You’ve heard the common advice a thousand times: “stop buying lattes,” “track your spending,” “cut subscriptions.” And while that’s not wrong, it’s also not the reason most budgets fail.

In my nearly 30 years as a financial planner, I saw that budgets don’t break because of a $5 coffee. They shatter under the weight of silent, structural flaws that generic advice never addresses.

To confirm this, I did a deep dive into the modern financial battlefield: Reddit. I analyzed thousands of posts from real people on forums like r/personalfinance, and their stories confirmed what I saw in my practice for decades.

This isn’t another list of tips. This is a unique framework identifying the hidden mistakes that derail real-world budgets.

We’ll explore the real mistakes people make, diagnose why they happen with insights from my planning career, and give you the specific strategies to fix them for good.

📌 The Real Reasons Budgets Fail: Forget lattes. My 25 years of experience and analysis of real Reddit stories show budgets fail due to hidden mistakes: ignoring non-monthly expenses (Sinking Funds), getting raises without a plan (Lifestyle Creep), and demanding perfection instead of building in flexibility.

Key Takeaways Ahead

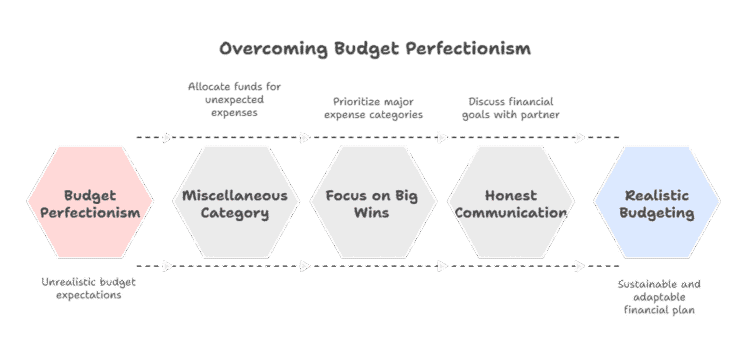

Mistake #1: The Perfectionist Prison: Why Your “Perfect” Budget Always Fails

Before a single number is written down, most busted budgets are already set up to fail because of two psychological traps.

Common Budget Buster

I read countless posts from users who spend hours crafting a perfect, color coded spreadsheet that allocates every single dollar. They stick to it for five days, then a friend invites them out for an unplanned $30 dinner.

The budget “breaks,” they feel like a failure, and they abandon the entire system in frustration.

The Michael Ryan Money Diagnosis

This is the “Perfect is the Enemy of the Good” fallacy.

A budget is not a moral document; it’s a data-driven tool. When you demand perfection, any deviation feels like a personal failure. Making you want to quit.

This is often driven by the social pressure of keeping up with the Joneses, where we feel our budget must look as perfect as the lives we see online.

The Strategic Fix

- Build a “Miscellaneous” Category:

This is non-negotiable!

Allocate 5% of your take-home pay to a category literally named “Whoops,” “Life Happens,” or “Miscellaneous.”

This gives you permission to be human without breaking your system. - Focus on “Big Wins,” Not Micro Management:

Don’t track every penny.

Focus on getting your three biggest expenses right: Housing (under 30% of take-home), Transportation, and Food.

If you nail those, the occasional latte is irrelevant.

A great spending plan prioritizes the big rocks first.

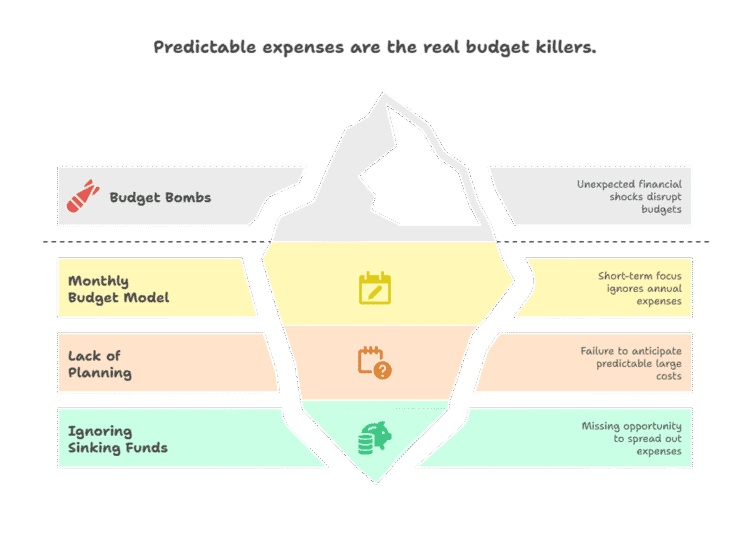

Mistake #2: The Monthly Budget Trap: Ignoring Predictable “Budget Bombs”

This is without a doubt, the single biggest structural mistake I’ve seen. People build budgets for a perfect, 30-day cycle. But real life doesn’t work that way. At least mine doesn’t.

