Hi, I’m Michael Ryan, a retired financial planner. After 25 years of guiding individuals, families, and business owners through the financial maze, I’ve seen firsthand what works and what doesn’t.

So many people wrestle with the idea of creating a spending plan because they think it’s too difficult, too restrictive. But what if I told you a realistic spending plan is the key to unlocking financial freedom, not limiting it?

Ready to ditch the chaos and finally take control of your money in 2025? Are you struggling to make your income stretch far enough? Tired of feeling like you’re constantly one unexpected expense away from financial disaster?

I’ve been there. And I can tell you that a solid, actionable plan will change things for the better.

In this guide, we’ll get into the psychology of overspending, debunk common budgeting myths, and build a customized spending plan that aligns with your unique lifestyle and goals. But don’t worry – this isn’t some stuffy financial lecture.

Consider this your personal finance cheat sheet from someone who’s seen it all. Let’s get started! But first, play around with the spending plan tool I created for you, below.

Spending Plan and Budget Worksheet

Your Personalized Spending Plan

Adjust the sliders to create a budget that works for you.

Your Budget Breakdown

Needs: $2500

Wants: $1500

Savings/Debt: $1000

TL;DR Key Takeaways: Creating The Right Spending Plan For You

- Why do most traditional budgets fail?

They fail because they ignore the human element. Rigid, unrealistic restrictions lead to burnout and overspending. Think flexible “budget buckets,” not ironclad rules. - How can I make budgeting less boring?

Make it a game! Automate the basics, track your progress, and reward yourself (within reason, of course). A little fun can go a long way in staying motivated. - Is a spending plan right for me, even if I’m not in debt?

Absolutely! A spending plan isn’t just for those struggling with debt. It’s a powerful tool for achieving any financial goal, from saving for retirement to buying a home. - How can I track my spending without getting overwhelmed?

Use technology to your advantage! Budgeting apps and spreadsheets can automate the process and provide valuable insights into your spending habits. Find the right tool to help minimize friction. - Does a spending plan need to be set in stone forever?

Never! A successful spending plan is a living document that evolves with your life. Review and adjust your plan regularly to stay on track with your changing needs and goals.

Why Traditional Budgets Fail (And How to Fix Yours)

Ever wonder why so many well-intentioned budgets bite the dust before February? It’s not your fault—it’s often the approach!

Best Budgeting Methods Comparison

| Method | Best For | Success Rate |

| Zero-Based | Detail-oriented users | 78% |

| 50/30/20 | Beginners | 82% |

| Envelope | Cash users | 75% |

| 90/10 | Minimalists | 80% |

Learn more about the Benefits of budgeting and why it’s important

A household spending plan can be defined as “a method for distributing your income among the mix of things you want and need“

according to the University of California, Berkely.

The Psychology of Overspending

Ever find yourself buying yet another gadget, even when you promised to save money this month?

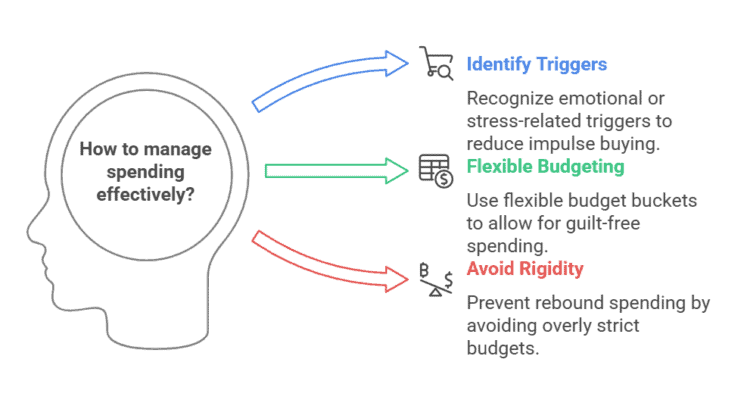

According to a 2025 NBER Study, traditional budgets often crumble because they ignore the most unpredictable factor: human behavior. Stress triggers spending!

Buying isn’t just a logical decision; it’s often a response to emotional needs, stress, or those oh-so-tempting marketing triggers (we’re looking at you, midnight snack ads).

