For years, I’ve seen the same advice echoed in online forums and even from financial professionals: “Avoid triggering IRMAA at all costs.” It’s treated as the third rail of retirement planning.

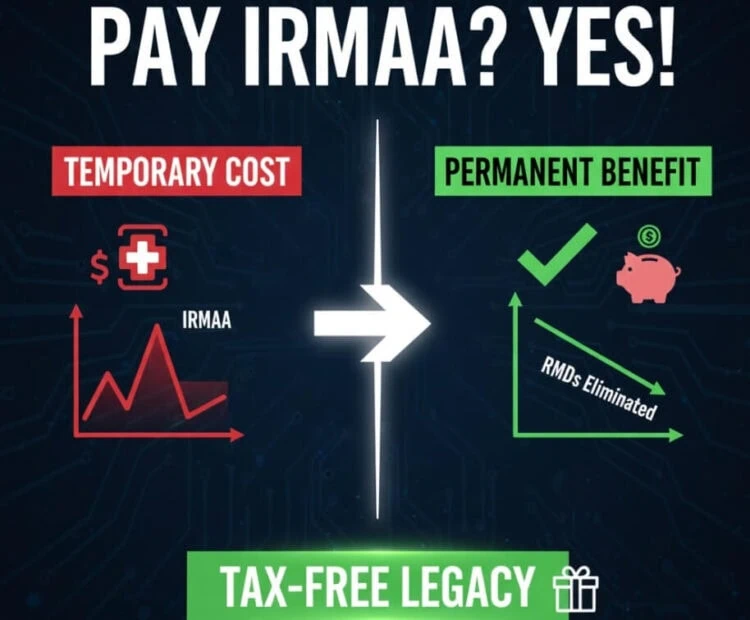

IRMAA is a costly penalty for earning too much. But what if I told you that, for many savvy retirees, willingly paying a temporary IRMAA surcharge is one of the smartest and most profitable financial moves you can make?

As a financial planner for nearly 30 years, I can tell you that the fear of IRMAA often leads to dangerously short-sighted decisions. Retirees with huge tax-deferred 401(k)s and IRAs tiptoe around their income, making minimal withdrawals to stay under the IRMAA cliffs.

In doing so, they are ignoring a much larger and more permanent threat: the Required Minimum Distribution (RMD) tax bomb that will detonate in their 70s and beyond.

Deciding to do a large Roth conversion that you know will trigger IRMAA isn’t a mistake; it’s a business decision. It’s a calculated trade-off. You are choosing to pay a known, temporary surcharge in exchange for a much larger, permanent tax benefit.

This guide will give you the three-step calculation framework to determine if this powerful strategy is right for you.

⚡ Key Takeaways

- Reframe the Cost: Think of the IRMAA surcharge not as a penalty, but as a one-time “cost of acquisition” to purchase a permanently tax-free asset (a large Roth IRA).

- It’s a Math Problem: The decision to pay IRMAA for a conversion is not emotional. It hinges on a simple break-even calculation: will your long-term tax savings be greater than the short-term cost of higher Medicare premiums?

- RMDs are the Real Enemy: For those with large pre-tax balances, your future RMDs will likely force you into a high tax bracket and trigger IRMAA every single year. A conversion is your chance to solve that problem permanently.

- A Powerful Legacy Tool: A Roth conversion is one of the greatest gifts you can leave your children, allowing them to inherit a large sum of money completely tax-free, sidestepping the SECURE Act’s 10-year rule tax trap.

Key Takeaways Ahead

The Core Conflict: A Temporary Premium Hike vs. a Permanent Tax Hike

The entire trade-off boils down to two competing forces.

On one side, you have the IRMAA cliffs.

Because Medicare premiums are based on your income from two years prior, a large Roth conversion will absolutely cause a spike in your premiums. As you can see in our 2026 IRMAA bracketscrossing a threshold by just one dollar can cost you over a thousand dollars in extra premiums for the year.

On the other side, you have the guaranteed tax savings and freedom a Roth IRA provides.

Once money is in a Roth, it grows tax-free forever, is never subject to RMDs, and can be passed on to your heirs tax-free. You are essentially paying a one-time fee (income tax + IRMAA) to eliminate a lifetime of future taxes.

