Many American households face a serious risk of running short of money in retirement.

According to a recent Allianz study in April 2026, about two-thirds of Americans (67%) say they worry more about running out of money than death itself. This isn’t just anxiety, It often reflects gaps in retirement planning.

The right retirement withdrawal strategies can transform retirement from anxious to comfortable. A retiree who saved diligently for decades can still face financial stress if they withdraw funds poorly.

This situation is all too common, underscoring the importance of understanding how to withdraw funds wisely from your retirement savings.

Here’s what you need to know:

- Master effective withdrawal strategies to ensure your savings last.

- Navigate tax-efficient withdrawals to maximize your retirement income.

- Avoid common pitfalls that can derail your financial plans.

Key Article Takeaways: FAQs on Retirement Withdrawal Strategies

- What are the most effective retirement withdrawal strategies?

Explore methods such as the 4% Rule, fixed-dollar strategy, and total return strategy to find the best fit for your financial goals. - How can I ensure my retirement account withdrawals are tax-efficient?

Prioritize taxable accounts first, consider Roth conversions, and implement proportional withdrawals to minimize your tax burden. - What should I do if market conditions change?

Stay flexible by reassessing your withdrawal strategy annually, adjusting based on portfolio performance and personal needs. - How do I create a sustainable withdrawal plan in retirement?

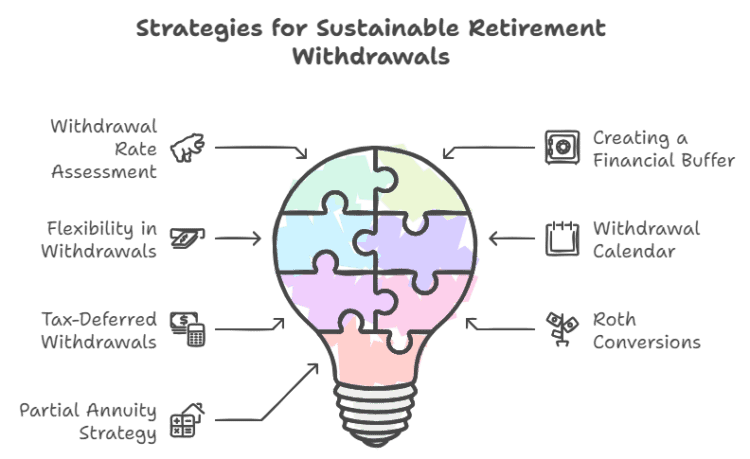

Assess your current withdrawal rate, establish a buffer for unexpected expenses, and diversify your income sources to enhance sustainability. - Can I combine different income withdrawal strategies?

Yes! Blending approaches like the bucket strategy and dynamic spending can create a robust and adaptable plan tailored to your circumstances.

RMD Calculator for 2026

Estimate 2026 owner required minimum distributions across multiple IRAs and workplace retirement accounts using December 31, 2025 balances.

Estimated 2026 RMD Summary

| Account | Type | 2025 balance | Estimated 2026 RMD | Status |

|---|

Deadline

Aggregation and withdrawal rules

Important next checks

- Confirm each December 31 balance and any account-specific adjustment with the custodian or plan administrator.

- Confirm whether a current-employer plan permits the still-working delay and whether the owner is treated as a 5% owner.

- Calculate an account separately if a spouse more than 10 years younger is its sole beneficiary.

- Coordinate distributions with income taxes, Medicare IRMAA, charitable giving, Roth conversions, and tax withholding.

Have you ever wondered how to adapt your retirement strategy in a volatile market? Or how to ensure your savings align with your lifestyle goals? By the end of this article, you’ll be equipped with the knowledge to secure a financially stable retirement. Let’s look at essential strategies that will help you enjoy your golden years without financial worry.

Quick Links For Retirement Plan Distributions

The Art of Sustainable Retirement Plan Withdrawals And Distributions

Retirement withdrawal strategies are the unsung heroes of financial planning. They determine not only how long your hard-earned savings will last but also how effectively you’ll weather market fluctuations and inflationary pressures.

As you ponder how long your money will last in retirement, consider using our retirement calculator to gain insights into your financial landscape.