I once worked with a client—let’s call her Maria—who was constantly derailing her budget with impulse clothing purchases. We discovered it was a way for her to cope with work stress. Once she identified that trigger, she started practicing yoga instead, and her spending significantly decreased.

In the world of budgeting, rigidity can lead to failure. Dr. Sarah Johnson points out that feeling deprived can spark “rebound spending,“ where a single splurge turns into a spending spree.

Think of your willpower like a phone battery; it drains throughout the day. A budget that relies entirely on willpower is like trying to run your phone on 1% all day—inevitably, it’s going to fail!

Instead of rigid line items, consider flexible “budget buckets,” where you allocate segments for essentials and a little for fun—hello, 90/10 rule! That’s 90% for essentials and saving, with 10% guilt-free spending.

How to create a spending plan that aligns with your lifestyle

How to Manage Emotional Spending Triggers

Behavioral finance apps can be your virtual therapist, using reminders and gamified savings goals to keep you on track.

Behavioral Finance Tools Quick Guide:

- Spending Tracker Apps

- Goal Visualization Tools

- Automated Savings Features

- Budget Alert Systems

Key Takeaways

- Flexibility is key: Rigid budgets often fail because they don’t account for human behavior.

- Identify triggers: Understand what drives your spending and find healthier alternatives.

- Use tools: Leverage apps and tools to automate and simplify your budgeting process.

Ready to take the next step? Let’s cover a few common myths about spending plans. And how to set up a budget that will work for you.

Common Budgeting Myths Debunked

Budgeting doesn’t have to feel like a tightrope walk across Niagara Falls! Let’s bust some myths:

Myth 1: You need a huge income to budget effectively.

Reality: Budgeting isn’t about how much you earn but how you manage it. Have fun with it! Assign funds to entertainment so you can enjoy guilt-free outings.

Myth 2: Budgeting is restrictive and boring.

Reality: It’s only boring if you make it! Think of it as a game—can you find creative ways to save, and then reward yourself (without breaking the bank, of course)? Think new book, not new car.

As Paula Pant from Afford Anything beautifully says, “Budgeting isn’t about restriction; it’s about creating freedom by aligning your spending with what truly matters to you.”

Myth 3: Budgeting is only for people in debt.

Reality: Even if you’re debt-free, budgeting helps ensure you’re saving effectively and spending in alignment with your values.

Learn more about How to create a spending plan that aligns with your lifestyle and Debunking myths about personal finance

Actionable Steps to a Realistic Budget

Unlike a budget, which looks backward, a conscious spending plan allows you to look forward”

Best-Selling Author Ramit Sethi

- Identify Your Triggers: Recognize emotional spending habits. Are stress or boredom frequent drivers? Awareness is the first step. How mental budgeting improves financial well-being

- Become a Spending Detective: Start noticing what situations or emotions make you want to overspend. Keeping a journal can really help!

- Use Budget Buckets: Create flexible spending categories instead of rigid restrictions. This helps in accommodating life’s unpredictability.

- Try Behavioral Apps: Get an app. Stop impulse buys. Save big.

- Implement the 90/10 Rule: Allocate 10% of your budget for “just because” moments, ensuring you don’t feel deprived.

- Review and Adjust: Budgeting is not a set-and-forget task. Regularly review your spending and adjust as needed to align with your goals.

In summary, budgets don’t have to be your enemy. With the right mindset and tools, you can manage your money while still enjoying the occasional splurge.

Spreadsheets – Excel, Google Sheets, or Airtable provide free and customizable household budget templates to populate with your categories and actual figures. Great for understanding cash flow at a glance. Read our recent article about creating and using a budget template and worksheet for free.

How To Create a Spending Plan (or budget) That Will Work For You

I will walk you through the steps to creating a successful spending plan. Based on my experiences of what works. And what doesn’t.

Now, if you are more of a visual learning, here’s a helpful Youtube video that will help work in combination with the article.

Step 1: Calculate Your True Income – Accounting for Taxes and Side Hustles

When it comes to budgeting, knowing your net income—the actual cash that lands in your bank account—is crucial. A Bank of America study highlights that 40% of American workers have a secondary income source, further complicating income calculations.

Freelancers and gig workers, you’ll need to account for those self-employment taxes. In 2024, the average freelancer paid 25-30% of their income in taxes (Source: Freelancers Union).

