Greetings, readers! My name is Michael Ryan, and after over 25 years as a financial planner, I’ve seen firsthand how confusing topics like annuities can be. But I’m here to tell you – having a solid grasp on annuities and related concepts can transform your retirement planning for the better.

In this article, my goal is to arm you with the knowledge and tools, like the present value of an annuity calculator, to take control of your financial future. Together, we’ll understand terms like “present value” explore why these calculations matter for your investment strategies, and set you up for success when evaluating annuities.

Ready to unlock the power within these present value formulas? Let’s get started!

Key Takeaways About Projecting Present Value of Annuities & Investments

- The Present Value of Annuity Calculator is a pivotal tool for retirement planning, enabling you to ascertain the current worth of a series of future annuity payments. By inputting variables such as payment amount, interest rate, and payment duration, you can determine how much you need to invest today to secure a desired future income stream.

- Looking into interest rates and payment periods, understanding how these factors influence the present value of an annuity table can significantly impact your investment strategy. The interest rate serves as a critical determinant, where higher rates elevate the premium, thereby affecting the annuity premium and ultimately the annuity payment.

- Exploring Annuity Contracts and Annuity Premiums unveils the contractual essence of annuities, highlighting the commitment between you and the insurer. This relationship dictates the premium’s size, which is contingent on various elements, including the interest rate and the payment period.

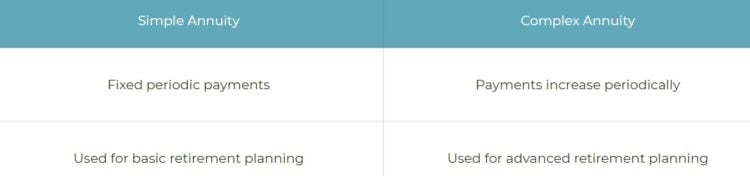

- Distinguishing between Simple and Complex Annuities offers a nuanced understanding of annuity payments. A Simple Annuity promises consistent payments at regular intervals, whereas a Complex Annuity introduces variability in payment amounts, adding a layer of complexity to your financial planning.

Present Value of Annuity Calculator With Steps

How do you calculate the present value of an annuity? Use the below present value annuity calculator – it is a tool that can be used to calculate the present value of an annuity.

The present value calculator takes into account the factors that affect the present value, such as the interest rate, the number of payments, and the amount of each payment.

The present value annuity calculator can be a useful tool for retirement planning. It can help you determine how much money you need to invest today in order to receive a stream of payments over a period of time.

In simpler terms, the present value calculator will answer your question:

- How much money do I need to put aside today to create an income stream of $x?

- If I put $x into an annuity today – how much income will I receive each month?

- Calculate lump sum present value of your annuity payments

The annuity payment calculator can be used to calculate the present value of an annuity.

Annuity Calculator of Present Value PV

Unlike other sites, I won’t make you keep scrolling to find the present value calculator. or just provide you the tool with no further explanation following it.

Here’s the calculator:

Present Value of Annuity Calculator

Estimate what a fixed series of future payments is worth today using your selected discount rate and payment timing.

Present Value Results

Formula used

Calculation steps

How to interpret the result

How to Use the Present Value of Annuity Calculator:

Follow these simple steps to find the present value of your annuity:

- Enter Payment Amount: Input the consistent amount you will pay or receive each period (PMT).

- Enter Annual Interest Rate: Provide the nominal annual interest rate (APR) used for discounting.

- Enter Annuity Term: Specify how long the payments last by entering the number of Years and/or Months.

- Select Payment Frequency: Choose how often payments occur (e.g., Monthly, Annually). By default, the calculator assumes interest compounds at this same frequency.

- (Optional) Adjust Compounding: If interest compounds differently than payments, click “Show Advanced Frequency” and select the correct Compounding Frequency.

- Select Annuity Type: Choose “Ordinary Annuity” if payments are made at the end of each period, or “Annuity Due” if payments are made at the beginning.