The 4% Rule: A Time-Tested Approach

The 4% withdrawal rule is often regarded as the cornerstone of retirement withdrawal strategies. This is a widely used approach that involves withdrawing 4% of your initial retirement portfolio balance each year.

Here’s how it works: To calculate, multiply your initial portfolio balance by 0.04 or 4%.

- Withdraw 4% of your portfolio in your first year of retirement.

- Adjust this amount for inflation in subsequent years.

Sounds simple. But 2026’s market reality tells a different story. Morningstar’s 2026 research suggests a 3.9% starting withdrawal rate for a 30-year retirement in its base case, up from 3.7% in the prior year’s research.

For example, if you have a $1 million portfolio, your first-year withdrawal would be $40,000. If inflation is 2% the next year, you’d withdraw $40,800. However, what happens if your portfolio decreases in value?

This method isn’t perfect. It struggles when market conditions diverge from the rule’s assumptions.

Retirement Withdrawal & Allocation Modeler

Explore the trade-off between initial portfolio withdrawals, stock exposure, retirement length, and your ability to reduce spending after difficult markets.

Your Modeled Trade-Off

Michael’s Perspective

What matters most in this combination

Stress-test question

Fixed-Dollar Strategy: Predictability at a Cost

Some retirees prefer the predictability of withdrawing a fixed amount each year, resembling a steady paycheck in retirement. However, this method overlooks an insidious threat: inflation.

Total Return Strategy: Embracing the Long Game

For those with higher risk tolerance, the Total Return Strategy for retirement income focuses on long-term growth investments. You withdraw only what you need in the short term, allowing the remainder of your portfolio to potentially grow.

This approach demands a delicate balance and isn’t about adhering to a fixed percentage or dollar amount but rather managing your portfolio to generate the returns you require.

Navigating the Choppy Waters of Retirement: Ensuring Your Funds Last

The fear of outliving your money is both real and justified. Here are some steps you can take today to mitigate this concern:

- Assess your current withdrawal rate: Is it sustainable given your portfolio size and market conditions?

- Create a buffer: Consider setting aside 2-3 years of expenses in cash or low-risk investments.

- Stay flexible: Be prepared to adjust your withdrawals based on market performance.

Additional Methods for Sustainable Withdrawal Rates:

- Withdrawal Calendar: Use a withdrawal calendar to plan your withdrawals, spreading them out over the year to avoid over-withdrawing in one month.

Example: If you have a 20,000 annual withdrawal, break it down into $1,667 per month or $416 per week for a more consistent income. - Tax-Deferred Withdrawals: Be strategic with withdrawals from tax-deferred accounts such as traditional IRAs and 401(k)s, since those withdrawals generally increase taxable income.

- Roth Conversions: Convert traditional IRAs or 401(k)s to Roth IRAs, which can provide tax-free growth and withdrawals.

- Partial Annuity Strategy: Combine a fixed annuity with a variable annuity to create a hybrid strategy, ensuring a guaranteed income stream and potential for growth.

Managing Market Volatility and Inflation

Market fluctuations are inevitable, and inflation is a silent wealth-eroder. Here’s how to stay ahead:

- Diversify your portfolio: Avoid putting all your eggs in one basket.

- Consider inflation-protected securities: Treasury Inflation-Protected Securities (TIPS) can help safeguard against inflation.

- Review and rebalance regularly: Aim to do this at least annually.

Your Action Plan: Securing Your Retirement Today

Are you ready to take control of your retirement withdrawals? Here’s what you can do right now:

- Calculate your current withdrawal rate: Divide your annual withdrawals by your total portfolio value.

- Review your asset allocation: Ensure it aligns with your risk tolerance and goals.

- Set up a meeting with a financial advisor: Discuss implementing a dynamic withdrawal strategy.

The key to a successful retirement isn’t just about how much you save—it’s about how wisely you withdraw. By understanding and implementing effective retirement withdrawal strategies, you’re taking a crucial step towards ensuring your golden years are truly golden.

Actionable Advice for Retirement Withdrawal Strategies: Tailoring Your Approach

Now that we’ve explored the fundamentals of retirement withdrawal strategies, let’s dive into actionable tips you can take to put this knowledge into practice. Remember, the key to a successful retirement isn’t just about how much you’ve saved—it’s about how wisely you manage those savings.

