Are you staring down the barrel of Required Minimum Distributions (RMDs) and wondering if you can just lump them all together? As someone who spent over 25 years as a financial planner helping folks understand retirement rules, this is one of the most common questions I’ve encountered.

Once you hit age 73 (thanks, SECURE 2.0 Act!), these mandatory withdrawals become a reality, and getting them wrong can lead to some pretty nasty IRS penalties. Nobody wants that.

The good news? For certain accounts, particularly your traditional IRAs, the IRS does offer some welcome flexibility that can simplify your life and even your tax situation. But – and this is a big “but” I’ve seen trip up even savvy investors – the rules are not a one-size-fits-all.

What works for your IRAs is generally a no-go for your 401(k)s, although 403(b) accounts have their own special aggregation rule. Understanding these RMD aggregation rules is crucial for a smooth retirement.

This isn’t just about reciting IRS jargon; it’s about giving you the practical real-world insights I’ve gained from decades of experience. So you can make informed decisions, avoid costly mistakes, and keep more of your money. We’ll look at

- What RMD’s you can combine

- What you absolutely can’t

- And some insider tips that can make managing your RMDs a whole lot less stressful.

RMD Aggregation MythBuster

Test whether you know which Required Minimum Distributions may be combined and which must remain separate.

Quiz Complete

Looking For a Quick Answer:

For most traditional, SEP, and SIMPLE IRAs, yes, you can calculate the RMD for each account separately and then withdraw the total RMD amount from just one, or a combination, of those IRAs.

However, for 401(k)s and most other employer-sponsored retirement plans, you must take the RMD separately from each account. A key exception is 403(b) accounts: you must calculate the RMD for each 403(b) separately, but you can generally aggregate those amounts and withdraw the total from one or more of your 403(b) accounts.

Inherited IRAs have their own specific, often complex, aggregation rules too, which we’ll untangle.

Let’s tackle this RMD puzzle piece by piece.

First – What Exactly is RMD Aggregation and Why Should You Care About Combining RMDs?

Before we get into the nitty-gritty, let’s make sure we’re on the same page. “RMD aggregation” simply means combining the total Required Minimum Distribution amount you owe from multiple similar retirement accounts and taking that total sum from just one (or a few) of those accounts. Rather than making separate withdrawals from each.

This understanding is the first step in correctly applying RMD aggregation rules.

Why does this even matter?

Trust me, after helping countless clients like Susan… A retired HR executive who just wanted her retirement to be simple, I can tell you that RMD aggregation (when done right) offers some real perks:

Streamlined Management:

This is the big one. Instead of juggling multiple withdrawals from, say, three different IRAs, you make one. Less paperwork, fewer transactions to track. It just makes life easier.

Think of it like consolidating your grocery list before you head to the store; one trip, one checkout.

Reduced Risk of Errors:

With fewer withdrawals to manage, there’s less chance of accidentally missing an RMD from one account. And believe me, missing an RMD isn’t a small oopsie.

The IRS can slap you with a hefty 25% penalty on the amount you failed to withdraw. Though this can sometimes be reduced to 10% if corrected promptly – a detail many overlook, as per IRS Form 5329, Additional Taxes on Qualified Plans.

Potential Tax Efficiency:

This is where a bit of strategy comes in. If you have multiple IRAs with different investment mixes, you might prefer to take the RMD from certain accounts. Such as an account holding more cash or assets you were planning to sell anyway, rather than being forced to sell investments in another IRA that you’d rather leave untouched.

It gives you a smidge more control over your asset allocation for retirees.

Simplified Recordkeeping:

Fewer transactions mean a cleaner paper trail when it comes to tax time and your own financial tracking.

I remember my client Dave, a sharp business owner who had meticulously saved across several IRAs. He loved the idea of aggregation because it allowed him to pinpoint which IRA to take the full RMD from. Often choosing one that had investments he felt were ripe for rebalancing.

It was a small tactical advantage, but Dave was all about maximizing every angle to optimize his retirement plan distributions.