- Calculate: Click the button to see the Present Value (PVA)!

The calculator will display the PVA, along with the intermediate values (periodic rate i, total periods n), the formula used, and a step-by-step breakdown of the calculation for full transparency.

The calculator will then output the present value of the annuity.

- You can let the present value of annuity calculator do the calculation for any of the above steps

- You can also expand the fields by using the calculators “advanced mode” too

- A key differentiator is this tool can also act as an ordinary annuity calculator

The calculator can be used to find the PVOA for a variety of investment types, including:

- Bonds

- Stocks

- Mutual funds

- Certificates of deposit

Be sure to read further to understand:

- what is the annuity value calculator

- how to use a NPV annuity calculator

- why it is important to use an online annuity calculator

- real life examples of the calculations and how they help you make investment decisions

- as well as what it all means for you!

If you are wondering what the value of an investment is calculated to be down the road – use our Future Value Calculator in this article.

Annuity and Financial Planning Basics

When clients first started asking me about annuities years ago, I realized few resources existed to simply explain key concepts for newcomers. So before we dive into the present value calculator itself, let’s ensure we’re all on the same page regarding some fundamental terminology and framework. Consider this your annuity crash course!

In plain English, an annuity at its core is simply a series of payments made to a recipient over a defined period of time. For many folks planning for retirement, annuities can provide reliable income year after year from a single upfront investment.

But how do we evaluate if a particular annuity is worthwhile? Or forecast how much we’ll ultimately receive over 20+ years? That’s where our friend “present value” comes in – and why finding a quality present value of annuity calculator is so vital.

- Learn about pros and cons of variable annuities, as well as pros and cons of fixed annuity here

When you’re ready, let’s move on to discussing exactly what present value means and how these special calculators work their magic!

| Term | Definition |

|---|---|

| Annuity | A series of payments made at regular intervals, used for retirement planning or other purposes. |

| Annuity Contract | A contract between an individual and an insurance company to make regular payments in exchange for a premium. |

| Annuity Premium | The lump sum of money paid upfront to the insurance company to initiate the annuity contract. |

| Interest Rate | A factor that determines the size of the annuity premium; higher rates result in higher premiums. |

| Annuity Payment | The amount received by the annuitant at each payment interval. |

| Simple Annuity | An annuity where payments are made at regular intervals and the same amount is paid each time. |

| Complex Annuity | An annuity where payments are made at regular intervals, but the amount of each payment may vary. |

| Retirement Annuity | A common type of complex annuity used to provide income during retirement. |

| Fixed Annuity | An annuity that pays a set amount each time, offering predictability in payments. |

| Variable Annuity | An annuity where payments can vary based on the performance of underlying investments. |

Understanding Present Value

Alright, let’s dive into the heart of the matter – what is this “present value” concept that holds the key to unlocking effective use of annuities?

In simple terms, the present value of any future payment stream allows us to estimate what that series of payments is really worth to us today. Since the same $1,000 payment 30 years from now is not nearly as valuable as $1,000 in hand this year, present value calculations account for this “time value” of money.

The inputs that affect the present value outcome include:

- The total payments (cash flows) you expect to receive

- The timing of those payment installments

- An assumed rate of interest or expected investment returns

So in evaluating an annuity that promises, let’s say, $20,000 per year for the next 25 years, the present value calculation will estimate the lump sum we would need to have in hand today to equate to receiving those future payments. This allows apples-to-apples comparisons of various options.

And that brings us to our magical tool…ready to bring out the present value annuity calculators?

Present Value Annuity Calculators to the Rescue

In my early days as an advisor, I remember clients struggling to wrap their heads around present value concepts that I took for granted. So I made it my mission to find practical tools, beyond complex formulas, to demystify these crucial calculations.

Enter online present value annuity calculators – easy-to-use resources that allow anyone to input their particular situation and derive the outcomes they need within seconds. Clients’ eyes lit up when seeing the translation of future payments to today’s dollars happen right before them!

