Ready to take charge of your financial future but not sure where to start?

Are you a financial dreamer looking to take control of your money and overcome financial struggles? If so, setting short-term financial goals is the perfect way to start.

Here’s something powerful: breaking your big financial aspirations into smaller, actionable steps makes your objectives not only achievable but empowering.

Let’s dig into the world of short-term goals, their definitions, examples, and the strategies you can use to achieve them.

Short-term financial goals refer to those objectives that a person needs to achieve in less than three years. Such as tackling debt, setting a budget, reducing debt, starting an emergency fund, or saving for more immediate expenses, like a down payment on a home or a new car.

I’ll show you how I have helped thousands of people just like you to set achievable short-term financial goals. And put you on the path to reaching your dreams. I’ll show you how to figure out how much to spend on your pursuits. Provide examples of short-term financial goals that you can complete within a 3-5 year window.

Don’t let financial stress hold you back any longer. Start setting goals today and take control of your financial future!

Key Takeaways Ahead

What Are Short-Term Financial Goals?

To define short-term financial goals, these are financial milestones you plan to achieve within a few months to 1-3 years. Think of them as stepping stones on the path to larger financial aspirations like independent achievements retirement or owning a business.

Short-term goals differ from long-term objectives because they prioritize immediate needs and manageable wins, like paying off a credit card, saving for a vacation, or building an emergency fund.

Success in these areas lays the foundation for greater financial security down the line.

Common Short-Term Goals

Emergency Fund

Building an emergency fund covering 3-6 months of living expenses is a fundamental current financial objective. This fund provides financial security and helps avoid high-interest debt when unexpected expenses arise

Debt Management

Paying off credit card debt is crucial, especially considering the average credit card APR remains above 22% in late 2025.

Some other common short-term savings goals typically include:

- Vacation funds

- Wedding savings

- Car down payments

- Home renovation funds

Example of Goal Setting

Consider this practical example: To save $9,000 for an emergency fund within 12 months, you would need to set aside $750 monthly through automatic transfers from your paycheck

This systematic approach removes the temptation to spend and ensures steady progress toward your goal.

Why Are Short-Term Financial Goals Important?

Imagine standing at the base of a mountain. You can see the peak—your long-term dreams—but reaching it feels impossible. Shorter-term goals are like the steps carved into the rock, guiding you upward one achievable step at a time.

Did you know that 73% of Americans rank finances as a significant source of stress? Tackling small goals can reduce this anxiety, build confidence, and give you the momentum to address larger challenges.

The good news is you’re not alone. Many people find this difficult. And I am here, with nearly three decades of experience as a financial planner, to guide you on your path. Together, we can navigate the complexities of financial planning and empower you to make informed decisions. I also provide valuable financial literacy resources for female readers, tailored to address unique challenges and foster confidence in managing your finances. With the right tools and support, you can achieve your financial goals and secure your future.

Short-Term Impact:

• Credit utilization reduction

• Emergency preparedness

• Stress reduction

Long-Term Benefits:

• Improved borrowing rates

• Investment opportunities

• Wealth building foundation

Financial Goal Prioritization Strategy

High-Priority Goals:

✓ High-interest debt elimination (20%+ APR credit cards)

✓ Emergency fund establishment (3-6 months expenses)

✓ Employer 401(k) match capture (100% ROI)

Medium-Priority Goals:

✓ Short-term savings objectives (vacation, wedding)

✓ Credit score improvement

Low-Priority Goals:

✓ Luxury purchases

✓ Optional upgrades

Current Financial Challenges

According to the CFPB Americans faced significant challenges:

- 49% had to dip into savings

- 51% would run out of money within one month if they lost income

- 47% tend to spend more than they earn

Success Statistics

Recent data shows that 83% of people who set financial goals report feeling better about their finances after just one year. However, 72% of households still lack a written financial plan, highlighting the opportunity for improvement.

Ask Yourself:

- What’s one financial win you’d like to achieve this month?

- How would your stress levels change if you had an emergency fund covering three months of expenses?