The Golden Rule of RMD Aggregation: Combining RMDs for Your IRAs

Alright, let’s get to the core of it. For your own traditional IRAs, SEP IRAs, and SIMPLE IRAs, the IRS is quite accommodating when it comes to combining RMDs.

Here’s how it works for these IRAs (as clarified in IRS guidance like Notice 2002-27):

RMD Calculator for 2026

Estimate 2026 owner required minimum distributions across multiple IRAs and workplace retirement accounts using December 31, 2025 balances.

Estimated 2026 RMD Summary

| Account | Type | 2025 balance | Estimated 2026 RMD | Status |

|---|

Deadline

Aggregation and withdrawal rules

Important next checks

- Confirm each December 31 balance and any account-specific adjustment with the custodian or plan administrator.

- Confirm whether a current-employer plan permits the still-working delay and whether the owner is treated as a 5% owner.

- Calculate an account separately if a spouse more than 10 years younger is its sole beneficiary.

- Coordinate distributions with income taxes, Medicare IRMAA, charitable giving, Roth conversions, and tax withholding.

- Calculate Separately:

You must calculate the RMD for each traditional, SEP, or SIMPLE IRA you own individually.

This involves taking the account balance as of December 31st of the previous year and dividing it by the life expectancy factor from the IRS’s Uniform Lifetime Table (found in IRS Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs)). - Sum the Totals:

Add up the RMD amounts calculated for all your eligible IRAs.

This grand total is the aggregate RMD amount you need to withdraw for the year from these accounts. - Withdraw Flexibly:

You can then withdraw this total RMD amount from any single one of your traditional/SEP/SIMPLE IRAs, or from any combination of them.

Example:

Tom, a retiree I worked with for years, had three traditional IRAs:

- IRA #1 RMD: $5,000

- IRA #2 RMD: $3,000

- IRA #3 RMD: $2,000

- His total RMD for his IRAs was $10,000 ($5k + $3k + $2k).

Tom could choose to take the entire $10,000 from IRA #1, or $5,000 from IRA #1 and $5,000 from IRA #2, or any other combination that added up to $10,000.

He usually opted to take it all from one to keep things simple, just like Susan preferred. Isn’t that a sigh of relief compared to juggling three separate checks? - Michael’s Key Takeaway for this Section:

- Yes, you can absolutely combine RMDs from multiple traditional IRAs.

Calculate for each, then withdraw the total sum from just one or a mix of them. - For your IRAs, think ‘calculate each, withdraw from one (or few).’ It’s IRS-approved simplicity for RMD aggregation.

- Yes, you can absolutely combine RMDs from multiple traditional IRAs.

The Big Stop Sign: When You CANNOT Aggregate RMDs (A Critical Aspect of RMD Aggregation Rules)

This is where many well-intentioned retirees and even some advisors get tripped up. The flexibility you have with your own IRAs does not extend to most other types of retirement accounts. Failing to understand these distinctions is a common path to RMD penalties.

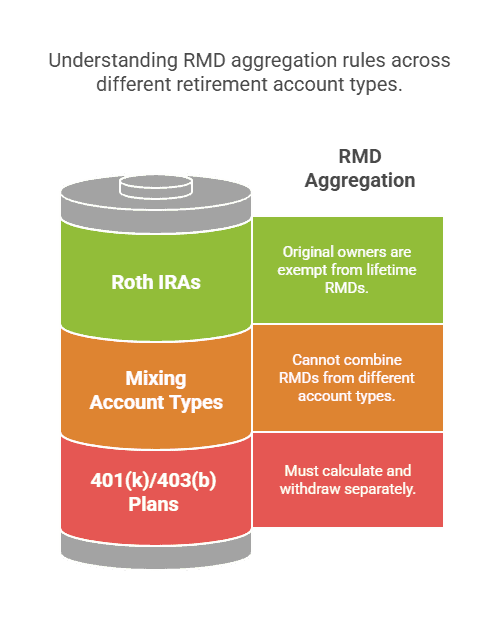

401(k) Plans, 403(b) Plans, and Other Employer-Sponsored Plans

The Rule:

If you have multiple 401(k) accounts (perhaps from different former employers), you must calculate and take the RMD separately from each 401(k) plan. You cannot aggregate the RMDs from different 401(k)s and take the total from just one.

