Let’s be blunt: Most people are just not good at saving. They dream big, but their bank accounts tell a different story.

I’m Michael Ryan, and after 25 years as a financial planner, I’ve seen it all. The 52-week money challenge? It’s not magic, but it’s very effective – if you understand the real secret.

This isn’t just about saving $10,000; it’s about rewiring your brain, crushing limiting beliefs, and finally taking control of your financial future. Forget the fluffy advice; I’m here to give you the truth about saving, and how to make this challenge work for you.

Free 52 Week Savings Challenge Calculator

Want to save $10,000 (or any amount) in a year, but not sure where to start? Tired of generic 52-week money challenge templates that don’t fit your life? Forget one-size-fits-all plans.

I’ve created a tool that solves that problem. This interactive calculator lets you customize every aspect of your savings plan – starting amount, weekly increment, challenge type – and instantly visualize your progress. Discover the most effective way to reach your savings goals.

52-Week Savings Challenge Calculator

Create a weekly savings schedule that increases, decreases, or stays the same throughout the year.

Total saved after 52 weeks

$0

Based on the challenge settings you entered.

| Week | Date | Deposit | Running total |

|---|

This calculator provides an educational savings schedule based on the amounts entered. It does not account for interest, investment returns, taxes, fees, missed deposits, or individual financial circumstances, and it is not personalized financial advice.

What is the 52-Week Money Challenge to Save $10k? (The Real Deal)

Okay, let’s cut through the noise. The 52-week money challenge is basically a gamified savings plan. You start small, increase your savings each week, and aim for that $10,000 mark. Sounds simple, right?

It is, mechanically. But here’s what most articles won’t tell you: The real power of this challenge isn’t the math; it’s the psychology. It’s about tricking your brain into building a savings habit, one small step at a time.

And trust me, after seeing hundreds of clients try (and sometimes fail) at saving, I know the tricks that actually work.

The Basic Principle: Incremental Savings (It’s Not Rocket Science)

Imagine trying to run a marathon without any prior training. It’s daunting, right? The 52-week challenge is like a training plan for your savings.

You start by saving a predetermined amount in the first week and increase that amount by a set increment each subsequent week. This seemingly simple approach has a powerful psychological effect, making large savings goals feel surprisingly achievable.

How the Math Works: Reaching $10,000

The challenge of saving $10,000 in a year can feel overwhelming. Breaking it down into weekly increments solves this problem. How? By making it more manageable.

To reach $10,000, the challenge requires a starting deposit of $82.17 in the first week. Each week, you add $19.23 to the previous week’s deposit.

- Week 2 is $

101.93 ($82.17 + $19.23) - Week 3 is $

121.16($101.93 + $19.23), and so forth.

While the math is straightforward, adhering to the schedule consistently requires a strategic approach. Which we’ll cover in detail.

But here’s the “aha” moment: You’re not finding $10,000; you’re finding $82.17, then $101.93, then $121.16…

See the difference?

Helpful Reading:

Calculating Your Weekly Savings for a $10,000 Goal (The Roadmap)

To successfully complete the 52-week money challenge and reach your $10,000 goal, you need a precise savings schedule. I will provide you that table, but first you need to understand the importance of it.

Understanding this schedule is crucial for planning and tracking your progress. And so many other sites make it more confusing.

