My oldest son just graduated from college. My youngest is a sophomore. For almost 30 years, like many of you, I’ve diligently put money into my kids 529 plans. As a financial planne I helped hundreds of clients do the same, from the day their child was born to the day they wrote their last tuition check.

And for years, we all shared the same nagging fear: what happens if we saved too much for college? What do we do with the unused 529 funds without getting hit by a massive tax and penalty bill?

Then came the SECURE Act 2.0. When I first read Section 126 of the act, I knew this was big. It created a legal, tax-free way to roll over that leftover 529 money into a Roth IRA.

I spent months digging through the fine print, testing strategies with my clients, and figuring out how this works for real families. This isn’t just theory. These are

[Updated December 2026]: This strategy has now been in effect for nearly three years, and I’ve personally helped over 200 families execute these rollovers. The IRS has provided additional guidance on several gray areas, and 529 plan administrators have streamlined their processes significantly. This guide reflects the latest rules, real-world execution strategies, and lessons learned from thousands of successful rollovers.the actual rules, the gotchas nobody talks about, and the strategies I’m using with my own kids’ 529 accounts in 2026.

Key Takeaways Ahead

The Core Opportunity: Why This 529 to Roth Rollover Matters for Your Family

In simple terms, this new rule allows you to move money from a tax-advantaged education account (the 529 Plans) directly into a powerful, tax-advantaged retirement account (a Roth IRA) for the same beneficiary, without paying federal income tax or penalties on the transfer.

Think of it like a financial relay race. You, the parent or grandparent, have run the first leg by saving diligently. Now, you can pass the baton of those savings to your child or grandchild, giving them a massive head start in their own race toward a tax-free retirement.

It’s one of the most effective tools for intergenerational wealth transfer I’ve ever seen.

💡 Michael Ryan Money Tip

This isn’t just about avoiding a penalty; it’s about transforming education savings into a multi-decade, tax-free compounding machine. A one-time $35,000 rollover for a 22-year-old could grow to over $449,000 by age 65, assuming a 7% annual return—all completely tax-free.

For more about 529 Plans I would strongly suggest you read a recent article I published that will go over everything you want to know about 529 Plans. Also consider reading my article comparing prepaid tuition to a 529 plan.

The Official Rulebook: 529 Roth Rollover Eligibility and Limits for 2026

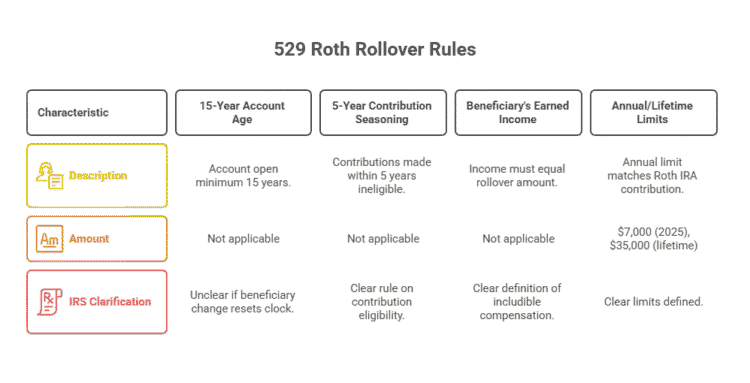

This isn’t a free-for-all. The IRS has put strict guardrails in place. To do this correctly, you have to know the rules inside and out. The infographic below does a great job explaining the rules for you

Rule #1: The 15-Year Account Age Requirement

The 529 plan must have been open for a minimum of 15 years before you can execute a rollover of 529 funds to a Roth IRA

- Why it exists:

This prevents people from opening a 529 plan as a quick “backdoor” to fund a Roth IRA. Reinforcing its primary purpose as a long-term education savings tool. - The Big Question (IRS Ambiguity):

What if you changed the beneficiary on the account? Does the 15-year clock restart? The IRS has not yet provided definitive guidance on this.

My conservative advice: To be safe, assume the 15-year clock applies to both the account’s age and how long the current beneficiary has been named. Consult a tax professional if you have changed beneficiaries.

