I’ll never forget a couple, the Flemings who came to my office back in 2009, right after the market crash had decimated their 401(k)’s. They were 67, retired, and terrified. Their number one question wasn’t about growth or returns; it was, “How can we make sure we never run out of money?”

For them, and for many retirees, the answer was an immediate annuity.

This guide is my near 30 years of experience distilled into a clear, honest playbook on this powerful tool.

We’ll cover what an immediate annuity is, how they work, how much income it can realistically provide, and the critical risks you must understand before you ever sign an annuity contract.

Key Takeaways Ahead

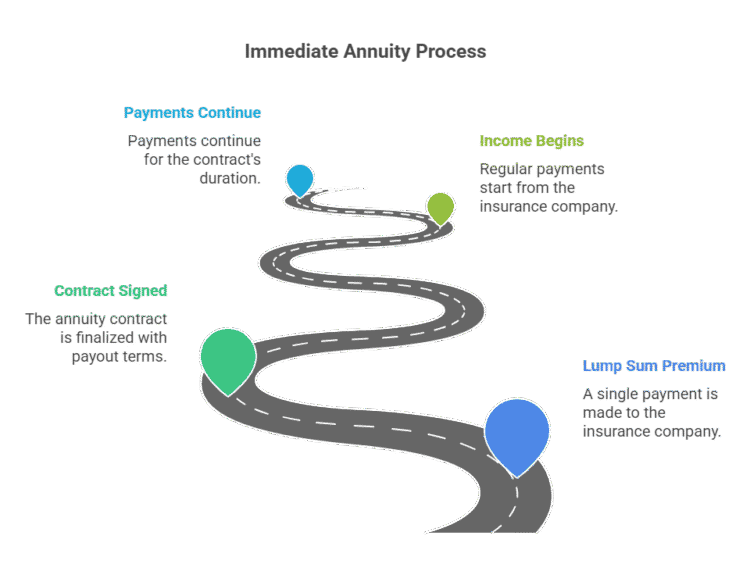

How an Immediate Annuity (SPIA) Works: The 4-Step Process

The concept is straightforward and has been around for centuries. It’s the opposite of life insurance: instead of paying premiums to protect against dying too soon, you pay a premium to protect against living “too long” and running out of money.

- The Lump Sum Premium:

You give a single, lump-sum payment to a life insurance company. Yes, you read that right, an insurance company.

This could come from a 401(k) rollover, the sale of a home, or other savings. - The Contract is Signed:

You and the insurance agent/insurer sign a contract that specifies the payout terms. I cannot stress this enough, please read the contract carefully!! I was amazed what types of terrible annuity contracts I have seen people sign. And the insurance agent did not explain any of it to them. - Income Begins:

The insurance company starts sending you regular, guaranteed checks, typically within a month to a year.

It’s not exactly the same, but the analogy I would explain to clients was simple. When you maintain an investment account, that’s like a 401(k). When you trade it in and annuitize the contract, that is more like a pension with pre-defined income. - Payments Continue:

These payments continue for the duration you’ve chosen and outlined in the contract you signed. It is often for the rest of your life.

This is fundamentally different from a deferred annuity, where you contribute money over time and let it grow for years before turning on the income stream.

For a video slideshow summary of the article, feel free to press play below

How Much Income Can a Single Premium Immediate Annuity Provide? (Examples for 2026)

This is the most common question I get from clients. The payout depends on your age, gender, the amount of your premium, and the payout option you choose. As of late 2025, with a more normalized interest rate environment, the payouts are more attractive than they have been in recent years.

Note: These are estimates for illustrative purposes only. Payouts for women are typically lower due to longer life expectancies. You must get a direct quote from an insurer for an accurate figure.

How Are Immediate Annuity Payments Taxed?

If you purchase your annuity with after-tax money (from a savings or brokerage account), the Internal Revenue Service (IRS) allows you to receive a portion of each payment tax-free. This is governed by the exclusion ratio.

Key Considerations and Risks Before You Buy An Immediate Annuity

An immediate annuity is an irreversible decision. Here’s what I always made sure my clients understood.

Choosing Your Payout Option

- Life Only:

Provides the highest monthly payout but payments stop when the annuitant (the person receiving payments) dies. - Life with Period Certain:

Guarantees payments for a specific period (e.g., 10 years), even if you die sooner. If you outlive the period, payments continue for life. The payout is slightly lower. - Joint and Survivor:

Payments continue as long as either you or your spouse is alive. This is crucial for married couples but provides the lowest initial monthly payout. - Life with Cash Refund: I

f you die before receiving payments equal to your original premium, your beneficiary receives the difference.

The Biggest Risk: Inflation

A fixed payment of $1,500 per month feels great today, but its purchasing power will be significantly eroded by inflation in 10 or 20 years. Some immediate annuities offer inflation adjustment options (COLAs), but they come at the cost of a much lower starting payout.

The Financial Strength of the Insurance Company

Your “guaranteed” income is only as good as the company that issues it. Before you buy, it is essential to check the insurer’s financial strength rating from an agency like A.M. Best or S&P. I never recommended a company with a rating lower than “A.”

Now, try searching for: annuity riders, what are deferred annuities, or retirement withdrawal strategies.

Final Verdict: My Golden Rule for Immediate Annuities

After nearly 30 years of advising clients, my golden rule is this:

Solve for needs, not for greed. An immediate annuity is not an “investment” to make you rich; it’s an insurance product to ensure you never become poor. Use it surgically to create a floor of guaranteed income to cover your essential, non-negotiable expenses (like housing, food, and healthcare).

Let your other, more liquid assets in your retirement plan handle growth and fight inflation. That balanced approach is the key to a truly secure and peaceful retirement.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.