Heard the same old “save more, spend less” advice until your eyes glaze over? Me too. Most financial blogs recycle generic tips that sound nice but rarely stick. It’s frustrating.

So, are you ready to learn to do it right? Learn how to save $10,000 in 6 months?

After nearly 30 years as a financial planner, watching countless clients try (and often fail) to reach big short term savings goals, I’ve seen exactly what works. It’s not magic, and it’s rarely about deprivation. It’s about having a specific, actionable plan.

Forget vague ideas. This is your step-by-step battle plan to potentially sock away $10k in just six months. Whether you need an emergency fund yesterday, want to crush debt, or save for a down payment, this roadmap is designed for action. Let’s get started.

Why Aim for $10,000 in 6 Months? It’s About Control.

Saving $10,000 quickly isn’t just about the money. It’s about proving to yourself you can take control of your finances. Imagine the peace of mind knowing you have a solid cushion.

Think what that $10k could do:

- Build a serious emergency fund. Handle unexpected bills without derailing your life.

- Aggressively pay down high-interest debt. Stop letting credit cards or loans eat your future income.

- Fund a major goal faster. Get closer to that down payment, car purchase, or big trip.

- Boost your financial confidence. Mastering this goal builds habits for lifelong wealth.

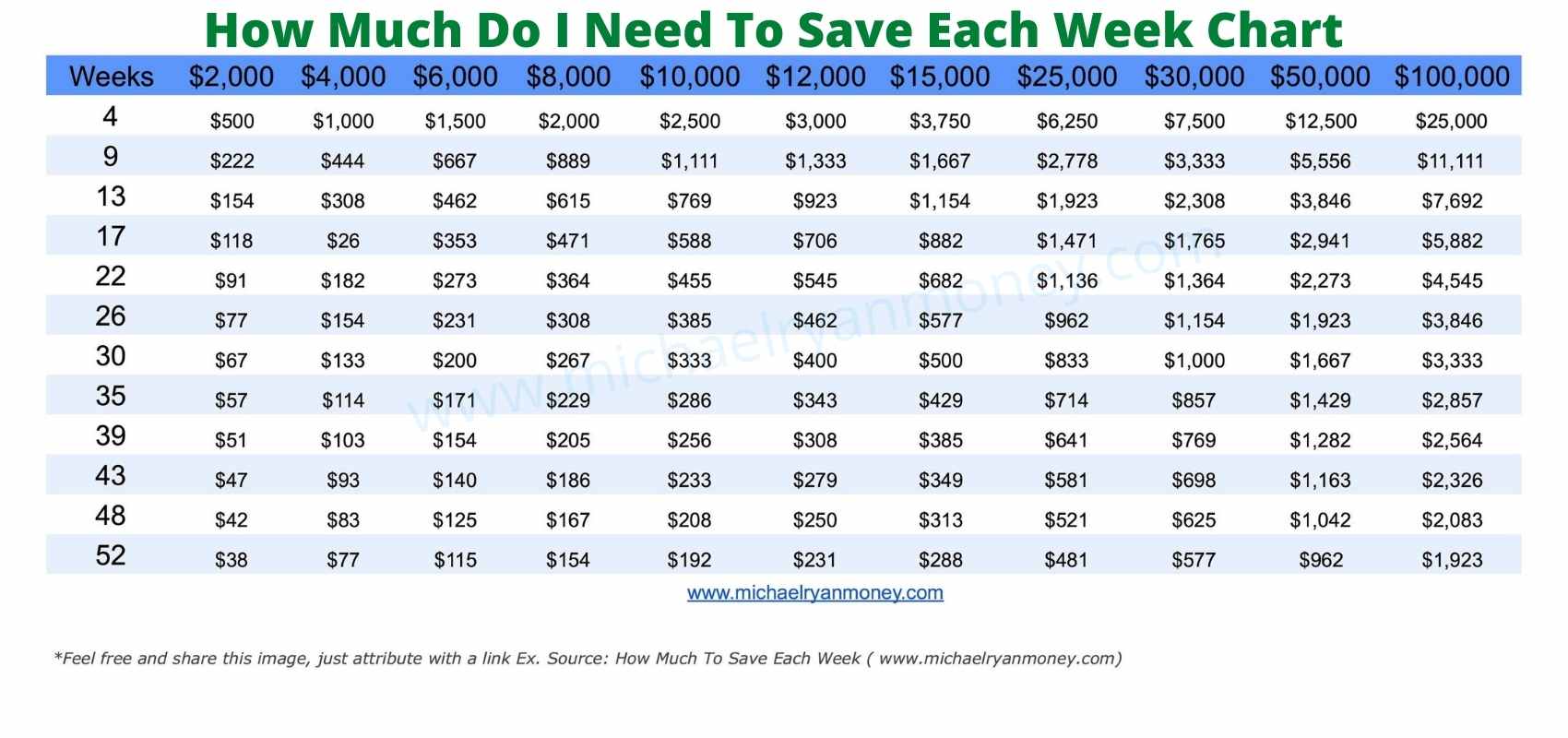

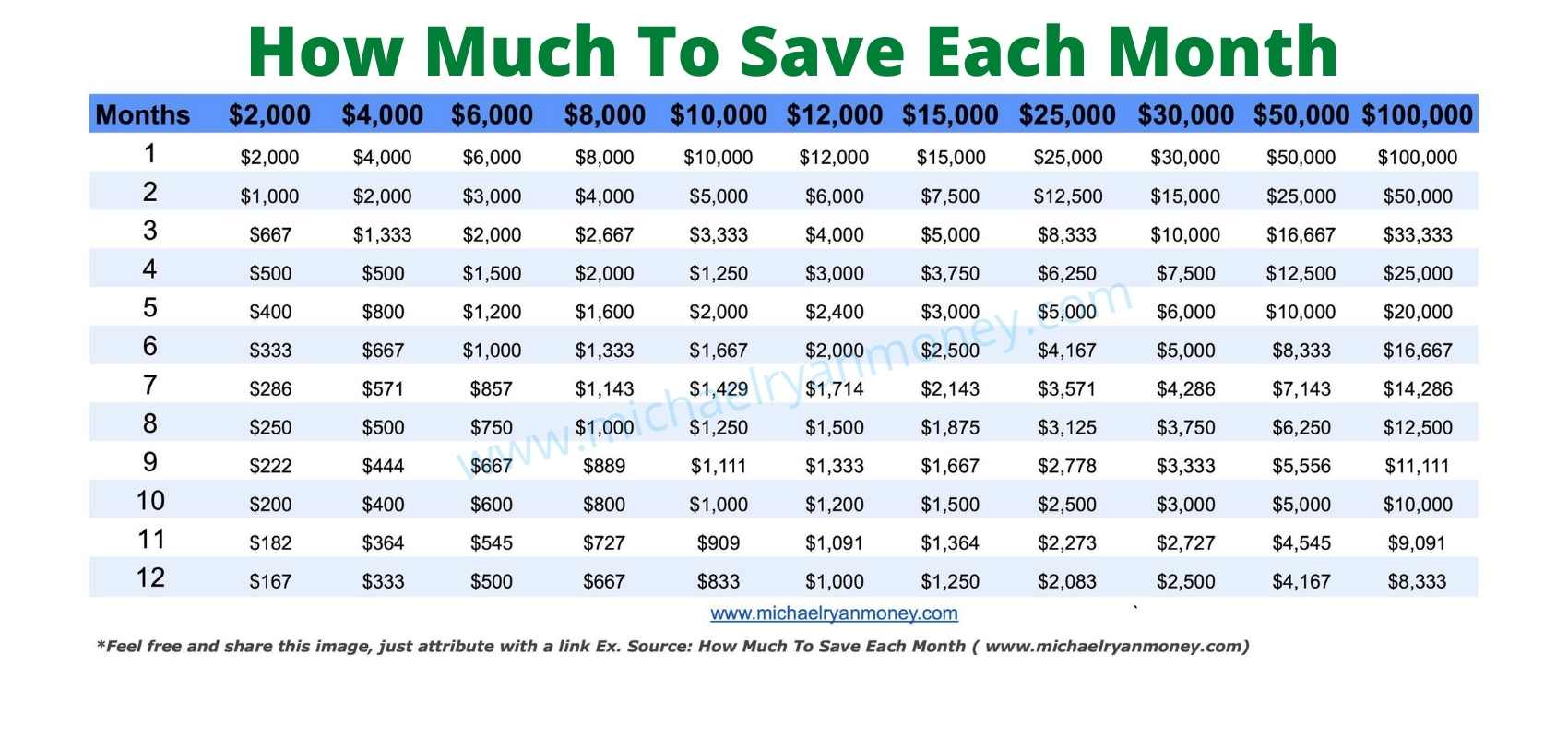

The Math Doesn’t Lie: Your Weekly & Monthly Target

Okay, let’s break it down simply. To save $10,000 in 6 months (which is 26 weeks), you need to put aside:

- $1,667 per month

- $385 per week

Does that number feel big? Maybe. But stick with me. We’ll break down how to find that money.