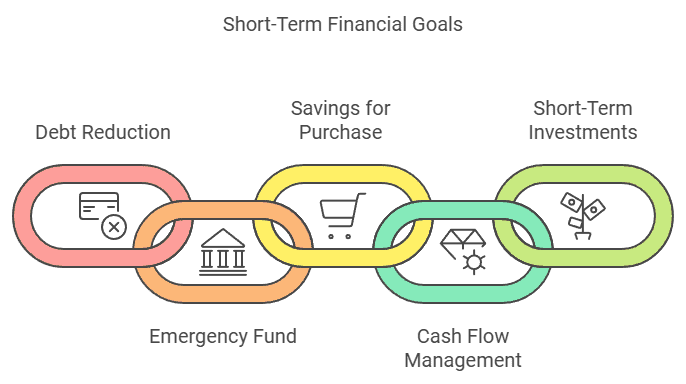

Examples of Shorter Term Financial Goals

Setting and achieving personal monetary objectives is an important part of successful financial planning. To reach a desired level of financial security, it’s essential to have short-term objectives that will help you get there.

For Individuals

- Debt Reduction: Pay off a high-interest credit card within six months. Use methods like the snowball (starting with smaller debts) or avalanche (prioritizing higher-interest debts) approaches.

- Emergency Fund Creation: Save $1,000 in three months for unexpected expenses like car repairs or medical bills.

- Savings for a Purchase: Set aside $2,000 for a new laptop or furniture upgrade.

For Businesses

- Cash Flow Management: Increase working capital by reducing unnecessary expenses over a quarter.

- Short-Term Investments: Allocate funds for a marketing campaign with a projected ROI within 90 days.

- Team Development: Budget for employee training programs to improve productivity within six months.

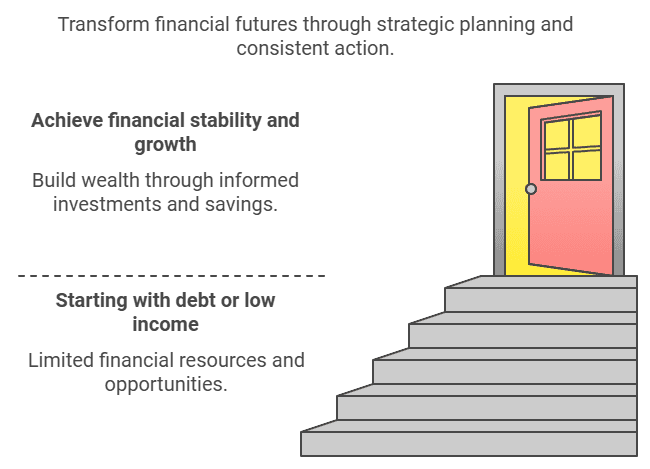

Success Stories That Show It’s Possible

These are stories readers and clients have shared with me

Zara’s Borrowing Breakthrough

After struggling with a 650 credit score, Zara Winters (32, graphic designer) committed to improving her borrowing rates. “I was paying 24% APR on everything,” she recalls. By systematically paying and keeping utilization under 30%, she boosted her score to 785 in 18 months. “Now I qualify for the best rates – my new car loan is just 3.9% APR.“

Kai’s Investment Journey

Kai Rodriguez (28, barista) started with just $25 weekly investments. “Everyone said you needed thousands to start investing,” he shares. Using micro-investing apps and gradually increasing his contributions, Kai built a $15,000 portfolio in a few years. “Small, consistent steps really do add up.”

River’s Side Hustle Success

River Thompson (26, retail worker) turned their weekend hobby into a wealth-building machine. “I started selling custom planners on Etsy during evenings,” they share. “First month: $50. Now? $2,000 monthly extra for investments. Anyone can start small and grow – you just need to begin.”

Key Takeaway: Whether you’re starting with debt, a low income, or minimal savings, these stories show that strategic planning and consistent action can transform your financial future. The common thread? They all started exactly where they were, with what they had.

Remember: Your story could be next! Start with one small step today.