403(b) plans follow a special rule: you must calculate the RMD for each 403(b) contract separately, but you can generally total those RMDs and take the combined amount from one or more of your 403(b) contracts.

Because 403(b) arrangements can be complex, it’s still wise to confirm the details with your plan administrator.

Why the Difference?

From my experience, it boils down to the plan administrator’s responsibility. Each 401(k) or 403(b) plan is its own entity with its own administrator responsible for tracking and reporting RMDs for that specific plan.

Aggregating across different plans would create an administrative nightmare for them and the IRS.

Michael’s Insider Tip:

If you have multiple old 401(k)s, consider rolling them over into a single traditional IRA. Once they are in an IRA, you can then benefit from RMD aggregation for those consolidated funds. This is a strategy I often recommended to clients looking to simplify their RMD landscape.

Of course, consider all factors like investment options and fees before any rollover.

Roth IRAs

The Rule (for Original Owners):

Good news here! Original owners of Roth IRAs are not required to take RMDs during their lifetime. So, aggregation isn’t an issue because there’s no RMD to aggregate in the first place. This is a major advantage of Roth accounts that I always highlighted to clients, sometimes even suggesting a Roth conversion strategy if it made sense for their tax picture.

(We’ll touch on inherited Roth IRAs later, as their rules are different.)

Mixing Account Types for Aggregation? A Definite No.

You cannot, for example, calculate the RMD for your IRA and the RMD for your 401(k), add them together, and take the total from just your IRA. They are treated as entirely separate buckets by the IRS for RMD purposes.

Client Mistake I’ve Seen:

A client once assumed he could cover his 401(k) RMD by taking a larger withdrawal from his IRA. We caught it before the deadline, but it would have resulted in a penalty for the missed 401(k) RMD. It’s a common point of confusion, highlighting why understanding specific RMD aggregation rules is paramount.

Michael’s Key Takeaway for this Section:

- No, you cannot combine RMDs from a 401(k) and an IRA. Each 401(k) plan requires its own separate RMD withdrawal.

- 401(k)s & 403(b)s play by their own RMD rules: one account, one withdrawal. No mixing and matching!

The Complex World of Inherited IRA RMD Aggregation: Navigating Post-SECURE Act Rules

Inherited IRAs are a whole different ball game, and the rules here have seen significant changes with the SECURE Act and subsequent IRS interpretations. This is an area where seeking professional advice is often essential, as incorrect handling of these RMD aggregation rules can be costly.

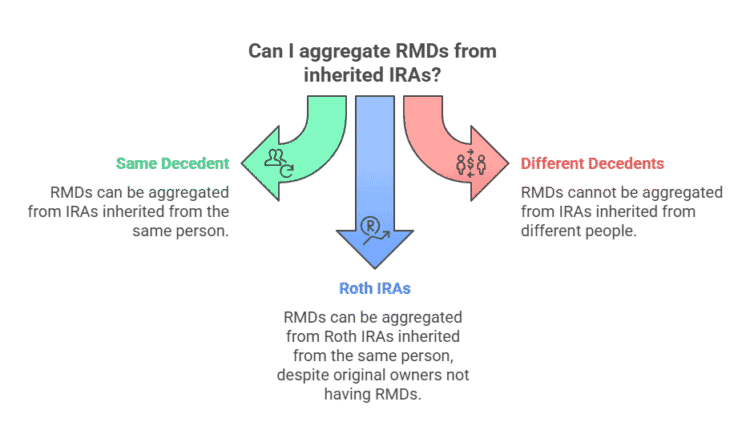

Inherited from the Same Decedent

If you inherit multiple IRAs (of the same type, e.g., all traditional, or all Roth) from the same person, you can generally aggregate the RMDs for those specific inherited IRAs. You’d calculate the RMD for each, sum them, and could take the total from one or a combination of those specific inherited IRAs.

