You worked for 40 years, paid your FICA taxes, and finally retired. You assumed your Social Security check was yours.

Then you get your tax bill.

Not only is the IRS taking a cut of your benefits, but Medicare just sent a letter saying your premiums are doubling next year. Welcome to the “Double Tax Trap”. The specific intersection where Social Security taxation collides with Medicare IRMAA surcharges.

The tax rules (IRC §86) governing your Social Security taxes haven’t been updated since 1984, and a single dollar of extra income can trigger a cascading failure of your tax plan.

I’ve seen retirees with a modest $70,000 lifestyle get hit with effective marginal tax rates of over 50% because they didn’t see this train coming. Here is how to spot it—and how to get out of the way.

⚡ Key Takeaways

- Definitive Reality: Up to 85% of your Social Security benefits become taxable income once you cross fixed thresholds ($34k single / $44k married).

- The Stealth Tax: These thresholds are fixed by federal law, meaning every COLA increase pushes more middle-class retirees into the tax net.

- The Interaction: Higher taxable Social Security increases your AGI, which can push you over the IRMAA Cliff, increasing Medicare Part B and D premiums by thousands.

- Actionable Strategy: Strategies like QCDs and Roth Conversions are the only reliable ways to manage this “Provisional Income” equation.

- Checklist:

[ ] Check AGI

[ ] Calculate Provisional Income

[ ] Compare to IRMAA tiers.

Key Takeaways Ahead

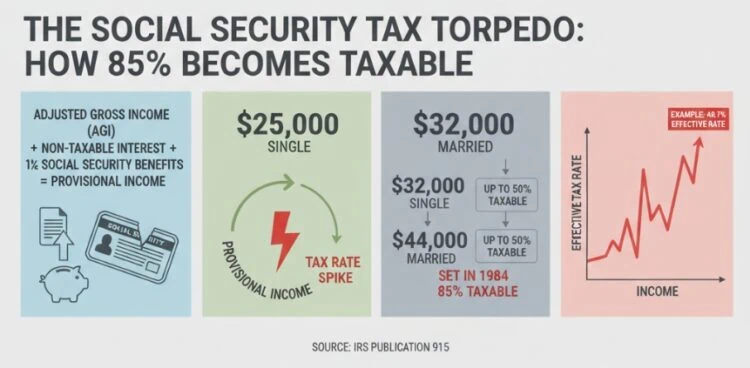

The Foundation: Why 85% of Your Check Disappears

Before we get to the Medicare penalties, we have to look at the engine driving the problem: Provisional Income.

Here’s what most people miss: The 85% figure isn’t a tax rate. It’s the amount of your benefit that gets added to your taxable income. You pay your regular income tax rate on that 85%.

But here is the unspoken truth: The thresholds determining this tax were set in the 1983 and 1993 Social Security Amendments. They were never indexed for inflation.

In 1984, $25,000 was a solid upper-middle-class retirement income. In 2026? It’s near the poverty line. Yet the tax trigger remains exactly the same.

What triggers 85% Social Security taxation?

To have 85% of your benefits taxed, your provisional income must exceed:

- $34,000 (single filers)

- $44,000 (married filing jointly)

The IRS Provisional Income Rule

The IRS uses a specific calculation (IRC §86) to decide if they tax your benefits. It is distinct from your AGI.

Provisional Income (called “Combined Income” in IRS Publication 915) = Adjusted Gross Income (AGI) + Nontaxable Interest + (50% of Social Security Benefits)

👉 Tax Return Check:

Look at your 2024 Form 1040. Add Line 11 (AGI) and Line 2a (Tax-Exempt Interest).

If this sum plus half your Social Security exceeds $44,000, you are in the danger zone.

- AGI (Line 11 of Form 1040): Wages, dividends, capital gains, RMDs, pensions.

- Nontaxable Interest (Line 2a of Form 1040): Municipal bond interest (yes, this counts against you here).

- 50% of SS: Half your annual benefit.

Real World Consequence:

If you are married and have $44,000 in combined income (which is low for two people in 2026), every additional dollar you withdraw from an IRA causes **$0.85** of your Social Security to become taxable.

This creates the “Tax Torpedo.”

