Managing serious wealth, the kind that spans generations, isn’t about chasing trendy stocks. It’s about building something that survives economic hurricanes. This requires a deep understanding of asset allocation, diversification, and risk management. For those looking to create a solid financial foundation, knowing how to save $2 million quickly can be a game changer.

I’m Michael Ryan. For nearly 30 years, I’ve been in the trenches with families navigating fortunes with nine, sometimes ten zeros. And here’s what nobody tells you: the strategies that built that mountain of wealth? They’re usually terrible at preserving it.

You might be thinking, “Great, another asset allocation lecture.” Bear with me. The playbook for ultra-high-net-worth families is nothing like what you’ve read elsewhere.

I’m about to pull back the curtain on how my clients actually blended private equity, real estate, alternatives, and yes, even public markets into something that doesn’t just grow wealth. It makes it bulletproof.

These aren’t ivory tower theories. These are the battle-scars-earned strategies that have helped families with $30+ million not just count their money, but make it matter for generations.

Ready to see how the titans really do it?

Alternative Investment Due-Diligence Readiness Evaluator

Screen a private or alternative investment for foundational risks, missing information, and the next level of diligence it may require.

Due-Diligence Readiness Result

Foundational issues

Unresolved diligence questions

Positive evidence already identified

Product-specific review points

Documents and evidence to request

Appropriate next step

Related education

Read the high-net-worth asset-allocation guideWhat Really Sets UHNW Wealth Apart? More Than Just Commas.

So, you’ve crossed that $30 million threshold in investable assets. That’s a monumental achievement, no doubt. But here’s the thing: it’s time to shift gears, maybe even change vehicles. The hard-charging strategies that got you here often need a serious overhaul.

At this stage of the game, it’s less about the sprint of “getting rich” and much more about the marathon of staying wealthy, thoughtfully and purposefully. Many UHNW individuals, especially those newer to this level of wealth, find this mental pivot surprisingly tough. For years, a significant part of my role was helping clients reframe their thinking around this crucial transition. It’s not just about having more; it’s about what that ‘more’ is for.

Globally, according to firms like Wealth-X, fewer than 290,000 people manage this level of wealth, A figure that has seen steady growth, with North America currently home to the largest contingent. They’re not just abstract numbers; they represent families with complex needs. Businesses with far-reaching impact, and legacies in the making.

The core objective often transforms from aggressive accumulation to a multi-faceted approach. Preserving capital, smart growth above inflation, and ensuring that wealth can sustain future generations and philanthropic ambitions.

The question I’d often pose to new UHNW clients was, “Now that you’ve ‘made it,’ how do we ensure this wealth not only lasts but also enriches the lives and causes you care most about, for decades to come?”

The UHNW Portfolio: Architecting Your Legacy, Brick by Thoughtful Brick

If your current portfolio still vaguely resembles a larger version of your old 401(k) or SEP IRA, it’s probably time for a fundamental redesign. The UHNW toolkit you see, is vastly broader and for very good reasons. Sure, public equities and bonds are part of the landscape (foundations of most asset allocations) but they’re only the starting point.

The real strategic craftsmanship at this level lies in how you thoughtfully incorporate a portfolio of alternatives – things like private credit and direct real estate.

Let me tell you about a client, Frank. (Names are changed, of course, but the stories are real.) Frank was a brilliant entrepreneur, came to me right after his software company’s IPO. He was cash-rich, suddenly very liquid, but also, understandably, a bit anxious about the dot-com era market fluctuations and how to protect what he’d built.

He needed a financial plan that was more robust than just a standard stock and bond portfolio. Together, we didn’t just throw money at the market; we meticulously built a diversified plan. This included carefully selected private equity to capture long-term growth. Some uncorrelated hedge fund strategies (this was back when they were less about leverage & more about actual hedging!. And even a slice of direct investment in income-producing commercial real estate.

That kind of tailored approach, moving beyond the obvious, is what UHNW planning is all about.

Strategic Allocation for the UHNW Investor: Beyond the Outdated 60/40

At the UHNW level, diversification isn’t just a buzzword; it’s a critical imperative. We’re not just talking about picking up a few different stocks or bonds. It’s about strategic deployment across a wide array of asset classes, many of which aren’t readily accessible to the average investor.