You cannot aggregate RMDs from IRAs you inherited with RMDs from your own IRAs.

Inherited from Different Decedents

If you inherit IRAs from different people (e.g., one from your mother and one from your uncle), you generally cannot aggregate the RMDs for these accounts. Each set of IRAs inherited from a different decedent must have its RMDs calculated and taken separately.

Why this rule?

It likely ties back to tracking the specific distribution rules (like the 10-year rule for many non-spouse beneficiaries under the SECURE Act) associated with each decedent’s original account.

Inherited Roth IRAs

While original Roth IRA owners don’t have RMDs, beneficiaries do.

The aggregation rules for inherited Roth IRAs generally mirror those for inherited traditional IRAs: you can aggregate RMDs from multiple Roth IRAs inherited from the same decedent.

A Common Stumbling Block:

Many beneficiaries are surprised they even have RMDs from an inherited Roth IRA, especially if they’re familiar with the “no RMDs for original owners” rule.

The SECURE Act and its impact on retirement accounts has made these rules particularly complex for non-spouse beneficiaries, often subjecting them to a 10-year withdrawal rule, which may or may not involve annual RMDs depending on the specific situation (e.g., if the original owner had already started RMDs).

This is an area where IRS guidance is still evolving, and professional advice is critical.

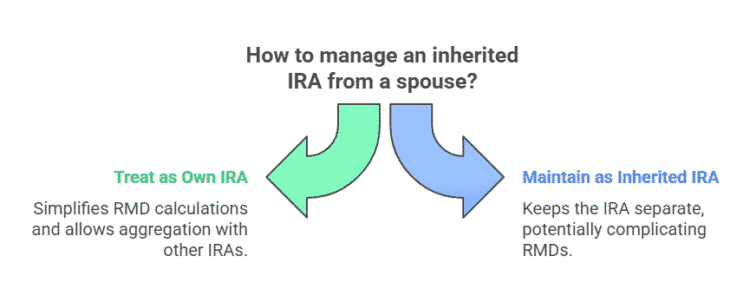

Spousal Beneficiaries – A Special Case for RMD Aggregation

If you inherit an IRA from your spouse, you often have more flexibility. A common option is to treat the inherited IRA as your own by rolling it into your existing IRA or renaming it as your own. If you do this, the RMDs are then based on your own age and life expectancy, and these funds can be aggregated with your other IRAs.

This is a key aspect of spousal IRA rules.

This is usually the most straightforward path for spousal beneficiaries, a strategy I often discussed with clients like Karen. She inherited an IRA from her late husband and rolled it into her own, simplifying her RMD calculations significantly.

Michael’s Key Takeaway for this Section:

- Generally, you can combine RMDs for IRAs inherited from the same person. However, you usually cannot combine RMDs for IRAs inherited from different people, nor can you combine inherited IRA RMDs with your own IRA RMDs. Spouses have special, more flexible options.

- Inherited IRAs? Aggregation gets tricky. ‘Same owner, same rules’ is a good start, but the SECURE Act added twists. When in doubt, ask a pro to ensure compliance with these RMD aggregation rules.

Strategic Considerations: When Combining RMDs Might (or Might Not) Be Best

Just because you can aggregate your IRA RMDs doesn’t always mean it’s the absolute best tactical move from an investment standpoint, though it nearly always wins for simplicity. So, what’s the catch, you ask?

Investment Strategy Alignment

Pulling the entire RMD from one IRA could mean selling assets you’d prefer to hold or unbalancing your desired asset allocation in that specific account. This direct impact on your portfolio is a critical factor when considering RMD aggregation rules.

Michael’s Approach:

I’d often work with clients to see if taking partial RMDs from several IRAs made more sense to maintain their overall investment strategy. For instance, if one IRA was heavily weighted in bonds and another in growth stocks, we might take RMDs proportionally or from the account that best suited their current cash flow needs or rebalancing goals, unlike a less flexible approach that might force suboptimal sales.