However, you might think you are in the 12% bracket. But because earning $1 exposes $0.85 of SS to tax, your effective marginal rate spikes. You are paying tax on $1.85 for every $1.00 you earn.

⚠️ Myth Busted: “My Tax Rate Will Drop in Retirement”

The “Tax Torpedo” often pushes retirees into a 40.7% effective marginal rate on IRA withdrawals—higher than they paid while working.

Example: If you are in the 22% bracket, you pay $0.22 on the $1.00 withdrawal.

But that withdrawal exposes $0.85 of Social Security to another 22% tax ($0.187).

Total tax on that one dollar = $0.407.

You are effectively paying a 40.7% tax rate on that specific withdrawal.

Medicare IRMAA Surcharges: The 2026 Brackets

While the IRS is taxing your benefits, Medicare (CMS) is watching your income from two years ago.

IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge added to your Medicare Part B and Part D premiums if your income is considered “high.”

Here is the trap: Taxable Social Security counts toward IRMAA.

The Feedback Loop

Therefore, a single financial decision can spiral:

- You take an extra $10,000 from your IRA.

- The withdrawal SPIKES your Provisional Income.

- More of your Social Security TRIGGERS into taxable status.

- Your AGI JUMPS by the IRA withdrawal plus the newly taxable Social Security.

- This inflated AGI PUSHES you over the IRMAA Cliff.

What income triggers IRMAA?

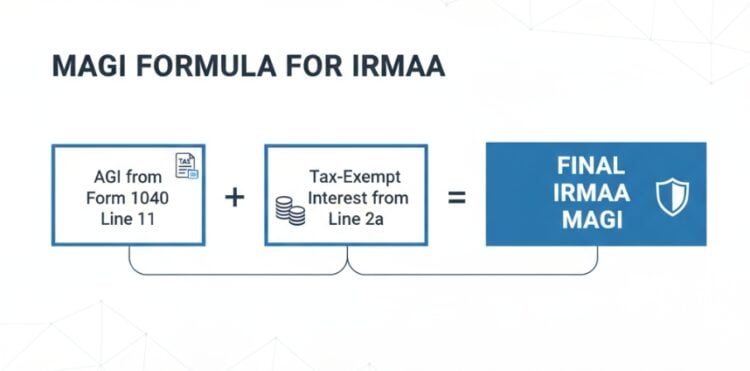

IRMAA is triggered when your Modified Adjusted Gross Income (MAGI) from two years prior exceeds:

- $109,000 (single, 2026)

- $218,000 (married, 2026)[

Note: Final 2026 numbers are released in late 2025, but they are based on your 2024 tax return.

IRMAA is a cliff penalty. Go $1 over the limit, and Medicare charges you the full surcharge. There is no partial adjustment.

Client Story: The $28,000 Mistake

In 2024, I met “Robert a~$212,000

nd Linda.” They sold a small rental property, generating a $150,000 capital gain. They thought, “We’ll just pay the 15% capital gains tax.”

Robert told me, “I worked 40 years for this money, and because I sold one rental, they treated me like a billionaire.”

The Reality:

- The gain pushed their Provisional Income through the roof.

- 85% of their $60,000 Social Security benefits became taxable (adding $51,000 to their taxable income).

- Their total MAGI spiked over the 3rd IRMAA tier.

- The Cost: They paid capital gains tax, PLUS income tax on the SS benefits, PLUS an extra $7,800 in Medicare premiums for the year.

- The Effective Rate: On that specific chunk of income, they lost nearly 55% to various government buckets.

Step-by-Step: How to Calculate Your Tax Torpedo Exposure

- Start with AGI: Locate Line 11 on your Form 1040.

- Add Tax-Exempt Interest: Locate Line 2a.

- Add 50% of Social Security: Take half of the amount in Box 5 of your SSA-1099.

- Compare to Thresholds: Are you over $34,000 (single) or $44,000 (married)?

- Identify the “Taxable Bump”: Calculate how much of your SS is moving from 0% taxable to 85% taxable based on your withdrawals.

- Calculate Effective Rate: If you are in the torpedo zone, multiply your bracket by 1.85 to see your real tax rate.