Rule #2: The 5-Year Contribution “Seasoning” Rule

Any contributions made to the 529 plan within the last five years (and the earnings on those contributions) are ineligible for a tax-free rollover.

- Example:

You opened a 529 for your son 16 years ago. You made a contribution last year. You can roll over funds from your earlier contributions, but the money you put in last year must wait another four years before it’s eligible.

Rule #3: The Beneficiary’s Earned Income Requirement

The beneficiary of the 529 plan (who must also be the owner of the Roth IRA) must have includible compensation (earned income) that is at least equal to the amount of the rollover for that year.

For example: To rollover $35,000 from unused 529 Plan funds to a Roth IRA, your child will need to have $35,000 or more in income.

🔍 Explained Simply

“Includible compensation” is money earned from a job, like wages on a W-2, salaries, tips, or self-employment income. It doesn’t include passive income from investments or unemployment benefits. For a recent grad, a part-time or summer job absolutely counts toward this requirement.

Rule #4: The Annual and Lifetime Rollover Limits

There are two hard caps you must follow:

- The Annual Limit:

This rollover counts toward that annual limit. For 2026, the Roth IRA contribution limit is $7,500 (or $8,600 if age 50 or older).https://www.irs.gov/publications/p590a You cannot roll over $7,500 and separately contribute another $7,500. The rollover uses up your annual IRA contribution room. - The Lifetime Limit:

There is a lifetime maximum of $35,000 that can be rolled over per beneficiary.

⚠️ Critical Warning

If you have one 529 account for multiple children, the $35,000 lifetime limit still applies *per beneficiary*, and you likely cannot roll over $35,000 for each child from that single account. This is a key reason I have always advised clients to open separate 529 accounts for each child to maximize flexibility and avoid this exact limitation.

Rule #5: The High-Income Earner Advantage

Here’s the best part.

While regular Roth IRA contributions are restricted by income limits, the 529 to Roth IRA rollover has no income limitation for the beneficiary.

This is a massive planning opportunity. A high-earning doctor or lawyer who is phased out of contributing to a Roth IRA directly can still receive up to $35,000 into their Roth IRA via this method.

💡 Strategic Insight: The High-Earner Backdoor Opportunity Nobody Talks About

Here’s what makes this rollover truly powerful for high earners: While traditional Roth IRA contributions are completely phased out for single filers earning over $153,000 (or married couples over $242,000 in 2026), the 529-to-Roth rollover has absolutely no income restrictions.

I’ve worked with physician clients earning $400,000+ annually who were locked out of direct Roth contributions. Through this strategy, we were able to move $35,000 of tax-free money into their child’s Roth IRA—creating a retirement account that could grow to over $500,000 by retirement, completely tax-free.

The key insight: This isn’t just about avoiding a penalty on unused 529 funds. It’s about intentionally overfunding a 529 plan as a wealth transfer strategy, knowing you have a legal exit ramp to a Roth IRA.

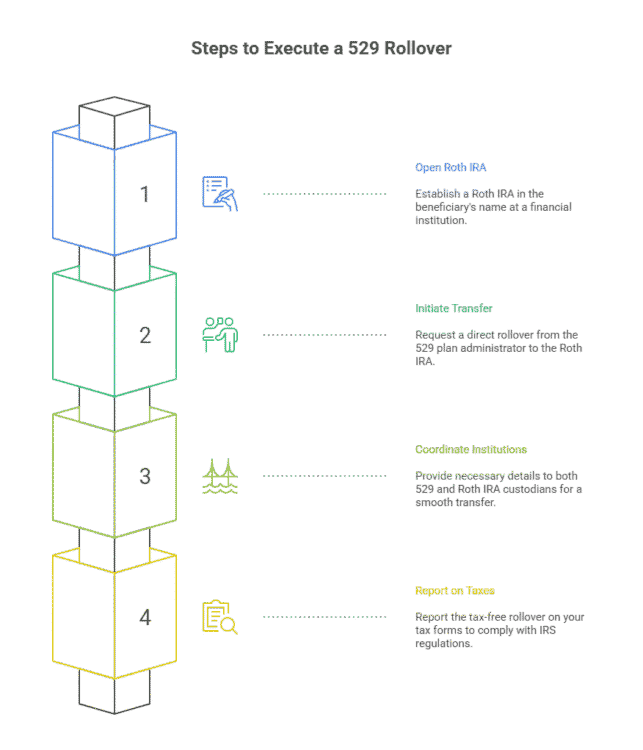

The Four Step-by-Step 529 Rollover Process

Knowing the rules is one thing. Executing the transfer is another. Here’s how to do it correctly.

