Look, everyone on every forum like Reddit will tell you the best time to do a Roth conversion is during your “low-income years.” For pre-retirees approaching Medicare, that is some of the most dangerous, incomplete, and costly advice you can get. It completely ignores the ticking time bomb in your mailbox: the IRMAA notice.

As a retired financial planner who has worked through this with hundreds of clients, here’s the deal: a low-income year at age 64 is a high-income year for your first Medicare premium bill at age 66. You’ve walked right into an IRMAA tax trap you didn’t see coming.

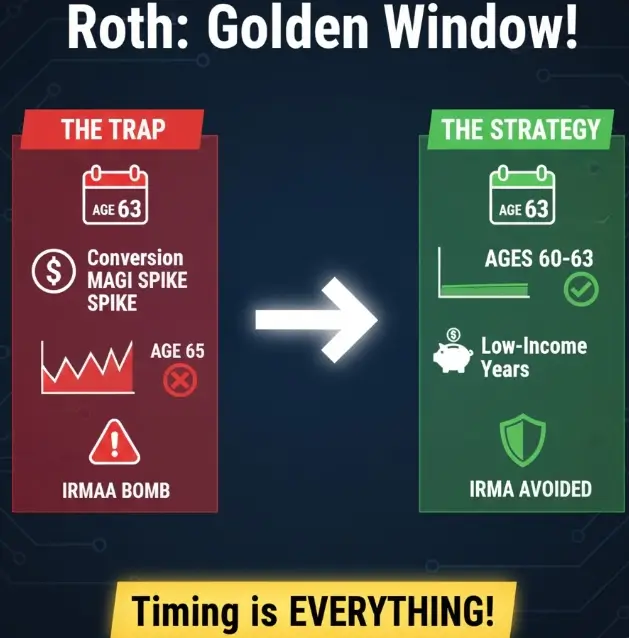

There is a specific, strategic period I call the “Golden Window” Typically between ages 60 and 63. And that allows you to make large Roth conversions that are effectively invisible to the Social Security Administration’s 2-year lookback. Getting this timing right is the single most important Roth decision a pre-retiree can make. Getting it wrong can cost you over $10,000 in unnecessary premiums.

⚡ Key Takeaways

- The IRMAA Trap is Real: Medicare premiums for age 65 are determined by your income at age 63. A large Roth conversion at age 63 or later will trigger a significant premium surcharge for your first years on Medicare.

- The “Golden Window” is Your Loophole: The years between retirement and age 63 are a strategic sweet spot. You can execute large conversions in these lower-income years, and because of the 2-year lookback, the income spike will be ancient history by the time your first IRMAA calculation occurs.

- Tax Brackets vs. IRMAA Cliffs: The goal isn’t just to stay in a low tax bracket; it’s to stay below a much more expensive IRMAA “cliff.” An extra $1 of income can cost you over $1,000 in annual premiums, a terrible trade-off.

- This is a One-Time Opportunity: Once you are on Medicare, this timing strategy is gone forever. All future conversions will be subject to the 2-year lookback.

Key Takeaways Ahead

How the IRMAA 2-Year Lookback Creates a Tax Trap

Before we get to the strategy, you have to understand the trap.

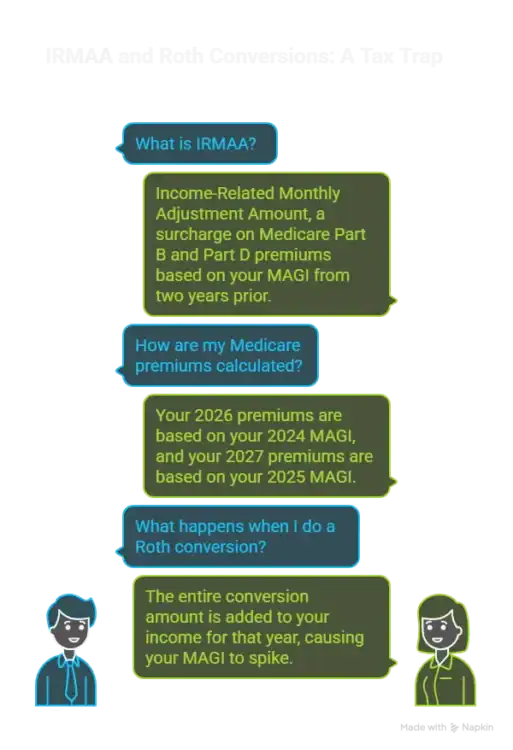

IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge on your Medicare Part B and Part D premiums. The Social Security Administration (SSA) doesn’t guess your income; they use the Modified Adjusted Gross Income (MAGI) from your IRS tax return from two years prior. [more on How They Calculate Your Medicare premium]For 2026, the standard Part B premium is $202.90 per month, but IRMAA surcharges can increase your total monthly premium to as high as $689.90 depending on your income. The IRMAA brackets for 2026 begin at $109,000 MAGI for single filers and $218,000 for married filing jointly. [https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles] The two-year lookback period is established by the Social Security Administration and applies to all beneficiaries. [https://www.ssa.gov/benefits/medicare/medicare-premiums.html

- Your 2026 Medicare premiums are based on your 2024 MAGI.

