What if your life savings could never shrink, even if the stock market plunged tomorrow. Would you sleep better at night? For many people nearing retirement in 2026, with inflation still hovering around 3% and market uncertainty, that promise of absolute safety is the most powerful draw of a fixed annuity.

As a retired financial planner with nearly 30 years of guiding clients through volatile markets, I’ve seen that fear firsthand. I’ve also seen the look of relief when a client secures a predictable, guaranteed income stream they can’t outlive. Fixed annuities, often called the “CDs of the insurance world,” can be a powerful tool for this peace of mind.

But they are not a one-size-fits-all solution. The guarantees come with trade-offs. Namely, restrictions on your money and returns that may not keep pace with inflation. This guide is my unvarnished look at their genuine benefits and hidden drawbacks, built on decades of real-world client scenarios. We’ll cut through the sales pitches and give you the truth.

Key Takeaways: The 60-Second Verdict

- What It Is:

A fixed annuity is an insurance contract that pays a guaranteed, fixed interest rate on your investment. It offers principal protection, meaning your initial investment cannot be lost to market downturns. - The Biggest Pro of a Fixed Annuity:

Unmatched predictability and safety. It provides a stable, guaranteed income stream, making it a cornerstone for conservative retirement income planning. - The Biggest Fixed Rate Annuity Con:

Lack of liquidity and inflation risk. Your money is often tied up for years in a surrender period, and the fixed payments can lose purchasing power over time due to inflation. - Who Are Fixed Annuities For:

Best suited for risk-averse pre-retirees (55+) who prioritize capital preservation and predictable income over high growth, and have already funded other retirement accounts. - The Bottom Line:

Think of it as a tool for creating your own private pension. It’s not a high-growth investment, but a powerful longevity insurance product for a portion of your portfolio.

Key Takeaways Ahead

What Is a Fixed Annuity? A Simple Definition

Considering a fixed annuity to provide steady retirement income? In simple terms, a fixed annuity is a contract you make with an insurance company. You give them a sum of money (a premium payment), and in return, they promise to pay you a specific, guaranteed interest rate for a set number of years.

Many people compare it to a Certificate of Deposit (CD) from a bank, but with a few key differences:

- Tax-Deferred Growth: Unlike a CD, the interest earned in a fixed annuity compounds tax-deferred. You don’t pay taxes on the growth until you withdraw the money. Learn more about Tax Implications of Fixed Annuities here.

- Payout Options: At the end of the term, you can receive your money back or convert it into a stream of guaranteed income payments for life (a process called annuitization).

It is a principal-protected annuity, meaning the initial amount you invest is shielded from market fluctuations, offering a foundation of security for your retirement savings.

🔍 Explained Simply

Imagine you have a savings bucket. With a fixed annuity, the insurance company puts a lid on it, protecting the contents from any stock market storms. They also promise to add a specific amount of water (interest) to the bucket each year, guaranteed.

Understanding the Different Types of Fixed Annuities

“Fixed annuity” is a broad category. In practice, you’ll likely encounter these specific types:

- Multi-Year Guaranteed Annuity (MYGA):

This is the most popular type and acts most like a CD. It guarantees a fixed interest rate for a specific term, typically 3 to 10 years. It’s a straightforward accumulation product. - Single Premium Immediate Annuity (SPIA):

With a SPIA, you pay a single lump sum, and the insurance company begins paying you a guaranteed income stream almost immediately (usually within a year). This is a pure income-generation tool. - Deferred Income Annuity (DIA):

A DIA is the opposite of a SPIA. You pay a lump sum now in exchange for a promise of income payments that will start at a future date you choose, often many years down the road. This is also known as longevity insurance.

The Pros: Where Fixed Annuities Shine

1. Guaranteed Returns & Principal Protection

This is the main event. In a world of market volatility, a fixed annuity’s promise is simple: your principal is safe, and your return is locked in. As of early 2026, top-rated MYGA contracts guarantee rates between 5.2% and 7.65% depending on term length. If your contract guarantees a 6.5% minimum guaranteed rate, you will earn 6.5%. Period.

