The straight answer: An annuity rider is an optional feature you can add to an annuity contract to provide specific benefits, like guaranteed lifetime income or long-term care coverage, in exchange for an annual fee. While these riders can be a powerful tool for securing your retirement, they come with costs that typically range from 0.25% to over 1.50% of your annuity’s value per year.

The biggest mistake investors make is either overpaying for annuity riders they don’t need or skipping a rider that could have saved their financial future.

Look, I’ve spent nearly 30 years as a financial planner, and I’ve seen people make two massive mistakes with annuity riders. They either waste money on riders they don’t need, or they skip the one that would’ve saved their retirement. I’m going to break down exactly which riders matter in 2026, what they actually cost, and which ones are complete BS.

We will break down the real annuity rider costs for 2026, compare the most critical options, and expose the annuity scam red flags you must avoid.

Here’s the thing: A rider’s whole purpose is to transfer a specific financial risk (like running out of money in retirement) from you to an insurance company. The real question is whether what you’re paying for that peace of mind is actually worth it.

Key Takeaways Ahead

First, What Is an Annuity Rider in Retirement Planning?

Think of a base annuity as a car and a rider as a specific performance upgrade. An annuity rider provides guaranteed income or other protections by customizing your contract. They are optional provisions that address specific risks and goals.

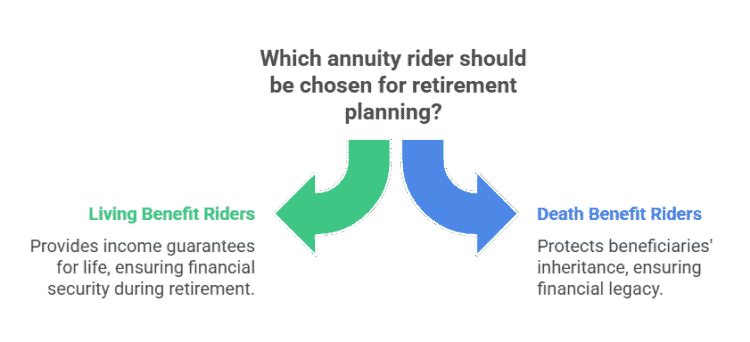

There are two primary categories you must understand:

Living Benefit Riders:

These provide protections and guarantees while you are still alive. The most common is the income guarantee, which ensures you receive a paycheck for life, even if your account value runs to zero.

Death Benefit Riders:

These are designed to protect your beneficiaries’ inheritance. They ensure your heirs receive a specific payout, often safeguarding the principal you invested.

As retirement expert Craig Hawley from Nationwide notes: “Americans are in danger of outliving their retirement savings as ongoing volatility compounds the existing challenges of greater longevity and an eroding retirement safety net.”

This is precisely the problem that a well-chosen rider is designed to solve.

The Most Important Annuity Riders in 2026 (And Which Ones Actually Matter)

While dozens of riders exist, a few have become critical in today’s financial landscape. Here is a breakdown of the most impactful options, including new and innovative riders being promoted now.

1. Guaranteed Lifetime Withdrawal Benefit (GLWB)

This is the heavyweight champion of income riders. A GLWB provides guaranteed lifetime income regardless of market performance.

- How it Works:

The rider creates a separate “benefit base” that typically grows at a guaranteed annual “roll-up rate” (often 5-8%). Your lifetime withdrawal percentage is applied to this benefit base, not your actual, lower account value if the market performs poorly. - Cost:

Typically 0.95% to 1.50% annually. - Best For:

Anyone whose primary fear is outliving their money or facing a market crash early in retirement.

Real Example: How a GLWB Saved a Client’s Retirement

In 2021, I had a client, “Robert,” a 64-year-old anxious pre-retiree. He had $500,000 and was terrified of a market crash like in 2008. We analyzed an annuity with a GLWB rider that had a 1.2% annual fee. Our modeling showed this would cost him approximately $6,000 per year. He was hesitant.

However, we then simulated a 30% market crash. Without the rider, his portfolio would have dropped to $350,000, permanently reducing his sustainable withdrawal income.

