Imagine inheriting a substantial IRA from a loved one, only to face unexpected tax bills that erode your newfound wealth. In 2026, navigating the maze of Inherited IRA Required Minimum Distribution (RMD) rules is more critical than ever.

With recent changes under the SECURE Act and IRS updates, making a misstep could cost you—literally.

When Emily received news of her inheritance—a $600,000 IRA from her grandfather—she felt both grateful and overwhelmed. Little did she know, a simple oversight in understanding the new RMD rules would cost her $50,000 in unnecessary taxes.

Navigating the maze of inherited IRA RMD rules isn’t just about compliance—it’s about safeguarding your financial future.

Think you can just wait until year 10 to deal with this? Think again.

I’m going to break down the 2026 inherited IRA RMD rules, show you how to minimize taxes, and help you avoid the costly mistakes even experienced investors make.

The 10-Year Rule Explained: How Inherited IRA Withdrawals Work After 2026

Time is money, especially when the IRS clocks are ticking.

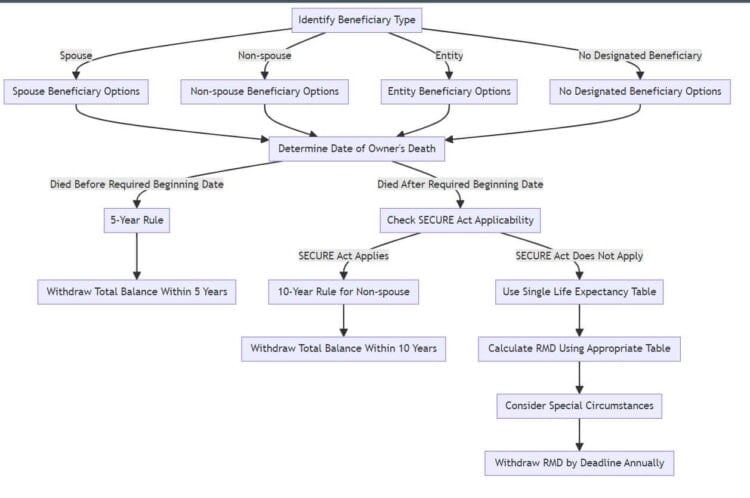

Under the post‑SECURE and SECURE Act 2.0 distribution rules for Inherited IRAs, most non‑spouse designated beneficiaries must fully distribute the account by the end of the 10th year following the original owner’s death, and if the original owner died after their Required Beginning Date, annual RMDs are required in years 1 through 9 using the IRS Single Life Expectancy Table.

- No annual RMDs? Think again: if the original owner died after their Required Beginning Date, current IRS guidance requires you to calculate and take annual RMDs in years 1 through 9 using the Single Life Expectancy Table and still empty the inherited IRA by the end of year 10

- Compound Interest or Compounded Mistakes? Waiting until the last year could bump you into a higher tax bracket, leading to hefty taxes.

| Strategy | Modeled total withdrawals (10 years) | Modeled total taxes paid (10 years) |

|---|---|---|

| Equal withdrawals over 10 years | $200,000 | $600,000 |

| No withdrawals until year 10 (lump sum) | $2,000,000 | $740,000 |

| Customized, tax‑efficient withdrawals | Varies by plan | $500,000 |

Note: In reality, qualified Roth IRA withdrawals are generally income‑tax‑free; this table models relative tax drag if the same strategies were applied to a taxable or pre‑tax retirement account to illustrate how timing affects lifetime taxes.[web:71][web:68]

One of my clients, Mark, inherited a $2 million IRA from his uncle, the original account owner. Believing he could wait until the end of the 10th year to withdraw, he deferred distributions.

In year ten, Mark faced a massive tax bill and was pushed into the highest tax bracket, losing over $740,000 is the total amount that may be subject to distribution requirements under the inherited IRA guidelines. to federal and state taxes.