While every family’s goals dictate the precise mix, a well-constructed UHNW portfolio often looks something like this (remember these are illustrative ranges based on industry observations, YMMV):

- Public Equities: 25-35% (Often quality, dividend-payers, and global)

- Alternative Investments: 20-30% (This is a broad category including Private Equity, Hedge Funds, and Private Credit)

- Real Estate & Real Assets: 12-18% (Direct holdings, REITs, land)

- Fixed Income: 10-15% (Tax-efficient munis, inflation-linked bonds)

- Cash & Equivalents: 5-10% (For liquidity, opportunities, and a sleep-at-night factor)

- Collectibles & Passion Assets: 5-8% (Art, wine, classic cars – we’ll get to these!)

The significant weighting towards alternative investments and real assets is what often sets these portfolios apart. As Jordan Thomas, a wealth strategist at Rockefeller Capital Management, has been quoted, “UHNW clients need two essential portfolio attributes: capital protection during downturns and participation in upside cycles.”

Alternatives, with their potential for non-correlated returns and inflation hedging, are absolutely critical tools in achieving that balance. These are often the core components that help a high-net-worth asset allocation truly serve long-term UHNW objectives. Moving far beyond simplistic asset allocation models.

What is the ideal asset allocation for ultra-high-net-worth individuals?

“If anyone tells you there’s one ideal percentage mix that fits every UHNW family, they’re selling you something. It simply doesn’t exist. The ‘ideal’ allocation is intensely personal. It must be tailored to your family’s specific long-term goals, your comfort with different types of risk, your expected timeline for various financial needs, and, crucially, your overall tax picture.”

Michael Ryan of Michaelryanmoney.com:

However, the portfolios I’ve built for UHNW clients almost invariably leaned into a robustly diversified blend of public and private assets, with a laser focus on capital preservation and tax-smart strategies.

They often looked quite different from the ‘model’ portfolios you see peddled to retail investors.

Public Equities & Fixed Income: The Foundation, Reimagined

Now, public equities and fixed income might seem like old news. But even here, the UHNW approach requires a layer of sophistication. It’s not just what you buy, but how and why.

For example, when I was constructing the equity portion of a UHNW client’s portfolio the focus wasn’t typically on chasing short-term, speculative gains. Far from it. We concentrated on:

- Blue-chip, dividend-paying stocks:

Companies with robust balance sheets, strong moats, and a history of returning cash to shareholders. Think stability and income. - Market-dominant growth companies:

Businesses with sustainable competitive advantages, still growing but with established market positions – not the flavor-of-the-month tech darlings. - Strategic use of sector-specific ETFs:

For targeted exposure where it made sense, not just for diversification’s sake. - Global Reach:

It’s a global economy; UHNW portfolios almost always reflect that, looking for opportunities and diversification beyond domestic borders.

The goal? Steady, reliable growth with less volatility, especially during those inevitable market downturns. It’s about building that financial fortress we talked about.

The same philosophy applies to fixed income. It’s less about squeezing out the absolute highest yield and more about:

- Risk Mitigation: Acting as a shock absorber when equity markets get turbulent.

- Tax Efficiency: This is a big one. For my U.S.-based clients, tax-advantaged municipal bonds were often a cornerstone.

Why hand over more to Uncle Sam than legally necessary, especially when you’re in the highest tax brackets?

A 3% tax-free yield from a muni could be equivalent to a 5% taxable yield if your combined federal and state tax rate is 40% – that’s real money. - Consistent Cash Flow: Providing a predictable income stream.

This refined approach to even traditional assets is fundamental.

Alternatives: The UHNW Edge in Private Equity, Hedge Funds & Real Assets

For many UHNW individuals, alternative investments represent a vital strategic component. This is where we often see the most significant divergence from standard investment portfolios. We’re talking about asset classes like private equity (which might make up 15-25% of the total portfolio), certain types of hedge funds (perhaps 5-10%), and direct investments in real assets like commercial real estate (12-18%).

These are not for everyone; they often come with higher minimums, longer time horizons, and significant illiquidity. But the potential benefits? Access to unique growth opportunities, returns not closely tied to public markets, and inflation protection can be compelling.

“But Michael,” I hear you ask, “aren’t these incredibly complex and risky?” They can be. And that’s precisely why rigorous due diligence and expert guidance are non-negotiable.

I’ve spent more hours than I can count vetting private equity managers and scrutinizing direct real estate deal. Checking the assumptions behind the glossy projections. The aim is always to ensure these investments genuinely align with my clients’ long-term objectives and risk tolerance.