With the rider, his account value dropped, but his benefit base for lifetime income remained untouched at $500,000. The rider protected his future “paycheck” from the crash. For him, paying the $6,000 fee was a price well worth the security. As he called it, an insurance policy for his income.

2. Long-Term Care (LTC) Rider

With nearly 70% of Americans needing some form of long-term care in their lifetime, this rider has become a vital planning tool.

- How it Works:

A long-term care rider covers ADLs (Activities of Daily Living) assistance. It typically allows you to double your annuity’s income payments for a set period (e.g., five years) if you need help with two or more ADLs. - Cost:

0.60% to 1.25% annually. - Why It Matters:

Medicare does not cover most long-term care costs. An LTC rider can prevent you from liquidating your portfolio to pay for care.

What’s New for 2026: Emerging Rider Options

The industry is evolving. Here are two newer rider types gaining traction:

- Hybrid Growth & Income Riders (“Enhanced GLWB”):

- What They Are:

These riders blend a traditional income guarantee with a performance-based component. Your income base can “step up” to a new high on contract anniversaries if the market performs well, but it never loses value in a down market. - The Good:

Offers a chance for your future income to grow faster than a fixed roll-up rate. - The Bad:

The fees can be higher (1.25% – 1.60%), and the “step-up” feature often comes with participation rate caps, limiting your upside.

- What They Are:

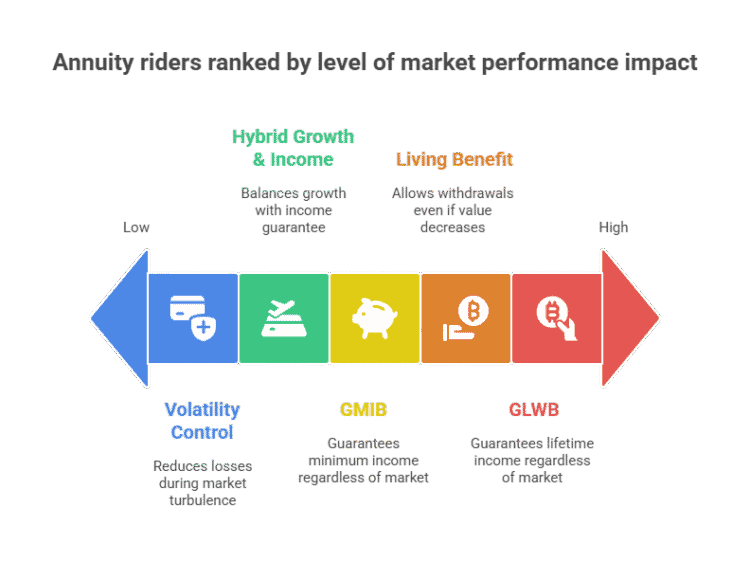

- Volatility Control Riders:

- What They Are:

These are often included in Registered Index-Linked Annuities (RILAs). They are not income riders but are designed to automatically shift your investment allocation to less risky assets when market volatility spikes, aiming to reduce losses. - The Good:

Provides a disciplined, automated way to de-risk your portfolio during turbulent times. - The Bad:

This automatic shift can cause you to miss out on sharp market rebounds. It can create a “whipsaw” effect if the market recovers quickly.

- What They Are:

- With the return of premium rider, if you decide to cancel your annuity or if you pass away, this rider guarantees that either you or your beneficiaries receive at least the amount of premiums paid into the annuity.

- What is a GMIB Rider? The Guaranteed Minimum Income Benefit (GMIB) rider ensures that you receive a minimum amount of income from your annuity, regardless of market performance. It’s like having a safety net for your retirement income. This rider is particularly beneficial if the market underperforms, guaranteeing you a baseline income.

- The living benefit rider in an annuity, especially in a variable annuity, offers additional security. It allows you to withdraw a certain percentage of your annuity’s value for living expenses, even if the actual value of the annuity decreases.

- Income riders on annuities, including those on variable annuities, are all about ensuring a steady income stream. They allow you to convert a part of your annuity’s value into a guaranteed series of payments. This is particularly appealing for those who want to ensure a consistent income during retirement.