- By coordinating withdrawals to stay within lower tax brackets and considering life’s income fluctuations, beneficiaries can significantly reduce their tax liabilities.

- Proactive planning is essential, as waiting until the last minute can be costly when dealing with IRA distribution rules.

Tip: Consult with a financial advisor to create a withdrawal strategy that balances tax efficiency and growth.

- RMDs for Spouses: Schwab’s Guide on IRA Withdrawals

- RMDs for Minor Children: Fidelity’s Overview of Inherited IRAs

- RMDs for Non-Spouse Beneficiaries: Journal of Accountancy’s Guide to Beneficiary IRAs

New IRS RMD Rules for Inherited IRAs: Key Changes You Can’t Afford to Miss

Navigating the complex world of inherited IRAs and their distribution rules? The Internal Revenue Service oversees the rules for traditional IRA and Roth IRA distributions.

Major Changes You Can’t Ignore

⚠️ Critical Successor Beneficiary Rule

When you inherit an IRA that was already an inherited IRA, you become a “successor beneficiary.”

The original 10-year clock does not reset.

The final distribution deadline is strictly tied to whatever time remained on the first beneficiary’s original 10-year schedule.

Example: If the first beneficiary passed away in Year 4 of their 10-year window, you only have the remaining 6 years to fully deplete the account.

- Clarification on the 10‑Year Rule: after several years of confusion, the IRS has now confirmed and begun fully enforcing that if the original owner died after their Required Beginning Date, annual inherited IRA RMDs are mandatory in years 1 through 9 in addition to the 10‑year payout requirement

- NEW: Mandatory annual RMDs if the original owner died after their Required Beginning Date

- IMPORTANT: Complete account distribution required within 10 years

- TIP: Plan ahead to avoid last-minute tax complications

- Example: If you inherited a $500,000 IRA in 2026, you’ll need strategic withdrawal planning through 2036.

- Penalty Changes: Miss an inherited IRA RMD and the excise tax is now 25% of the shortfall, and it can be cut to 10% if you correct the mistake quickly and file Form 5329, but even a 10% penalty on a six‑figure inherited account is a painful and avoidable hit to your inheritance.

- Reduced penalty: From 50% to 25% for missed RMDs

- Early correction bonus: Further reduction to 10% if fixed promptly

- Action required: File Form 5329 for corrections

Don’t let ignorance empty your pockets. Understanding these nuances is crucial for preserving your inheritance.

Remember: While this guide provides valuable information, inherited IRA rules are complex. Consider consulting with qualified financial professionals for personalized advice. What happens to your IRA accounts when you inherit an IRA? I suggest you read my article about how many IRAs you are allowed to have .

How to Calculate Inherited IRA RMDs in 2026

Calculating your RMD isn’t just crunching numbers—it’s about safeguarding your financial future.

The Inherited IRA RMD Formula: A Step-by-Step Breakdown

Don’t let RMD calculations intimidate you! This comprehensive guide breaks down everything you need to know about calculating your Inherited IRA. Required Minimum Distributions (RMDs) for 2026.

Step-by-Step Calculation Process:

- Determine the Account Balance:

• Use the IRA’s fair market value as of December 31, 2025.

• Include all year-end adjustments

• Account for any outstanding rollovers - Find Your Life Expectancy Factor:

• Refer to the IRS Single Life Expectancy Table corresponding to your age in 2026.

• Use your age as of December 31, 2026, to determine your withdrawal rules.

• Verify you’re using the current IRS guidelines for IRA or Roth distributions. Inherited IRA RMD Table - Calculate the RMD = Account Balance ÷ Life Expectancy Factor

Example:

- Account Balance: $500,000

- Age: 40

- Life Expectancy Factor: 43.6

- RMD: $500,000 ÷ 43.6 ≈ $11,467

Inherited IRA RMD Calculation

For beneficiaries who must take annual inherited IRA RMDs, the core calculation is:

*Note: Calculations must use the updated Single Life Expectancy Tables that went into effect in 2022.