This stability can be a powerful anchor in a diversified portfolio, especially for those who can’t stomach market swings.

2. Tax-Deferred Growth

Your money compounds without you having to pay taxes on the interest each year. This allows your savings to grow faster than they would in a taxable account like a CD or savings account, especially if you are in a higher tax bracket.

This tax-deferred growth is a significant advantage for long-term retirement savings.

3. A Predictable Income Stream for Life

Through annuitization, you can turn your accumulated savings into a lifelong paycheck. This addresses one of the biggest fears in retirement: outliving your money. Knowing you have a check coming every month to cover essential expenses provides immense psychological comfort.

💡 Michael Ryan Money Tip

I often advised clients to use a fixed annuity to cover their non-discretionary “floor” expenses in retirement—like mortgage, utilities, and groceries. Once those were covered by guaranteed income, they felt more confident letting the rest of their portfolio grow in the market.

4. Simple Legacy Planning (Death Benefit)

Fixed annuities come with a death benefit. If you pass away during the accumulation period, your named beneficiary will receive, at a minimum, the full amount of your original investment.

This makes it a simple and direct way to pass money to heirs outside of the probate process.

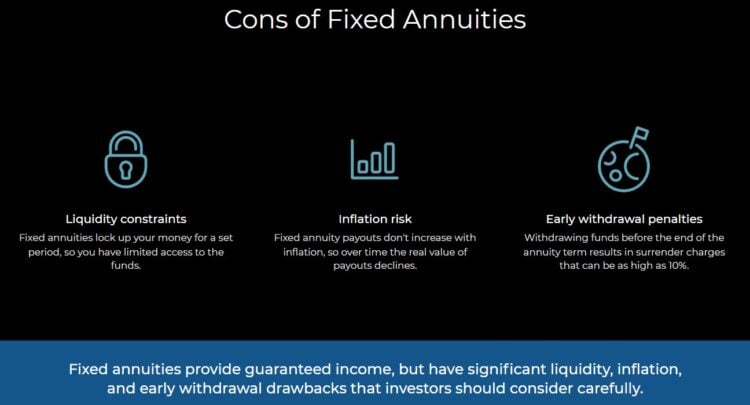

The Cons: The Critical Drawbacks to Consider

The guarantees offered by fixed annuities come at a price. Here are the trade-offs you must understand.

1. Limited Liquidity & Surrender Charges

Your money is not readily accessible. Most fixed annuities have a surrender period, often lasting 6-8 years. If you withdraw more than the allowed penalty-free amount (typically 10% per year) during this period, you will pay a steep surrender charge.

📉 Bad Advice to Ignore

A salesperson might say, “The surrender period doesn’t matter if you plan to hold it.” This is dangerous advice. Life is unpredictable. An unexpected healthcare emergency could force an early withdrawal, turning your “safe” investment into a costly one.

For example, a 7-year surrender charge schedule might start at 7% in year one and decrease by 1% each year. Withdrawing $50,000 in year two could cost you $3,000 (6%) in penalties.

