“Michael, is the 60/40 asset allocation model portfolio dead?“

After 25+ years helping folks untangle their finances, I swear, I hear that question more now than ever before. And you know what? It’s fair. We all felt that gut punch in 2022. And again in April 2025. That old reliable 60% US stocks, 40% US bonds mix? It didn’t just dip; it cratered; one of its worst years on record. (60/40 Portfolio performance study) Left a lot of smart, hardworking people feeling like the rug got pulled out from under them.what

Believe me, I get it. I’ve poured coffee for clients like Priya – sharp marketing director, totally on top of her game, but secretly terrified of making a big money mistake. And sat with retirees like Frank, a kind former teacher who wasn’t scared of market crashes as much as he was haunted by the thought of inflation silently eating away his nest egg. These aren’t spreadsheet problems; they’re middle-of-the-night worries.

But here’s something I learned deep in my bones over those decades: Panic is never a strategy. Market weather changes, sometimes drastically. But the foundations of smart investing? They tend to hold firm. And the absolute bedrock, the cornerstone of it all, are Asset allocation models.

Forget the hot stock your brother-in-law won’t shut up about. Seriously. How you divvy up your investments across different types of assets; growth engines like stocks, stabilizers like bonds, maybe some curveballs like alternatives – that decision is going to have a bigger impact on whether you reach your goals (and how bumpy the ride is!) than almost anything else.

So, in this guide, we’re skipping the Wall Street jargon and the flavor-of-the-month hype. We’ll break down the different ways to approach asset allocation. The time-tested strategies and the newer kids on the block. In plain English.

More importantly, I’m pulling back the curtain on the practical, battle-tested framework I used for years to help real people build portfolios that actually fit their lives. We’ll talk straight about the common tripwires I saw folks stumble over. My aim isn’t just to lecture; it’s to give you the kind of clarity and confidence that comes from having an experienced guide by your side. Let’s get into it.

Asset Allocation Scenario Modeler

Compare hypothetical long-term outcomes for sample asset allocations. Results are educational illustrations, not forecasts or personalized recommendations.

Explore allocation approaches

Model sample outcomes

Illustrative outcomes

Simplified methodology

- 800 simulated paths are calculated for each sample portfolio.

- Hypothetical arithmetic annual returns and volatility: stocks 8% and 15%; bonds 3% and 5%; alternatives 5% and 10%.

- Asset returns are modeled independently using a normal distribution and limited to a maximum annual loss of 95%.

- Contributions are added at the beginning of each modeled year, followed by annual rebalancing.

- Results are nominal and exclude inflation, taxes, fees, withdrawals, and product-specific factors.

- Identical inputs produce identical illustrations so comparisons remain consistent.

The 10th-to-90th percentile range is not a best- or worst-case range. Actual markets may produce materially different results. This tool is an educational starting point and does not recommend an allocation or provide personalized financial advice.

Get practical financial education in your inbox.

What IS Asset Allocation? (Hint: It’s More Than Just Pie Charts)

“Asset Allocation.” Sounds a bit stuffy, doesn’t it? Maybe brings to mind those generic pie charts in glossy brochures. But what it really means is simply deciding the recipe for your investment portfolio. What percentage goes into the main investment categories, or asset classes?

When I worked with two friends, same age, same salary — one was all crypto, the other mostly CDs. Why? Their personalities, not math, drove their allocation. And that’s the first truth: asset allocation is less about equations than emotion and intention.

Think of these as your core food groups for investing:

Stocks (Equities)

Your potential powerhouse for growth. Owning tiny pieces of companies. They can deliver fantastic returns over time, but buckle up. They come with volatility (those sometimes nausea-inducing ups and downs).

Bonds (Fixed Income)

Often the portfolio’s shock absorber. Essentially, loans you make to governments or companies. They generally offer more stability and income than stocks, acting as ballast when the stock market gets stormy.

Cash & Cash Equivalents

Your safety net and “opportunity fund.” Think high-yield savings accounts, money market funds. Ultra-safe, easy to access, but don’t expect them to grow much, inflation often outpaces them.

Alternative Investments

The spice rack. This is a catch-all for everything else: real estate (often via REITs – Real Estate Investment Trusts), commodities (like gold or oil), private equity (investing in companies not on public stock exchanges), hedge funds, and yes, even things like cryptocurrency.