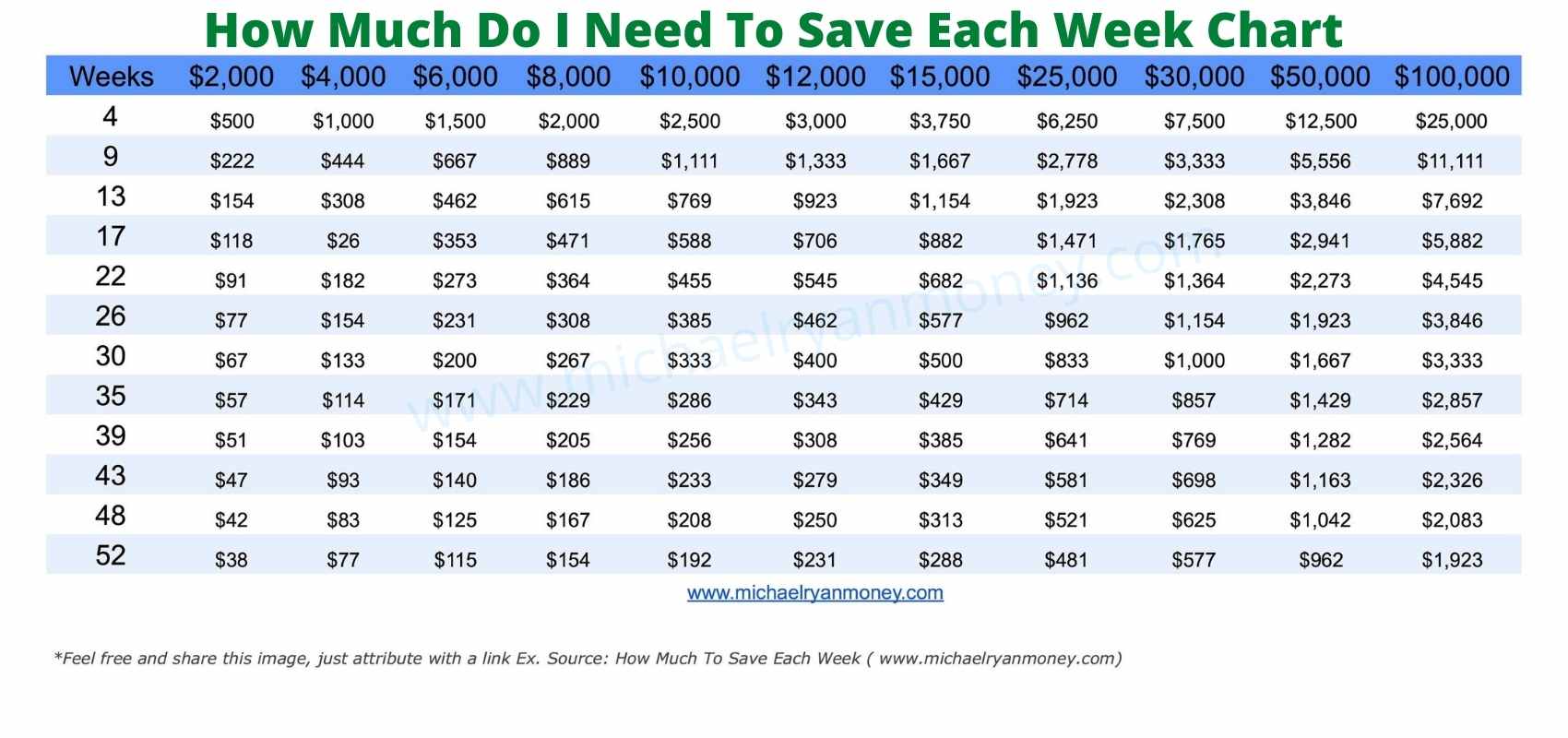

How Much Do I Need To Save Each Week Chart

Understanding the Weekly Increments (The Key to Consistency)

Insider Tip: As a retired financial planner, I’ve seen many people get tripped up by not fully understanding the incremental nature of the challenge. This section clarifies this for you.

The key to the $10,000 challenge for many, is the consistent weekly increase of $19.23. This amount is added to the previous week’s deposit, creating a steadily increasing savings curve.

While the increment is constant, your ability to adapt to unexpected expenses is vital for long-term success.

Another topic I’ll address later.