Essential Steps:

✓ Use the current IRS Single Life Expectancy Table, which was updated starting in 2022 and still governs inherited IRA RMD factors in 2026

✓ Calculate based on December 31 previous year value

✓ Verify age requirements carefully

WATCH OUT! Common Mistakes to Avoid:

- Outdated Tables

• WARNING: Using pre-2022 tables can lead to incorrect calculations

• EXAMPLE: John used an old table and underpaid by $5,000, triggering penalties - Age Miscalculations

• Use age at year-end, not current age

• Consider special rules for deceased owner’s age - Multiple Beneficiary Complications

• Separate account rules

• Joint life expectancy considerations

• Division deadline requirements for inherited IRA distribution requirements - Misclassifying beneficiary status

• Account separation options as a beneficiary

• Individual calculation methods for taking RMDs.

• Deadline considerations - Missing mid-year inheritance adjustments

• Pro-rata calculations required

• First-year special rules

• Documentation requirements - Trust as Beneficiary:

• Look-through trust rules

• Qualifying trust requirements

• Special calculation methods

IRS Audit Prevention Checklist

Essential Documentation:

✓ Account statements

✓ Calculation worksheets for understanding Roth IRAs.

✓ Beneficiary designations

✓ Distribution receipts

Red Flag Prevention:

• Double-check all calculations

• Maintain accurate records

• Submit distributions on time

• Document special circumstances

For Reporting Purposes:

- Form 5498: Report IRA contributions (file by May 31st)

- Form 1099-R: Report distributions taken (file by January 31st)

- Form 5305: Establish an Iherited IRA

Michael Ryan Money Pro Tips for Success

- Set Up Automatic Calculations for your retirement account.

• Use reliable financial software

• Schedule annual reviews

• Keep calculation records - Create Safety Nets

• Set up automatic distributions

• Use calendar reminders

• Build in review time - Professional Support

• Consider tax advisor consultation

• Regular financial planning review for inherited retirement accounts.

• Stay updated on rule changes

Additional Resources

- For more insights on retirement planning, check out “Retirement Planning Essentials“

- For comprehensive IRS guidelines on RMDs, visit IRS RMD Resource.

- Essential References:

IRS Publication 590-B: Available directly on IRS.gov or by searching “Publication 590-B” on the IRS website - Current Life Expectancy Tables for IRA Beneficiaries: Found in IRS Publication 590-B and on the IRS website under Required Minimum Distribution tables

- RMD Calculation Worksheets: Available in IRS Publication 590-B and through major financial institutions

- Professional Tax Directory: Can be accessed through the IRS website for the latest IRA distribution rules. IRS website’s tax professional finder tool

- IMPORTANT: The Internal Revenue Service scrutinizes RMD calculations carefully. Even small errors can trigger audits or penalties. When in doubt, consult with a qualified tax professional.

- Note: Always verify current IRS rules and consult with financial professionals for personalized advice regarding beneficiary RMD rules.

Inherited IRA RMD Calculator: How to Estimate Your 2026 Withdrawals

Why do the math yourself when technology can help?

Here’s an interactive RMD calculator specifically designed for 2026 Inherited IRA beneficiaries. This tool estimates your distribution based on the latest IRS proposed regulations, life expectancy tables, and tax implications. But obviously confirm these numbers with your tax professional!

RMD Estimator for the 2026 Tax Year

Estimate your 2026 owner RMD across one or more Traditional, SEP, or SIMPLE IRAs using December 31, 2025 balances.

2026 RMD Estimation Record

| IRA | Type | 2025 balance | 2026 RMD calculation |

|---|

Calculation basis

Deadline and aggregation notes

2027 age-factor comparison

Related planning tools

Consider These Factors:

• Calculation complexity

• Required features

• Update frequency

• Support availability

• User reviews

- Fidelity’s RMD Calculator: User-friendly interface with up-to-date tables.