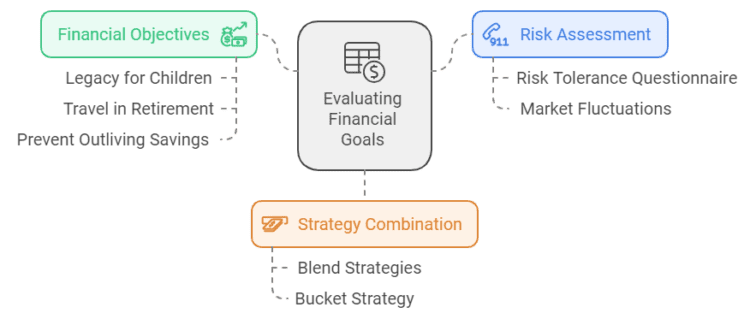

Evaluate Your Financial Goals

Before implementing any withdrawal strategy, know what you’re trying to achieve. Start with a thorough risk assessment and evaluate your financial objectives.

Conduct a Risk Assessment

Understanding your risk tolerance matters. Consider both how much risk you can handle emotionally and how much your financial situation can withstand.

Action Step:

Take an online risk tolerance questionnaire to establish a baseline understanding of your risk profile. These tools can offer valuable insights into how comfortable you are with market fluctuations and potential losses.

Align with Financial Objectives

Your withdrawal strategy should harmonize with your overall financial goals. Are you looking to leave a legacy for your children? Do you want to travel extensively in your early retirement years? Or is your primary concern ensuring that you don’t outlive your savings?

Action Step:

Write down your top three financial objectives for retirement. Be specific. Instead of vague goals like “have enough money” try framing them as “maintain my current lifestyle while accounting for inflation.”

Strategy Combination: The Power of Flexibility

One size doesn’t fit all when it comes to retirement planning. That’s why combining different strategies can offer you the best of all worlds.

Blend Different Strategies

By mixing approaches, you can create a withdrawal plan that’s both stable and adaptable. For instance, you might use the 4% rule as a baseline but adjust it based on market performance, in line with the total return strategy.

Personalized Planning

Your retirement plan should be as unique as you are. Factors such as your health, family longevity, and even where you plan to live can all impact your ideal withdrawal strategy.

Action Step: Create a “retirement budget” that encompasses both essential expenses (housing, food, healthcare) and discretionary spending (travel, hobbies). This will help you determine how much flexibility you need in your withdrawal strategy.

Embracing Flexible Strategies

The ability to adapt your withdrawal strategy is crucial for long-term success. Market conditions change, life throws curveballs, and your needs may evolve over time.

Action Step: Set up annual “strategy check-ins” with yourself or your financial advisor. During these sessions, review your withdrawal rate, investment performance, and overall financial situation. Be ready to make adjustments as needed.

Keep up with the latest retirement withdrawal strategies and economic trends that might impact your plan.

Remember, the most effective retirement withdrawal strategy is one that you can stick to and adjust as needed. By taking these actionable steps and remaining flexible, you’re setting yourself up for a more secure and enjoyable retirement.

Addressing Secondary Concerns: Tax-Efficient Withdrawals in Retirement

While we’ve covered the basics of withdrawal strategies, it’s essential to consider tax efficiency, which can significantly impact your retirement income. By implementing tax-smart withdrawal strategies, you can potentially keep more of your hard-earned money and extend the life of your retirement savings.

Tax efficiency in retirement isn’t just about paying less in taxes; it’s about optimizing your withdrawals to maintain your lifestyle while minimizing your tax burden. Let’s explore two key strategies that can help you achieve this balance.

Strategy 1: The Traditional Withdrawal Order

Conventional wisdom suggests a specific order for withdrawals:

- Taxable Accounts: Start here to allow tax-advantaged accounts more time to grow.

- Tax-Deferred Accounts: Next, tap into your traditional IRAs and 401(k)s.

- Roth Accounts: Save these for last to maximize tax-free growth.

This approach can be effective, but it’s not without potential pitfalls.

Case Study: Joe’s Tax Bump

Joe diligently followed this traditional withdrawal order in retirement. Initially, things went smoothly. However, midway through his retirement, Joe encountered a “tax bump.” Over 12 years, he ended up paying approximately $66,000 in taxes. That’s when Joe decided to explore alternative strategies.

