Just last fall in October 2024, a client I’ll call ‘Grieving Grace’ sat in my office, completely overwhelmed. Her mother had passed, leaving her a modest estate worth about $2 million.

And she was terrified she’d lose 40% of it to the ‘death tax’ she’d heard about on the news.

Like most, Grace was unsure how inheritance and Estate taxes work. Or how they would affect her.

My take? The federal estate tax is a ghost. It haunts the headlines, but for 99.9% of Americans, it’s not real. The real tax threat is the one nobody talks about until it’s too late: capital gains tax on a poorly managed inheritance.

Instead of facing a tax cliff where exemptions would be cut in half, wealthy families now have even higher permanent exemptions. The $15 million threshold represents a 7.2% increase from 2025 levels.

Key Takeaways Ahead

Inheritance Tax vs. Estate Tax: Michael Ryan Money “Pizza” Analogy

First, let’s clear up the biggest point of confusion. While often used interchangeably, these are two completely different taxes.

- Estate Tax:

A tax levied on the total value of a deceased person’s estate before assets are distributed to heirs. This is paid by the estate itself. - Inheritance Tax:

A tax levied on the assets received by a beneficiary. This tax is paid by the heir.

🔍 Explained Simply

Imagine your late uncle’s estate is a pizza. The estate tax is a slice the government takes from the whole pizza before anyone else gets a piece. The inheritance tax is a smaller bite the government takes out of your individual slice after you’ve received it.

The Federal Estate Tax: A Tax on the Ultra-Wealthy

The United States does not have a federal inheritance tax. The federal government does, however, impose an estate tax. Which only applies to the wealthiest of estates.

For 2025, the federal estate tax exemption is a historic $13.99 million per individual. And as I mentioned earlier, will climb further to $15mm in 2026.

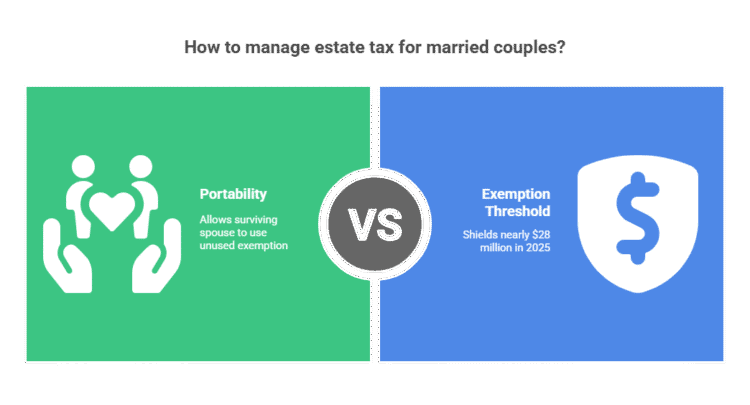

A married couple in 2025 can shield nearly $28 million. If the total value of your loved one’s estate is below this massive threshold, no federal estate tax is due.

The estate’s executor files Form 706 to calculate this tax if necessary. A key strategy for married couples is “portability,” which allows a surviving spouse to use any of the deceased spouse’s unused exemption.

State-Level Inheritance and Estate Taxes in 2025

This is where geography becomes critical. A handful of states impose their own “death taxes,” and their rules vary dramatically.

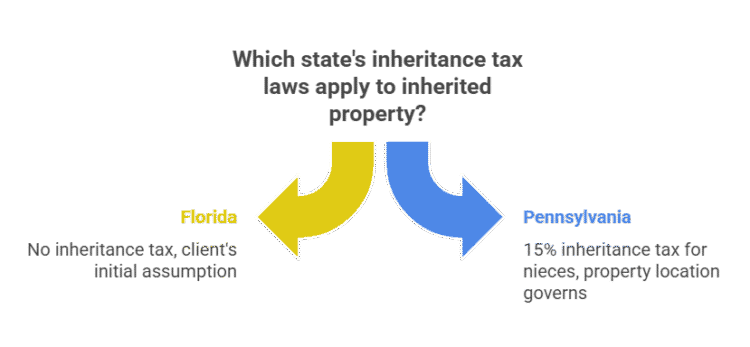

I had a client in 2024 who lived in Florida but inherited property from her aunt in Pennsylvania. She assumed Florida’s no-tax rules applied. Her estate attorney and I had to explain that for real estate, the law of the state where the property is located governs.

That conversation about Pennsylvania’s 15% inheritance tax for nieces was a tough one.

States With an Inheritance Tax

As of 2025, only five states levy an inheritance tax on the beneficiary. You can learn more about state specific rules, such as Texas inheritance laws here Your tax rate typically depends on your relationship to the deceased.

| State | Who Pays Tax (Non-Exempt Heirs) | Tax Rate Range |

|---|---|---|

| Kentucky | Nieces, nephews, friends, etc. | 4% – 16% |

| Maryland | Most heirs (siblings, children, parents are exempt) | 10% |

| Nebraska | Most relatives (spouses exempt) | 1% – 15% |

| New Jersey | Siblings, in-laws (spouses, children, parents are exempt) | 11% – 16% |

| Pennsylvania | Siblings and other heirs (spouses, children under 21 are exempt) | 4.5% – 15% |

Data sourced from the Tax Foundation. Note: Iowa repealed its inheritance tax for deaths on or after Jan 1, 2025.