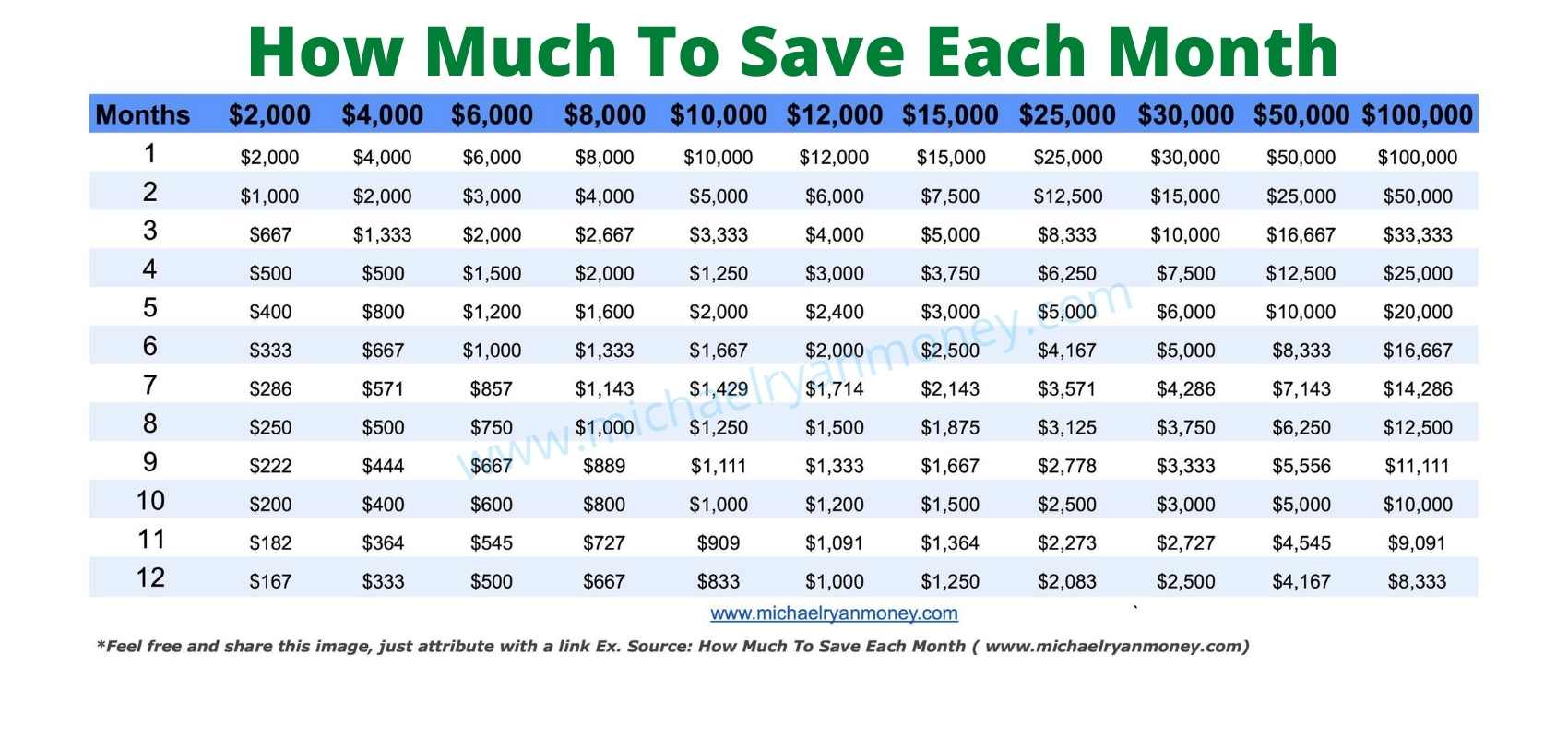

How Much Do I need To Save Each Month?

52-Week Money Challenge Variations: Find Your Perfect Fit For You

As a retired financial planner, I’ve seen firsthand how personal finance strategies need to be as unique as the individuals who use them. The standard 52-week money challenge is a popular tool for building savings, but it’s not a one-size-fits-all solution.