Consolidating Accounts for Ultimate Simplicity

While not strictly RMD aggregation, if you have many small IRAs, consolidating them into one or two larger IRAs can make the entire RMD process (and your financial life) vastly simpler year after year. Think of it as financial decluttering.

Client Story (Susan Revisited):

Susan had four small IRAs from previous jobs. We consolidated them into one main IRA. Come RMD time, she had only one calculation and one withdrawal. The peace of mind was palpable for her.

When NOT to Aggregate (Rare, but Possible)

This is an “insider” thought, but very rarely, there might be a specific reason to keep withdrawals separate.

For example, if one IRA holds highly appreciated company stock with specific NUA (Net Unrealized Appreciation) tax benefits you’re trying to manage carefully, you might not want to pull the RMD from that account if other options exist. These are highly specific scenarios best discussed with a tax advisor.

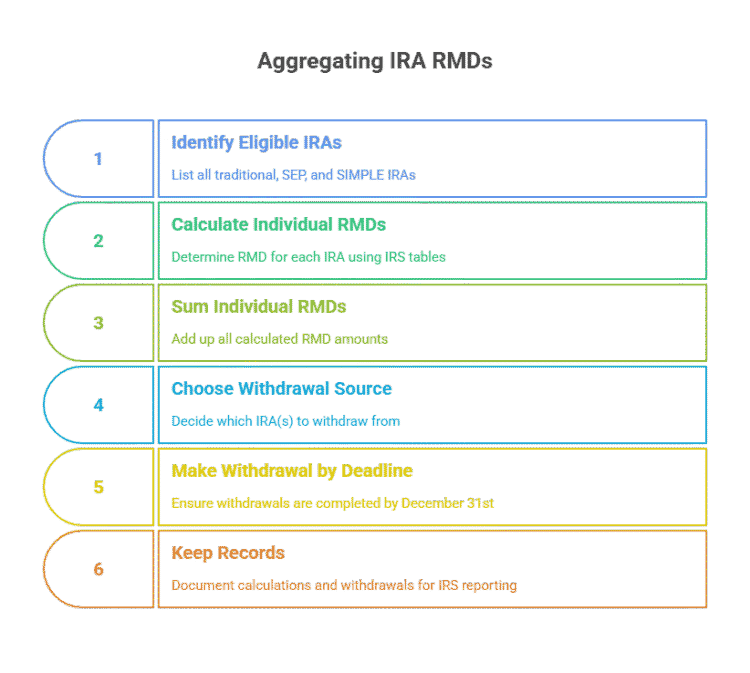

Step-by-Step: How to Aggregate Your IRA RMDs (Your Action Plan for Combining RMDs)

Feeling a bit more confident about the “can I or can’t I?” Let’s walk through the actual steps for aggregating RMDs for your traditional, SEP, and SIMPLE IRAs. This is your practical guide to implementing the RMD aggregation rules.

Step 1: Identify All Eligible IRAs.

Make a list of all your traditional IRAs, SEP IRAs, and SIMPLE IRAs. Exclude Roth IRAs (unless inherited, then see specific inherited rules), 401(k)s, and other employer plans.

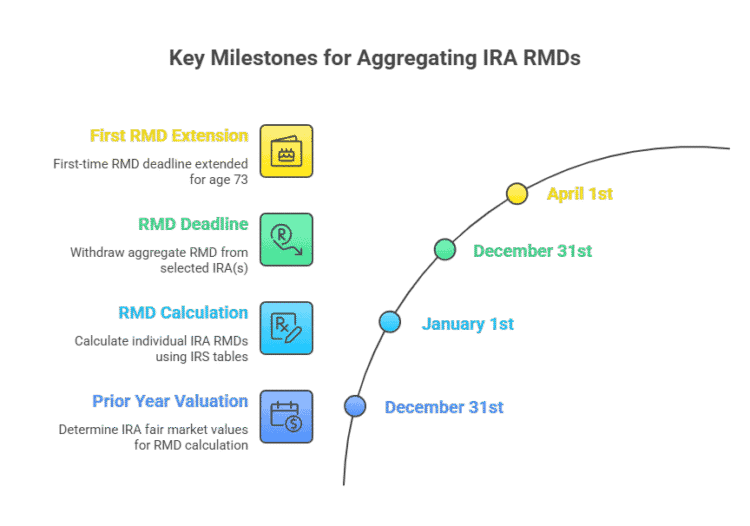

Step 2: Calculate the RMD for Each IRA Individually.