The 3 Calculations to Run Before You Act

To make an informed decision, you need to quantify the trade-off. Here are the three calculations you and your financial planner should model.

Calculation #1: The IRMAA Break-Even Point

This is the most important calculation. It tells you how many years it will take for your future tax savings to pay back the initial cost of the conversion.

The Formula: (Total Cost of Conversion) / (Annual Tax Savings) = Years to Break Even

🧮 Real Numbers Example: The Break-Even Calculation

Let’s take a 67-year-old married couple, the Clarks, with $1.5M in a Traditional IRA and a base MAGI of $200,000. They are just under the first IRMAA cliff.

The Conversion Plan: Convert an additional $150,000. This pushes their MAGI to $350,000 for one year.

The Costs:

- Federal Income Tax: The conversion is taxed at 24%. Cost: $150,000 x 24% = $36,000.

- IRMAA Surcharge: Their $350,000 MAGI pushes them into the fourth IRMAA tier for two years (2026 & 2027 based on their 2024 and 2025 tax returns). According to the official 2026 CMS IRMAA brackets, this costs them a Part B surcharge of $324.60 per person, per month ($3,895 per person, per year). Total IRMAA Cost: $3,895 x 2 people x 2 years = $15,580.

- Total One-Time Cost: $36,000 + $15,580 = $51,580.

The Benefit (Annual Savings):

- Without the conversion, their future RMDs at age 73 would be ~$75,000 per year, pushing them into a higher tax bracket. By converting, they’ve eliminated that future taxable income. Let’s estimate this saves them $10,000 per year in combined federal/state taxes in their mid-70s and beyond.

The Break-Even Calculation:

$51,580 (Total Cost) / $10,000 (Annual Savings) = 5.2 Years

The Verdict: The Clarks will “earn back” the full cost of their conversion and IRMAA hit within 5.2 years. For the next 20+ years of their retirement, they will enjoy an extra $10,000 per year in pure tax savings. Paying the IRMAA was an incredibly profitable move.

💡 Make Confident Roth Decisions & Win the Long Game

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Master the IRMAA break-even calculation.

- → Learn when to trade a subsidy for savings.

- → Get proven RMD-avoidance strategies.

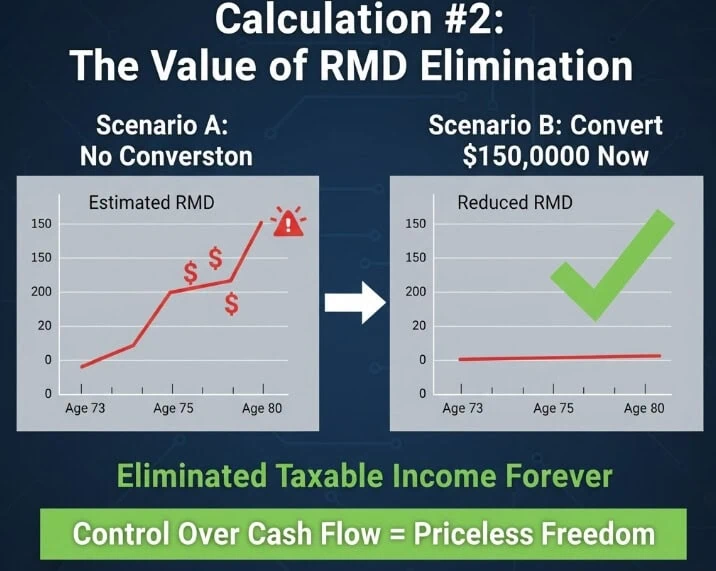

Calculation #2: The Value of RMD Elimination

This calculation is less about a single number and more about a strategic outcome. By converting funds to a Roth IRA, you are permanently removing them from the RMD calculation pool. Review the official IRS rules on RMDs and use an RMD calculator to project the following:

- Scenario A: What will my estimated RMD be at age 73, 75, and 80 if I don’t convert?

- Scenario B: What will my estimated RMD be if I do convert $150,000 now?

The difference in those RMD amounts represents the taxable income you have successfully eliminated forever.