A common finding in leading industry surveys – such as UBS’s Global Family Office Report and Campden Wealth’s North America Family Office Report – is that a large majority (often exceeding 80%) of family offices now make direct investments to secure greater control and negotiate more favorable terms.

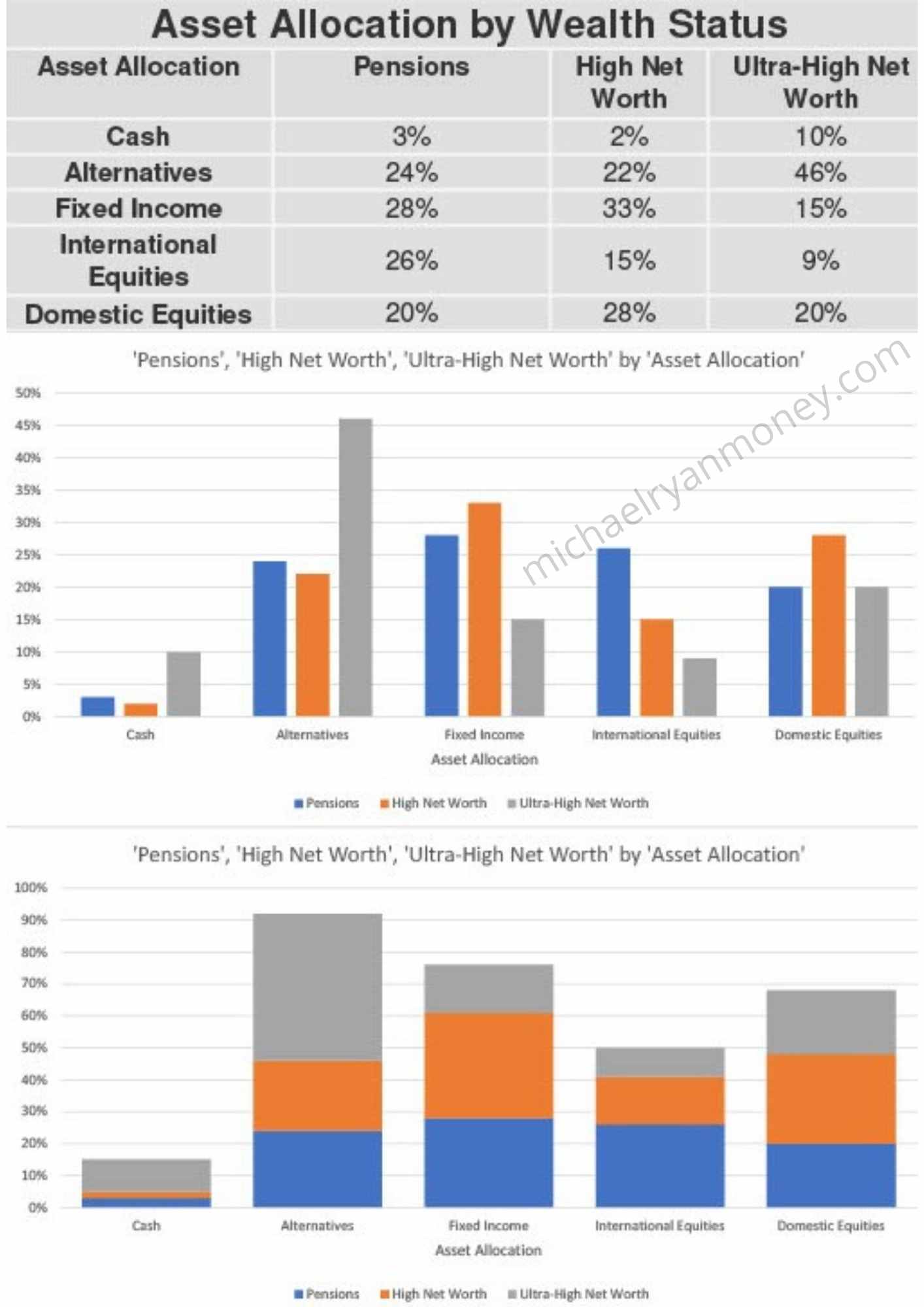

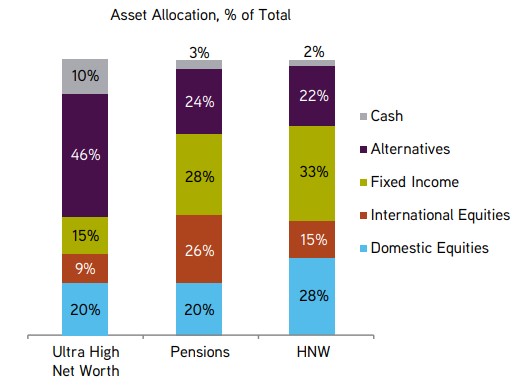

Asset Allocation % of Total for High Net Worth, Ultra High Net Worth investors and Pensions