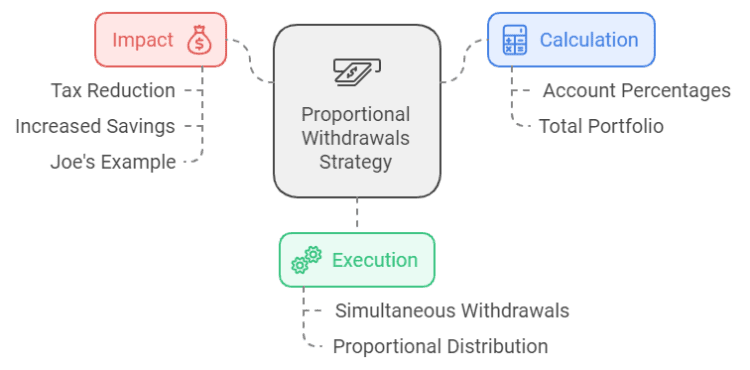

Strategy 2: Proportional Withdrawals

Enter the proportional withdrawal strategy. This approach involves withdrawing money from all account types simultaneously, based on their proportion of your total savings. Here’s how it works:

- Calculate the percentage each account type represents in your total portfolio.

- Withdraw from each account based on these percentages.

The Joe Transformation

In some cases, proportional withdrawals can reduce lifetime taxes by smoothing income across taxable, tax-deferred, and tax-free accounts, though the results depend heavily on the retiree’s account mix, tax bracket, and withdrawal timing.

Why Proportional Withdrawals Can Work

The power of proportional withdrawals lies in tax diversification. By spreading your withdrawals across different account types, you can effectively manage your tax liability. This strategy can help you:

- Avoid RMD surprises: Required Minimum Distributions from tax-deferred accounts can push you into a higher tax bracket. Proportional withdrawals can help mitigate this risk. Use our RMD Calculator here.

- Maximize tax brackets: By carefully managing your taxable income each year, you can potentially stay in lower tax brackets throughout retirement.

- Maintain flexibility: This strategy allows you to adjust based on changing tax laws or personal circumstances.

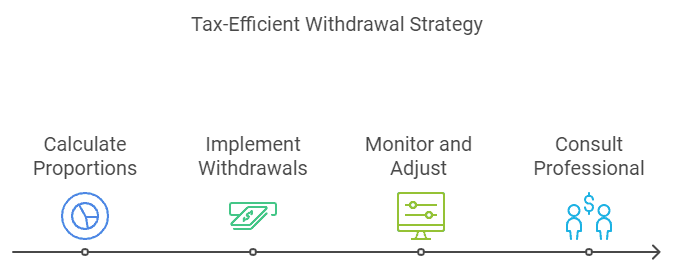

Your Action Plan: Implementing Tax-Efficient Withdrawals

Ready to optimize your retirement withdrawals for tax efficiency? Here’s your step-by-step guide:

- Calculate Your Proportions: Determine what percentage each account type represents in your total portfolio.

- Implement Proportional Withdrawals: Start withdrawing from each account based on these percentages.

- Monitor and Adjust: Regularly monitor your strategy and adjust based on changes in tax laws or your personal situation.

- Consult a Professional: Work with a financial advisor to optimize your withdrawal strategy based on your unique financial situation.

Remember, while the proportional withdrawal strategy worked wonders for Joe, everyone’s situation is unique. The key is to stay informed, be proactive, and don’t hesitate to seek professional advice.

Long-Term Strategies and Advanced Solutions: Maximizing Your Retirement Success

Here’s what most retirement advisors won’t tell you: Fixed withdrawal rates fail during the most critical period—your first decade of retirement. Sequence-of-returns risk means a market crash in year 2 destroys your portfolio faster than one in year 20. Dynamic strategies solve this.

Dynamic Spending: Adapting to Market Realities

One of the most powerful advanced strategies is dynamic spending. This approach allows you to adjust your withdrawals based on market performance, helping you strike a balance between your current lifestyle and future financial security.

