For nearly 30 years as a financial planner, I’ve seen one word paralyze more families than any other: probate. A recent AARP study found that the average probate process takes 18 months and can consume up to 10% of an estate’s value in fees. It’s the costly, public, and painfully slow court process that your estate can get trapped in if you only have a will.

I once had a client whose family spent two years and nearly $50,000 settling his estate. A simple living trust would have settled it in weeks.

Too many people fall for the myth that trusts are only for the ultra-wealthy. That’s dangerously wrong. For most families with a home and some retirement savings, a trust isn’t a luxury; it’s a necessity.

This guide will cut through the legal jargon and show you, in plain English, how to use a trust to protect your legacy, especially in light of the massive 2025/2026 tax law changes.

🔥 Your Trust Firewall: Key Takeaways

- Dodge the Probate Nightmare: A trust is the single best tool to bypass the public, expensive, and time-consuming court process of probate, potentially saving your family 3-8% of your estate’s value.

- Control Your Legacy from the Grave: A trust allows you to dictate who gets what, when, and under what conditions, protecting inheritances from creditors, lawsuits, or a beneficiary’s poor judgment.

- The OBBBA Shake-Up is Here: The 2025 tax law made the $15 million federal estate tax exemption permanent (indexed for inflation), but state estate taxes and asset protection make trusts more critical than ever.

- A Trust is Not a Document, It’s a Process: A trust is useless unless you “fund” it by retitling your assets. I’ve seen 70% of DIY trusts fail at this critical step.

Key Takeaways Ahead

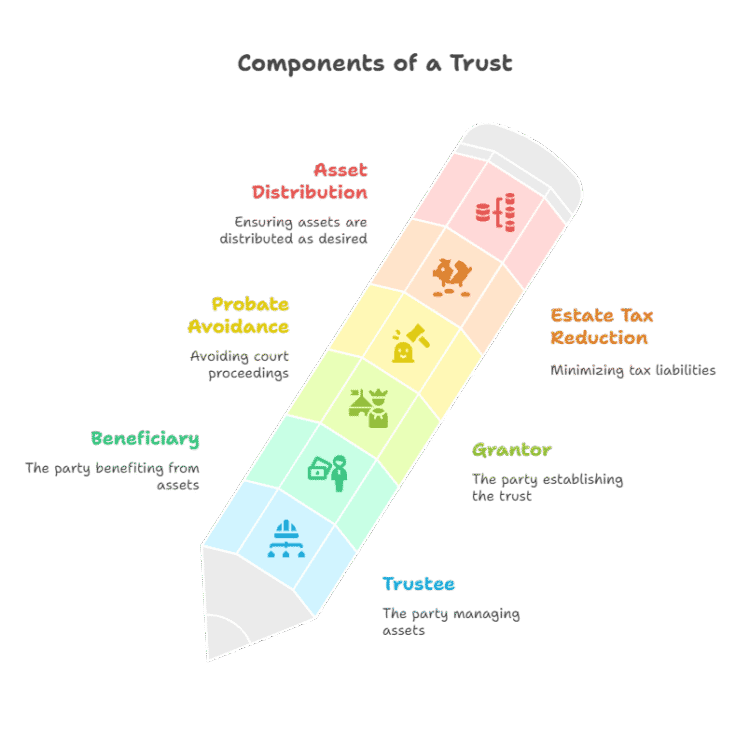

What is a Trust, Really?

A trust serves as a powerful tool in comprehensive estate planning, allowing you to establish a structured plan for asset management and distribution.

A trust is simply a legal arrangement that holds assets on behalf of your beneficiaries. Think of it as a special, protective box with its own rulebook, written by you. According to the Internal Revenue Service official trust guidance, a trust is a relationship where one person (the trustee) holds title to property for the benefit of another (the beneficiary).

💡 Advisor Tip:

Don’t let trust complexity paralyze you. In my 30 years of practice, I’ve found that for over 80% of families benefit from starting with a simple revocable living trust, then adding complexity only when needed.