Budgeting for Irregular Income

Carol, bless her heart, was a hot mess when it came to her freelance income. One month she’d be rolling in dough, the next she’d be scraping by. But then she discovered YNAB, and everything changed!

Practical Tip: Establish a “buffer fund” to handle those months when income is lower than usual. This fund becomes a safety net, providing peace of mind and financial flexibility.

Michael Ryan Tip: Start small—even $50 a month can make a difference. Treat it like an essential bill that needs to be paid each month!

Step 2: Track Expenses Without Obsession – Apps vs. Spreadsheets: What Works Best?

Apps track expenses. Let’s break it down:

Top Budgeting Apps for 2025:

- YNAB (You Need a Budget): Ideal for those committed to zero-based budgeting. YNAB forces you to assign every dollar a job, helping you reduce overspending and achieve your financial goals.

- Monarch Money: A comprehensive budgeting and financial tracking app that offers collaborative features, making it great for couples or families. It allows for detailed customization and goal setting.

- Empower: Focuses on investment tracking and financial planning, making it a good choice for those looking to manage their net worth, track investments, and get retirement planning advice, in addition to budgeting.

SIGN UP FOR A FREE EMPOWER ACCOUNT TODAY!!

Practical Tip: For those of you who crave customization, spreadsheets might be your best friend. However, if you’re looking to save time, apps can automate much of the heavy lifting while offering visually engaging dashboards.

- Download or print a simple, easy to use: Budget Worksheet

- LINK TO A SPENDING PLAN Spreadsheet

- A simple Google Docs: Spending Plan

How to track expenses effectively

The 48-Hour Rule for Impulse Buys

When confronted by a tempting purchase, employ the 48-hour rule. This simple strategy involves waiting two days before committing to a non-essential purchase. During this period, evaluate if the item is genuinely needed or just an impulse buy.

Behavioral finance apps can support this practice, featuring reminders and nudge features to help curb impulse spending. You might find that two days of reflection reveal a cheaper alternative or that the desire fades entirely.

Personal Anecdote: I was once about to purchase an expensive camera, but I waited, and discovered I was buying the camera for someone else, to impress them. Once they were no longer in the picture, I decided I no longer needed it.

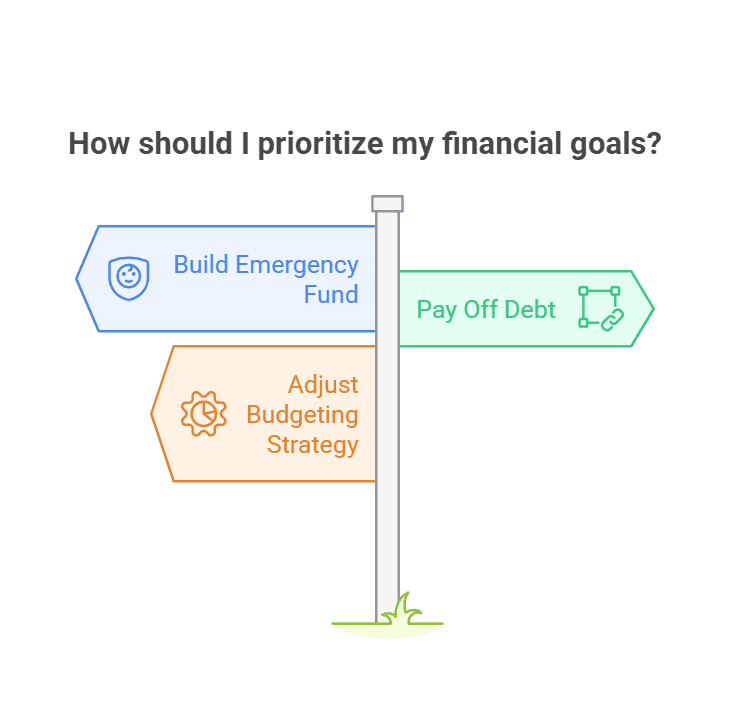

Step 3: Prioritize Goals Like a Pro

Learn more about The Dave Ramsey Baby Steps approach to wealth building

Emergency Funds vs. Debt: What Comes First?

Emergency fund first, or debt? Ah, the classic personal finance dilemma! Dave Ramsey says knock out the smallest debts first, snowball style. Sound easy enough, right?