The Reddit Story

A user posts in a panic in July: “My budget was going perfectly, but then my $600 car insurance premium and my $150 Amazon Prime renewal hit in the same week and I’m completely broke. I have to put groceries on my credit card.”

Michael Ryan’s Diagnosis

This isn’t an emergency; it’s a predictable expense that the monthly budget model is uniquely terrible at handling.

These “budget bombs” are what truly destroy financial progress, not daily spending. Understanding the benefits of budgeting means planning for the entire year, not just the next 30 days.

The Strategic Fix

Time-Shift Your Expenses with Sinking Funds. A sinking fund is a mini-savings account for a specific, future expense. You break down the large cost into small, automated monthly savings goals.

This turns a budget-breaking panic into a completely boring, planned-for transaction.

| Predictable “Budget Bomb” | Total Cost | Monthly Sinking Fund Contribution |

|---|---|---|

| Annual Car Insurance | $1,200 | $100 / month |

| Holiday Gifts | $600 | $50 / month |

| Car Registration / Tabs | $240 | $20 / month |

| Annual Subscriptions (Prime, etc.) | $180 | $15 / month |

Want to Dodge Costly Money Mistakes?

Get short, practical emails that help you sidestep common budgeting traps and make smarter financial decisions. Learn it once—profit for years.

Join thousands of readers just like you.

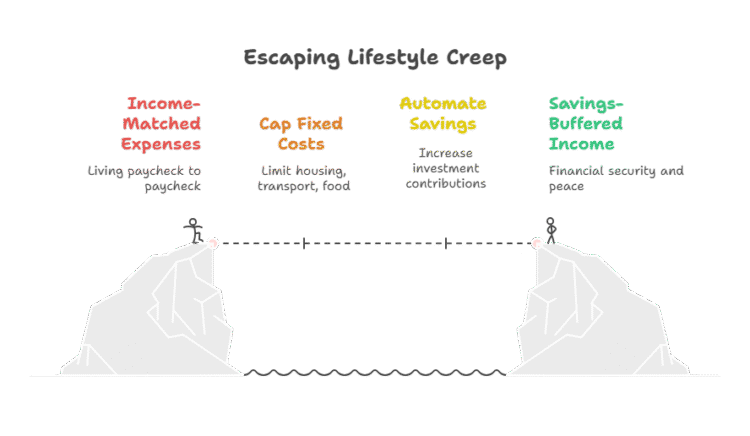

Mistake #3: The “Lifestyle Creep” Ambush: When a Raise Makes You Poorer

This mistake is subtle because it feels like a reward. You get a raise, and your lifestyle quietly expands to meet your new income, leaving you feeling just as broke as before.

The Lifestyle Creep Story

A couple saw their income grow from $80,000 to $120,000 over three years. Instead of saving the difference, they upgraded their home and cars, locking over 50% of their take-home pay into fixed costs.

When one of them faced a potential layoff, they had almost no savings buffer.

The Planner’s Diagnosis

This is Lifestyle Creep, and it’s the default setting for human behavior. Without a plan, new money gets spent. The most dangerous form is when it inflates your fixed expenses (housing, transportation), as these are the hardest to cut in an emergency.

You can learn more in our deep dive on how to avoid lifestyle creep.

The Strategic Fix

- Cap Your “Big 3”:

Create a hard rule that your fixed costs for Housing, Transportation, and Food will not exceed 50% of your take-home pay.

Before any major upgrade, calculate the new percentage. If it breaks the rule, the answer is no. - Automate Your Raise:

The day you get a raise, log in to your 401(k) or IRA and increase your automatic investment contribution by at least a third of the new amount.

You can’t spend what you never see.

What The Experts Say About Budget Mistakes People Make

- “A budget tells us what we can’t afford, but it doesn’t keep us from buying it.” – William Feather

- “A budget is telling your money where to go instead of wondering where it went.” – Dave Ramsey

- “The budget is not just a collection of numbers, but an expression of our values and aspirations.” – Jacob Lew

- “A budget is more than just a series of numbers on a page; it is an embodiment of our priorities.” – Barack Obama

- “The most important principle of budgeting is to keep a sustained focus on your long-term financial goals.” – Suze Orman

Mistake #4: The 50/30/20 Lie: Forcing Your Life into a Generic Box

The internet is full of one size fits all budget rules, but personal finance is personal.

The 50/30/20 Budget Story

A user in San Francisco posted their frustration with the popular 50/30/20 Rule. With their rent for a small apartment consuming nearly 50% of their income alone, the rule made them feel like a constant failure.

The Michael Ryan Money Diagnosis

Generic rules are a starting point, not gospel. Forcing your unique life into a generic template is a recipe for failure. Your budget must reflect your local cost of living and, most importantly, your personal financial goals.

The Strategic Fix

- Create a Localized Budget:

Use a tool like the MIT Living Wage Calculator to understand the actual cost of living in your specific county. This will give you a realistic baseline for your “Needs” category. - Budget Based on Your Values:

If travel is your passion, it’s okay to allocate 15% of your budget to it, as long as you mercilessly cut back on things you don’t care about, like owning a new car or buying designer clothes.