Different income patterns, psychological preferences, and financial goals mean that what works for one person might not work for another. I’ll show you various adaptations of the challenge, allowing you to tailor it to your specific needs.

Finding the right fit is crucial for maximizing your chances of success.

Reverse 52-Week Challenge: Conquer the Hardest Part First (The Psychology Hack)

Myth Debunked: Many believe starting small is always best. The reverse challenge proves that tackling the largest savings amounts first can be surprisingly effective for some.

The reverse 52-week challenge flips the script. You begin with the highest weekly deposit (corresponding to week 52 in the standard challenge) and decrease the amount each week.

This approach leverages a psychological principle known as “front-loading,” which can be particularly beneficial for certain personality types. You get that big win early, and it fuels your momentum.

Bi-Weekly & Monthly Options: For Irregular Income (The Real-World Solution)

If you’re a freelancer, contractor, or have a variable income, the standard weekly challenge might feel impossible. This variation is designed specifically for you.

The bi-weekly and monthly options adapt the challenge to match less frequent pay schedules. You simply calculate the total savings amount for the relevant period (two weeks or a month) and deposit that sum. This flexibility ensures that the challenge aligns with your cash flow, making it more sustainable and less stressful. No more feeling guilty for “missing” a week!

Custom Amount Challenge: Set Your Own Savings Target (The Power of Personalization)

Question to Ponder: What if $10,000 isn’t your goal? What if you’re aiming for $5,000, or even $20,000?

The custom amount challenge allows you to adjust the weekly increments and starting deposit to reach a different savings target. This is very flexible to what your goals are. This personalization ensures that the challenge is directly aligned with your specific financial objectives. You’re in control.

The “Mini-Challenges” Approach: Break It Down (The Overwhelm Buster)

Feeling overwhelmed by the thought of saving for an entire year? The mini-challenges approach addresses this common emotional hurdle.

The “mini-challenges” approach divides the 52 weeks into four 13-week segments. Each segment becomes a smaller, more manageable goal. This strategy leverages the power of short-term wins to maintain motivation and build momentum. It’s like running four sprints instead of a marathon.

The “Random Deposit” Approach (Spontaneous Savings!)

For those that find saving boring. Try making it random! Pick a random amount each week to save. This is a great way to change it up.

These variations offer flexibility and personalization. Allowing you to find the perfect fit for your financial journey. Whether you’re tackling the hardest part first, aligning with your income schedule, or setting your own targets, there’s a version of this challenge that can work for you.

Remember, the key to successful saving is consistency and finding a method that keeps you motivated.

WANT AN EASY WAY TO TRACK YOUR NET WORTH – SIGN UP FOR A FREE Empower ACCOUNT TODAY!!

Mastering the Mental Game: The Psychology of This Challenge

Let’s be real: Saving $10,000 (or any significant amount) isn’t just about the numbers. It’s about your mindset. The 52-week challenge, while simple in concept, can be a surprisingly powerful tool for rewiring your brain and building lasting financial habits – if you understand the psychology behind it.

Here’s the insider perspective I’ve gained from 25 years as a financial planner:

Know Your Savings Style (and Choose the Right Variation)

Hard Truth –> You might think you know how you save best, but your past failures might be telling a different story.

Are you energized by small, consistent wins? The standard challenge might be your best bet. Do you prefer to tackle the hardest part first? The reverse challenge could be your key to success. Do you have irregular income? The bi-weekly or monthly options are designed for you. Your past saving, success, or failures, can tell you a lot about the challenge that may work best for you.

Choosing the right variation for your personality is half the battle.

The Habit Loop: Making Saving Automatic (and Almost Effortless)

Insider Tip –> This is the secret weapon I used with countless clients: turning saving into an automatic habit, not a conscious decision.

The 52-week challenge is a perfect framework for building a habit loop. The cue is your payday (or a set day each week/month). The routine is the automatic transfer to your savings account. The reward isn’t just the final amount; it’s the feeling of accomplishment each time you see that balance grow (check it weekly!).