How to Set and Achieve Your Immediate Financial Goals

- Get Crystal Clear on Your Priorities

Begin by asking yourself, What’s the most pressing issue I need to address? Write down your goals and rank them by urgency.

For instance:

* Emergency fund

* Debt repayment

* Saving for a holiday

Remember, the more specific your goals, the better. Instead of saying, “Save money,” try, “Save $500 in three months by cutting dining-out expenses.”

- 23 Money Savings Challenge To Try

- How To Save $10000 In 3 Months

- Develop a Short-Term Financial Plan

A strong financial plan ensures you stay on track. Here’s an example of a short-term financial plan:

| Goal | Time Frame | Action Steps | Resources Needed |

|---|---|---|---|

| Emergency Fund | 3 months | Save $200/month Cancel unused subscriptions | High-interest savings account |

| Pay Off Credit Card | 6 months | Pay $300/month Focus on highest interest debt | Debt snowball calculator |

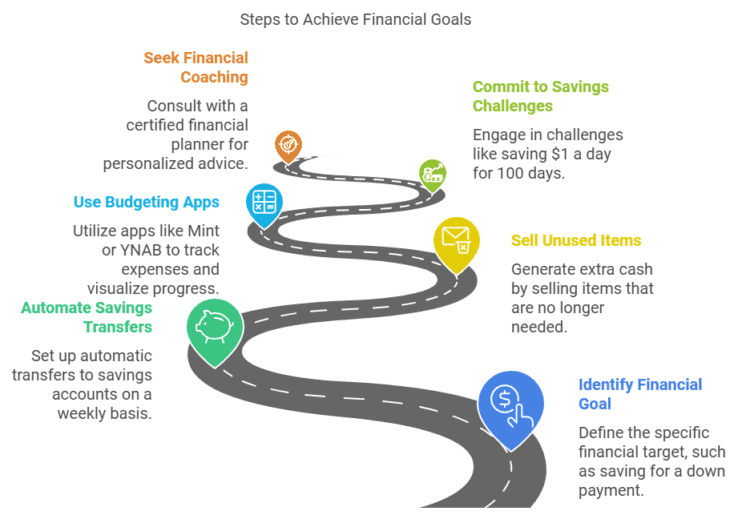

- Break Down Goals into Actionable Steps

If your goal is saving for a down payment, actionable steps might include:- Automating savings transfers weekly.

- Selling unused items for extra cash.

- Using a budgeting app to track spending.

- Utilize Smart Tools and Resources

- Budgeting Apps: Try apps like Mint or YNAB to track expenses and visualize progress. Read my reviews on The Most Popular Budgeting Apps for more.

- Savings Challenges: Commit to a money-saving challenge, such as saving $1 a day for 100 days.

- Financial Coaching: Seek advice from a certified financial planner for a personalized approach.

SMART Goal Framework

To effectively achieve short-term financial targets, implement the SMART framework:

| Component | Description |

|---|---|

| Specific | Define exact amounts and purposes |

| Measurable | Set concrete dollar amounts |

| Achievable | Align with financial capacity |

| Relevant | Match your priorities |

| Time-bound | Establish clear deadlines |

Saving and Setting Financial Goals

Recommended Savings Vehicles

| Account Type | Best For | Features |

|---|---|---|

| High-yield Savings | Most short-term goals | Earns interest, highly liquid |

| Money Market | Emergency funds | Higher interest rates than traditional savings |