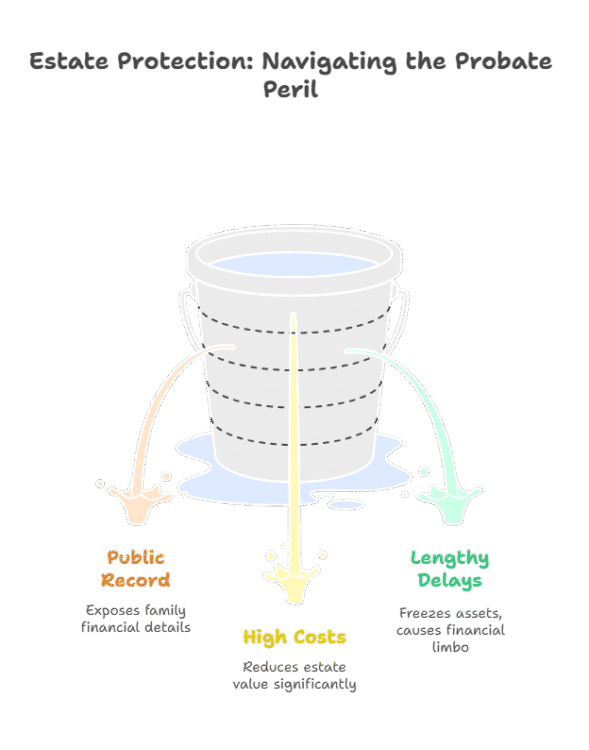

The #1 Threat to Your Estate: The Probate Trap

When I sit down with new clients, they’re often focused on taxes. But for most families, the bigger, more immediate threat is probate. Here’s why you want to avoid it at all costs:

Probate is a Public Spectacle:

A will is a public document. In states like California, that means anyone can see a complete list of what you owned, who you owed, and who got what.

Do you want your family’s finances laid bare for nosy neighbors or opportunistic predators?

Trusts offer a higher level of privacy compared to a traditional will and testament, as trust details remain confidential. Assets held in a trust generally bypass probate, unlike assets distributed through traditional wills or nuncupative wills.

Probating an Estate is Shockingly Expensive:

While the national average for fees is 3-8% of an estate’s value, some states are far worse. Under the California Probate Code, statutory fees for a $1 million estate are a non-negotiable $46,000 for the attorney and executor—a nearly 5% hit before any extraordinary fees are even considered.

On a $1 million estate, that’s a guaranteed cost that a trust avoids.

🚀 Next Steps:

Calculate your potential probate savings using our trust cost-benefit analysis. Many families save $15,000-$50,000 in probate fees alone, making trust setup costs a smart investment.

Probate Process is Painfully Slow:

The probate process can drag on for months, or even years, freezing your assets and leaving your family in financial limbo while they grieve.

- By creating a properly constructed trust, you can potentially reduce estate taxes and avoid the costly probate process that can delay inheritance for months.

- Certain types of trusts can provide tax benefits, such as reducing estate taxes and minimizing inheritance tax implications in certain states.

- The National Association of Personal Financial Advisors offers additional insights on probate avoidance strategies through proper trust implementation.

Choosing Your Trust: A Goal-Based Playbook

Instead of getting lost in a list of 15 trust types, let’s focus on your goal. In my experience, most needs fall into one of three categories.

🎯 Which Trust is Right for Your Specific Situation?

Click Here to See Which Trust is Right for You 👆

Goal 1: Avoid Probate & Maintain Control (For Most Families)

Your Weapon: Revocable Living Trust. This is the workhorse of modern estate planning. You create it during your lifetime, you control it as the trustee, and you can change or cancel it anytime. Upon your death, your chosen successor trustee steps in and distributes the assets according to your rules—no probate court required.

💡 Perfect For: Families with $300K+ in assets who want flexibility and probate avoidance without giving up control.

Goal 2: Minimize Estate Taxes & Protect Assets (For Entrepreneurs and High Net Worth Families)

Your Weapon: Irrevocable Trust. Once you create this trust and transfer assets into it, you generally cannot change it. The trade-off for this loss of control is immense: the assets are no longer legally yours, removing them from your taxable estate and shielding them from future creditors.

For entrepreneurs like my client Alex, an Irrevocable Life Insurance Trust (ILIT) is a powerful tool to provide tax-free liquidity to keep a business in the family without having to sell assets to pay estate taxes.