50/30/20 Budget Rule Calculator

Compare your monthly spending with the 50/30/20 budgeting guideline. The percentages are flexible reference points, not requirements.

Your Budget Snapshot

This comparison shows how your entered amounts line up with the guideline.

| Category | Guideline target | Your amount | Comparison |

|---|---|---|---|

| Needs | $0 50% | $0 0% of income | — |

| Wants | $0 30% | $0 0% of income | — |

| Savings and additional debt repayment | $0 20% | $0 0% of income | — |

Needs

Actual percentage of monthly income

Wants

Actual percentage of monthly income

Savings and debt repayment

Actual percentage of monthly income

What your numbers suggest

About the guideline: The 50/30/20 approach is a general budgeting framework, not a required allocation. Housing costs, healthcare, caregiving, debt, taxes, location, income level, and retirement circumstances can make different percentages more appropriate.

This calculator provides educational estimates based only on the amounts entered. It does not provide personalized financial, investment, tax, legal, insurance, or debt advice.

See a problem or have a suggestion? Contact Michael Ryan Money .

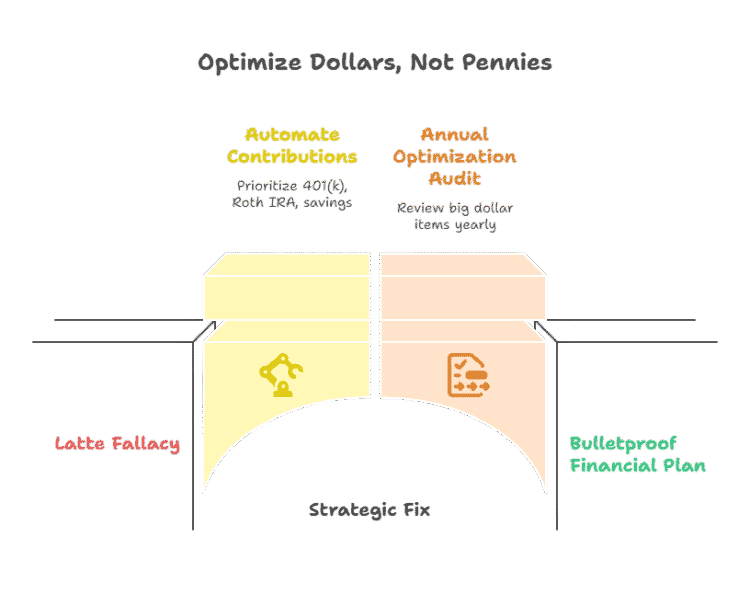

Mistake #5: The “Latte Fallacy”: Optimizing Pennies While Ignoring Dollars

This is a mistake even the most diligent budgeters make. They focus on clipping coupons while leaving five figure sums on the table.

The Reddit Story

A user on r/financialindependence shared how they had “optimized” their budget, saving an extra $100 a month. However, they had neglected to increase their 401(k) contributions after several raises, missing out on an estimated $50,000 in potential compound growth over the next decade.

The Planner’s Diagnosis

The human brain is wired to focus on small, tangible wins. It’s easier to feel good about saving $5 on coffee than it is to calculate the long term benefit of increasing your investment rate from 8% to 10%.

This leads to optimizing the pennies while ignoring the dollars.

The Strategic Fix

- Prioritize the Big Three Automations:

Your budget’s primary job is to automate three things in this order:

1) Contribute enough to your 401(k) to get the full employer match.

2) Max out your Roth IRA (learn how to start a Roth IRA here).

3) Increase your 401(k) contribution until you reach a total savings rate of at least 15%. - Schedule an Annual “Optimization Audit”:

Once a year, spend one hour reviewing these “big dollar” items.

This single hour is more valuable than 40 hours of coupon clipping.

Build a Bulletproof Financial Plan

-

Follow a Proven Financial Framework

Integrate your new budget into a complete plan for debt, emergencies, and investing with the 7 Baby Steps.

-

Try a Tactile Budgeting Method

For a hands-on approach to controlling spending, explore the cash stuffing and envelope budget system.

-

Accelerate Your Savings Goals

Ready to supercharge your new budget? Discover 15 proven ways to save money quickly.

From Mistakes to Mastery: Your New Budget Blueprint

The real reason budgets fail isn’t a lack of willpower; it’s a lack of the right system. By moving beyond the generic advice and fixing these five hidden budgeting mistakes, you’re no longer just tracking numbers. You’re building a resilient, real world financial plan that accounts for human nature.

Forget the shame and frustration. Use the power of Sinking Funds to eliminate surprises from non-monthly expenses. Actively fight Lifestyle Creep by automating your raises into a “pay yourself first” system. And abandon generic templates like the 50/30/20 Rule for a personalized plan that reflects your values. This is the blueprint that turns a budget from a prison into a pathway to true financial freedom.

Now, try searching for: sinking funds, how to stop lifestyle creep, or pay yourself first.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.