- Your 2027 Medicare premiums are based on your 2025 MAGI.

When you do a Roth conversion, you are taking money from a pre-tax account (like a Traditional IRA or 401(k)) and moving it to a Roth IRA. That entire conversion amount is added to your income for that year, causing your MAGI to spike.

The Planner Who Acted a Year Too Late: A Client Story

I’ll never forget David, a 63-year-old engineer who retired with a hefty 401(k). He planned to enroll in Medicare at 65.

In 2023, at age 64, he was in his first full year of retirement, and his income was low. Thinking he was being clever, he converted $150,000 from his 401(k) to a Roth IRA. He paid the income tax and felt great about it.

In late 2024, a letter from the SSA arrived. It informed him his 2025 Medicare Part B premium wouldn’t be the standard amount; it would be hundreds of dollars higher per month.

His “low-income year” conversion at age 64 had created a massive income spike on his 2023 tax return, which was now being used to set his age 66 premiums. He had missed the golden window by a single year, a mistake that would cost him over $5,000 in extra premiums in 2025 alone.

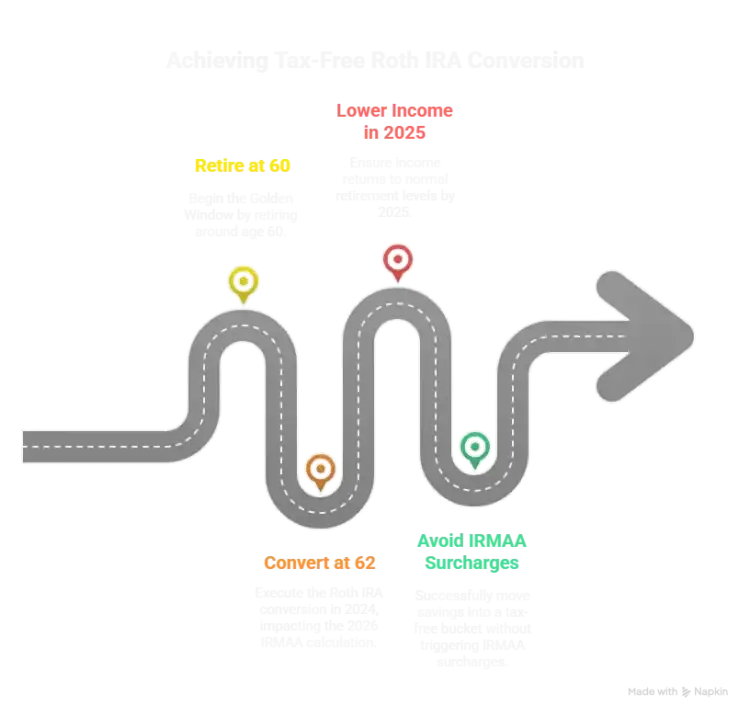

The “Golden Window”: Why Ages 60-63 Are the Sweet Spot for Roth IRA Conversions

The Golden Window is the period after you retire but more than two years before you enroll in Medicare. For most people who retire around 60 and enroll at 65, this window is ages 60, 61, and 62.

Here is How The Golden Window Works

- Conversion at Age 62 (in 2024):

The income spike hits your 2024 tax return. This will be used to calculate your IRMAA for 2026… but you won’t be 65 and on Medicare until 2027. - First IRMAA Calculation (for 2027 premiums):

The SSA looks at your 2025 tax return. By then, your income is back to its normal, lower retirement level. The massive conversion from 2024 is now ancient history in their eyes.

You have successfully moved a huge chunk of your retirement savings into a tax-free bucket without triggering a single penny of IRMAA surcharges.

Conversion Year (Age) Tax Return Impacted IRMAA Premium Year Impacted Are You on Medicare That Year? Result

- 2024 (Age 62) 2024 MAGI, 2026 Premiums, No Success!