Once this loop is established, saving becomes almost effortless.

Visualization: Fueling Your Motivation (Beyond the Numbers)

Relatable Scenario –> Imagine a weightlifter. They don’t reach their goals through will alone, but they lift increasingly larger weights. Saving works the same way.

Don’t just focus on the $10,000. Visualize what you’ll do with that money. Imagine that debt paid off, that vacation booked, that emergency fund providing peace of mind. Picture yourself checking off each week on your tracker, getting closer and closer to your goal.

This mental imagery creates a powerful emotional connection, making you much more likely to stick with the challenge, even when things get tough.

Beyond the Challenge: Building a Foundation (a Glimpse into your future)

- After sticking to the money challenge, your options will open up, use your discretion on what you do next.

- Saving consistently builds more than just your bank account. It will help you build your financial confidence.

- Studies in behavioral economics show that consistent habits are far more effective than willpower alone when it comes to achieving long-

7 Proven Tips for 52-Week Money Challenge Success (From a Financial Planner – Me!)

Based on my years of experience helping clients achieve their financial goals, I’ve compiled seven proven tips to maximize your success with the 52-week money challenge. These aren’t just generic suggestions; they’re practical strategies grounded in real-world financial planning principles.

Implementing these tips will significantly increase your odds of reaching your $10,000 target and building lasting financial habits.

- Set Realistic Goals (No Delusions of Grandeur): Starting with unrealistic expectations is a common setup for failure. Carefully assess your income and expenses to ensure the challenge is achievable. Be honest with yourself. If $10,000 is too much, start smaller. A consistent win is better than an ambitious failure.

- Automate Your Savings: The Non-Negotiable: This isn’t a suggestion; it’s a requirement. If you’re serious about this challenge, automate your savings. Period. No excuses. Set up a recurring transfer from your checking to a separate, high-yield savings account (don’t even think about using your regular checking account). This does two things:

1) It removes the temptation to spend the money.

2) It puts your savings on autopilot.

I’ve seen this one simple step make the difference between success and failure countless times. Don’t skip it. - Track Your Progress (The Visual Reinforcement): Studies show that people who actively track their progress towards goals are significantly more likely to achieve them.

Use a spreadsheet, a budgeting app, or a printable tracker to monitor your weekly deposits and cumulative savings. This provides visual reinforcement of your progress, keeping you motivated and accountable. Seeing that number grow is powerful.

Studies show that people who actively track their progress towards goals are significantly more likely to achieve them. - Find an Accountability Partner (The Buddy System): Just like having a workout buddy can help you stay committed to an exercise routine, having a savings partner can boost your success with the 52-week challenge.

Find someone to go along with you on the savings challenge, and keep each other accountable. This is another tactic to utilize to help build up your discipline.

Misery loves company, and so does success! - Visualize Your Goal (The Mental Movie): What’s one of the most powerful (and often overlooked) tools for staying motivated? Visualization. Stay focused and remember the reason why you are doing the challenge.

Your motivation will continue to fuel your success. Keep a picture of your goal – that vacation, that house, that debt-free life – where you can see it every day. - Reward Yourself (The Carrot, Not the Stick): Before setting rewards, many people fall off track because they feel deprived. After implementing a system of small, strategic rewards, adherence rates soar.

Set small milestones along the way, and give yourself a reward. Small rewards. We’re building good habits, not blowing our budget. - Don’t Get Discouraged (The Resilience Factor): It’s inevitable that you’ll face setbacks or temptations along the way. Don’t let these derail your entire effort.

Remember, it’s a marathon, not a sprint. Do not get discouraged, it happens to most people.

Stay focused and motivated. Do not give up! One missed week doesn’t mean failure. Just get back on track. - Integrate with your overall Financial Plan: The 52-week money challenge is just one tool in your financial toolkit. Make sure your challenge saving is apart of your budget.