While many quality calculators exist, I recommend the one above that balances accuracy, usability, transparency, and functional flexibility:

In the next section, we’ll walk step-by-step through how to use these calculator tools to shed new light on your own annuities or retirement planning scenarios.

So if you’re still with me…congratulations! You now know more about annuities and present value techniques than 95% of the population. Let’s keep going and start putting our knowledge into practice!

Using Present Value Annuity Calculators – Real Client Examples

Now that you’re armed with background knowledge and have access to the right calculation tools, let’s get hands-on practice applying these concepts to real-life scenarios.

Walk with me through a step-by-step illustration of using a present value annuity calculator to evaluate a hypothetical retirement income option. We’ll use one of my favorite tools above, but feel free to follow along with any of the recommended calculators from the previous section.

PV Annuity Calculator & Calculation

The present value of an annuity (PVA) is the sum of all future payments from an annuity, discounted back to the present day. The discount rate is the interest rate used to determine how much future payments are worth today.

Here’s the situation in Example 1: Deciding Whether To Buy a Fixed Annuity

Richard, a 55-year-old client, is considering purchasing an immediate annuity that promises $15,000 of annual income, starting in 10 years at age 65, guaranteed for his lifetime. The annuity issuer quotes the upfront cost at $100,000. Should Richard accept this offer?

First, we enter the known data points into the calculator:

- Annual payment amount: $15,000

- Years until the first payment: 10

- Length of payments: Lifetime (let’s assume 25 more years)

- Discount rate: We’ll use 4% estimated investing returns

After clicking “Calculate,” the calculator churns through the present value formula and displays the result: $138,355

This means that based on the contracted payment schedule, an upfront investment of $138,355 today would equate to receiving $15,000 per year for the next 25 years. Comparing to the $100,000 actual cost, this appears to be solid value for Richard!

Now you have direct experience going through the motions of assessing annuities with present value data. Let’s build on this example with some additional scenarios for you to practice evaluating…

Example 2: Deciding Whether to Invest ina Deferred Fixed Annuity

Susan, a 45-year-old client, is evaluating purchasing a deferred fixed annuity that will start paying $10,000 per year at age 65 for the rest of her life. The annuity issuer offers this for a one-time premium of $100,000. Susan wants to estimate the potential present value she would gain from this stream of future payments.

We input the following into our present value annuity calculator:

- Annual payment amount: $10,000

- Years until first payment: 20 years (when Susan turns 65)

- Length of payments: Lifetime (let’s assume 25 more years)

- Discount rate: 5% expected returns

The calculator estimates the present value of this annuity to be $138,200 – meaning based on the proposed terms from the issuer, Susan would effectively gain over $38,000 in present value versus her upfront investment if she lives to projected life expectancy.

Example 3: Calculating If a Variable Annuity Makes Sense or Not

John, a 50-year-old, is exploring a variable annuity offering indexed returns to a stock market fund. The initial investment would be $50,000, which would then pay out annual gains based on the fund’s performance for the next 30 years. The company shows backtested historical averages of 5% annual returns over extended periods.

John inputs the following estimates into the present value calculator:

- Initial investment: $50,000

- Annual payments: Variable based on 5% yearly fund gains

- Length of payments: 30 years

- Discount rate: 3%

The tool estimates a present value of $55,500. Since the upfront premium cost is $50,000, the over $5,500 in excess present value suggests this could be a favorable long-term investment if the projected growth rates prove reasonably accurate going forward.

I hope these real illustrations help cement your comfort applying these vital concepts. Never again will discussions of present values or annuities need to intimidate you!