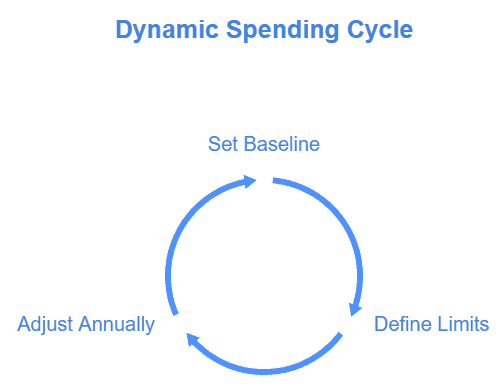

How Dynamic Spending Works

- Set a Baseline: Establish your initial withdrawal rate based on your retirement savings and expected expenses.

- Define Limits: Create a “floor” (minimum spending) and a “ceiling” (maximum spending) for your annual withdrawals.

- Adjust Annually: Based on your portfolio’s performance, adjust your withdrawals within these limits.

Real-World Example:

Suppose your initial withdrawal is $50,000 per year. You might set a floor of $45,000 and a ceiling of $55,000. In years of strong market performance, you could increase your withdrawal up to $55,000. In downturns, you’d reduce spending, but never below $45,000.

Benefits of Dynamic Spending

- Flexibility: This strategy allows you to adapt to market changes, enabling increased spending in favorable years and reduced spending during downturns.

- Sustainability: Aligning your spending with investment returns helps maintain portfolio longevity.

- Peace of Mind: Enjoy current spending while safeguarding your future needs.

For a deeper dive into dynamic spending strategies, check out Vanguard’s article on retirement withdrawal strategies.

The Bucket Strategy: Balancing Risk and Growth

Another advanced approach is the bucket strategy, which divides your assets into different time-horizon categories or “buckets.” This method helps manage risk by aligning asset allocation with your spending timeline.

Implementing the Bucket Strategy

- Short-Term Bucket (0-2 years): Allocate cash and cash equivalents for immediate needs.

- Intermediate-Term Bucket (3-10 years): Invest in a mix of bonds and moderate-risk assets.

- Long-Term Bucket (10+ years): Focus on growth-oriented investments, primarily stocks.

How It Works

You draw from the short-term bucket for current expenses while allowing the intermediate and long-term buckets to grow. Periodically, you rebalance by shifting money from longer-term buckets to replenish the short-term bucket.

Key Benefit:

This strategy provides peace of mind by ensuring you have liquid assets for immediate needs while still pursuing growth opportunities for the future.

Future-Proofing Your Retirement Plan

Retirement planning isn’t a set-it-and-forget-it endeavor. To ensure long-term success, regular reassessment and adjustments to your strategy are essential.

Regular Reassessment

- Annual Assessment: At least once a year, conduct a comprehensive look at your retirement plan.

- Market Analysis: Consider how current market conditions might impact your strategy.

- Life Changes: Adjust your plan based on personal circumstances such as health, family dynamics, or changing goals.

Leveraging Financial Tools and Professional Advice

- Retirement Calculators: Utilize online tools to project future needs and assess the sustainability of your current strategy.

- Professional Consultation: Regular meetings with a financial advisor can provide tailored advice and necessary adjustments to your plan.

For access to helpful retirement planning tools, visit our helpful retirement calculators and retirement planning resources.

Common Pitfalls and FAQs: Navigating the Complexities of Retirement Planning

Even with the best-laid plans, retirement planning can be fraught with potential mistakes and unexpected challenges. In this section, we’ll explore some common pitfalls to avoid and address frequently asked questions to help you navigate your retirement journey more smoothly.

Mistakes to Avoid: Don’t Let These Derail Your Retirement

- Over-Reliance on a Single Withdrawal Strategy

- Why It’s a Problem: Financial markets are unpredictable, and personal circumstances can change. A strategy that works well in one economic climate might falter in another.

- Solution: Embrace flexible planning. Combine different withdrawal methods to enhance adaptability. For example, consider using a combination of the 4% rule, dynamic spending, and the bucket strategy to create a more robust plan.

- Action Step: Check your current withdrawal strategy. If you’re relying solely on one method, consult with a financial advisor to diversify your approach.

- Ignoring Tax Implications

- Why It’s a Problem: Different types of accounts (traditional IRAs, Roth IRAs, taxable accounts) have varying tax treatments. Withdrawing without considering these differences can lead to unnecessarily high tax bills.