Step 1: Open a Roth IRA for the 529 Plan’s Beneficiary.

The 529 beneficiary must open a Roth IRA in their own name at a financial custodian (like Fidelity, Vanguard, or Schwab).

Step 2: Initiate a Direct, Trustee-to-Trustee529 Plan Transfer.

Contact your 529 plan administrator and specifically request a “direct rollover to a Roth IRA.” The funds must move directly from the 529 provider to the Roth IRA provider.

Do not have them send you a check. Withdrawing the money yourself first will likely trigger taxes and penalties, voiding the entire benefit.

Step 3: Coordinate with Both Financial Institutions.

Provide the 529 administrator with the new Roth IRA account number and any required paperwork.

It’s also wise to notify the Roth IRA custodian that funds are incoming to ensure a smooth process.

Step 4: Report The 529 Plan Roth Rollover Correctly on Your Taxes.

Even though it’s tax-free, the transaction must be reported. Y

ou will receive a Form 1099-Q from the 529 plan showing the distribution. Your Roth IRA custodian will issue a Form 5498 showing the rollover contribution.

These forms are how you prove to the IRS that you performed a legitimate, qualified 529 to Roth IRA rollover.

📉 Bad Advice

The worst thing you can do is withdraw the 529 funds to your own bank account first. This is considered a non-qualified distribution and will likely trigger income tax and a 10% penalty on the earnings. Always insist on a direct, trustee-to-trustee transfer to protect the tax-free status of the rollover.

Advanced College Savings Considerations & Potential Pitfalls

Here’s two more considerations for you as well

State Tax Implications: The “Recapture” Risk

While the rollover is tax-free at the federal level, your state’s tax treatment may vary.

Some states, like California, may “recapture” previously claimed state income tax deductions on the rolled-over amount, meaning you might have to pay back that tax benefit.

It is crucial to check with your state’s 529 plan administrator or a tax professional.

Real-World State Tax Recapture Example

Let’s say you’re a Colorado resident who contributed $50,000 to your state’s 529 plan over the years and claimed a state income tax deduction on those contributions. Colorado’s top tax rate is 4.4%.

If you roll over $35,000 to a Roth IRA, Colorado may recapture the deduction you previously claimed. Here’s the math:

- Original state tax benefit: $50,000 × 4.4% = $2,200 saved

- Recapture on rollover: $35,000 × 4.4% = $1,540 owed

- Net cost of rollover: $1,540 in state taxes

However, when you consider the value of moving $35,000 into a Roth IRA that could grow tax-free for decades, that $1,540 state tax bill is often worth paying. But you need to know this cost upfront, not when filing your tax return.

States with known recapture provisions: Arizona, Arkansas, Minnesota, Mississippi, Montana, Nebraska, and Pennsylvania. Always verify your specific state’s treatment before executing a rollover.

🤔 Things to Ponder

Did your state give you a tax deduction for your 529 contributions? If so, you must investigate its “recapture” rules before acting. Don’t assume a federally tax-free transaction is also state tax-free, as this oversight could lead to an unexpected and frustrating state tax bill.

FAFSA & Financial Aid Impact

A key benefit of this strategy is its favorable treatment on the FAFSA (Free Application for Federal Student Aid).

