Does your spouse stay home to raise the kids or manage the household? Did they take a career break for school, or do they work part-time with a low income? If so, you’re likely facing one of the most common retirement planning anxieties I saw in my 30-year career:

How does the non-working or lower-earning spouse save for their own future?

Many couples believe that if you don’t earn an income, you can’t contribute to an IRA. For years, this was true, creating a massive retirement savings gap, especially for women. But that changed, and the solution is the Spousal IRA. What I call the ultimate Financial Equalizer for married couples.

This is not a special type of account. It’s a set of IRS rules that allows a working spouse to fund an IRA for their partner. This guide is the playbook I’ve used with hundreds of clients. We’ll dismantle the confusion and give you a clear, actionable plan as part of your overall retirement planning.

Key Takeaways Ahead

What a Spousal IRA Is (and What It Isn’t)

Let’s clear this up immediately: you cannot open a “joint IRA.” A Spousal IRA isn’t a new type of account you select from a dropdown menu. It is a standard Traditional IRA or Roth IRA that belongs only to the non-working or lower-earning spouse.

The “Spousal” part simply refers to the IRS rule that allows the higher-earning spouse’s income to be used to fund the other spouse’s account. This concept was championed by former Senator Kay Bailey Hutchison to promote financial equality in retirement, as noted in congressional records.

The 5-Step Checklist to Qualify for a Spousal IRA

During my years as a financial planner, I saw countless couples miss out because they assumed they didn’t qualify. Don’t make that mistake. The rules are like a combination lock. All tumblers need to align, but it’s simpler than you think.

Here is the definitive checklist based on the rules outlined in IRS Publication 590-A. In my practice, I’ve seen more couples mistakenly disqualify themselves over rule #3 (Earned Income) and #4 (Contribution Limits) than any other.

Pay close attention to these because you must be able to say “yes” to all five.

- You are legally married.

The rules are based on marital status at the end of the tax year (December 31st). - You file a joint federal income tax return.

Filing as “Married Filing Separately” disqualifies you. - The contributing spouse has earned income.

This includes wages, salaries, commissions, and self-employment income. Passive income like rent or investments doesn’t count. - Your combined earned income is greater than the total IRA contributions.

For 2025, if you both want to contribute the maximum of $7,000, your household earned income must be at least $14,000. - The receiving spouse is under age 73 for a Traditional IRA.

There are no age limits for contributing to a Roth IRA.

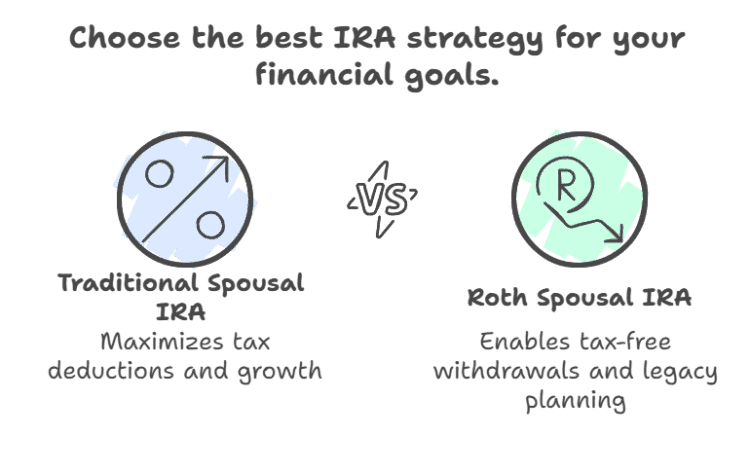

Traditional vs. Roth Spousal IRA: A Planner’s Guide to Choosing

Once you’ve confirmed you’re eligible (IRS Eligibility Rules for IRA), you face the most important strategic decision: Traditional or Roth? The right choice could mean a difference of tens of thousands of dollars in taxes over the course of your retirement.

The decision boils down to one simple question I’d ask every client:

When do you want to pay your taxes?

Pay them now with a Roth IRA and withdraw tax-free later or get a tax break now with a Traditional IRA and pay taxes on withdrawals later.

For a full breakdown of the differences, see our detailed guide on the Roth vs. Traditional IRA.

Don’t overlook ACA subsidies when planning a Roth conversion. A taxable Roth conversion generally increases your household MAGI. If you are under 65 and receive Marketplace premium tax credits, the additional income may reduce your subsidy or increase the amount of advance credits you must repay. That loss acts like an additional tax on the conversion. Compare your expected premium tax credit before and after the conversion, then include the difference in the conversion’s total current-year cost.

The calculator below lets you include that additional ACA cost in the Roth-versus-Traditional comparison. The calculator will then model the long-term impact, showing you the estimated upfront tax cost versus the potential tax-free growth, helping you make a data-driven decision.

Roth Decision Calculator

Compare a Roth conversion with leaving money pre-tax, including the potential effect of Marketplace premium-tax-credit changes, or compare recurring Roth and Traditional IRA contributions.

Roth Decision Comparison

ACA Marketplace comparison

| ACA household MAGI before conversion | |

|---|---|

| ACA household MAGI after conversion | |

| Advance credits received | |

| Estimated reconciliation without conversion | |

| Estimated reconciliation with conversion | |

| Additional ACA cost caused by conversion |

What is driving this result

Important planning checks

Roth Decisions Are Tax-Timing Decisions

Get independent financial education about Roth conversions, retirement tax brackets, ACA subsidies, RMDs, Medicare IRMAA, and coordinating withdrawals over time.