“Do not save what is left after spending, but spend what is left after saving.”

– Warren Buffett

How Long Will It Take? Use This Savings Calculator To Reach Your $10k Goal

Research consistently shows that developing strong savings habits leads to better financial outcomes. According to a Consumer Federation of America survey, fewer than two-fifths (38%) of American households report good or excellent progress in meeting their savings needs. With over one-quarter (27%) indicating no progress at all. This highlights both the challenge and importance of establishing effective saving practices. Are you ready to change that?

Savings Goal Calculator

Calculate the contribution needed, the time required, or the amount your savings plan could reach.

Savings Goal Results

Projected savings path

Annual savings schedule

| Year | Added during year | Growth during year | Ending balance |

|---|

Here are two ways to visualize hitting that weekly goal:

Challenge 1: Consistent Weekly Savings

In this challenge, you save $385 every single week for 26 weeks. Simple and steady.

Challenge 2: Variable Weekly Savings (Cycle)

This method varies the weekly amount, which some find easier to manage. After week 4, the cycle repeats.

Pick the approach that best suits your income flow.

Meet Priya: A Real-World $10k Success Story

Theory is nice, but real stories show what’s possible. Let me tell you about “Priya” (name changed, story is real).

- Background:

Priya was a 28-year-old graphic designer in Austin, Texas. She earned a decent $65,000 salary but felt constantly broke. Student loans and a love for dining out meant savings were minimal. Her goal: a $10,000 emergency fund in 6 months. - Challenge:

Finding an extra $1,667 per month seemed impossible. She tracked expenses “sometimes” using a notes app, but money just seemed to disappear. The goal felt overwhelming.

Click play below and watch the quick slideshow for more info on saving $10,000 in six months or less:

Our Strategy:

- Honest Tracking:

First, Priya tracked every penny for two weeks using the Mint app. No judging, just data. The results were eye-opening (hello, $600 on restaurants!). - Zero-Based Budget:

We implemented a zero-based budget. This means every dollar of her income got a job: $1,667 went to savings first, then essential bills, then debt minimums, then carefully allocated ‘fun money’. - Targeted Cuts:

We identified easy wins: canceling three unused subscriptions ($50/m), packing lunch 3 days/week ($150/month), and swapping two fancy dinners out for great home-cooked meals ($200/mo). Total found: $400/month. - Income Boost:

Priya used her design skills on Upwork for small freelance gigs, averaging an extra $800/month without burning out. - Automation:

Crucially, we set up an automatic weekly transfer of $385 from her main checking account to a separate Marcus by Goldman Sachs High-Yield Savings Account (HYSA). Out of sight, out of mind.

(An HYSA is just a savings account, usually online, that pays way more interest than typical brick-and-mortar bank accounts. Check sites like NerdWallet or Bankrate for current top rates).

Result:

Six months later, Priya had over $10,000 saved. More importantly, she built incredible financial discipline, learned budgeting skills, and even had a new income stream. Her confidence? Through the roof.

Priya’s story shows it’s not just about earning more; it’s about having a plan and executing it.