💡 Perfect For: Business owners, professionals at risk of lawsuits, or families with estates over $13.61 million (2024 exemption limit).

Goal 3: Protect Vulnerable Beneficiaries

Your Weapons: Special Needs Trust (SNT) & Spendthrift Trust. For a retiree like my client Margaret, a Special Needs Trust was the answer to protect her grandchild’s inheritance without disqualifying him from crucial government benefits like Medicaid.

For beneficiaries who are irresponsible with money, a Spendthrift Trust allows your trustee to manage their inheritance for them, protecting the principal from bad decisions or creditors.

💡 Perfect For: Families with disabled beneficiaries or adult children who struggle with financial responsibility.

Goal 4: Blended Families & Marital Protection

Your Weapon: Qualified Terminable Interest Property (QTIP) Trust. A trap I’ve seen many times in second marriages is a new spouse inheriting everything, unintentionally disinheriting the children from the first marriage.

A QTIP trust solves this by providing income and support for the surviving spouse for their lifetime, with the remaining assets passing to the original children upon the surviving spouse’s death. It’s a bulletproof way to ensure everyone is cared for according to your wishes.

💡 Perfect For: Second marriages where you want to provide for your current spouse while ensuring your children from a previous relationship receive their inheritance.

Goal 5: Leave a Charitable Legacy While Saving Taxes

Your Weapon: Charitable Remainder Trust (CRT). This sophisticated strategy allows you to donate appreciated assets to charity while receiving income for life and significant tax deductions. You avoid capital gains taxes on the donated assets and reduce your estate tax burden.

💡 Perfect For: Philanthropically minded individuals with highly appreciated assets like stock or real estate who want to diversify while supporting their favorite causes.

⚠️ Decision Framework: Start with your primary goal, then consider your asset level, family situation, and risk tolerance. Most families benefit from beginning with a revocable living trust and adding complexity only when needed.

🚀 Ready to Take Action on Your Trust Strategy?

Now that you understand which trust aligns with your goals, don’t let analysis paralysis cost your family thousands in unnecessary taxes and probate fees. The most expensive mistake I see families make is waiting too long to implement their estate plan.

Your Next Steps:

- Calculate your estate value including life insurance, retirement accounts, and real estate

- Identify your primary goal from the five scenarios above

- Schedule a consultation with an estate planning attorney who specializes in your trust type

- Begin the trust funding process within 60 days of creation to ensure effectiveness

Remember: A trust without proper funding is like a safe without the combination—it provides zero protection when you need it most.

The SEC’s guidance on charitable remainder trusts provides additional regulatory perspective on these complex arrangements.

💡 Get Smarter About Estate Planning Trusts

Receive one clear, actionable money move each week—designed to help you:

- Sidestep costly tax traps & penalties

- Save thousands in probate fees & estate taxes

- Apply proven estate planning playbooks in minutes

✅ Join thousands of readers already protecting their wealth.

📬 No spam. Unsubscribe anytime.

The OBBBA Shake-Up: Tax Planning in 2026 & Beyond

The tax landscape for estates has permanently shifted. The Opportunity for Business and Border Adjustment Act (OBBBA) of 2025 made the federal estate tax exemption permanent at $15 million per person, indexed for inflation.

For high-net-worth families, advanced strategies remain crucial:

Beyond the exemption increase, OBBBA preserved three critical wealth transfer tools:

- (1) the step-up in basis at death, allowing heirs to inherit appreciated assets without capital gains tax on prior appreciation;

- (2) the 2026 annual gift tax exclusion rises to $19,000 per recipient (up from $18,000 in 2025), enabling families to transfer $76,000 annually to each child without touching their lifetime exemption; and

- (3) the Qualified Opportunity Zone program became permanent with new provisions effective January 1, 2027, offering continued tax-deferred growth for strategic real estate and business investments.

Critical Planning Note:

Even if your estate falls below the $15 million threshold, an estate tax return (Form 706) must be filed to elect portability of the unused exemption to a surviving spouse. Many families miss this filing deadline—which is 9 months after death—permanently losing millions in unused exemption that could have protected the surviving spouse’s estate.