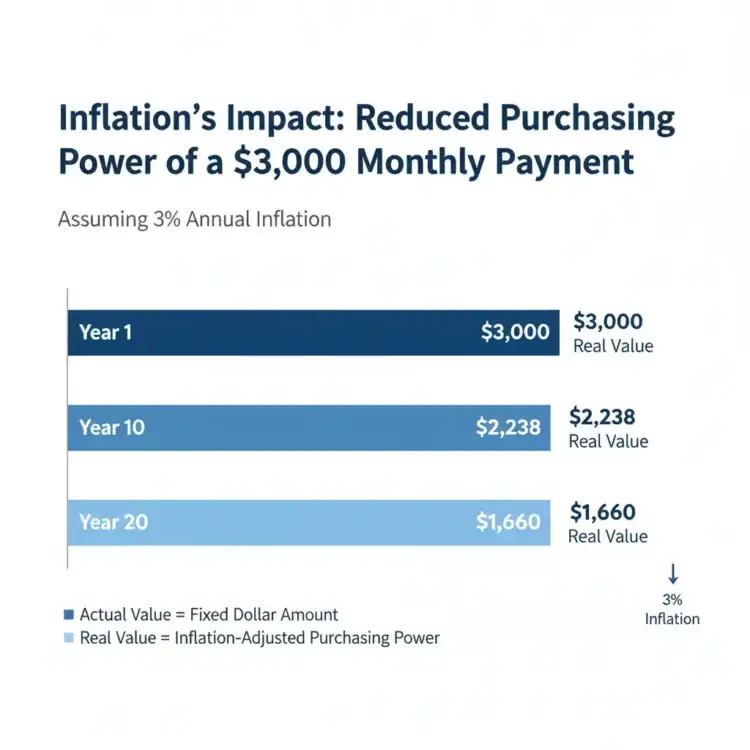

2. Inflation Risk Can Erode Your Purchasing Power

This is the silent killer of fixed income. With inflation projected at 3% in 2026, a guaranteed 6% return may feel comfortable today, but what happens if inflation rises to 4-5% in future years? Over a long retirement, even modest inflation can dramatically reduce the real value of your fixed payments.

| Year | Purchasing Power of $3,000/month |

|---|---|

| Year 1 | $3,000 |

| Year 10 | $2,232 |

| Year 20 | $1,653 |

| Year 25 | $1,433 |

Some annuities offer an inflation rider for an extra cost, but this reduces your initial payment amount.

3. Ordinary Income Tax on Gains

While growth is tax-deferred, all the interest you earn is taxed as ordinary income upon withdrawal, which is often a higher rate than the long-term capital gains tax you’d pay on stocks or mutual funds held in a brokerage account.

4. Potentially Lower Returns

The price of safety is modest growth. The guaranteed returns on fixed annuities will almost always be lower than the potential long-term returns of a diversified stock portfolio. It’s a trade-off: you’re sacrificing potential upside for downside protection.

Fixed Annuity vs. CDs and Bonds: A Head-to-Head Comparison

For a conservative investor, fixed annuities compete directly with other safe retirement investments like CDs and bonds. Here’s how they stack up:

| Feature | Fixed Annuity | Bank CD | Treasury I-Bond |

|---|---|---|---|

| Principal Safety | Backed by insurer & state guarantee fund | FDIC insured up to $250,000 | Backed by U.S. Government |

| Tax Treatment | Tax-deferred growth, gains taxed as income | Interest taxed annually as income | Tax-deferred growth, exempt from state/local tax |

| Liquidity | Low (Surrender charges apply) | Low (Early withdrawal penalty) | Medium (Locked for 1 year, 3-month penalty before 5 years) |

| Inflation Protection | Generally no, unless a rider is purchased | No | Yes, interest rate adjusts with CPI |

Myth Busting: What Advisors Don’t Always Tell You

⚠️ Myth Busted: “Fixed Annuities are completely illiquid.”

Reality: While they are not liquid investments, most contracts have **free withdrawal provisions**, allowing you to take out up to 10% of the value annually without penalty. Many also include a **nursing home waiver** or **terminal illness waiver** that allows full access in a crisis.

⚠️ Myth Busted: “The interest rate you see is the rate you get.”

Reality: Be wary of a potential **Market Value Adjustment (MVA)**. If interest rates have risen since you bought your annuity, the insurer may reduce your withdrawal value if you surrender early. Conversely, an MVA can increase your value if rates have fallen. Always check if your contract includes this feature.