For each IRA on your list, find the fair market value as of December 31st of the preceding year.

Look up your life expectancy factor in the appropriate IRS table (usually the Uniform Lifetime Table in Appendix B of IRS Publication 590-B). You can also find tools like an IRA RMD calculator helpful here.

Divide the account balance by the life expectancy factor to get the RMD for that specific IRA.

(Pro Tip: Many brokerage firms will calculate your RMD for accounts held with them, but it’s your responsibility to ensure it’s correct and that you account for all IRAs you own, wherever they are held.)

Step 3: Sum All Individual IRA RMDs.

Add together all the RMD amounts you calculated in Step 2. This is your total, aggregate RMD for your IRAs for the year.

Step 4: Choose Your Withdrawal Source(s).

Decide which IRA(s) you will take the total RMD from. You can take it all from one, split it 50/50 between two, or any other combination, as long as the total amount withdrawn by the deadline matches your aggregate RMD calculated in Step 3.

Step 5: Make the Withdrawal(s) by the Deadline.

The RMD deadline is generally December 31st of the year the RMD is due. For your very first RMD (for the year you turn 73), you have an extension until April 1st of the following year. However, if you delay that first one, you’ll have to take two RMDs in that following year – something I usually advised clients to avoid if possible, as it can bump up taxable income.

Step 6: Keep Good Records.

Document your calculations and the withdrawals you made. Your IRA custodian will send you (and the IRS) Form 1099-R reporting the distribution.

Common Mistakes to Avoid with RMD Aggregation (And How Michael Ryan Has Seen Them Play Out)

Over the years, I’ve seen a few common pitfalls when it comes to RMD aggregation. Avoiding these can save you a lot of headaches and potential penalties. Are you making any of these common RMD aggregation errors?

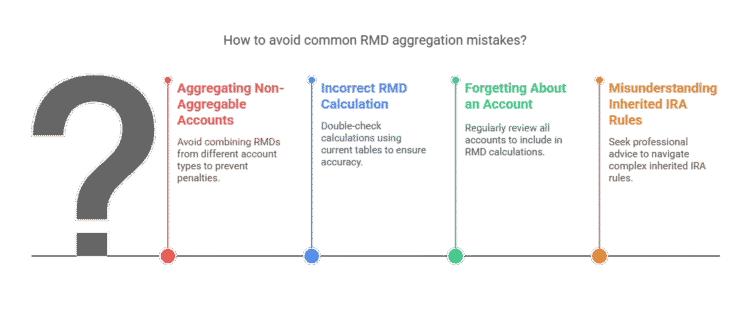

Mistake #1: Aggregating Non-Aggregable Accounts.

The Trap:

Assuming you can lump 401(k) RMDs with IRA RMDs.

The Reality (and a Client Story):

My client Frank (name changed, of course!) almost did this. He had a sizable IRA and a smaller 401(k) from a previous job. He thought he could just take a larger sum from his IRA to cover both. Luckily, we caught it during a review. He would have owed a 25% penalty on the entire missed 401(k) RMD. We quickly arranged the separate 401(k) withdrawal.

Mistake #2: Incorrect RMD Calculation.

The Trap:

Using the wrong prior year-end balance or an outdated life expectancy factor (referencing, for instance, old RMD tables instead of the new required minimum RMD tables).

The Reality: While custodians often provide RMD figures, the ultimate responsibility is yours. I always encouraged clients to double-check, especially if they had IRAs at multiple institutions.

Mistake #3: Forgetting About an Account.