Source: KKR

It’s vital to understand the nuances. For example, with private equity, you’re often looking at a “J-curve” effect – initial paper losses as investments are made, before (hopefully) significant appreciation later on. Patience isn’t just a virtue here; it’s a requirement.

If a 7-to-10-year lock-up on your capital makes you break out in a cold sweat, then certain alternatives might not be the right fit, no matter how shiny the projected returns.

The key is tailoring. For one client, it might be a carefully selected basket of venture capital funds to capture early-stage innovation. For another, it could be investing in a portfolio of income-producing commercial properties.

There’s no one-size-fits-all answer, only the right answer for a specific family’s unique circumstances and legacy goals. For a deeper understanding of the alternative investment landscape, the CAIA Association offers excellent educational resources.

What are typical alternative investment allocations for UHNW individuals?

"There's no magic percentage, as it's intensely personal to the family's goals and risk appetite. However, it's not uncommon for alternatives (encompassing private equity, certain hedge funds, direct real estate, and private credit) to make up 20% to even 50% of a UHNW portfolio.

The 'why' is key.

They offer potential for higher returns, diversification away from public market swings, and inflation hedging. But remember, these often come with illiquidity and demand serious homework before committing capital. You're trading daily liquidity for potential long-term outperformance and access to unique opportunities."

- Michael Ryan

ESG, Crypto, and The Cutting Edge: Where Prudence Meets Progress

Now, let’s touch on a couple of areas that are increasingly part of the UHNW conversation: ESG (Environmental, Social, and Governance) investing and the ever-evolving world of digital assets, including cryptocurrencies.

The landscape is always shifting, and part of smart UHNW planning is understanding these shifts without getting swept away by hype.

When it comes to ESG and impact investing, especially for younger UHNW family members; our “Elena ‘Next-Gen Heir'” persona comes to mind. We’ve seen a significant evolution here. It’s not just about avoiding companies with poor environmental records anymore. It’s about proactively seeking investments that generate a measurable positive impact alongside a financial return.

Think investments in clean energy infrastructure, sustainable agriculture, or educational technology. According to reports from groups like the US SIF Foundation or the Global Impact Investing Network (GIIN), a substantial portion of UHNW families are now integrating these factors.

My experience? When approached thoughtfully, aligning wealth with values doesn’t have to mean sacrificing returns; often, it means investing in the sustainable future.

Then there’s crypto. Ah, crypto. A topic that can elicit strong reactions! My usual starting point with clients curious about Bitcoin or other digital assets has always been one of extreme caution.

For the core UHNW portfolio, this is generally not where you want to be taking significant risks. I’d often say, “If you’re determined, let’s treat this like a very small, speculative ‘Vegas money‘ allocation. Not your legacy capital.” That said, some UHNW individuals, often guided by a younger generation or a very high-risk tolerance for a tiny slice of their wealth, are exploring:

How are UHNW individuals approaching cryptocurrency investments?

- Tiny allocations (1-2%, if that) to established cryptocurrencies.

- Venture capital funds focused on blockchain technology (the underlying engine, which is different from the currencies themselves).

- The tokenization of traditional assets. A fascinating space, but still very early.

Is this area evolving? Absolutely. Could blockchain technology be transformative? Possibly. But for now, for a UHNW portfolio primarily focused on preservation and steady growth, this remains a highly speculative and very small consideration, if any.

The key is to distinguish between the speculative froth and genuine, long-term technological shifts. And that requires a healthy dose of skepticism and expert guidance.