| Certificate of Deposit | Fixed-term savings | Guaranteed returns |

| Brokerage Account | Growth potential | Higher risk, more flexibility |

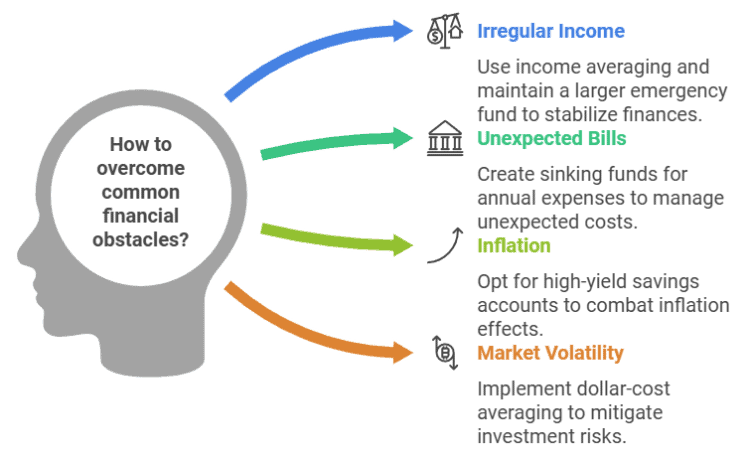

Challenges You Might Face

Even with the best intentions, life can throw curveballs. Here are common obstacles I have seen clients face. And how you can overcome them:

- Unexpected Expenses: Build flexibility into your plan by allocating 10% of your budget for “miscellaneous.”

- Loss of Motivation: This one is vital to your success. Celebrate small wins to stay engaged, like treating yourself to a favorite meal after reaching a mini-milestone.

- Economic Fluctuations: Adjust your strategy to align with changing circumstances, such as inflation or job changes.

Common Financial Obstacles & Solutions

Common Barriers:

• Instant gratification bias

• Loss aversion

• Analysis paralysis

Recommended reading: “Atomic Habits” by James Clear

Obstacle → Solution

• Irregular Income → Income averaging + larger emergency fund

• Unexpected Bills → Sinking funds for annual expenses

• Inflation (was 8.5% in 2022) → High-yield savings accounts (3-5% APY)

• Market Volatility → Dollar-cost averaging

• Lifestyle Creep → 50/30/20 budgeting rule

Balancing Short-Term and Long-Term Financial Goals

One thing that I taught every single one of my clients. Every day, you’re financially living three lives:

- Yesterday: You live the financial decisions you have made in the past.

- Today: Many people forget to live this life. Start enjoying today.

- Tomorrow: Save, save, save.

Saving for short and long-term goals

But. How do you strike a balance?

The key is integration. For example:

- If you’re saving for a home down payment (short-term), also contribute a small percentage to your 401(k) (long-term).

- Use debt repayment momentum to fuel longer-term investments in mutual funds or a Roth IRA.

- Don’t stop! When you pay off a debt, roll those payments into your next debt or future savings. it has a snowball affect!

Balancing Long-Term and Short-Term Financial Planning

Thought Experiment:

If you could fast-forward five years, what small financial habit today would make the biggest difference?

Measuring Success: Are You on Track?

Regularly evaluate your progress. Create checkpoints monthly or quarterly to ensure you’re aligned with your objectives. For instance:

- Did you save the planned amount last month?

- Are you making consistent debt repayments?

Quick Tip: Use visual tools like bar charts to track savings growth. Seeing progress can be incredibly motivating!

Financial Progress Tracking Methods

Daily:

• Expense logging

• Budget checking

Weekly:

• Account reconciliation

• Progress visualization

Monthly:

• Goal milestone review

• Budget adjustment

Quarterly:

• Major goal evaluation

• Strategy refinement

Psychological Techniques:

• Visual progress tracking (charts/graphs)

• Money journaling

• Accountability partnerships

• Reward milestones

Key Takeaways: Building Momentum with Short-Term Goals

Based on my experience of seeing what works, and what doesn’t. Here are my top tips:

- Start Small: Focus on manageable objectives, like saving $100 this month.

- Leverage Tools: Automate your savings or use a debt tracker.

- Adjust and Adapt: Stay flexible; financial plans often need tweaking.

- Celebrate Progress: Recognize your achievements, no matter how small.

Taking control of your finances begins with one action. Whether it’s downloading a budgeting app, scheduling a consultation with a financial advisor, or making your first debt repayment, each step moves you closer to financial freedom.

Final Aha Moment:

Your financial journey is uniquely yours. But the strategies to succeed—goal setting, discipline, and actionable planning—are universal. What’s the first short-term goal you’ll tackle today?

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.