- Vanguard’s Retirement Distribution Tool: Tailored advice based on your inputs.

- Schwab’s Inherited IRA Planner: Includes tax implications and strategy suggestions.

Pro Tip: Always double-check calculations, especially if you’re managing significant sums.

Inherited IRA Beneficiary Rules: Who’s Exempt from the 10-Year Rule?

Not all heirs are created equal in the eyes of the IRS.

Spouses, Minors, and Disabled Beneficiaries: Special RMD Exceptions

Certain beneficiaries qualify as Eligible Designated Beneficiaries (EDBs):

- Spouses:

- Option 1: Do a spousal rollover and treat the IRA as your own, which moves you onto the standard Uniform Lifetime Table for RMDs at your age instead of the Single Life Table and generally gives you the longest payout period

- Option 2: Treat it as an Inherited IRA. Beneficial if you’re under 59½ to avoid early withdrawal penalties.

- Minor Children of the account owner can generally stretch inherited IRA RMDs over their life expectancy until they reach age 21. And once they turn 21 a separate 10‑year payout period begins for the remaining balance

- After 21, the 10-Year Rule kicks in.

- Disabled or Chronically Ill Individuals:

- Allowed to stretch distributions over their lifetime.

Navigating these exceptions can significantly impact your inheritance’s longevity.

Grandchildren and Non-Spouse Beneficiaries: Hidden Tax Traps

- 10-Year Dealine Applies: Must withdraw the entire balance by the end of the tenth year.

- No Early Withdrawal Penalty: Regardless of age, but taxes still apply.

- Kiddie Tax: For minors, unearned income over $2,500 may be taxed at the parents’ rate.

Avoiding Pitfall: Consider a Roth conversion if the original owner is still alive to mitigate future tax burdens on heirs.

Required Minimum Distribution Mistakes That Could Cost You 25%

In the world of taxes, what you don’t know can hurt you.

The #1 Myth About Inherited IRA Withdrawals (And How to Avoid It)

Myth: “I can wait until the tenth year to withdraw everything.”

Reality: If the original owner died after their Required Beginning Date, you must take annual inherited IRA RMDs in years 1 through 9 based on the Single Life Expectancy Table and still clear the account by the end of year 10, so dumping everything into the final year usually means stacking a very large taxable withdrawal on top of nine years of prior distributions.

Avoiding the Trap:

- Stay Informed: Understand the distribution requirements for inherited IRAs in 2023. Know the original owner’s RBD status to determine your beneficiary RMD rules.

- Annual Check-ins: Regularly review your withdrawal plan with a financial advisor.

Real-Life Penalty Stories: How Skipping RMDs Wiped Out $12k in Savings

Meet Lisa, who inherited a $400,000 IRA in 2022:

- Mistake: Believing she didn’t need to take annual RMDs.

- Consequence: In 2025, the IRS slapped her with a 25% penalty on missed RMDs totaling $48,000.

- Total Penalty: $12,000 lost to avoidable errors.

Lesson Learned: Ignorance isn’t bliss—it’s expensive.

Next Steps For Managing Your Inherited IRA RMDs:

Mastering the inherited IRA RMD tables is crucial for preserving your inheritance and avoiding costly penalties. The recent RMD updates bring both challenges and opportunities for strategic distribution planning.

Take Action Now:

- Use our RMD Calculator Tool

- Schedule a tax planning review

- Set up automatic distribution reminders

Remember: “Smart inheritance management isn’t about avoiding distributions—it’s about distributing wisely.”

Want to ensure you’re maximizing your inherited IRA? Try our exclusive RMD Planning Tool, designed specifically for 2026’s new requirements.

The difference between successful inheritance management and costly mistakes often comes down to understanding these crucial tables. Don’t leave your financial future to chance.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.