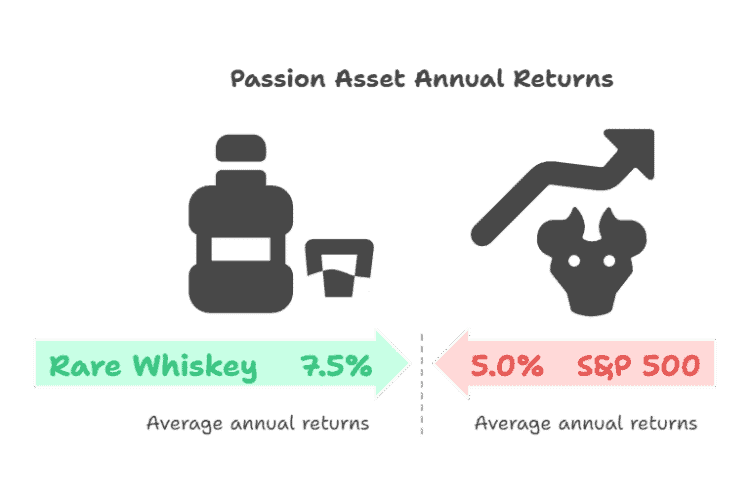

Passion & Legacy: Collectibles, Art, and “Emotional Dividends”

Now, let’s step away from the purely financial for a moment and talk about the assets that often bring as much joy as they do diversification: your passions. UHNW individuals often allocate 5-8% of their wealth to collectibles and passion assets. Think fine art, rare watches, classic cars, fine wine, or even rare manuscripts.

I’ve seen clients light up discussing their art or classic car collections in a way no stock certificate ever could. My role was often to help them structure these passions wisely. For enjoyment, yes, but also for preservation and potential appreciation, ensuring it wasn’t just a very expensive hobby.

The art market, for instance, according to indices like the Knight Frank Luxury Investment Index, has delivered average annual returns of around 7.5% over the past 25 years. Bet you didn’t know some rare whiskeys have outperformed the S&P 500 in recent years… but that doesn’t mean you fill your cellar without expert advice! It’s not just about the ROI in dollars, but the ROI in joy and connection to something tangible.

These assets offer several unique benefits:

- Low correlation with financial markets: They often move to their own rhythm.

- Tangible value: Especially during times of currency instability or high inflation.

- Cultural and historical significance: Which can enhance long-term value.

- “Emotional dividends”: The sheer joy of ownership and engagement with something you love. There’s a profound connection to history or artistry for many.

A newer trend is fractional ownership. Allowing diversification across multiple high-value assets rather than concentrating in a few pieces. This can make entry into, say, a blue-chip Picasso or a rare Ferrari collection more accessible.

However, investing in passion assets requires specialist knowledge, due diligence on provenance, understanding of storage and insurance costs, and a clear eye on liquidity (or lack thereof).

I always told clients, if you’re going to buy that multi-million dollar painting, love it. Because there’s no guarantee it’ll beat the market. But if it brings you joy, and we’ve done our homework on provenance and value, then it can be a wonderful part of a truly diversified UHNW life. The key is passion informed by prudence. When managing your passion assets wisely, these can be a fulfilling part of the UHNW tapestry. For broader fine art market trends, sources like Artsy can offer insights.

How do taxes impact UHNW asset allocation?

Taxes aren’t just an afterthought for UHNW investors; they’re a co-pilot in every single investment and structural decision. We’re talking about a fundamental focus on maximizing after-tax returns, not just chasing headline numbers. This involves strategically locating assets in the right types of accounts.

Using vehicles like dynasty trusts or PPLI to shield growth, managing capital gains carefully, and often integrating sophisticated philanthropic strategies. Get this right, and you can add what we call ‘tax alpha’ – a significant boost to long-term wealth. Get it wrong, and you’re simply making Uncle Sam a much larger beneficiary of your hard work than necessary.”

Dynamic Allocation & Rebalancing: The UHNW Approach to Market Shifts

Set-it-and-forget-it? Not when you’re managing a fortune designed to last generations. The truly savvy UHNW investor knows their allocation needs to breathe with the markets, adapting to new realities. I can’t tell you how many UHNW clients came to me with portfolios that had drifted wildly off course from their intended targets because their previous advisor just set static percentage bands for rebalancing and then walked away until the next annual review.

What if your portfolio was heavily overweight equities just before a major downturn because you weren’t dynamically rebalancing? That’s not just a paper loss; that’s a hit to real, generational wealth.

Dynamic asset allocation means having a strategic framework that allows for tactical adjustments based on market conditions, valuations, or changes in your own circumstances, rather than just rebalancing back to a fixed target once a year or when a band is breached by a fixed percent. It’s about having a plan before the storm hits.