Understanding the distinctions between the Tax Torpedo and IRMAA is critical for retirees optimizing their financial planning. This comparison highlights how different income calculations can significantly impact Social Security taxation and Medicare premiums, offering vital insights for strategic withdrawals and conversions.

| Feature | Tax Torpedo | IRMAA |

|---|---|---|

| Based on | Provisional Income (Combined Income) | MAGI (Modified Adjusted Gross Income) |

| Affects | % of Social Security subject to Income Tax | Medicare Part B & D Monthly Premiums |

| Trigger Type | Sliding Scale (0% → 50% → 85%) | Hard Cliff ($1 over = Full Penalty) |

| Lookback | Current Tax Year | 2 Years Prior |

| Planning Tools | QCDs, Roth Withdrawals, Income Smoothing | SSA-44 Appeal, Roth Conversions (Timing) |

Proactive planning around these income triggers can significantly reduce your tax burden and optimize Medicare costs in retirement.

The Widow’s Penalty: A Hidden Risk

Surviving spouses often face the harshest version of this trap.

When a spouse passes away, the household income often remains similar (inherited IRAs, survivor benefits), but the tax filing status shifts from Married Filing Jointly to Single.

- The Threshold Drop: The Provisional Income hurdle drops from $44,000 to $34,000.

- The IRMAA Cliff: The IRMAA cliff drops from $218,000 to $109,000.

- The Result: A widow often pays more tax on less income.

Michaeal Ryan Money Tip: If you are recently widowed, you have a 2-year window to file as “Qualifying Widow(er)” before these single brackets hit. Use that time to execute Roth conversions or accelerate withdrawals while you still have the married brackets.

The Escape Hatch: 4 Strategies to Diffuse the Trap

You cannot change the tax code, but you can control your “Provisional Income.”

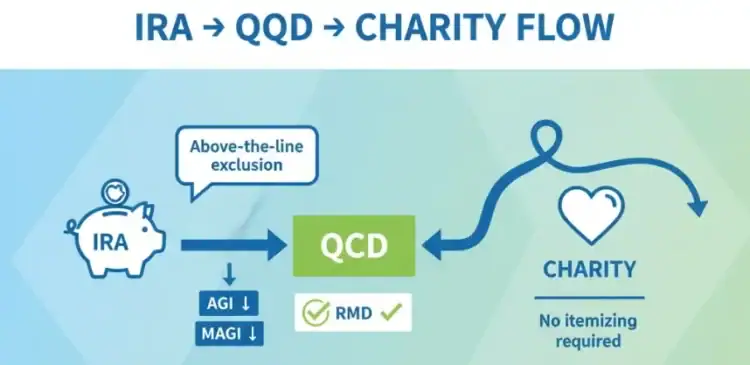

1. Qualified Charitable Distributions (QCDs)

This is the single most effective tool for retirees over age 70½. A Qualified Charitable Distribution (QCD) allows you to send money directly from your IRA to a charity.

- The Magic: It satisfies your RMD (Required Minimum Distribution) but does not count as income.

- The Result: It lowers your AGI. It lowers your Provisional Income. It lowers your IRMAA MAGI. It saves your Social Security from taxation.

- Limit: Up to $111,000 (indexed) per year for 2026.

💡 Michael’s Tip: The 1099-R Trap

Crucial Note: Your IRA custodian will send a Form 1099-R that looks like a normal taxable withdrawal. They do NOT separate the QCD amount. You must explicitly tell your CPA (or mark it in your tax software) that it was a QCD, or the IRS will assume it is fully taxable income.

2. The “Roth Firewall”

Roth IRA withdrawals are tax-free.

- They do not count toward Provisional Income.

- They do not count toward IRMAA.

- Strategy: If you need a lump sum (for a car or roof), pull it from the Roth, not the Traditional IRA. This keeps your taxable income low and protects your SS check.

- Important Distinction: Roth Conversions count as income in the year you do them (and can trigger IRMAA), but future withdrawals are tax-free. Roth Contributions have income limits, but conversions do not.

3. Managing “Lumpy” Income

IRMAA has a 2-year lag. If you plan to sell a house or realize a large gain in 2026:

- Accept that 2028 premiums will spike.

- OR, try to spread the gain over two years (installment sale) to stay under the cliffs.