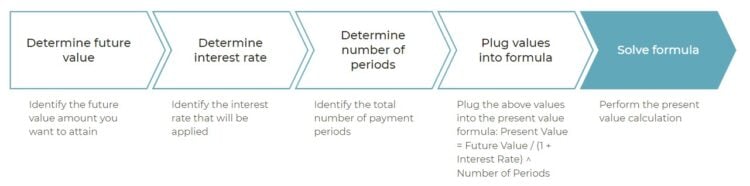

Formula For Calculating Present Value of Annuity

To calculate the present value of an annuity, the present value of an annuity formula is:

PV = PMT * ((1 – (1 / (1 + i)^n)) / i)

Where:

- PV = present value

- PMT = payment amount

- i = interest rate

- n = number of payments

Present value of annuity example:

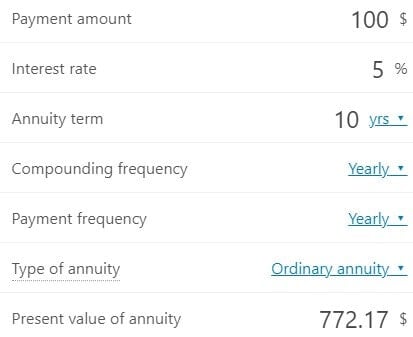

For example, let’s say that you will receive $100 per month for the next 10 years. The interest rate is 5%. How would you find the present value of your annuity?

The formula for calculating the present value of an annuity is PV = A * ((1 – (1 / (1 + r)^n)) / r), where A is the annual payment, r is the interest rate, and n is the number of years. In this case, A = $100, r = 0.05, and n = 10.

When you plug those values into the formula, you get PV = $100 * ((1 – (1 / (1 + 0.05)^10)) / 0.05) = $772.17.

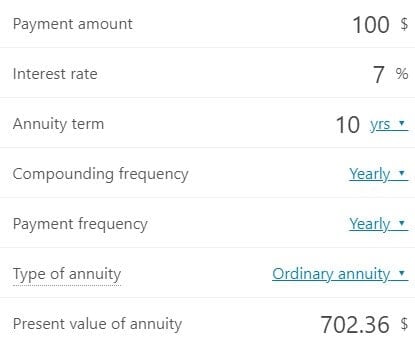

This calculation assumes that you could earn a 5% interest rate on your investments. If the interest rate you could earn was lower, the present value of the annuity would be higher. The higher the interest rate, the lower the present value of the annuity, since the interest rate is used to discount future payments.

- For example, if you could only earn a 3% interest rate, the present value would be $853.02.

- And if you could earn a 7% interest rate, the present value would be $702.36.

- How much does a $10,0000 annuity pay per month? As you see above, it depends on the interest rate that you expect to earn!

- An alternative to using the above present value annuity calculator is to use the present value of annuity

Present Value for Advanced Financial Planning

By this point in our journey, you’re likely feeling empowered by your expanded comprehension of annuities, present value techniques, and how to leverage handy calculation tools. Now let’s build on that foundation to see how these concepts can optimize major financial planning decisions.

Armed with the power to translate future cash flows into today’s dollars, you can completely change how you evaluate investments, retirement options like pensions, and even major purchase choices. Ask yourself:

“What lump sum would I need to have on hand today to equate to this future income stream?”

This mental shift uncovers hidden values, risks, and opportunities you likely glazed over previously.

As an example, let’s return to our friend Richard from the last section deciding whether to invest $100,000 into a retirement annuity. If we project Richard living to 90 and used a present value calculator for his full lifetime. The annual $15,000 payments might actually equate to a $350,000 lump sum value instead of the shorter 25 year horizon we initially analyzed.

Running through these expanded timeframe calculations allows Richard to make an apples-to-apples comparison of invest that $100k in other markets to aim for average 5% returns for life. The lifetime present value analysis provides key insights compared to a narrow focus only on the guaranteed 25 year period.

The applications of present value and annuity calculations in advanced financial planning are nearly endless, but I hope this illustration spurs your thinking on how to view your assets with a new lens.

In our final section, we’ll tackle the last major piece of the puzzle – estimating future values rather than only present outcomes. Get your calculators fired up once more as we continue building out your financial analysis toolkit!

Present Value Annuity Table

The following table shows the present value of an annuity of $1,000 per year for 10 years, discounted at a variety of interest rates.