States With a State Estate Tax

Twelve states and the District of Columbia impose their own estate tax on the estate itself. If the deceased lived in one of these states, the estate may owe taxes even if it’s below the federal exemption.

For example, in Massachusetts, the exemption is only $2 million.

Capital Gains Tax: The Real Tax Trap for Most Heirs

For 99% of beneficiaries, the most important tax concept is not the estate tax, but the capital gains tax. This tax only comes into play when you sell an inherited asset.

And luckily, you get a massive tax break called the “stepped-up basis.”

I’ll never forget a client Nancy, who inherited her mother’s home in 2024. The condo was purchased for $50k in the late 80s and was worth $400k when her mother passed. Grace was terrified she’d owe capital gains on all $350k of the appreciation.

I showed her how the ‘stepped-up basis’ reset her cost to the $400k date-of-death value. She sold it for $405k and only had to pay tax on a mere $5,000 gain. This one rule saved her over $50,000 in taxes.

⚠️ The Tax Time Bomb: Inherited IRAs and 401(k)s

This tax gift has a secret, nasty exception: inherited pre-tax retirement accounts. Assets like a Traditional IRA are considered “Income in Respect of a Decedent” (IRD) and do not get a step-up in basis. Beneficiaries see a $500,000 account balance, not realizing that every dollar they withdraw will be taxed as ordinary income, potentially pushing them into a higher tax bracket.

Strategies to Minimize Estate and Inheritance Taxes

For those with estates approaching the exemption limits (“Planner Pete”), several key strategies exist. As attorney Min Hwan Ahn advises, “Strategies such as lifetime gifts, trusts, estate tax exemptions, and credits can help reduce or even eliminate estate taxes.” Additionally, it is crucial to regularly review and update estate plans to adapt to changing laws and financial situations. Utilizing strategies for effective tax planning, such as taking advantage of charitable deductions or creating family limited partnerships, can further enhance the benefits of estate planning.

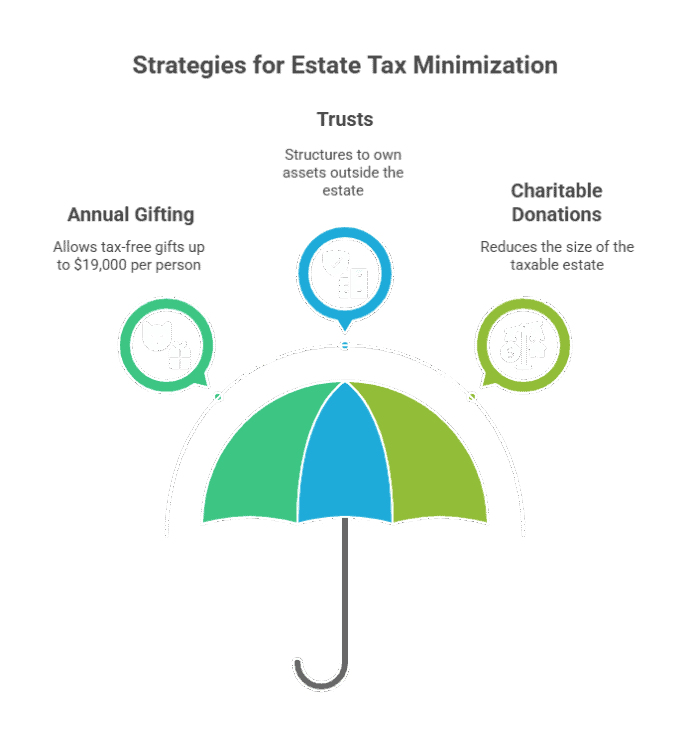

- Annual Gifting:

In 2025, you can gift up to $19,000 per person per year without any tax consequences. A married couple can jointly gift $38,000. - Setting Up Trusts:

Irrevocable trusts can be structured to own assets outside of your estate, shielding them from estate taxes. - Charitable Donations:

Giving to qualified charities can reduce the size of your taxable estate.

Frequently Asked Questions About Taxes on an Inheritance

Is inherited money considered income?

No, inheritances are not considered taxable income for federal or state purposes. However, if the inherited asset itself generates income (like dividends from stock or rent from a property), that ongoing income is taxable to you.

What if the deceased lived in a different state than me?

Generally, the inheritance tax laws of the state where the deceased lived apply. However, for real estate, the laws of the state where the property is located govern. Owning a vacation home in Massachusetts could subject your estate to a process called “ancillary probate,” where that state can claim taxes on that asset.

Can you pay inheritance taxes with estate assets?

Yes, often the will specifies that any inheritance taxes should be paid from the residual assets of the estate. However, the legal responsibility ultimately falls to the beneficiary.

Your Next Steps: Navigating Your Inheritance

The estate tax is a problem for the estate. The inheritance tax is a problem for the heir.

Knowing the difference is everything. For the vast majority of Americans, the only tax you’ll need to consider is the capital gains tax if and when you sell an inherited asset. And remember, the stepped-up basis is the last, best tax loophole in America. Don’t waste it.

Feeling overwhelmed and need a clear path forward? Download our free “Beneficiary’s 5-Step Tax Checklist.” This simple guide will walk you through the key questions to ask and the documents to find to ensure you’re handling your inheritance correctly and protecting your financial well-being.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.