Most people believe estate planning is about death.

That belief is the reason most estate plans fail.

Estate planning basics are not about who gets what when you die.

Estate planning basics are about who controls decisions when you can’t, which assets move without court interference, and where silence triggers outcomes you never intended.

After nearly three decades working alongside families, attorneys, and probate systems, one pattern repeats:

The common understanding of estate planning is dangerously incomplete.

Wills do not control most assets. Incapacity happens more often than death. Probate is triggered by ownership gaps, not wealth. And beneficiary designations quietly override intent every day.

Estate plans don’t fail because documents are missing.

Estate plans fail because authority, ownership, and beneficiaries were never aligned.

This article proves that claim step by step.

Key Takeaways (Actionable, Not Theoretical)

- A will controls only probate assets, often a minority of your net worth.

- Incapacity planning breaks more families than death planning.

- Probate is caused by missing instructions, not large estates.

- Beneficiary designations override wills and trusts every time.

- Guardianship decisions default to judges when parents stay silent.

If any of those statements feel surprising, your current plan is likely incomplete.

Key Takeaways Ahead

The Basics of Estate Planning: Your Foundation

Estate planning controls who decides, who receives, and how fast assets move.

Here’s what most guides miss: the court steps in whenever documents fail to speak clearly.

What “Estate Planning Basics” Actually Means

Estate planning basics refers to the legal framework that determines:

- Who makes financial decisions during incapacity

- Who makes medical decisions during incapacity

- How assets transfer at death

- Whether courts intervene

- How fast beneficiaries gain access

- Whether outcomes follow intent or statute

It is a system of authority allocation, not a document checklist.

How Estate Planning Actually Works

- Ownership structure determines transfer

- Beneficiary designations override documents

- Incapacity triggers authority gaps

- Probate fills silence with state law

Real Example:

A $900,000 retirement account bypasses a will entirely if a beneficiary exists, even if outdated. <a href=”https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-beneficiary”>IRS Retirement Plan Beneficiary Rules, 2025</a>

If incapacity happens tomorrow, who controls your checkbook?

What Families Miss at 3 A.M.: Beneficiary Overrides That Spark Estate Chaos

You’re not worried about money. You’re worried about asset delay, probate confusion, and family conflict.

In 2025, a widowed parent had a valid will. But no updated beneficiaries on retirement accounts and insurance policies.

Result: assets transferred automatically to an ex‑spouse.

Scary, right? Happens ALL THE TIME.

No lawsuit. No appeal. The paperwork won.

What Is a Nuncupative Will? Are Oral Wills Valid?

Why? Because beneficiary designations legally override wills and other testamentary documents. See the IRS on retirement account beneficiaries here:

That’s why failing to update beneficiaries after divorce, remarriage, or major life changes can completely defeat an otherwise airtight estate plan.

⚠️ Socratic Check: If incapacity happens tomorrow, who controls the checkbook?

Most families can’t answer. That silence costs $10,000–$50,000 in guardianship fees and delays. See the Power of Attorney framework that prevents it.

Actionable Fixes

Like forgetting to change your ex’s name on that old gym membership. But with millions at stake.

Review all accounts (IRAs, 401(k)s, life insurance, POD bank accounts) annually.

Use a “beneficiary review checklist” tied to tax season.

💡 Avoid Probate, Protect Assets

One proven estate strategy each week — straight from 28 years of seeing what costs families thousands.

- → Tax-smart moves that minimize estate taxes

- → Probate-avoidance tactics you can implement today

- → Red flags that derail family plans

The Michael Ryan Money C.L.E.A.R. Estate Framework™

C — Control

Who decides during incapacity?

L — Liquidity

Which assets bypass probate?

E — Execution

Which documents override others?

A — Authority

Who signs, spends, and consents?

R — Review Cycle

Updated after every life event?

⚡ The C.L.E.A.R. Check

One framework review per week — the four questions courts ask when your documents fail.

- → Control: Who decides if you can’t?

- → Liquidity: Which assets skip probate?

- → Execution: Which document wins?