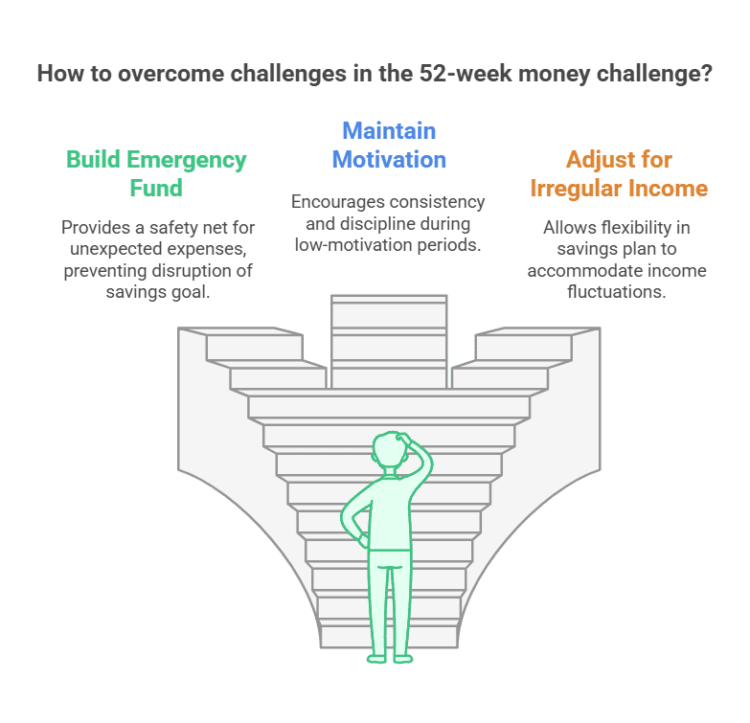

Overcoming Challenges: A Reality Check From a Financial Planner’s Perspective

Do You Have More Questions? (The FAQ Section – Because I Know You Do)

This section addresses some of the most common questions I’ve encountered about the 52-week money challenge, providing clear, concise answers.

- How do I start the 52-week money challenge?

Choose a variation (standard, reverse, etc.), set up a dedicated high-yield savings account, and make your first week’s deposit. Download a tracker to monitor your progress. - What if I can’t afford to save the required amount one week?

Don’t give up! You can catch up the following week, adjust the plan slightly, or switch to a more flexible variation (like the bi-weekly or custom amount challenge). - Where should I keep the money I’m saving?

A high-yield savings account (HYSA) is generally recommended, as it offers a higher interest rate than traditional savings accounts, allowing your money to grow faster. Don’t just let it sit in your checking account! - Can I use a budgeting app to help me?

Absolutely! Budgeting apps like YNAB (You Need a Budget), Mint, or Personal Capital can help you track your income, expenses, and savings progress, making it easier to stay on track with the challenge. - What is the standard 52 week challenge amount?

1$ the first week and increasing a dollar per week results in a saving of $1,378. - How can I use the 52-week challenge to build better financial habits?

Focus on consistency, track your progress, celebrate milestones, and integrate the challenge into your overall financial plan. The challenge is a tool for building discipline and a positive relationship with money. It’s a starting point, not a destination.

So, Are You Ready To Take on the $10,000 Savings Challenge? (The Call to Action – No More Excuses)

The 52-week money challenge is a powerful tool for achieving a significant savings goal, but it’s more than just a numbers game. It’s an opportunity to cultivate lasting financial habits, improve your money mindset, and build a more secure future.

By understanding the principles, adapting the challenge to your needs, and leveraging the strategies outlined in this guide, you can transform your financial life, one week at a time. Remember, consistency and a proactive approach are your greatest allies. Start your challenge today, and take control of your financial journey! I’ve seen it work for countless clients, and I know it can work for you. Now, go make it happen.

No more excuses. Download the tracker, set up that automatic transfer, and let’s do this!

52 week Money Challenge pdf template – Free Calculator

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.