As a financial planner for nearly 30 years, I saw the same look of surprise on my clients’ faces when they reached their RMD age 73 (or later for some younger retirees under current law). After a lifetime of diligent saving, the IRS required them to begin withdrawing money from certain tax-deferred retirement accounts. Whether they needed it or not. This is the reality of the Required Minimum Distribution (RMD).

So, what do you do with required minimum distributions that you don’t need?

For many retirees whose daily expenses are covered by pensions or Social Security, this forced withdrawal feels like a solution in search of a problem. RMD’s become a mandatory income bump that can trigger a cascade of unwanted tax consequences.

The good news? An unneeded RMD isn’t a problem; it’s an opportunity. Doing nothing isn’t neutral; it’s choosing to pay more tax than you need to, which is money that won’t be going to your charity or your family.

This is the playbook I used with hundreds of clients to transform this obligation into a strategic financial win. We’ll go beyond the basics and give you a clear framework for making the smartest possible move with your money.

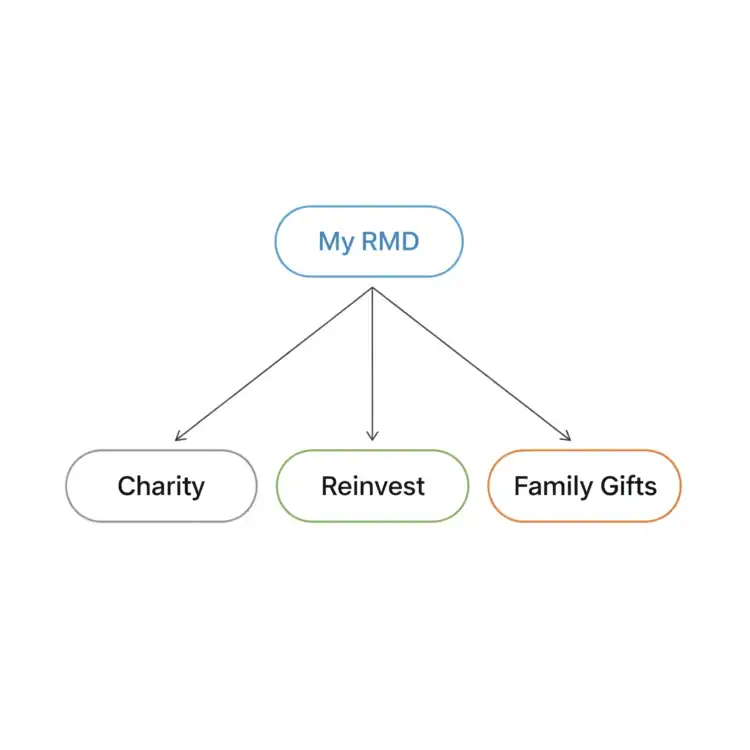

The 3 Smartest Things to Do With Unneeded RMDs: Give, Grow, or Gift

When you have an RMD you don’t need for living expenses, your decision-making process should be guided by your primary goal.

Over my career, I found that every successful strategy fell into one of these three categories.

Strategy 1: Give It (The Qualified Charitable Distribution)

For retirees with a philanthropic heart, the Qualified Charitable Distribution (QCD) is a grand slam. It is, without a doubt, the most tax-efficient way to handle unneeded RMDs.

A QCD allows you to transfer up to $111,000 (for 2026) per year directly from your Traditional IRA to a qualified 501(c)(3) charity. This direct transfer satisfies your RMD requirement, but the brilliant part is that the money is never included in your Adjusted Gross Income (AGI).

Strategy 2: Grow It (Reinvesting Your RMD)

If your primary goal is to continue growing your wealth, you can reinvest your RMD. But remember the cardinal rule: you cannot put it back into an IRA or another tax-deferred account.

Instead, you take the distribution, pay the necessary income taxes on it, and then reinvest the net amount into a taxable brokerage account.

Strategy 3: Gift It (Legacy & Family Planning)

An unneeded RMD provides a wonderful opportunity to support your family’s financial goals. You can use the after-tax proceeds from your RMD to:

- Fund a 529 College Savings Plan: You can contribute up to the annual gift tax exclusion amount for the year per grandchild without using any of your lifetime gift and estate tax exemption.

- Fund a Roth IRA for a Working Grandchild: If your grandchild has enough earned income, you can gift them money that they can use to fund their own Roth IRA, subject to the annual contribution limits and eligibility rules.

A Planner’s Comparison: Which Strategy is Right for You?

Choosing the right strategy depends entirely on your personal financial goals. This table breaks down the decision-making process.

What About a QLAC? The Advanced RMD Strategy

For those looking for more advanced techniques, a Qualified Longevity Annuity Contract (QLAC) is an option. A QLAC allows you to use up to the applicable dollar limit from eligible retirement accounts to purchase a deferred annuity, and qualified amounts are excluded from RMD calculations until payments begin.

Now, try searching for: RMD calculator, inherited IRA rules, or Roth conversion strategies.

Conclusion: Turn an Obligation into an Opportunity

An unneeded RMD is a clear sign of a successful life of saving. By treating it not as a tax burden but as a strategic asset, you can further enhance your financial security, support the people and causes you care about, and build a lasting legacy.

The key is to move from being a passive rule-follower to an active manager of your retirement income. By using the strategies in this playbook, you can turn this annual obligation into a powerful financial opportunity.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.