The Trap: An old, smaller IRA gets overlooked, and its RMD isn’t included in the aggregate calculation or withdrawn.

The Reality:

Even a small missed RMD can trigger a penalty on that missed amount. Regular financial “check-ups” can help ensure all accounts are accounted for.

Mistake #4: Misunderstanding Inherited IRA Rules.

The Trap:

Applying your own IRA aggregation rules to IRAs you’ve inherited, especially if from different decedents.

The Reality:

This is a minefield. I’ve seen beneficiaries unknowingly misaggregate, leading to stressful IRS notices. The rules are specific and often counter-intuitive.

Michael’s Pro Tip:

If you’re even slightly unsure, especially with inherited accounts or multiple account types, consult with a qualified financial advisor or CPA. The cost of advice is almost always far less than the cost of an IRS penalty and the stress that comes with it. (For more on finding the right professional, see my guide on Financial Coach vs Financial Advisor vs Financial Planner).

What If I Mess Up? Correcting RMD Errors and Requesting Penalty Waivers

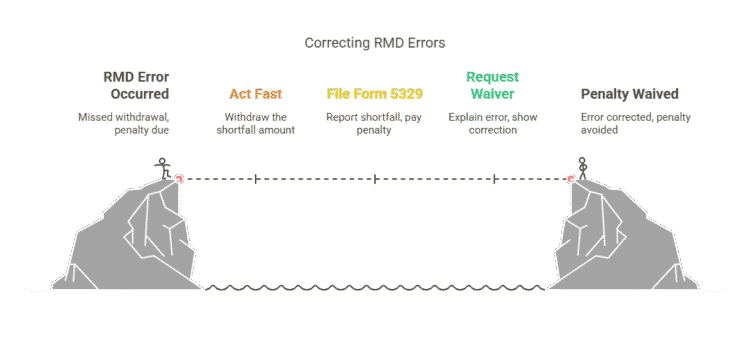

Let’s be real, mistakes happen. If you realize you’ve made an RMD error (like missing one, taking too little, or aggregating incorrectly):

- Act Fast:

The sooner you correct it, the better. Withdraw the shortfall amount immediately. - File Form 5329:

This IRS form, “Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts,” is used to report the RMD shortfall and pay any penalty due. Understanding this form is key when facing potential RMD penalties for missing the deadline. - Request a Penalty Waiver:

The good news is the IRS can waive the 25% penalty if you can show that the shortfall was due to reasonable error and that you are taking reasonable steps to remedy the shortfall. You’ll attach a letter of explanation to Form 5329 detailing why the error occurred and what you’ve done to fix it.- From Experience:

I’ve helped numerous clients draft these letters. Being clear, concise, and demonstrating you understand the rule now and have corrected the error goes a long way. Common reasonable errors include reliance on incorrect custodian information (if you can document it) or a simple oversight that was promptly corrected.

This isn’t a guaranteed get-out-of-jail-free card, but a well-crafted explanation significantly improves your chances.

- From Experience:

The Bottom Line: Simplify Your RMDs, But Strategize Wisely

Combining your RMDs for eligible IRAs can absolutely simplify your financial life in retirement. It reduces administrative burden and can even offer a touch of tax planning flexibility. However, it’s crucial to remember that this flexibility has clear boundaries. You can’t mix and match RMDs from IRAs with those from 401(k)s or other employer plans, and inherited IRAs have their own labyrinth of rules. Effectively managing these RMD aggregation rules is a cornerstone of savvy retirement income planning.

The key is to understand the specific rules for your specific accounts. When done correctly, RMD aggregation is a helpful tool. When misunderstood, it can lead to unwelcome attention from the IRS. So, will you let RMDs manage you, or will you manage them?

My best advice, honed over decades of practice? Create a clear inventory of all your retirement accounts. Understand the RMD requirements for each. And if you’re managing multiple account types or inherited assets, don’t hesitate to map out your strategy with a qualified financial professional. A little planning upfront can make your retirement withdrawals smooth sailing.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.