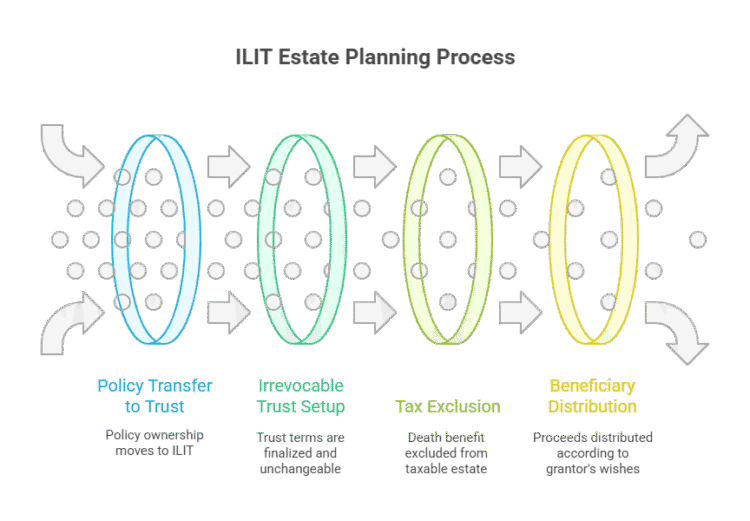

Irrevocable Life Insurance Trust (ILIT):

Removes life insurance proceeds from your taxable estate.

But for an ILIT to work, your beneficiaries must be notified of their right to withdraw contributions each year via a legal notice known as a “Crummey letter.” This small, technical step is essential for qualifying for the annual gift tax exclusion and is a detail many DIY plans miss.

A $2 million life insurance policy properly structured within an Irrevocable Life Insurance Trust (ILIT) can save a family $800,000 in federal estate taxes at the current 40% maximum tax rate, since the death benefit remains outside the taxable estate when the trust owns the policy.

⚠️ Myth Busted:

“Irrevocable trusts can never be changed” – While generally true, many states now allow trust modifications through decanting, judicial modifications, or beneficiary agreements under specific circumstances.

Grantor Retained Annuity Trust (GRAT):

An excellent tool for entrepreneurs like Alex to transfer appreciating as

Real Dollar Impact:

Consider a startup founder with $15 million in pre-IPO equity. If they hold the asset until death and it grows to $60 million, their heirs face a $24 million estate tax (40% on $45 million above the $15M exemption).

However, if they gift that $15 million asset today into an irrevocable trust via a GRAT, the asset grows tax-free outside their estate, saving the family $45 million in estate taxes. The full appreciation escapes taxation entirely while preserving the full $15 million exemption for other assets (like startup equity) to heirs with minimal or zero gift tax.

Additionally, understanding A/B trust structures can be crucial for optimizing tax efficiency and protecting your loved ones.

Use our interactive calculator to estimate setup costs and long-term savings for different trust types based on your estate value and state of residence.

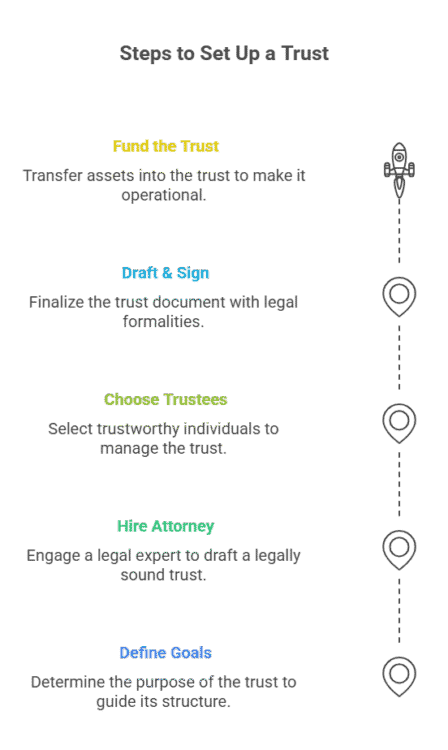

How to Set Up a Trust: The 5-Step Velocity Plan

- Define Your Goals: Are you dodging probate, slashing taxes, or protecting heirs? Your goal dictates your trust type.