Simple present value annuity table

| Interest Rate (%) | Present Value of Annuity |

| 0.5 % | $10,000 |

| 1.0 % | $9,091 |

| 1.5 % | $8,264 |

| 2.0 % | $7,517 |

| 2.5 % | $6,841 |

| 3.0 % | $6,225 |

| 3.5 % | $5,661 |

| 4.0 % | $5,142 |

| 4.5 % | $4,665 |

The higher the interest rate, the lower the present value of the annuity

As can be seen from the PVOA annuity table, the present value of an annuity decreases as the interest rate increases. This is because the higher the interest rate, the higher the discount rate, and the lower the present value of the annuity.

Full Present Value annuity table

| n | 1% | 2% | 3% | 4% | 5% | 6% | 8% | 10% | 12% |

| 1 | 0.990 | 0.980 | 0.971 | 0.962 | 0.952 | 0.943 | 0.926 | 0.909 | 0.893 |

| 2 | 1.970 | 1.942 | 1.913 | 1.886 | 1.859 | 1.833 | 1.783 | 1.736 | 1.690 |

| 3 | 2.941 | 2.884 | 2.829 | 2.775 | 2.723 | 2.673 | 2.577 | 2.487 | 2.402 |

| 4 | 3.902 | 3.808 | 3.717 | 3.630 | 3.546 | 3.465 | 3.312 | 3.170 | 3.037 |

| 5 | 4.853 | 4.713 | 4.580 | 4.452 | 4.329 | 4.212 | 3.993 | 3.791 | 3.605 |

| 6 | 5.795 | 5.601 | 5.417 | 5.242 | 5.076 | 4.917 | 4.623 | 4.355 | 4.111 |

| 7 | 6.728 | 6.472 | 6.230 | 6.002 | 5.786 | 5.582 | 5.206 | 4.868 | 4.564 |

| 8 | 7.652 | 7.325 | 7.020 | 6.733 | 6.463 | 6.210 | 5.747 | 5.335 | 4.968 |

| 9 | 8.566 | 8.162 | 7.786 | 7.435 | 7.108 | 6.802 | 6.247 | 5.759 | 5.328 |

| 10 | 9.471 | 8.983 | 8.530 | 8.111 | 7.722 | 7.360 | 6.710 | 6.145 | 5.650 |

| 11 | 10.368 | 9.787 | 9.253 | 8.760 | 8.306 | 7.887 | 7.139 | 6.495 | 5.938 |

| 12 | 11.255 | 10.575 | 9.954 | 9.385 | 8.863 | 8.384 | 7.536 | 6.814 | 6.194 |

| 13 | 12.134 | 11.348 | 10.635 | 9.986 | 9.394 | 8.853 | 7.904 | 7.103 | 6.424 |

| 14 | 13.004 | 12.106 | 11.296 | 10.563 | 9.899 | 9.295 | 8.244 | 7.367 | 6.628 |

| 15 | 13.865 | 12.849 | 11.938 | 11.118 | 10.380 | 9.712 | 8.559 | 7.606 | 6.811 |

| 16 | 14.718 | 13.578 | 12.561 | 11.652 | 10.838 | 10.106 | 8.851 | 7.824 | 6.974 |

| 17 | 15.562 | 14.292 | 13.166 | 12.166 | 11.274 | 10.477 | 9.122 | 8.022 | 7.120 |

| 18 | 16.398 | 14.992 | 13.754 | 12.659 | 11.690 | 10.828 | 9.372 | 8.201 | 7.250 |

| 19 | 17.226 | 15.678 | 14.324 | 13.134 | 12.085 | 11.158 | 9.604 | 8.365 | 7.366 |

| 20 | 18.046 | 16.351 | 14.877 | 13.590 | 12.462 | 11.470 | 9.818 | 8.514 | 7.469 |