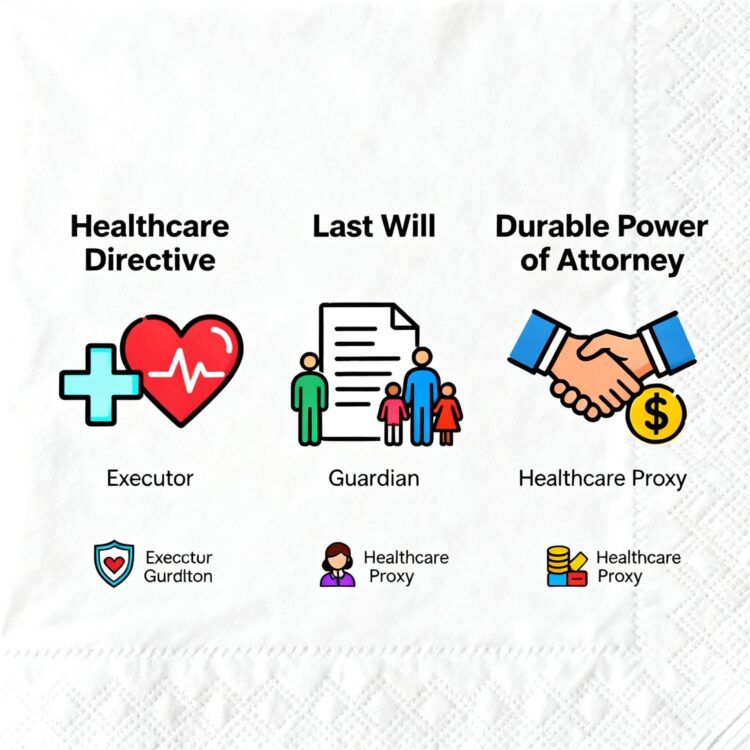

The Core Estate Planning Documents (What Each One Really Controls)

Every estate plan centers on four foundational documents: a last will and testament, durable power of attorney, healthcare proxy, and often a revocable living trust to bypass probate. <a href=”https://shoptax.wolterskluwer.com/en/practical-guide-to-estate-planning-2025.html”>American Bar Association Estate Planning Guide, 2025</a> These documents control asset distribution, medical decisions, and financial authority when you can’t act for yourself.

I wrote an article with a more in depth explanation of the documents you may need for your estate planning.

Probate: The Silent Cost Multiplier

Probate guarantees three things: public records, court delays, and statutory fees. Average probate timelines range 9–18 months, with court standards recommending 90% of cases close within 8 months but actual performance often falling short. <a href=”https://www.courts.wa.gov/caseload/content/pdf/superior/Annual/probcm.pdf”>National Probate Court Statistics, 2024</a>

In high-volume Florida counties, probate judges handle 2,780–4,419 new cases per year on average, creating significant backlogs for contested matters.

Understanding the right estate planning documents is essential for protecting your assets and wishes. This comparison guides you through five critical legal tools, from wills to healthcare directives, showing exactly when you need each one and what it costs. Make informed decisions about your financial future with this clear breakdown of benefits and expenses.

| Document Type | Do I Need It? | Key Benefits | Cost Range |

|---|---|---|---|

| Last Will and Testament | Do you want to determine where your assets go? | Allows you to determine how your assets will be distributed after death. | $100–$1,000 |

| Revocable Trust | Do you want to avoid probate? | Avoids probate and allows for more control over how assets are distributed. | $1,500–$3,000 |

| Beneficiary Designation | Do you have retirement or investment accounts? | Assets can be transferred upon death without the need for probate. | Free |

| Financial Power of Attorney | What happens if you become unable to make decisions for yourself? | Allows someone to make financial decisions on your behalf if you are unable to do so. | $100–$500 |

| Advanced Healthcare Directive | What happens if you become unable to make medical decisions for yourself? | Designates someone to make medical decisions on your behalf if you are unable to do so. | $100–$500 |

Start with a will or trust today—even one free beneficiary designation can protect your loved ones and avoid costly probate delays.

Question: Would privacy matter to surviving family members?

Probate filings are public record. Anyone can see asset values, creditor claims, and family disputes.

Estate Taxes vs Estate Chaos

Only 0.1% of estates face federal estate tax exposure in 2026, with the exemption projected at approximately $15 million per person ($30 million for married couples). <a href=”https://www.kiplinger.com/taxes/new-estate-tax-exemption-amount”>Tax Policy Center, 2025</a>

Yet 67% of Americans lack any estate plan. <a href=”https://www.caring.com/caregivers/estate-planning/wills-survey/”>Caring.com Estate Planning Survey, 2024</a>

Federal estate taxes affect very few families.