Real-World Scenarios: How My Clients Won with Spousal IRAs

Theory is one thing; results are another. Here is how these strategies played out for real people I worked with.

The Situation: “The Millers” – A single-income family.

The husband was a high-earning executive, and the wife was a stay-at-home parent. They were in a high tax bracket.

The Strategy:

For 20 years, they maxed out a Traditional Spousal IRA for the wife. This gave them a significant tax deduction each year during their peak earning years, which they used to fund a taxable brokerage account.

The Result:

The immediate tax savings compounded over two decades, adding an extra six figures to their overall net worth. Which they then used to fully fund a 529 plan for their two children.

The Situation: “The Jacksons” – A young couple.

The wife was a teacher, and the husband was a freelance graphic designer with a fluctuating, lower income. They were in a low tax bracket.

The Strategy:

They knew their income would grow. They maxed out a Roth Spousal IRA for the husband, paying the taxes now while their rates were low.

The Result:

They built a completely tax-free bucket of money that will be invaluable in retirement, protecting them from future tax rate increases and the impact of future Required Minimum Distributions.

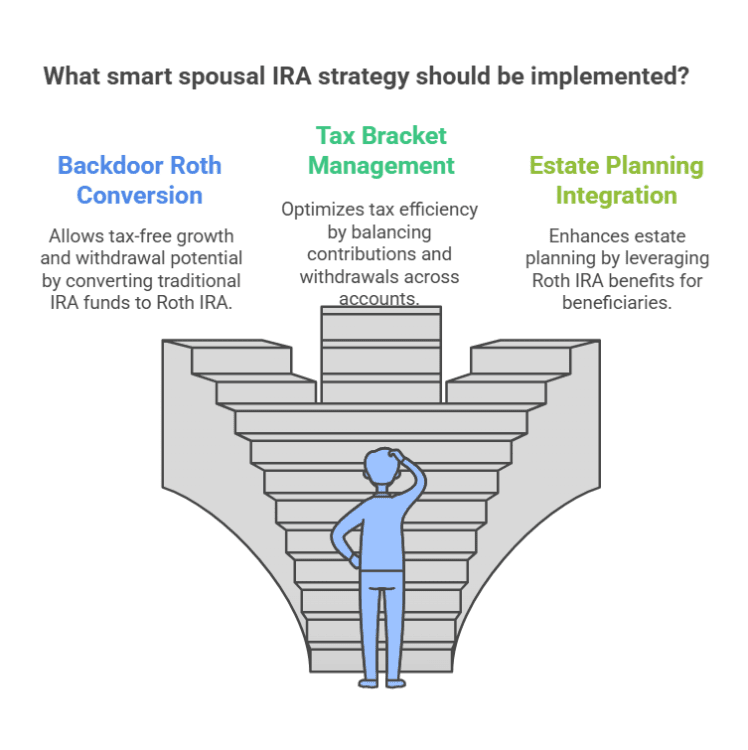

Advanced Strategies for High Earners

For my clients who were high earners (“Maximizer Marks”), the standard rules were just the beginning.

The Backdoor Roth IRA for a Non-Working Spouse

If your household income is too high to contribute to a Roth IRA directly (the MAGI phase-out for 2025 starts at $230,000 for joint filers, according to the latest IRS announcements), you can use the Backdoor Roth IRA strategy for the non-working spouse.

For my high-earning clients whose income exceeded the MAGI phase-out, the front door to a Roth IRA was closed. So, we used the back door.

The Process:

- Contribute the maximum amount to a new, empty Traditional Spousal IRA. Do not take a tax deduction for this contribution.

- Wait a few days for the funds to settle.

- Convert the full balance of the Traditional IRA to a Roth IRA.

Because you didn’t take a deduction, the conversion is a non-taxable event. This legally bypasses the income limits.

Warning:

This strategy can create a major tax headache if the receiving spouse has any other pre-tax IRA assets. This is known as the pro-rata rule (critical component of the Roth conversion rules). And it’s a trap I’ve helped many clients navigate. Do not attempt this without consulting a professional.

How to Open a Spousal IRA in 15 Minutes

Ready to take action? Here are the simple, concrete steps.

- Choose a Brokerage.

Go with a low-cost, reputable firm like Vanguard, Fidelity, or Charles Schwab. - Select “Open a New IRA.”

Remember, you are opening a standard Traditional or Roth IRA. There is no special “Spousal IRA” button. - Enter the Receiving Spouse’s Information.

The account must be in the name and Social Security number of the non-working or lower-earning spouse. They are the owner. - Fund the Account.

Link the joint bank account and transfer the contribution. The money can come from a joint account or from the working spouse’s individual account. - Designate the Tax Year.

When you contribute between January 1st and the tax filing deadline (usually April 15th), you can choose to apply it to the previous year or the current year. Our guide to the IRA contribution deadline explains this in detail. - Invest the Funds.

The money is in the account, but it’s not invested yet! Choose a simple, low-cost investment like a Target-Date Index Fund or a broad-market ETF.

Now, try searching for: IRA contribution limits, Roth conversion rules, or retirement planning guide.

Conclusion: The Ultimate Financial Equalizer for Your Family

In my three decades of planning, I’ve seen that the Spousal IRA is often the unsung hero of a successful retirement plan. It’s more than just a savings vehicle; it’s a tool of financial equality. It ensures that both partners in a marriage have the dignity and security of their own retirement nest egg, regardless of who earns the primary paycheck.

It transforms a potential retirement gap into a powerful, shared opportunity. By understanding the rules and using the strategies in this guide, you can turn your family’s teamwork into a legacy of financial strength as you work to get your personal finances in order.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.