Now, Dave’s approach works for a lot of folks, but I’m going to play devil’s advocate here. What if you’re living paycheck to paycheck, and a sudden job loss would leave you scrambling? In that case, I’d argue that building a bigger emergency fund is priority number one.

The 50/30/20 Rule Revisited

Popularized by personal finance guru Elizabeth Warren, the 50/30/20 budget —in which 50% of your income goes to needs, 30% to wants, and 20% to savings or paying off debt—can serve as a solid budgeting foundation.

If you’re drowning in debt, consider shifting some of your ‘wants’ allocation to debt repayment. Or, if you’re a super saver, maybe aim for a 40/30/30 split.

To wrap it up, mastering your budget involves more than just crunching numbers. It’s about leveraging tools and techniques to align your financial actions with your life goals. Start today and don’t fear making adjustments along the way. Your wallet—and peace of mind—will thank you.

Step 4: Adjusting Your Plan Without Guilt – Quarterly Budget Audits

Think of your budget like a sourdough starter—you can’t just ignore it and expect it to thrive! It needs regular feeding and attention to ensure it stays healthy.

Every quarter, take some time to audit your budget. What does this mean? You look at your spending patterns, track your progress towards goals, and tweak any categories that seem a bit off course. I strongly suggest you read How To Stop Spending Money as well.

Budget Variance = Plan vs. Reality. Spot the difference to adjust your plan.

As Ramit Sethi, author of “I Will Teach You to Be Rich,” says, “Automating savings is the easiest way to build wealth over time. Set it and forget it—but don’t forget to review it!”

Practical Tip: Use this audit time to automate part of your savings if you haven’t yet. Try: Save now. Effortlessly.

How to conduct a quarterly budget audit

Celebrating Small Wins

Who doesn’t love a victory dance, right? Especially when it’s about personal finance! Acknowledging your progress towards financial goals, no matter how small, can be a powerful motivator. Did you save a little more than expected this month? Did you stick to your grocery budget? Celebrate these achievements!

Personal Anecdote: When I paid off my first credit card, I didn’t go wild, but I did treat myself to a fancy coffee. It was a small reminder that my hard work was paying off!

This recognition can prevent burnout and maintain motivation. Remember, it’s okay to reward yourself within reason. Perhaps a little treat or simple pleasures help reinforce positive behavior without going overboard.

What is too much to spend on a reward?

Step 5: Real-World Examples, Misconceptions, and Mistakes

Misconceptions often lurk around personal finance, creating confusion or poor financial habits.

Misconception 1: Budgeting is Restrictive.

Reality: Budgeting empowers you to control your money so it doesn’t control you. Allocating funds for entertainment or hobbies can bring enjoyment without the guilt.

Misconception 2: Automation Solves Everything.

Reality: While automation helps simplify financial management, manual reviews are crucial to prevent surprise subscriptions or fees.

Common Mistake: Ignoring Irregular Expenses.

Solution: Setting up a sinking fund can prepare you for unpredictable expenses like car repairs or holiday gifts, reducing financial strain.

Be sure to take a look at a recent article on Common reasons budgets fail

Visual Progress Tracker:

- Monthly Milestone Chart

- Savings Thermometer

- Debt Payoff Visualization

- Goal Achievement Timeline

As you draw up and refine your financial plan for 2025, remember that perfect plans don’t exist—only ones that get better with practice and iteration. Keep tweaking and celebrating your progress, and soon enough, you’ll find your financial rhythm!

By integrating these steps and understanding behavioral finance concepts like nudge theory, you can make smarter financial decisions and set the stage for a more informed and financially stable year.

Now that you understand the fundamentals of household budgeting, below are recommended resources for deepening skills:

- Continuing to visit Michaelryanmoney.com

- Sign up for our personal finance newsletter here

- Read our reviews of personal finance books

- Government Agencies such as Consumer Financial Protection Bureau (CFPB) or the Internal Revenue Service (IRS)

- Non-Profit Organizations like National Endowment for Financial Education (NEFE), JumpStart Coalition for Personal Financial Literacy or the FPA

- Financial Experts such as Dave Ramsey, Suze Orman, Barbara Corcoran, Robert Kiyosaki or Jean Chatzky

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.