- The annuity death benefit rider is about peace of mind. It ensures that in the event of your passing, your beneficiaries receive a specified amount, often the total premium paid or the annuity’s value at the time of death. It’s a way to ensure your loved ones are financially taken care of.

The Good, The Bad, and The Expensive: A Balanced View

Annuity riders are tools, and they come with clear pros and cons. To learn more, check out our guide on the Do’s & Don’ts for Baby Boomers Buying Annuities.

Annuity Scams & Red Flags to Watch Out For in 2026

The annuity market is complex, and unfortunately, it attracts some bad actors. Here’s how to protect yourself.

- Made-Up Titles and Certifications:

Stan “The Annuity Man,” a well-known industry watchdog, warns about agents using fake titles like “senior advisor specialist.” Look for legitimate, verifiable credentials like CFP® (Certified Financial Planner®) or ChFC® (Chartered Financial Consultant®). - The “Free Lunch” Trap:

Those expensive dinner seminars are designed to create a sense of obligation. As Stan advises: “Swallow the food, don’t swallow the pitch.” These events are almost always geared to sell you one specific, high-commission product. - Hidden Fee Structures:

Be vigilant about “fee stacking.” A contract might have administrative fees, mortality & expense charges, and multiple rider fees that can add up to 2-4% annually, severely dragging down your returns. Always ask for a full fee disclosure. - The Suitability Trap:

The biggest risk isn’t always outright fraud; it’s an unsuitable sale. An advisor might neglect to fully explain surrender charges (which can be 7-10% in early years) or other contract limitations because the product pays a high commission.

Warning: The Suitability Trap

Cyrus Bamji from the Alliance for Lifetime Income explains: “Overwhelmingly, these annuity fraud cases are based around ‘suitability,’ where an advisor neglects to share important information about fees, costs and other contractual features.” This is why working with a fiduciary advisor is critical.

Frequently Asked Questions (FAQ) About Annuity Riders

Are annuity riders worth it in 2026?

It depends on the value you place on the guarantee. If the peace of mind from a guaranteed lifetime income allows you to sleep at night and stay invested during market downturns, the fee may be well worth it. A financial advisor can help you run a break-even analysis.

What is the most popular annuity rider?

The Guaranteed Lifetime Withdrawal Benefit (GLWB) or other income riders are by far the most popular, as they directly address the primary retirement fear of outliving one’s money.

Can I cancel an annuity rider later?

In most cases, no. Riders are typically integrated into the contract at the time of purchase and cannot be removed later to lower fees. This makes the initial decision critically important.

Now, try searching for: Annuity Types, Annuity Taxation, LTC Rider vs Insurance.

Final Verdict: Making the Smart Rider Decision

In today’s environment of market volatility and increased longevity, the contractual guarantees offered by annuity riders have become more relevant than ever. With annuity base rates surging to over 7.7%—the highest in a decade—the underlying products are more attractive, which can help justify the cost of a well-chosen rider.

However, the key is strategic selection, not collection. Adding riders should be a precise surgical procedure, not a shopping spree.

Your Action Plan:

- Identify Your #1 Risk: Pinpoint your single greatest retirement fear (market loss, inflation, or a long-term care event).

- Isolate the Solution: Choose only the rider that directly addresses that primary risk.

- Calculate the True Cost: Ask for the rider fee in both percentage and dollar terms. A 1.2% fee on a $500,000 annuity is $6,000 per year. Is that price worth the guarantee it provides?

- Demand a Comparison: Ask your advisor to show you the same annuity without the rider to see the impact on potential growth.

Annuity riders are not inherently good or bad—they are tools. When used correctly, they can provide powerful security. But when sold improperly, they can be an expensive drag on your retirement portfolio. Your best defense is to arm yourself with knowledge and ask the tough questions before you sign anything.

This article was last updated in December 2025. The information here is for educational purposes and isn’t investment advice. Talk to a qualified fiduciary financial advisor about your specific situation. For more on annuities, check out the SEC and FINRA resources.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.