For 2026:

- Federal estate tax exemption: $15 million per individual

- Married couples: $30 million

- Tax rate above exemption: 40%

- Most estates owe zero federal estate tax

State estate or inheritance taxes may still apply.

The real danger is not taxes, it is poor execution:

The real risk isn’t tax. It’s beneficiary designation errors, outdated documents, family conflict, and probate delay eating into inheritances through legal fees and court costs.

The real risk is silence.

- Probate delays

- Liquidity shortages

- Forced asset sales

- Family disputes

- Click here to learn all about Is Your Inheritance Taxable

Here is a quick table outlining steps you can take to minimize or eliminate estate taxes:

Smart tax reduction strategies can preserve hundreds of thousands—even millions—of dollars for your beneficiaries. This breakdown compares five proven approaches, showing the cost and time commitment required alongside potential tax savings, so you can prioritize which strategies fit your situation.

| Strategy | Estimated Cost | Estimated Time | Estimated Tax Savings |

|---|---|---|---|

| 1. Review and update estate plan regularly | $0 | 1–2 hours annually | Potentially thousands to millions |

| 2. Establish trusts for beneficiaries | $3,000–$10,000+ | Several weeks to months | Potentially millions |

| 3. Utilize annual gift tax exclusion | $0 | 1–2 hours annually | Up to $19,000 per recipient in 2026 ($38,000 for married couples) |

| 4. Make charitable donations | $0–$10,000+ | 1–2 hours to several weeks | Potential tax deductions |

| 5. Purchase life insurance | Varies based on policy | Several weeks to months | Potential tax-free payout to beneficiaries |

Start with free strategies today—annual reviews and gift exclusions require minimal effort but deliver significant long-term savings. Consult a tax professional to create a comprehensive plan tailored to your estate.

Gift Taxes (Planning Tool, Not a Trap)

Gift taxes share the same lifetime exemption as estate taxes.

Key points:

- Annual exclusion gifts reduce estate size

- Gifting shifts appreciation out of the estate

- Documentation matters

- Strategy matters more than volume

This is an area where tax and legal coordination is essential.

- \Understanding Estate Taxes or Inheritance Taxes

Last Will and Testament

Controls: Probate assets at death only

A Last Will and Testament determines:

- Distribution of probate assets

- Executor appointment

- Guardian nomination for minor children

Without a will, intestate succession laws determine outcomes using rigid statutory formulas that ignore family dynamics, estrangements, blended households, and verbal promises.

American Bar Association – Intestate Succession & Probate

Critical limitation:

A will does not control retirement accounts, life insurance, or payable-on-death accounts.

This single misunderstanding causes more estate failures than any drafting error.

💡 Avoid Probate, Protect Assets

One proven estate strategy each week — straight from 28 years of seeing what costs families thousands.

- → Tax-smart moves that minimize estate taxes

- → Probate-avoidance tactics you can implement today

- → Red flags that derail family plans

Revocable Living Trust

Controls: Assets during life, incapacity, and death — if funded

- Avoids probate for titled assets

- Maintains privacy

- Allows seamless management during incapacity

- Uniform Trust Code – Uniform Law Commission

Common real-world failure:

Unfunded trusts. Assets left outside the trust still go through probate.

A trust without asset retitling is not a plan.

It is paperwork.

Durable Power of Attorney

Controls: Financial authority during incapacity

A durable power of attorney allows an appointed agent to:

- Pay bills

- Access accounts

- Manage investments

- File taxes

- Sell property

Without this document, families must seek court-appointed guardianship. A public, slow, and expensive process that strips autonomy.

In practice, incapacity almost always arrives before death.

U.S. Courts – Guardianship & Conservatorship Overview

Advance Healthcare Directive

Controls: Medical decisions and HIPAA access

An advance healthcare directive:

- Names medical decision-makers

- Documents treatment preferences

- Authorizes information sharing

Without it, hospitals follow statutory priority, not family preference or emotional closeness.

U.S. Department of Health & Human Services – HIPAA Patient Rights

Naming an Executor (Operational Reality, Not Honorific)

An executor:

- Collects assets

- Pays debts and taxes

- Manages timelines

- Distributes property

The best executor is:

- Organized

- Available

- Emotionally steady

The closest relative is often the worst choice.