These often behave differently from stocks and bonds, which can be great for diversification, especially when traditional assets move together (like they frustratingly did in 2022).

- For more about asset allocation and how it helps you, read our Full Guide to Asset Allocation here. Or our article about High Net Worth Asset Allocation

Now, why all the fuss about the asset mix?

It boils down to two critical ideas: managing risk through diversification and the fact that your portfolio allocation drives most of your portfolio’s bumpiness.

The brilliant Harry Markowitz, who literally won a Nobel Prize for figuring this stuff out (Modern Portfolio Theory, or MPT), famously called diversification “the only free lunch in finance”. The idea is that by owning a mix of assets that don’t all move in lockstep (they have low correlation, here’s an asset correlation map).

You can potentially lower your overall portfolio risk without necessarily giving up long-term return. It’s like having both an umbrella and sunscreen. You’re better prepared for different weather. But, let’s be clear: it doesn’t mean you won’t lose money sometimes, and owning 50 different tech funds isn’t diversification; it’s just concentrating your bet! True diversification involves fundamentally different types of risk.

In 2022, I ran a what-if simulation for five clients. One who owned tech stocks, another with a diversified allocation. Over 12 months, the diversified client had 60% less volatility and slept way better. Harry Markowitz might’ve called that ‘the only free lunch,’ but I call it insurance for sanity.

Asset Allocation vs. Diversification

So, what’s the difference again?

- Asset allocation is the big picture strategy. Setting your target percentages for stocks, bonds, cash, alternatives.

- Diversification is the tactic you use within and across those buckets. Owning multiple stocks, various types of bonds, maybe some international exposure, etc., to avoid putting all your eggs in one tiny basket.

And the impact of that big picture strategy? Huge.

Seminal research, like the Brinson, Hood, and Beebower studies, consistently points to the asset allocation decision being responsible for the vast majority (often cited as 90%+) of a portfolio’s return variability over time.

Read that again. It’s not which stock you pick, but the overall mix that largely determines how much your portfolio jumps around. Getting that fundamental structure right, aligned with your life, is job number one.

The “Big Three” Allocation Flavors: Finding Your Investing Personality

Okay, let’s talk practical approaches. Forget the dry textbook stuff for a minute. I think of these as different investing personalities. Which one sounds most like you?

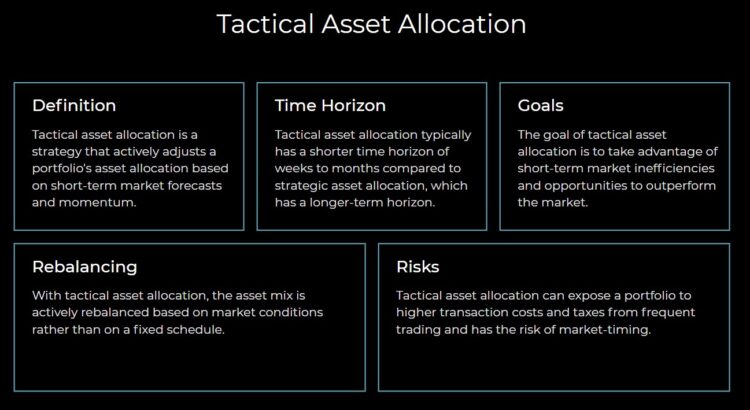

Strategic vs Tactical Asset Allocation

What’s the real difference between strategic and tactical allocation? It’s about your timeframe and what you believe drives returns. Strategic is the long-haul plan; Tactical is the short-term bet. Dynamic tries to automate the adjustments.

Jason, a tech exec, bet on oil stocks in 2022 thinking he was being tactical. They tanked. We had to rebuild his plan from scratch, and honestly, his confidence too

Feeling unsure which approach aligns best with your personality and goals? Take our quick ‘Asset Allocation Starter Quiz’ later in this guide to get a personalized pointer.

Let’s unpack these personalities:

Strategic Asset Allocation: The Marathon Runner

The philosophy: Slow and steady wins the race.

This was the foundation for probably 9 out of 10 client portfolios I ever built. You figure out a sensible long-term target mix based on your goals and nerve (more on that next). You build it with low-cost, diversified tools like index funds or ETFs.