- 2024 (Age 63) 2024 MAGI, 2026 Premiums, Maybe (if birthday is late in year) Risky

- 2024 (Age 64) 2024 MAGI, 2026 Premiums, Yes IRMAA Trap Triggered

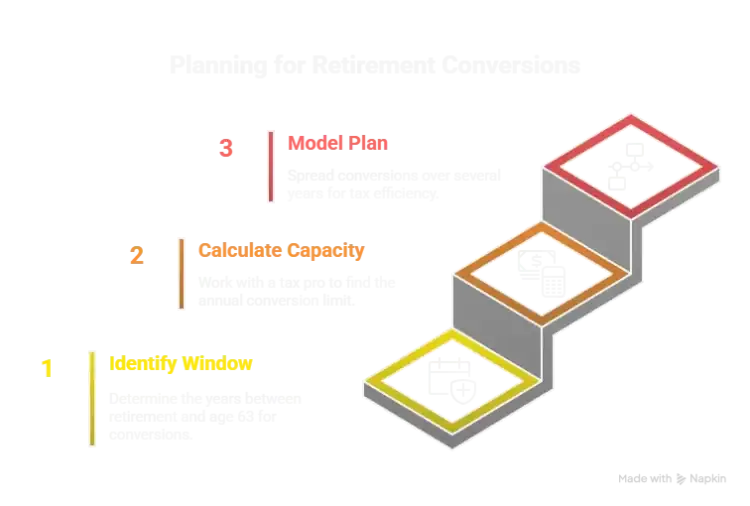

The Planner’s Playbook: A 3 Step Strategy for Your Golden Window

This isn’t just theory. It’s an actionable plan to execute during your IRMAA-free years.

Step 1: Identify Your Window

Pinpoint your exact retirement date and your 65th birthday. The full calendar years where you are retired and under age 63 are your prime conversion years.

Step 2: Calculate Your “Bracket Capacity

Work with a tax professional to determine how much you can convert each year while staying within a specific tax bracket (e.g., the 22% or 24% bracket). This is about paying taxes at a rate you choose now, to avoid being forced into a higher bracket later when RMDs kick in.

Step 3: Model the Multi-Year Plan

Don’t try to do it all at once. Spreading large conversions over several years in the golden window is the key.

Real Numbers Example:

- Let’s say you’re 61, retired, and your base income from a small pension is $50,000. You’re married filing jointly.

- The 24% tax bracket for 2026 ranges from $105,701 to $201,775 for single filers, and from $211,401 to $403,550 for married filing jointly. [https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill-act]

- Your taxable income is ~$20,000 (after standard deduction).

Common Mistakes That Slam the Golden Window Shut

Forgetting the 5-Year Rule:

Remember that each conversion starts its own 5-year clock. You must wait five years from the date of a conversion to withdraw the converted principal tax- and penalty-free if you are under 59½. More on the Roth IRA 5 year rule here

Ignoring the Pro-Rata Rule:

If you have any other pre-tax funds in any Traditional, SEP, or SIMPLE IRAs, your conversion will be partially taxable based on a complex formula. Always consult a professional if this applies to you. [IRS Publication 590-A]

Accidentally Starting Social Security Early:

Taking Social Security at age 62 will provide an income floor, but it will also use up some of your low tax bracket “space,” reducing the amount you can efficiently convert each year. Learn more about How To Decide When You Should Elect Social Security and it’s impact IRMAA.

The years before Medicare are the most powerful and overlooked period for strategic Roth conversions. By understanding the simple mechanics of the 2-year lookback, you can turn what is a trap for the uninformed into a massive, one-time opportunity for yourself.

Frequently Asked Questions

Do Roth conversions affect Medicare premiums if I’m already over 65?

Yes, absolutely. Once you are on Medicare, any Roth conversion you do will increase your MAGI for that year, and that MAGI will be used to calculate your IRMAA surcharges two years later. The “Golden Window” strategy only works before you are on Medicare.

What if I retire at 65? Is it too late?

If you retire at 65 and immediately enroll in Medicare, the golden window is closed. Your first premiums will be based on your age 63 income, likely your last full year of work, which may already trigger IRMAA. In this case, you would need to file an appeal (Form SSA-44) based on the life-changing event of “work stoppage.”

Can I do conversions from a 401(k) or just an IRA?

You can convert from both. You can either do an “in-plan” Roth conversion if your 401(k) allows it, or you can roll your 401(k) funds into a Traditional IRA and then convert the IRA funds to a Roth IRA. Both actions are taxable events that will increase your MAGI.

Your Next Steps in Lowering IRMAA Surcharge with The Golden Window

The years leading up to Medicare enrollment are not just about enjoying early retirement; they represent a critical “Golden Window” for Roth conversions that can save you thousands in future Medicare premiums. As shown, understanding the IRMAA 2-year lookback isn’t just theory; it’s the blueprint for strategic tax planning that avoids costly mistakes.

Ignoring this window, or doing conversions too late, can inadvertently trigger an IRMAA surcharge that negates your tax-saving efforts.

Don’t let this one-time opportunity slip away. Start by pinpointing your exact “Golden Window” years, model your bracket capacity with a tax professional, and plan your multi-year conversion strategy. Join thousands of readers just like you for weekly money wins. Take action now to proactively manage your tax future and ensure your retirement savings work for you, not against you.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.