Beneficiary Designations: When to Name, and When to Pause

Always name a beneficiary when:

- Speed matters

- Probate avoidance matters

- Privacy matters

Delay or redirect when:

- Assets should flow through a trust

- Beneficiaries lack maturity

- Divorce or major life transitions are ongoing

Blank beneficiary forms are silent instructions — and silence defaults to court control.

Naming a beneficiary is one of the most important decisions in estate planning, but it comes with both advantages and potential drawbacks. Understanding both sides helps you make the right choice for your financial situation and family circumstances.

| Reasons to Name a Beneficiary | Reasons Not to Name a Beneficiary |

|---|---|

| ✓Avoid Probate | ✗Concerns about privacy or control |

| ✓Ease of Asset Transfer | ✗Conflicts with estate planning |

| ✓Privacy |

Weigh these factors carefully and consult an estate planning attorney to ensure your beneficiary designations align with your overall financial and legal goals.

Controls: Most wealth transfers

Beneficiary designations govern:

- IRAs and 401(k)s

- Life insurance

- Annuities

- Many brokerage and bank accounts

Non-negotiable rule:

Beneficiary designations override wills and trusts — always.

IRS – Retirement Plan Beneficiary Rules

Outdated beneficiaries execute exactly as written, even when intent has changed.

Why Probate Happens (And Why People Misunderstand It)

Probate is not a punishment for wealth.

Probate is the legal process that fills silence.

Probate is triggered when:

- Ownership is unclear

- Beneficiaries are missing

- Authority is unassigned

Even modest estates enter probate when planning gaps exist.

Choosing between probate and probate avoidance strategies has major implications for your family’s timeline, costs, and privacy. This comparison highlights the critical differences—from distribution speed to court fees—so you can make an informed decision about the best path for your estate.

| Factor | Going Through Probate | Avoiding Probate |

|---|---|---|

| Time it Takes to Distribute | Several months | A few weeks to a few months |

| Costs Involved | Court and legal fees | Legal fees only (if any) |

| Privacy | Public record | Private, non-public record |

| Control Over Distribution | Limited | More flexibility and control |

| Possibility of Disputes | Possible | Less likely |

Most families benefit from avoiding probate entirely—consult an estate planning attorney today to set up trusts, beneficiary designations, or other strategies that protect your family’s time and money.

National Center for State Courts – Probate Overview

Guardianship: The Most Avoided, and Most Consequential, Decision

If minor children exist, guardianship planning is mandatory, not optional.

Parents must decide:

- Who raises the children

- Who manages the money

- Whether those roles are separate

- When children gain financial control

Without nominations, judges decide using statutory rules — not parental intent.

U.S. Courts – Guardianship of Minors

I have never seen a family grateful that a court made this decision for them.

Special Situations and Circumstances That Break Estate Plans

A basic estate plan handles ordinary scenarios.

Real estate failures happen in edge cases — incapacity, dependent children, taxes, probate friction, and outdated beneficiary structures.

These situations are where plans either function smoothly… or collapse under pressure.

Planning for Incapacity (The Most Common Failure Point)

Incapacity rarely announces itself.

It arrives through stroke, accident, illness, or cognitive decline — often years before death.

When incapacity occurs, the question is not what you intended, but who has legal authority.

Without preparation:

- Financial decisions default to court-appointed guardians

- Medical decisions default to statutory priority

- Access to accounts can freeze instantly

A functioning incapacity plan requires:

- A durable power of attorney for financial authority

- An advance healthcare directive for medical authority

These documents prevent court involvement and preserve autonomy when decision-making ability disappears.

Learn more about protecting your family with Disability Insurance here.

Advance Healthcare Directive (Medical Authority, Not Just Preferences)

An advance healthcare directive is not about end-of-life ideology.

It is about decision control under stress.

It determines:

- Who speaks to doctors

- Who consents to treatment

- Who accesses medical records

- How conflicts between family members are resolved

Think of it as insurance against medical chaos, not a statement of wishes.

Without one:

- Hospitals follow statutory decision hierarchies

- Family disputes escalate quickly

- Courts intervene when disagreements arise

What Happens If You Can’t Make Decisions

If incapacity occurs without proper documents:

- A court appoints a guardian

- Proceedings are public

- Authority is delayed

- Costs escalate

- Control is lost

This is not hypothetical.