Think of your strategic asset allocation as your ship’s rudder, and dynamic rebalancing as the skilled captain adjusting the sails. A static approach is like lashing the wheel and hoping for the best.

I taught my clients to watch certain ‘weather patterns’ – say, extreme market sentiment (both fear and greed), significant shifts in economic indicators like inflation or interest rate expectations, or when certain asset classes got way out of whack with their historical values or their contribution to overall portfolio risk. That was our cue to trim here, add there, always guided by the long-term map outlined in their Investment Policy Statement (IPS). Which, by the way, is an absolutely indispensable document.

The market doesn’t care about your annual review schedule. Opportunity and risk arrive unannounced. Your rebalancing strategy needs to be ready to answer the door.

Key triggers for dynamic rebalancing might include:

- Volatility Spikes: Significant increases in market volatility might trigger a reduction in risk assets or a shift to more defensive postures.

- Valuation Thresholds: If an asset class becomes extremely overvalued or undervalued relative to historical norms or your own targets.

- Economic Regime Shifts: Material changes in inflation, interest rate outlooks, or GDP growth trends.

- Liquidity Events: Large cash inflows (like Frank’s business sale) or significant planned outflows.

- Changes in Family Goals or Risk Tolerance: For example, as Elena takes on more responsibility, her views on impact investing might influence allocation shifts.

This isn’t market timing in the speculative sense; please don’t misunderstand me. It’s disciplined risk management and strategic opportunism based on pre-defined rules.

Sophisticated UHNW investors and family offices may even use tools like Monte Carlo simulations to stress-test their portfolios against various scenarios and understand potential sequence of returns risk, especially if the portfolio is supporting ongoing lifestyle distributions. This proactive approach helps in managing portfolio risk and navigating market shifts more effectively.

How often should UHNW portfolios rebalance?

Forget what the calendar says, for the most part. For UHNW portfolios, rebalancing shouldn’t be tied strictly to a quarterly or annual date like it’s some kind of dental appointment. Instead, it should be driven by strategic triggers and ranges defined in your Investment Policy Statement.

This means you rebalance when an asset class drifts too far from its target allocation – say, equities grow to be 5% over their target – or when significant market events or changes in your family’s circumstances warrant a review. It’s about discipline and responding to material changes, not just a date on the wall.

This dynamism is key to managing risk and capturing opportunities over the long haul.

Conclusion: Architecting Your UHNW Legacy, Not Just a Portfolio That Looks Good on Paper

So, after all these strategies and structures, what’s the real takeaway for managing ultra-high-net-worth wealth? It’s this: building and managing a UHNW portfolio is one of the most significant responsibilities one can have. It’s not just about financial engineering; it’s about being a steward for future generations.

The strategies we’ve discussed are tools. Powerful ones, to be sure. But the real art, the true value I’ve always strived to bring, lies in wielding those tools with wisdom, with discipline, and with a crystal-clear vision for the legacy you want to create.

In my three decades, the families who thrived weren’t just financially astute. They had a clear vision for their wealth, strong family governance, and a commitment to ongoing education and adaptation. They understood that wealth is a means, not an end.

Before we even talked about specific investments, I’d often ask clients, “What are the common mistakes you’ve seen others make, or are perhaps worried about yourselves?” And the answers were revealing. Many worried about chasing ‘hot’ tips without real diligence, or becoming dangerously over-concentrated in a single area (even if it was the family business that created the wealth).

They fretted about the corrosive impact of fees and taxes if not managed proactively. And the risk of a static allocation that didn’t adapt to major life changes or profound market shifts. And perhaps the biggest underlying fear? Not having that clear, written Investment Policy Statement to act as their North Star through it all.

Addressing these upfront is just as important as picking the right asset mix.

My best advice? It’s three-fold:

- Build a great, trustworthy team around you – legal, tax, investment. No one is an expert in everything.

- Stay relentlessly curious and committed to learning, because the financial world never stands still.

- And most importantly, never, ever forget the ‘why’ behind your wealth. That’s your compass.

Ready to move beyond generic advice and architect a UHNW asset allocation strategy truly built for your family’s future? If you’re looking for a seasoned perspective to guide that journey, perhaps start with my “Complete Guide to Asset Allocation” for foundational principles, or feel free to reach out to discuss your specific UHNW asset allocation needs when you’re ready for a deeper conversation.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.