- Solution: Implement tax-efficient withdrawal strategies. This may involve:

- Prioritizing withdrawals from taxable accounts first.

- Balancing withdrawals from tax-deferred and tax-free accounts.

- Considering Roth conversions in low-income years.

- Action Step: Revisit your withdrawal strategy with a tax professional to ensure you’re minimizing your tax burden.

FAQs: Your Burning Retirement Questions Answered

Q: How do Required Minimum Distributions (RMDs) affect my retirement strategy?

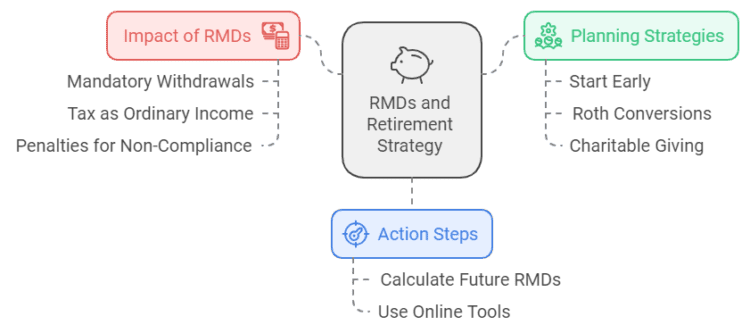

A: Required Minimum Distributions can significantly impact your retirement planning, especially if not properly accounted for. Key points to understand:

- RMDs are mandatory withdrawals from most tax-deferred retirement accounts, including traditional IRAs and 401(k)s. For many current retirees, RMDs begin at age 73, while people born in 1960 or later will begin at age 75 under SECURE 2.0.

- These withdrawals are taxed as ordinary income, which can push you into a higher tax bracket if not managed carefully.

- Failure to take the full RMD generally results in a 25% excise tax on the shortfall, which can drop to 10% if corrected in a timely manner.

How to Plan for RMDs:

- Start Early: Even before RMDs kick in, consider strategies to manage the size of your tax-deferred accounts.

- Roth Conversions: Converting some traditional IRA funds to a Roth IRA before RMDs begin can reduce your future RMD amounts.

- Charitable Giving: If you’re charitably inclined, consider qualified charitable distributions (QCDs) to satisfy your RMD without increasing your taxable income.

Action Step: Calculate your future RMDs using an online RMD calculator to help you anticipate and plan for the tax impact. Calculate your future RMDs using our online RMD calculator.

Q: How can I ensure my retirement strategy remains flexible?

A: Flexibility in retirement planning is crucial for adapting to changing personal circumstances and market conditions. Strategies for flexible planning include:

- Regular Inspections: Assess your retirement plan annually, or more frequently if significant life changes occur.

- Multiple Income Streams: Diversify your income sources (e.g., Social Security, pensions, investments, part-time work).

- Emergency Fund: Maintain a cash reserve to cover unexpected expenses without disrupting your long-term strategy.

- Adaptable Spending: Implement a dynamic spending approach that adjusts based on market performance.

By being aware of these common pitfalls and having answers to frequently asked questions, you’re better equipped to navigate the complexities of retirement planning. Remember, the key to a successful retirement is not just in the initial planning, but in the ongoing management and adaptation of your strategy.

Conclusion: Empowering Your Retirement Journey

In summary, effective retirement withdrawal strategies are crucial for ensuring your financial security in your golden years. By understanding the nuances of withdrawal methods, tax implications, and the importance of flexibility, you can create a plan that aligns with your lifestyle and goals.

With this knowledge, you can confidently navigate the complexities of retirement planning. Take immediate action by calculating your current withdrawal rate, reviewing your asset allocation, and consulting with a financial advisor to optimize your strategy.

- Evaluate your current withdrawal strategy.

- Implement tax-efficient withdrawal methods.

- Schedule regular check-ins with your financial advisor.

The difference between a comfortable retirement and running out of money often comes down to one thing: your withdrawal strategy. Not how much you saved. Not your investment returns. How you withdraw. Start with our retirement savings calculator, then adjust your approach annually. Your future self will thank you.

How will you ensure that your hard-earned savings serve you well throughout your retirement? The choices you make today will shape your financial future tomorrow.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.