It is routine.

I’ve seen families referred only after a spouse became incapacitated — when options were already limited and expensive.

Planning beforehand preserves dignity.

Planning afterward limits damage.

Providing for Dependent Children

If you have dependent children, guardianship planning is mandatory, not optional.

Parents must decide:

- Who raises the children

- Who controls finances

- Whether those roles should be separate

- When children receive full access to assets

Without explicit nominations:

- Judges decide custody

- Statutory rules override parental intent

- Emotional and financial strain increases

A well-structured plan often includes:

- Guardian nominations in a will

- A trust to manage funds for children

- Distribution schedules beyond age 18

Review and Update When Life Changes

Estate plans degrade over time.

Triggers that require review:

- Marriage or divorce

- Birth or adoption of a child

- Death of a beneficiary or fiduciary

- Significant asset changes

- Relocation to a new state

Annual reviews prevent silent failures.

This is not a full rewrite exercise — it is a verification process:

- Beneficiaries

- Fiduciaries

- Titles

- Authority documents

Distributing Assets According to Your Wishes

Asset distribution fails when:

- Ownership conflicts with intent

- Beneficiaries are outdated

- Probate is triggered unnecessarily

A proper distribution strategy starts with:

- Full asset inventory

- Ownership review

- Beneficiary verification

- Trust alignment (if applicable)

Outright distributions are simple.

Trust-based distributions provide control.

The correct approach depends on:

- Family dynamics

- Maturity of beneficiaries

- Tax exposure

- Creditor risk

Probate Process and Probate Court (Why Silence Is Expensive)

Probate is the legal system filling gaps you left behind.

It involves:

- Validating a will (if one exists)

- Identifying assets

- Paying debts and taxes

- Distributing property

Probate is:

- Slow

- Public

- Expensive

- Emotionally draining

Avoidance strategies include:

- Properly funded trusts

- Beneficiary designations

- Transfer-on-death registrations

- Joint ownership (used carefully)

Intestate: When the State Writes Your Plan

Dying without a will means:

- State law controls distribution

- Guardianship decisions default to courts

- Family intent becomes irrelevant

Everyone has a will.

Some people just let the state write it.

Assets and Property Distribution of an Inheritance

Once legal authority is established, assets must be transferred efficiently.

Common friction points:

- Frozen accounts

- Outdated beneficiaries

- Probate delays

- Tax misunderstandings

Proper planning eliminates most delays.

Transfer on Death (TOD): The Easiest Win Most People Miss

Transfer on Death designations allow assets to bypass probate.

Common TOD-eligible assets:

- Bank accounts

- Brokerage accounts (non-retirement)

Despite simplicity, TODs are often:

- Not offered

- Not explained

- Not completed

This omission alone causes thousands in unnecessary legal costs.

Retirement Accounts and Insurance Policies

These assets pass by beneficiary designation — not by will.

Common failure:

- Beneficiaries never updated

- Ex-spouses unintentionally inherit

- Large distributions trigger tax or Medicare issues for survivors

Beneficiary review is not optional maintenance.

Real Estate Considerations

Real estate passes:

- By title

- By trust

- Or through probate

Ownership structure determines:

- Speed of transfer

- Tax treatment

- Court involvement

Title review is as important as document review.

💡 Avoid Probate, Protect Assets

One proven estate strategy each week — straight from 28 years of seeing what costs families thousands.

- → Tax-smart moves that minimize estate taxes

- → Probate-avoidance tactics you can implement today

- → Red flags that derail family plans

Cost Reality (Why “Doing Nothing” Is the Most Expensive Option)

Estate planning costs are predictable. The cost of inaction is not. The table below compares the typical out-of-pocket cost for core estate planning documents against the real-world consequences families face when those documents are missing. The pattern is consistent: modest upfront costs prevent court involvement, delays, and loss of control—especially during incapacity.

| Document | Typical Cost | Cost of Absence |

|---|---|---|

| Will | $100–$1,000 | Court-controlled distribution |

| Trust | $1,500–$3,000 | Probate delays and loss of privacy |

| Power of Attorney | $100–$500 | Guardianship proceedings |

| Healthcare Directive | $100–$500 | Statutory decision-makers |

| Beneficiary Updates | Free | Frozen accounts and misdirected assets |

The takeaway is simple: small, controllable costs today prevent irreversible outcomes tomorrow. Use this comparison to identify which missing document exposes your family to the greatest risk—and address that gap first.