- Warning: Do not execute a massive Roth conversion in the same year you are taking large capital gains. You are stacking income on top of income.

- Learn more about income spikes and the impact on IRMAA here.

4. The Life-Changing Event Appeal (SSA-44)

If your income spiked in 2024 because you were working, but you retired in 2025, you do not have to pay the 2026 IRMAA surcharge based on that old income.

- The Solution: File Form SSA-44 and do a life changing appeal.

- Action: Skip to Step 1: Life-Changing Event.

- Check the box for “Work Stoppage” or “Work Reduction.”

- The SSA will recalculate your premiums based on your current, lower retirement income.

Michael Ryan Note: When filing Form SSA-44, I always advise clients to include a copy of the signed settlement statement from their employer as proof of “Work Reduction.” The SSA often rejects the form without this specific evidence.

The Bottom Line on the Double Tax Trap

Social Security tax thresholds were set decades ago. Because they were never indexed for inflation, more retirees cross these limits every year. Triggering both taxation and IRMAA surcharges.

If you simply withdraw from your 401(k) without doing the math, you are volunteering for a tax hike.

Want to see exactly where you stand?

📉 Get the Official 2026 IRMAA Brackets

The 2026 IRMAA numbers will be finalized in November. Sign up here, and I will email you the exact brackets the day they are released.

What This Means for You

If you are approaching age 63:

This is your IRMAA lookback window for age 65. Watch your income in 2024/2025 carefully.

If you have RMDs starting:

Calculate if the RMD will push you into the “85% Taxable” SS zone. If so, consider QCDs immediately.

If you are high-income ($200k+):

Accept IRMAA as a cost of wealth, but fight to stay out of the highest tiers. The top tier surcharge is punitive.

Printable Checklist: Avoiding the Double Tax Trap

[ ] Calculate Provisional Income (AGI + Tax-Free Interest + 50% SS)

[ ] Check IRMAA MAGI (AGI + Tax-Free Interest)

[ ] Identify income spikes (Planned property sales or Roth conversions)

[ ] Review Roth vs Traditional withdrawals for major purchases

[ ] Consider QCDs if over age 70.5 to satisfy RMDs

[ ] Model 2-year IRMAA lookback impact before taking gains

Sources & Verification

- IRS Publication 915: Social Security and Equivalent Railroad Retirement Benefits{target=”_blank” rel=”noopener noreferrer”}

- CMS Medicare Costs: Medicare Part B Costs & IRMAA{target=”_blank” rel=”noopener noreferrer”}

- SSA Program Operations Manual System (POMS): IRMAA Calculation Rules{target=”_blank” rel=”noopener noreferrer”}

- IRC §86: Social Security Benefit Taxation Rules{target=”_blank” rel=”noopener noreferrer”}

Frequent Reader Questions

At what income is 85% of Social Security taxed?

For single filers, up to 85% of benefits are taxable if combined income exceeds $34,000. For married couples filing jointly, the threshold is $44,000. These thresholds are not indexed for inflation, meaning they hit more retirees every year. [IRS Publication 915]

Does Social Security count toward IRMAA?

Yes, but only the taxable portion. Since IRMAA is based on Modified Adjusted Gross Income (MAGI), and your AGI includes the taxable portion of your Social Security, higher benefits can indirectly trigger higher Medicare premiums.

Can I deduct IRMAA premiums on my taxes?

Yes. IRMAA surcharges are considered part of your medical insurance premiums. If you itemize deductions, they can be included as a medical expense (subject to the 7.5% AGI floor). If you are self-employed, you may be able to deduct them “above the line.” [IRS Publication 502]

What is the “Tax Torpedo”?

The “Tax Torpedo” refers to the income range where earning an extra $1 of income triggers tax on $0.85 of Social Security benefits. This creates an effective marginal tax rate that is much higher than your statutory tax bracket—often pushing a 12% or 22% bracket filer into a 40%+ effective rate zone.

Will these thresholds ever be indexed for inflation?

No. Unlike tax brackets, the Provisional Income thresholds ($25k/$32k) are fixed by federal law. This means the “Tax Torpedo” will effectively hit lower-income retirees every single year as COLA raises push their income higher while the cliff remains stationary.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.