Your 5-Step Battle Plan to Save $10k Fast

Ready to build your own success story? Here’s the exact plan I use with clients:

Step 1: Know Your Numbers (The Brutal Truth)

- Action:

For one week, track every single dollar you spend. Use an app like YNAB (You Need A Budget), Empower Personal Cash™ (formerly Personal Capital), or even a simple notebook. Don’t judge yet, just track. - Why:

You can’t change what you don’t measure. This reveals where your money actually goes, not where you think it goes. - Financial Planner’s Tip:

This is often the most eye-opening step for clients. Be honest with yourself! Those small daily coffees or impulse buys add up faster than you think.

“A budget is telling your money where to go, instead of wondering where it went.”

– John C. Maxwell

Step 2: Build Your ‘Save First’ Budget

- Action:

Use the Zero-Based Budget method. List your monthly income. Subtract your savings goal ($1,667) first.

Then, allocate money for essential needs (rent/mortgage, utilities, groceries, transport, debt minimums).

Finally, assign any remaining money to wants (dining out, entertainment). Every dollar gets a job. - Why:

Paying yourself first guarantees savings progress. It shifts saving from an afterthought to a priority. Learn more about zero-based budgeting on Investopedia. - Michael Ryan Money Tip:

This might require tough choices initially. Be realistic. Your budget needs to be sustainable for 6 months.

The Federal Reserve’s Survey of Consumer Finances indicated that, the average balance of transaction accounts for American households was $8,000

Step 3: Make Smart Cuts (Not Painful Deprivation)

- Action:

Review your spending from Step 1. Focus on the “Big Three”:- Housing: Can you get a roommate temporarily? Any way to reduce utility usage?

- Transportation: Can you drive less, use public transport, carpool, or bike more? Shop around for car insurance (GEICO, Progressive often have online quotes)?

- Food: This is huge. Plan meals, cook more at home, pack lunches, buy generic brands. Aim to cut your food spending by 15-20%.

- Subscriptions/Memberships: Use a tool like Rocket Money or Trim to find and cancel unused subscriptions. Be ruthless!

- Why:

Small, consistent cuts across multiple categories add up significantly without making you feel totally deprived. - Planner Expert Tip:

Don’t try to cut everything you enjoy. Focus on the things you won’t miss much. Aim for finding300−300−500+ here.

Step 4: Boost Your Income (Find That Extra Cash)

- Action:

Aim to generate an extra $500 – $1,000+ per month for the next 6 months. - Ideas:

- Sell Stuff: Declutter your home and sell items on Facebook Marketplace, eBay, or Poshmark.

- Use Your Skills: Offer services on Fiverr or Upwork (writing, design, admin, tutoring).

- Gig Work: Drive for Uber/Lyft, deliver food with DoorDash or Instacart during peak hours.

- Odd Jobs: Offer pet-sitting, babysitting, handyman services, or lawn care in your neighborhood (post on Nextdoor).

- Ask for Overtime/Raise: If applicable at your main job, now’s the time to ask!

- Why:

Cutting expenses has a limit. Increasing income dramatically accelerates your savings goal. - Planner’s Tip:

Focus on the quickest path to cash for this short-term goal. Don’t try to build a complex business in 6 months. Choose something you can start this week.

Step 5: Automate & Optimize (Make it Easy)

- Action:

Set up an automatic transfer of $385 weekly or $1,667 monthly from your checking account to a separate High-Yield Savings Account (HYSA). Choose a bank separate from your main checking, like Ally Bank, Marcus by Goldman Sachs, or Discover Bank. - Why:

Automation removes willpower from the equation. Money you don’t see is less likely to be spent. An HYSA ensures your savings earn some interest while staying safe and accessible. - Michael Ryan‘s Tip:

This is non-negotiable. Automate it and pretend the money doesn’t exist.

This single step is often the difference between success and failure.

How to Save Money Fast?

From the Trenches: Michael Ryan Money Hard-Won Savings Secrets

After three decades, you see patterns. Saving $10k fast isn’t just math; it’s psychology. Here’s what truly works:

- Systems Beat Willpower:

Relying on willpower alone fails. The clients who succeed build systems: automated transfers, specific budgets (like Zero-Based), calendar reminders for check-ins. They make saving the default path.