And then comes the discipline: you rebalance it periodically. Quarterly or annual portfolio rebalance, or if an asset class drifts significantly (say, 5-10% off target) just to bring it back in line. That’s it. No chasing headlines, no panicked selling.

Why does this work?

Because over decades, different asset classes tend to deliver returns commensurate with their risk. Trying to perfectly time the market’s zigs and zags? Good luck. Most fail miserably. Strategic allocation relies on discipline and the power of compounding.

Who’s it for? Almost everyone investing for goals five years or more away. It demands patience but offers sanity. It was the right fit for retirees like Frank who needed reliability above all else.

Tactical Asset Allocation: The Day Trader Wannabe (Usually)

The mindset: “I can outsmart the market!”

Tactical starts with a strategic base but then actively makes short-term bets. Think loading up on energy stocks because you think oil prices will spike, or slashing your bond holdings because you’re convinced interest rates are heading to the moon. It’s seductive, the idea of dodging downturns and catching updrafts.

But here’s the cold, hard truth I saw play out again and again: Successfully timing the market consistently is extraordinarily difficult. Even many professionals can’t do it reliably, let alone individual investors glued to CNBC. The DALBAR studies consistently show that investors underperform the very funds they invest in.

Largely because of emotional, poorly timed tactical moves. High trading costs and taxes eat away at any potential gains too. While a sophisticated advisor might use tiny, well-researched tactical “tilts,” for most people, it becomes a costly exercise in chasing yesterday’s news.

I actively discouraged clients like Jason, often drawn to the ‘optimization’ idea, from making significant tactical bets. The risk of getting it wrong is just too high.

Dynamic Asset Allocation: The Algorithm Approach

The idea: Let the computer decide based on rules.

Dynamic models automatically adjust the portfolio mix based on pre-set signals. Maybe market valuation metrics (like P/E ratios), economic indicators, or volatility levels. Think of it like a car’s traction control system, trying to adapt to changing road conditions.

The appeal is taking emotion out of the equation.

The reality? Building and back-testing robust dynamic models is complex, PhD-level stuff. Models based on past relationships can fail when those relationships change (like the stock-bond correlation flip in 2022).

And even if the model is sound, sticking to its signals when they feel ‘wrong’ requires immense discipline. While interesting for institutional players or specialized quantitative funds, it’s generally not a practical DIY strategy.

Key takeaway? For most people, Strategic Allocation is the most reliable path. The real customization comes not from market timing, but from tailoring that strategic mix perfectly to you.

What REALLY Drives Your Allocation? (Spoiler: It’s Not Your Neighbor’s Hot Tip)

I can’t stress this enough: your neighbor Bob’s portfolio is irrelevant.

Your brother-in-law’s stock pick is irrelevant.

Your allocation needs to be built around your unique life circumstances. When I sat down with a new client, we spent most of our first meeting unpacking these four critical pieces:

Factor 1: Your Time Horizon (How Long is the Runway?)

This is the simplest but maybe the most important factor. Money you absolutely need in the next 1-5 years (for a house down payment, upcoming tuition bill) has no business being in volatile stocks. It needs safety. Think high-yield savings, CDs, maybe very short-term bonds.

But money you won’t touch for 10, 20, 30 years or more? That’s where you need the growth potential of equities to outpace inflation and build real wealth. You have time to recover from market downturns. Mismatching your timeframe to your risk level is a classic mistake.

Factor 2: Your True Risk Tolerance (The Gut Check)

This isn’t just a checkbox on a form; it’s about understanding your deep-seated reaction to seeing your hard-earned money fluctuate. There’s your financial capacity for risk (can you afford a loss without derailing your goals?) and your emotional willingness (can you sleep at night?).

I remember Priya, that marketing director. Brilliant, successful, claimed high risk tolerance on paper. Long time horizon, high income. Textbook aggressive investor, right? Then 2008 hit. The fear was real. She was ready to liquidate everything near the bottom.

Her gut tolerance was way lower than her paper tolerance. We had to dial back the risk in her plan to something she could actually live through without panicking. That behavioral gap, the difference between how investors should behave and how they do behave, often stems from this mismatch.

Michael Ryan Money Rule of Thumb:

Take your initial guess for stock allocation, then subtract 10-15%. That’s probably closer to your ‘sleep-at-night’ number. Be honest!