The Real Failure Pattern (Observed Repeatedly)

Estate planning fails when:

- Documents exist, but authority is misaligned

- Beneficiaries contradict intent

- Incapacity is ignored

- Ownership is outdated

This is not a knowledge problem.

It is an execution problem.

Learn more about avoiding the most common estate planning mistakes people make.

💡 Avoid Probate, Protect Assets

One proven estate strategy each week — straight from 28 years of seeing what costs families thousands.

- → Tax-smart moves that minimize estate taxes

- → Probate-avoidance tactics you can implement today

- → Red flags that derail family plans

Bottom Line: Estate Planning Is About Control, Not Death

Estate planning basics succeed when:

- Authority exists before it’s needed

- Ownership matches intent

- Beneficiaries reflect reality

- Silence is eliminated

Documents don’t fail.

Silence does.

What to Do Next

If this guide exposed gaps:

- Inventory every account and title

- Verify every beneficiary designation

- Confirm incapacity authority

- Review guardianship nominations

- Align ownership with intent

Estate planning is not morbid.

It is preventive maintenance for the people you love.

If you lost capacity tomorrow, which single asset would trigger court involvement first. And who would legally control it by default?

That answer tells you where to start.

📚 Apply C.L.E.A.R. to Your Plan

- Control: Durable Power of Attorney Essentials — Who decides your finances if you can’t. (Why naming wrong agent costs families $20,000+)

- Liquidity: Beneficiary Designations Override Wills — The $900,000 retirement account rule. (How outdated forms transfer assets to ex-spouses)

- Execution: Which Document Wins? Hierarchy Explained — Why your will loses to beneficiary forms every time. (The legal pecking order courts follow)

- Review: Life Events That Trigger Probate Risk — Marriage, divorce, inheritance, new accounts. (When silence becomes expensive)

You now have the foundation: wills, trusts, beneficiary designations, powers of attorney. The 2026 estate tax exemption is $15 million per person, which means most families won’t owe federal estate tax. But state taxes, probate costs, and family drama can still destroy what you’ve built.

Estate planning isn’t something you do once. Review it annually, especially after major life events (marriage, divorce, kids, property purchases). Your 2026 plan needs to account for current tax laws, digital assets, and your state’s specific rules.

Building a solid estate plan requires a coordinated team of professionals, each bringing specialized expertise. Understanding the role of your estate attorney, tax professional, and trustee ensures your plan is legally sound, tax-efficient, and properly executed for your beneficiaries.

| Professional | Role in Estate Planning Process | Key Benefits | Examples of Work |

|---|---|---|---|

| Estate Attorney / Estate Planning Attorney | Drafting and reviewing estate plan | Ensures legally valid estate plan | Drafting a will or trust |

| Tax Professional | Tax planning | Minimizes taxes | Tax planning and inheritance tax law guidance |

| Trustee | Overseeing distribution of assets | Ensures proper distribution | Administering a trust |

Assemble your estate planning team today—coordinating with an estate attorney, tax professional, and trusted trustee creates a comprehensive strategy that protects your legacy.

FAQ – Frequently Asked Questions:

What are some examples of estate planning?

Estate planning is the process of preparing for the management and distribution of your assets upon your death or incapacity. Examples of estate planning include:

– Creating a will to distribute your assets

– Setting up a trust to manage and distribute your assets

– Designating beneficiaries for retirement accounts and life insurance policies

– Establishing durable powers of attorney for healthcare and financial matters

– Creating a living will or healthcare directive

– Planning for long-term care needs

– Gifting assets to family or charities

– Minimizing estate taxes

What are the 7 steps in the estate planning process?

The seven steps in the estate planning process are:

– Take inventory of your assets

– Determine your goals and objectives

– Consider tax implications and plan accordingly

– Choose appropriate beneficiaries, fiduciaries, and trustees

– Create and execute the necessary legal documents

– Review and update your estate plan regularly

– Communicate your estate plan with your loved ones and professional advisors

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.

We are audience supported - when you make a purchase through our site, we may earn an affiliate commission.