Read this article to learn more about my tips on How To Create A Budget. - Find Your Powerful ‘Why’:

Saving “just because” isn’t motivating. Why do you want this $10,000? Visualize that debt-free feeling, the security of an emergency fund, or achieving that specific goal. Write it down. Look at it daily. - It’s Not Always About Income:

I’ve seen clients earning six figures struggle to save, while others on modest incomes hit goals like this consistently. Discipline and a plan matter more than paycheck size. Learn how you to can Set Financial Goals - Inflation Makes This Urgent:

In today’s environment, with costs rising (check the latest Consumer Price Index from BLS.gov), having a cash buffer is more critical than ever. Think of this $10k as your personal inflation shield.

Wondering where savings can grow long-term? Explore the Best Roth IRA Accounts.

Common Roadblocks (And How I Help Clients Smash Them)

Life happens. Even the best plans hit bumps. Here’s how to stay on track:

- Unexpected Expenses:

Car repair? Medical bill? It stings. First, use any existing emergency mini-fund if you have one. If not, you might need to temporarily pause the $10k goal contribution for a week or two to handle the emergency. Don’t derail completely. Adjust next month’s budget to catch up if possible, or extend your timeline slightly. The key is getting back on track ASAP. - Motivation Dip:

Around month 3 or 4, the initial excitement can fade. Want some motivation?

If you start investing $200 each month at 25, you’ll have around $698,000 by 65 (assuming an 8% annual return).

But if you wait until 35 to invest the same amount, you’ll only have $298,000 by 65.- Revisit Your ‘Why’:

Remind yourself why you started. - Track Progress Visually:

Use a savings tracker printable or app to see how far you’ve come. - Celebrate Mini-Milestones:

Hit $2,500? Treat yourself to something small (and budgeted!). - Find Accountability:

Tell a trusted friend or join an online finance community (like forums on Reddit‘s r/personalfinance) for support.

- Revisit Your ‘Why’:

🧠 Planning Tip: Setbacks are normal. Don’t beat yourself up. Acknowledge it, adjust, and refocus on the goal. Resilience is key.

Common Questions & Answers- Saving Different Amounts in 6 Months?

Maybe $10k feels like too much, or not enough? Here’s a quick guide:

How to save $6,000 in 6 months?

- Monthly: $1,000

- Weekly: $231

How to save $8,000 in 6 months?

- Monthly: $1,334

- Weekly: $308

How to save $15,000 in 6 months?

- Monthly: $2,500

- Weekly: $577

How to save $12,000 in 6 months?

- Monthly: $2,000

- Weekly: $462

How to save $20,000 in 6 months?

- Monthly: $3,334

- Weekly: $770

(Note: Weekly amounts are rounded slightly)

How To Save Half a Million Dollars

How To Save $1 Million Dollars

Need a different timeline?

- How to save $10,000 in 4 months? (Approx. 17 weeks)

- Monthly: $2,500

- Weekly: $588

- How to save $10,000 in 5 months? (Approx. 22 weeks)

- Monthly: $2,000

- Weekly: $455

- How to save $10,000 in 7 months? (Approx. 30 weeks)

- Monthly: $1,429

- Weekly: $334

The core principles (track, budget, cut, boost, automate) apply no matter the target amount or timeframe!

How to Save $10,000 in Just 3 Months

52 Week Money Challenge

Your Next Move: Make That $10k Happen

Saving $10,000 in six months is ambitious, but you absolutely can do it with focus and the right plan. We’ve covered:

- The Target: $1,667/month or $385/week.

- The Method: Zero-Based Budget + Smart Cuts + Income Boost.

- The System: Automate savings into a separate HYSA.

- The Mindset: Find your ‘why’ and build systems, not rely on willpower.

This journey requires dedication, but the payoff – financial control, reduced stress, and hitting a major goal – is immense. You build skills that last a lifetime.

So, what is the very first action you will take TODAY after reading this? Will you download a tracking app? Calculate your weekly target? Identify one expense to cut?

Share your commitment in the comments below! Let’s hold each other accountable.

Ready to dive deeper?

Want my personal budget template and more insider tips delivered straight to your inbox? Sign up for the Michael Ryan Money newsletter below. Let’s build your financial future, together.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.