Factor 3: Your Specific Financial Goals (Why Are You Investing?)

“To make money” isn’t a goal; it’s a wish. Get specific. What are you saving for? Retirement? Kid’s college? Buying a business? Financial independence by age 50?

Each goal has a different target amount and timeframe, demanding a different strategy. Saving for multiple goals? You might even have different allocation “buckets” for each one. Clarity on the purpose of the money dictates the required return and the appropriate level of risk.

Factor 4: Your Complete Financial Picture (The Context)

Your allocation doesn’t exist in a vacuum. We need to consider:

- Income Stability: Rock-solid job vs. freelance/commission? More stability allows potentially more investment risk.

- Savings Rate: Are you saving 5% or 25% of your income? A higher savings rate can compensate for lower investment returns or allow for taking less risk.

- Existing Assets/Net Worth: Do you have home equity? A pension (like Frank did, which was a huge safety net)? Significant existing investments?

- Debt: High-interest debt (credit cards!) needs tackling aggressively, often before focusing heavily on investing beyond retirement account matches.

- Health & Longevity: Especially crucial nearing retirement. Potential healthcare costs and living longer than expected (longevity risk) need to be factored in, often suggesting a slightly more conservative approach initially in retirement.

Unpacking these factors honestly is the non-negotiable first step in building an allocation that won’t just look good on paper, but will actually serve your life.

Modern Twists: Risk Parity, Factors, and The Endowment Way – Should You Bother?

The investment world loves complexity, and new models pop up constantly. Let’s quickly cover the ones you might hear about, with a dose of my real-world skepticism:

Risk Parity: Balancing the Risk, Not Just the Dollars

The idea is clever: equalize the risk contribution from different assets, often using leverage on bonds.

The Problem: As we saw in 2022, when correlations go haywire and both stocks and bonds drop, leverage amplifies the pain.

It’s complex and adds risks many individuals shouldn’t take on. Usually best left to institutions, if anyone.

Factor Investing: Beyond Just “Stocks” and “Bonds”

Focusing on characteristics like Value, Momentum, Quality.

The Problem: Factors are cyclical and hard to time. Owning broad index funds already gives you exposure. Deliberately tilting requires expertise and risks chasing past performance. Interesting for pros like Marcus, likely unnecessary complexity for Elaine or Jason’s core portfolio. Research from firms like AQR often highlights the challenges.

Core-Satellite: A Practical Compromise?

A large, low-cost strategic core, plus smaller “satellite” bets on specific areas (sectors, factors, alternatives).

My Take: This can work well! It satisfies the desire to “do something” (like Jason might want) without jeopardizing the main plan.

Key: Keep satellites small (5-20% total), genuinely diversifying, and don’t churn them constantly.

The Endowment Model: Investing Like Yale (Good Luck!)

Huge allocations, often 50%+ (NACUBO data concept) to illiquid alternatives like private equity and venture capital, as pioneered by David Swensen.

The Problem: Individuals lack the access, expertise, scale, and infinite time horizon of a Yale. High fees, illiquidity, and complexity make this unrealistic and often dangerous to mimic. Adding a small sleeve of liquid alts (REITs, maybe gold) via the satellite approach? Fine.

Trying to replicate Swensen? Don’t do it.

My philosophy evolved over 25 years: Complexity is rarely the answer for individual investors. Mastering a simple, strategic allocation consistently usually beats chasing fancy models.

The Michael Ryan Resilience Allocation Framework™: My 7 Steps to Building YOUR Plan

Enough theory. Let’s get practical. How do you actually build this thing? Here’s the step-by-step process I used with clients for decades – focused on creating a plan robust enough to stick with.

Step 1: The Deep Dive – Goals, Timeline, TRUE Risk Tolerance

(Yes, again! Foundation first.) Get brutally honest. What’s the money for? When do you need it? How much downside can you actually stomach without freaking out? Write. It. Down.

Common Mistake: Using vague goals like “financial security” instead of specific targets.

Step 2: Choose Your Core Strategy – Keep It Real

Based on Step 1, pick your approach. For 90% of long-term goals, Strategic is the answer. Maybe Core-Satellite if you understand the risks and want a small active component. Be honest about your time, skill, and emotional bandwidth.

