposit can be rejected. Some banks also have hold times, like the 7 Day Hold on Check Chase.

The Check 21 Act & “Stale” Checks:

This act [Federal Reserve page on Check 21 Act] allows banks to process digital images of checks. While banks can refuse checks older than 6 months, sometimes older checks can still slip through.

Michael’s Take:

Everyone says checks are dead, but the information on them is more alive than ever. It powers many digital money movements. Master these numbers.

“Can Someone Steal My Money With Just My Routing and Account Number?”

This is a common fear. The short answer: Yes, potentially, but it’s not simple.

- Fraudulent ACH Debits: A scammer could try an unauthorized ACH debit. Monitor your bank statements and dispute unauthorized transactions immediately [FTC.gov on disputing fraudulent charges].

- Counterfeit Checks: They could print fake checks.

Your Best Defense:

- Guard your checks.

- Monitor your account regularly.

- Shred old checks/statements.

- Never give these numbers out via unsecure email or over the phone unless you initiated the contact with a trusted entity.

Yes, this sounds a bit like a spy movie, but in my 28 years, I’ve seen enough financial espionage to know that a little paranoia pays off.

💡 Avoid Check Fraud & Banking Disasters

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Spot the red flags scammers exploit

- → Protect your routing & account numbers

- → Sidestep the costly mistakes I’ve seen happen

Finding Your Numbers Without a Physical Check

No checkbook handy?

- Online Banking Portal: Most reliable source.

- Bank Statement: Will have your account number. Verify routing for electronic use.

- Call Your Bank.

- “Voided Check” Generator (Some Banks).

Your 72-Hour Challenge: Become a Check Number Pro

- Locate Your Numbers: Identify your routing, full account number (inc. leading zeros!), and a check number.

- Inspect a Check: Look for security features.

- Review Your Last Bank Statement: Spot any unrecognized transactions?

This isn’t just an exercise; it’s building a reflex for financial security. The details matter.

Downloadable: My “Two-Minute Check Security Checklist” to keep these tips handy

Final Thoughts from Your Friendly Retired Planner

Checks might feel old-school, but the numbers on them are keys to your financial kingdom. Understanding them is fundamental to protecting your hard-earned money.

What’s your biggest fear or confusion about checks or these numbers? Share in the comments below – I read and reply to every one!

Next up: Why that “fractional routing number” still appears on checks and the one time you might actually need it (it’s rarer than a sensible tax code, but it happens!)

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.