| 21 | 18.857 | 17.011 | 15.415 | 14.029 | 12.821 | 11.764 | 10.017 | 8.649 | 7.562 |

| 22 | 19.660 | 17.658 | 15.937 | 14.451 | 13.163 | 12.042 | 10.201 | 8.772 | 7.645 |

| 23 | 20.456 | 18.292 | 16.444 | 14.857 | 13.489 | 12.303 | 10.371 | 8.883 | 7.718 |

| 24 | 21.243 | 18.914 | 16.936 | 15.247 | 13.799 | 12.550 | 10.529 | 8.985 | 7.784 |

| 25 | 22.023 | 19.523 | 17.413 | 15.622 | 14.094 | 12.783 | 10.675 | 9.077 | 7.843 |

| 26 | 22.795 | 20.121 | 17.877 | 15.983 | 14.375 | 13.003 | 10.810 | 9.161 | 7.896 |

| 27 | 23.560 | 20.707 | 18.327 | 16.330 | 14.643 | 13.211 | 10.935 | 9.237 | 7.943 |

| 28 | 24.316 | 21.281 | 18.764 | 16.663 | 14.898 | 13.406 | 11.051 | 9.307 | 7.984 |

| 29 | 25.066 | 21.844 | 19.188 | 16.984 | 15.141 | 13.591 | 11.158 | 9.370 | 8.022 |

| 30 | 25.808 | 22.396 | 19.600 | 17.292 | 15.372 | 13.765 | 11.258 | 9.427 | 8.055 |

Estimating Future Value

We’ve covered a lot of ground when it comes to analyzing present value for annuities and financial planning. Now, let’s shift gears to discuss the flipside concept – future value.

While estimating the current worth of future payments can guide immediate decisions, projecting how much a lump sum could grow to over time is equally important. Do you want to take a guess how large today’s $10,000 investment might become in 30 years? How about $100,000?

This is where future value calculations come into play! The same inputs that shape present value formulas can be tweaked to instead forecast long-term growth:

- Present cash amount (lump sum investment)

- Assumed annual returns

- Time horizon

For example, let’s say Richard is deciding whether to invest $75,000 into mutual funds today. If we predict his portfolio averaging 7% annual returns over 20 years, here are the steps to determine the future projection:

- Enter initial lump sum: $75,000

- Input annual returns estimate: 7%

- Define time period: 20 years

Running this data through a future value calculator results in an estimated future balance of over $380,000! Now Richard can better weigh if that long-term payoff possibility aligns with his goals compared to utilizing that $75k elsewhere.

The takeaway for you is that present and future values are two sides of the same coin. Together they provide immense insight into financial decision points so you can plan and invest wisely.

Conclusion

Congratulations on expanding your skills to not only determine the current value of annuities but also to project the possibilities they may bring years down the road. With this knowledge in hand, you can approach your financial future with confidence!

I appreciate you joining me on this journey to unlocking the power within these annuity formulas. Please don’t hesitate to reach out with any other questions or scenarios you want to discuss further!

The present value of an annuity calculator is a tool that can be used to determine the PVOA. The calculator can be used to find the PVOA for a variety of annuity types, including:

- Ordinary annuities

- Future annuity payments

- Mathematical tables

- Accumulation tables

- Difference in figures

To use the calculator, simply enter the amount of money that you plan to invest, the interest rate that you expect to earn, and the number of years that you expect to invest for. The calculator will then provide an estimate of the future value of your investment.

While the Future Value of an Annuity Calculator can be a helpful tool, it is important to remember that it is only an estimate. The actual future value of your investment may be higher or lower than the amount estimated by the calculator.

When making any financial decision, it is important to consult with a financial advisor to get the most accurate and up-to-date information.

Feel free to share this calculator with friends, family or on social media. And don’t forget to look at the top of my website for the “Calculator” tab to see more fun interactive personal financial calculators to use, for free. Or browse through the site and enjoy a few articles. Lastly, sign up below for our free newsletter so that you don’t miss any of our future calculators as well.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.