Michael’s Take (The Commission Paradox): You might wonder why some advisors push complex variable or indexed annuities over simpler fixed ones. Research from the National Bureau of Economic Research suggests psychological factors, but my experience points to something simpler: commissions. A complex variable annuity can pay an advisor a 7% commission, while a simple fixed annuity might only pay 1-3%. Always ask your advisor how they are compensated. A true fiduciary will prioritize your needs over their paycheck.

Are You a Good Candidate for a Fixed Annuity? A Checklist

This isn’t an investment for everyone. See if your profile matches the ideal candidate for a fixed deferred annuity or MYGA.

Fixed Annuity Decision Checklist

Case Studies: When Fixed Annuities Worked (and When They Didn’t)

Success Story: Mark’s Journey to Financial Security

Mark, a 64-year-old engineer, had $500,000 in a volatile stock portfolio just a year before his planned retirement in early 2026. He was terrified of a market crash derailing his plans. We moved $200,000 into a 5-year Multi-Year Guaranteed Annuity (MYGA) with a guaranteed 6.45% annual rate—one of the best rates available in early 2026.

This secured $12,900 in predictable annual interest ($200,000 × 6.45%) and, more importantly, protected that principal from any future market volatility. It gave him the confidence to keep the rest of his portfolio invested for long-term growth.

Cautionary Tale: Emily’s Emergency Fund Mistake

I’ll never forget the panic in Emily’s voice. A 62-year-old client, she had placed a large portion of her savings into a 7-year fixed annuity. Two years later, she needed $40,000 for an urgent medical procedure. Because she was still deep in the surrender period, the penalty was 6%, a staggering $2,400 fee to access her own money.

It was a harsh lesson: an annuity is a retirement tool, not an emergency fund.

What if the Insurance Company Fails? Understanding the Safety Net

A common and valid question is: “Is my money safe if the insurance company goes bankrupt?” Unlike bank CDs, fixed annuities are not FDIC insured.

However, they are protected by State Guaranty Associations. Each state has a fund designed to protect policyholders if their insurer becomes insolvent.

📌 Key Takeaway

Protection limits vary by state but are typically around $250,000 per person, per company. This is why it is critical to check your state’s specific coverage and to work only with insurers that have high financial strength ratings.

How to Choose the Best Fixed Annuity Company in 2026

Selecting the right provider is just as important as choosing the right product. The “best” company depends on who offers the optimal combination of a competitive guaranteed interest rate and impeccable financial stability.

Key Factor: Insurance Company Financial Strength Ratings

Before you look at rates, look at the insurer’s claims-paying ability. This is graded by independent agencies like A.M. Best, Standard & Poor’s, and Moody’s. You should only consider companies with a rating of A (Excellent) or higher.

As of early 2026, some of the most competitive MYGA providers with strong A.M. Best ratings include MassMutual (A++), New York Life (A++), Northwestern Mutual (A++), and Nationwide (A+). These carriers consistently offer rates in the 6-7% range for 5-10 year terms. But don’t chase an extra 0.25% with a B-rated insurer. The rating matters more than the rate.

Final Verdict: What 30 Years of Client Work Taught Me About Fixed Annuities

In 2026, with interest rates still relatively elevated and market volatility persistent, fixed annuities are having a moment. The guaranteed rates we’re seeing (6-7.5% on quality MYGAs) are the best in over a decade. For the right person—someone who is risk-averse, nearing retirement, and values security above all else—they can be a robust part of a diversified asset allocation, providing a stable foundation for a long retirement.

However, for most others, the high costs, lack of liquidity, and inflation risk make lower-cost alternatives like CDs, bonds, or a simple, diversified portfolio of ETFs a more efficient path to building wealth.

Your Next Steps:

- Assess Your Profile: Honestly review the “Ideal Candidate” checklist.

- Compare Rates and Ratings: If you fit the profile, research current MYGA rates and the A.M. Best ratings of the top providers.

- Consult a Fiduciary Advisor: Before signing any annuity contract, get a second opinion from a qualified, fee-only financial advisor who is legally obligated to act in your best interest.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.