Common Mistake: Thinking you’ll be a disciplined tactical trader when you’re really not.

Step 3: Paint the Broad Strokes – Your Main Asset Buckets

Decide your target percentages for Stocks, Bonds, Cash. Keep it simple to start (e.g., 70% Stocks / 30% Bonds for Jason; maybe 50/50 for Frank). Then decide if a small (5-10% MAX) allocation to liquid Alternatives (like a diversified REIT ETF or a gold ETF) adds value for you.

Common Mistake: Over-complicating with too many niche asset classes too early.

Step 4: Fill the Buckets – Pick Your Tools (Low-Cost ETFs/Funds)

Now select investments. My strong advice: use low-cost, broadly diversified index funds or ETFs for your core. Think Total Stock Market (US + Int’l) and Total Bond Market funds. Cheap, simple, effective. Avoid single stocks or expensive, actively managed funds for the bulk of your money.

Common Mistake: Paying high fees for funds that simply hug their benchmark index anyway.

Step 5: Pull the Trigger – Implement!

Analysis paralysis is real. Once the plan is set, open accounts at a reputable brokerage (like Vanguard, Fidelity, Schwab) and actually invest the money according to your targets. Getting started is crucial.

Common Mistake: Waiting for the “perfect” time to invest, which never comes.

Step 6: Automate Your Defense – Set Rebalancing Rules

How will you maintain your targets? Decide now.

Rebalancing Frequency Calendar (e.g., annually) is easy.

Threshold (e.g., rebalance when any bucket is +/- 5% off target) is often more efficient. I preferred the 5% threshold rule – it avoids noise but enforces discipline.

Pick one, write it down in your IPS.

Common Mistake: ‘Set and forget’ turning into ‘drift and regret’ as allocations get way out of whack.

Step 7: Document & Review – Your IPS & Annual Check-up

Put Steps 1-6 into a simple Investment Policy Statement (IPS). Your roadmap. Your anchor. Then, schedule an annual financial check-up. Review performance, yes, but more importantly, review your life. Goals changed? Income changed? Approaching retirement? Adjust the plan if needed, thoughtfully.

Common Mistake: Never reviewing or adjusting the plan as life circumstances inevitably change.

This framework isn’t magic, but it’s grounded in reality and designed for resilience.

IPS Downloadable

Staying the Course: Winning the Battle Against Your Own Brain

Here’s the hardest truth: you can have the most brilliant allocation plan ever devised, and it can still fail if you let your emotions drive the bus off a cliff. That DALBAR study showing investors consistently lag the market? That’s the behavioral penalty in action – buying high in euphoria, selling low in panic. Your own brain can be your worst enemy. So how do you fight back?

Have That Written Plan (IPS)

I know I sound like a broken record, but when markets are plunging and headlines are screaming “SELL!”, pulling out that IPS you wrote when you were calm and rational is like a dose of smelling salts. This is the plan. Stick to it.

Automate, Automate, Automate

Set up automatic monthly investments from your bank account or paycheck. Dollar-cost averaging isn’t exciting, but it enforces discipline and prevents you from trying to time deposits based on fear or greed.

Control the Controllable

You can’t control the Fed, inflation, or what happens overseas. You can control how much you save, keeping investment costs low, sticking to your allocation, and crucially, managing your own reactions. Focus your energy there.

Go on a News Diet (Seriously!)

Constant financial pornography (excuse my language, but that’s what a lot of it is) is designed to trigger fear and action. Check your portfolio quarterly. Maybe monthly if you absolutely must. Turn off the noise, especially during volatile times. Sometimes strategic ignorance is bliss.

Remember History (But Respect Today)

Yes, markets have always recovered eventually. Knowing this helps during downturns like 2008 or the dot-com bust. But don’t get arrogant. This time always has unique wrinkles. Your plan needs to be resilient enough to handle surprises, not just based on past patterns repeating exactly.

Reframe Fear as Opportunity (If Appropriate)

If you’re decades from retirement like Jason, a market drop is a sale. Your regular contributions are buying more shares cheaper. Rebalancing might mean buying low too. It’s a mental switch, but it helps turn panic into calculated action.