This not only saves you on direct income tax but also gives you complete control over your cash flow in retirement, a freedom that is priceless.

Calculation #3: The Estate Planning & Legacy Value

This is where a Roth conversion becomes a powerful legacy tool.

Thanks to the SECURE Act, most non-spouse beneficiaries who inherit a Traditional IRA must withdraw all the funds (and pay all the taxes) within 10 years. This can be a massive tax burden for your children during their peak earning years.

📘 Client Story: The Widow’s Inheritance Dilemma

I recently worked with a 67-year-old widow, Maria, who had just inherited her husband’s $1.2M IRA. The 10-year rule meant she had to pull out over $100,000 a year, which would have triggered high taxes and IRMAA for a decade. Instead, we made a strategic choice. We did a massive $400,000 Roth conversion in a single year.

Yes, it triggered the highest IRMAA bracket for two years, a calculated cost of about $20,000. But in exchange, she moved a huge chunk of the IRA into a Roth. This solved her RMD problem and, more importantly to her, created a tax-free inheritance for her children. For more on these complex rules, see our guide to inherited IRA RMDs.

When your children inherit a Roth IRA, they still have to empty it within 10 years, but every single withdrawal is 100% tax-free. You are paying the tax and the temporary IRMAA surcharge so that they don’t have to.

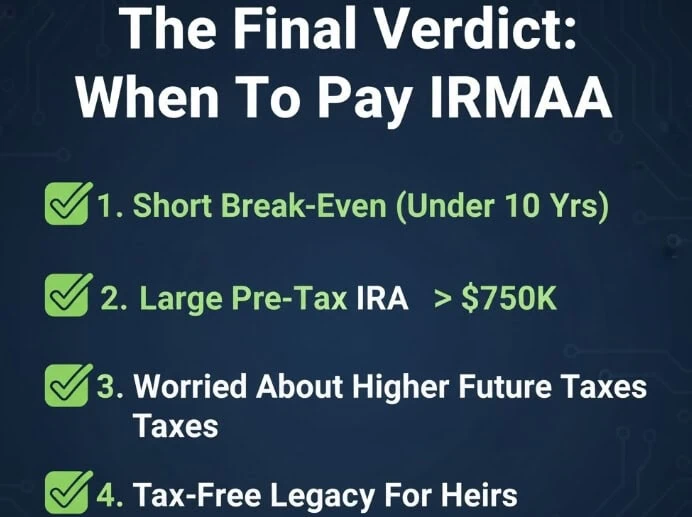

The Final Verdict: When It’s Worth Paying IRMAA

You should strongly consider a Roth conversion that triggers IRMAA when:

- Your break-even period is reasonably short (typically under 7-10 years).

- You have a large pre-tax balance that will create a significant RMD problem in the future.

- You are concerned about future tax rates being higher than they are today.

- Leaving a tax-free legacy to your heirs is a primary goal of your estate plan.

⚠️ Myth Busted

You cannot appeal an IRMAA surcharge that was caused by a voluntary Roth conversion. The SSA does not consider this a “life-changing event.” The decision to convert is a proactive financial choice, and the resulting IRMAA is considered a foreseeable consequence. This is why running the numbers beforehand is absolutely critical.

Frequently Asked Questions

What if I’m wrong and tax rates go down in the future?

This is a key risk. If tax rates are significantly lower in the future, the “tax savings” part of your break-even calculation becomes less valuable, extending the time it takes to recoup the conversion costs. However, given current government debt levels, most financial planners believe the risk of higher future taxes is greater than the risk of lower ones.

Should I use funds from my IRA to pay the conversion tax?

No, this is a major mistake. You should always use cash from a non-retirement (taxable) account to pay the taxes on a Roth conversion. Paying the tax from the IRA itself is considered a distribution, and if you are under 59.5, it could be subject to a 10% penalty.

Does this strategy work for conversions from a 401(k) as well?

Yes. The logic is identical. Whether you are converting from a Traditional IRA, a 401(k), or a SEP-IRA, the converted amount is added to your income and can trigger IRMAA. The break-even and RMD elimination calculations work exactly the same way.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.