- Hire a Qualified Estate Planning Attorney: This is not a DIY job. A qualified attorney will draft a trust that is legally sound and tailored to your state’s laws. Expect to invest $3,000 to $8,000 for a comprehensive plan.

- Choose Your Trustee and Successor Trustee: You can be the trustee of your own living trust, but you must name a successor. Choose someone organized, trustworthy, and impartial.

- Draft and Sign the Trust Document: Your attorney will create the legal document. You will need to sign it in front of a notary. The trust document becomes one of your essential estate planning documents that guides asset management and distribution.

- Fund the Trust (The Most Critical Step): A trust is an empty box until you fill it. You must retitle your assets (real estate deeds, non-retirement investment accounts, bank accounts) into the name of the trust.

Beyond the Binder: The Living, Breathing Trust

Creating the trust document is step one. The real work is in the ongoing administration. Contrary to popular belief, trust isn’t a “set it and forget it” tool; it’s a living entity that needs to be managed correctly to work when you need it most.

Understanding fiduciary responsibilities and duties is crucial for trustees managing trust assets effectively.

Annual Reviews are Non-Negotiable

I recommend my clients review their trust annually with their attorney or financial planner. Why? Life changes.

A divorce, a new grandchild, a significant change in asset value. All of these events can impact your estate plan. An annual review ensures your trust document, asset funding, and beneficiary designations remain perfectly aligned with your wishes.

💡 Get Smarter About Estate Planning Trusts

Receive one clear, actionable money move each week—designed to help you:

- Sidestep costly tax traps & penalties

- Save thousands in probate fees & estate taxes

- Apply proven estate planning playbooks in minutes

✅ Join thousands of readers already protecting their wealth.

📬 No spam. Unsubscribe anytime.

Trust vs. LLC for Asset Protection

A common question I get from business owners like “Alex” is whether they need a trust or an LLC for asset protection. The answer is often both. An LLC protects your personal assets from business liabilities, while an irrevocable trust can protect your business ownership (your shares in the LLC) from personal creditors.

This two-part structure creates a powerful asset protection firewall.

📚 Related Reading to Go Deeper

- Understand the full cost of setting up a trust – Get a detailed breakdown of attorney fees and what to expect.

- Find out if your inheritance will be taxed – Learn the difference between estate tax and inheritance tax.

- Explore the rules for a Special Needs Trust – Get answers to the most common questions about protecting a disabled loved one.

For comprehensive financial protection, consider reviewing your insurance coverage options alongside your trust planning strategy.

💡 Critical Timing: Special needs trusts must be established before the beneficiary turns 65 to qualify for certain Medicaid benefits. Don’t wait—early planning prevents costly mistakes.

FAQs About Trusts

What is the main disadvantage of a trust?

For a revocable living trust, the main disadvantages are the upfront cost and the administrative work of funding it. For an irrevocable trust, it’s the loss of control over the assets you place into it.

At what net worth should you get a trust?

There’s no magic number. If your goal is avoiding probate, a trust can be beneficial even for modest estates, especially in high-fee states like California. For tax planning, you should start the conversation as your net worth approaches your state’s exemption limit or half of the federal limit.

Does a trust protect assets from a nursing home?

A revocable living trust offers no protection from Medicaid or nursing home costs. An irrevocable trust can offer this protection, but only if the assets were transferred into it at least five years before applying for Medicaid, due to the federal Medicaid five-year “look-back” rule.

Next Steps: Your Legacy Awaits

Incorporating a trust into your estate plan is one of the most profound acts of financial care you can take for your loved ones. It replaces courtrooms with clarity, taxes with legacy, and chaos with control. Now that you understand the possibilities, take the next step and consult with a qualified professional to design a plan that protects everything you’ve worked so hard to build.

- U.S. Department of Justice – Resource Center: The Department of Justice offers a comprehensive resource center on trust-related topics, including asset protection.

- National Association of Estate Planners & Councils – Tax-Efficient Trusts: The NAEPC offers resources on tax-efficient trusts and strategies to minimize tax burdens in estate planning. ()

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.