Don’t Chase Ghosts or Shiny Objects

Resist the urge to pile into whatever did great last year. Resist the urge to overhaul your strategic plan based on short-term noise. Discipline isn’t sexy, but over 25 years, I saw it create far more wealth than market timing ever did.

Frequently Asked Questions (FAQ)

Let’s tackle a few more common questions I always got:

What asset allocation is really best for retirement?

Anyone giving you a single percentage is selling snake oil. There’s no universal ‘best’. It must be customized based on: How much income do you need to draw? What are your other income sources (Social Security, pension)? How long do you realistically expect to live (and potentially need healthcare)? What’s your comfort with seeing portfolio values fluctuate while you’re drawing income (sequence risk)?

While retirees often lower stock exposure, the right mix is deeply personal. Talk to a fiduciary advisor to build a withdrawal strategy and corresponding allocation.

How often should I actually rebalance? Feels like I should be doing something…

Less is often more! Annually is fine. Or use a 5% or 10% threshold rule (rebalance only when an asset class drifts that much). This avoids excessive trading (and taxes in taxable accounts) while keeping your core strategy intact.

Resist the urge to constantly tinker based on headlines. Follow the rule in your IPS.

Crypto? Real Estate? My buddy’s private deal? Where do they fit?

With extreme caution, in small doses, if at all. Treat crypto as speculation (1-2% max, if any, with money you can afford to lose).

- Direct real estate is a business – illiquid, costly, requires management.

- Private deals are usually off-limits and high-risk for individuals.

- REIT ETFs can offer liquid real estate exposure for a small slice (maybe 5%) of an ‘Alternatives’ bucket for diversification.

My thoughts? Nail your core stock/bond allocation first. Don’t add complexity you don’t fully understand or that doesn’t demonstrably improve your risk-adjusted return potential for your specific situation.

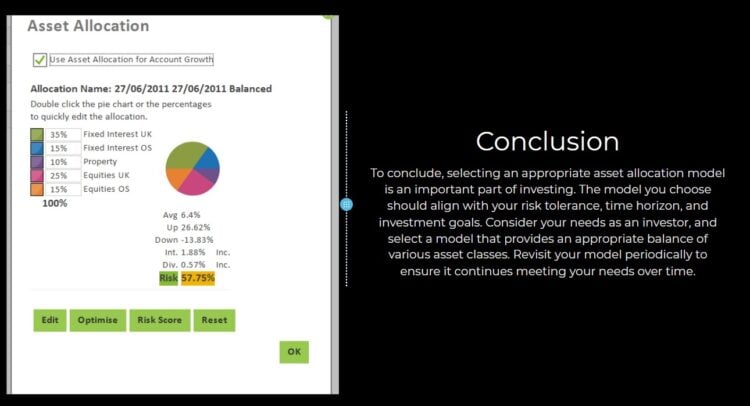

Conclusion: Your Allocation is Your Anchor, Not Just Numbers

So, after all that, what’s the one thing to remember?

The “perfect” theoretical asset allocation model is a myth. The best strategy for you, the one that will actually help you build wealth and sleep at night, is the one that:

- Is laser-focused on your real goals and timeline.

- Respects your actual tolerance for risk (the gut check!).

- Is simple enough for you to understand and stick with.

- Can be implemented consistently with low costs.

- You have the discipline to maintain through market chaos, resisting fear and greed.

Your asset allocation isn’t just a pie chart; it’s the financial engine built specifically for your journey. It’s the anchor that keeps you steady when the inevitable market storms hit. It’s the deliberate plan that turns today’s disciplined savings into tomorrow’s comfortable retirement for Frank, financial freedom for Priya, or whatever future you are building.

Building it right takes honesty with yourself, thoughtful planning, and then the hardest part – sticking to it. But the confidence and peace of mind that comes from knowing you have a plan tailored to your life? That’s priceless.

Disclaimer: The information in this article is for educational purposes only and does not constitute personalized financial advice. Investing involves risk, including the potential loss of principal. All anecdotes are based on generalized client experiences and have been anonymized and composited to protect privacy. Consult with a qualified, fiduciary financial professional before making investment decisions tailored to your specific situation.

Ready to build an allocation that truly fits? This guide gives you the framework, but applying it wisely takes care. If you’d like personalized help navigating these choices and building a resilient plan, let’s talk. [Link to Contact/Services Page]

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.