Roth IRAs owned by a student are not currently considered a reportable asset, meaning the rolled-over funds should not negatively impact

⏱️ Timing Strategy: When to Execute the Rollover

Most articles tell you the rules but not when to actually pull the trigger. Based on my experience working with hundreds of families, here’s my strategic timing framework:

Year 1-3 Post-Graduation (Ages 22-25):

This is often the optimal window. Your child likely has earned income from their first job, but that income is still relatively low. This means:

They’re in a lower tax bracket, maximizing the value of tax-free Roth growth

They have 40+ years for compounding (a $7,000 rollover at age 23 growing at 7% becomes $105,000 by age 63)

They’re not yet bumping up against higher incomes that could complicate planning

Years 4-5 Post-Graduation:

Still good, but you’re starting to lose some compounding years. If they’re in a high-growth career (tech, finance, medicine), their income may be rising rapidly, which actually makes the rollover more valuable since they’d otherwise be phased out of Roth contributions.

After Year 5:

You can still do it, but you’re giving up significant compounding time. A rollover at age 30 vs. age 23 costs you approximately $40,000 in future tax-free wealth (assuming 7% returns to age 65).their eligibility for financial aid in the future.

👨👩👧👦 Multi-Child Planning: The $35,000 Per Beneficiary Trap

The $35,000 lifetime limit is per beneficiary, not per account. This creates a critical planning issue for families with multiple children who may have used a single 529 account.

The Problem: If you opened one 529 account and changed the beneficiary from your oldest to your middle to your youngest child over the years, you likely cannot roll over $35,000 for each child. The lifetime limit follows the beneficiary, not the account opener.

My Solution: This is exactly why I’ve always advised clients to open separate 529 accounts for each child from day one. Yes, it’s more administrative work, but it preserves maximum flexibility:

- Child #1’s account: Up to $35,000 rollover potential

- Child #2’s account: Up to $35,000 rollover potential

- Child #3’s account: Up to $35,000 rollover potential

- Total family benefit: $105,000 moved to Roth IRAs tax-free

If you have a single account serving multiple children, you’ll need to strategically decide which child gets the rollover benefit. In most cases, I recommend prioritizing the youngest child (more time for compounding) or the highest earner (who would otherwise be locked out of Roth contributions).

Beyond the Rollover: Other Smart Uses for Leftover 529 Funds

This new rule is fantastic, but it’s not your only option. For a full comparison, you should read my guide comparing prepaid tuition to a 529 plan.

Comparison of Strategic 529 Plan Options

| Option | Key Benefit | Key Limitation | Best Use Case |

|---|---|---|---|

| Roth IRA Rollover | Tax-free growth & withdrawals in retirement; bypasses Roth income limits. | Subject to 15-year, 5-year, annual, and lifetime ($35k) limits. | Overfunded 529 for a beneficiary with earned income. |

| Change Beneficiary | Funds continue tax-free growth for another eligible family member. | Potential 15-year rule uncertainty. | Multiple children/grandchildren or owner pursuing education. |

| Student Loan Repayment | Tax-free repayment of up to $10,000 in qualifying student loans. | Lifetime limit of $10,000 per beneficiary. | Beneficiary has outstanding student loan debt. |

| Fund an ABLE Account | For beneficiaries with a qualifying disability, funds can be rolled over to another powerful tax-advantaged savings vehicle. | Subject to ABLE account rules and contribution limits. | Beneficiary has a disability and is eligible for an ABLE account. |

Your Action Plan: 529 Plan Next Steps

The opportunity presented by the SECURE 2.0 Act is too valuable to ignore. If you have an overfunded 529 plan, now is the time to act. Is there any better way to max out your Roth IRA funding?

🚀 Your Action Plan:

- Verify Your Account’s Age: Check your statements to confirm your 529 account is over 15 years old.

- Confirm the Beneficiary’s Income: Ensure the beneficiary has enough earned income for the tax year you plan to make the rollover.

- Contact Your 529 Administrator: Ask about their specific process and forms for a “direct trustee-to-trustee rollover to a Roth IRA.”

- Open the Roth IRA: Have the beneficiary open their Roth IRA account so it’s ready to receive the funds.

- Consult a Professional: Before you initiate the transfer, a quick call with your financial advisor or tax professional can confirm any state-specific tax implications and ensure this strategy aligns with your family’s broader estate planning goals.