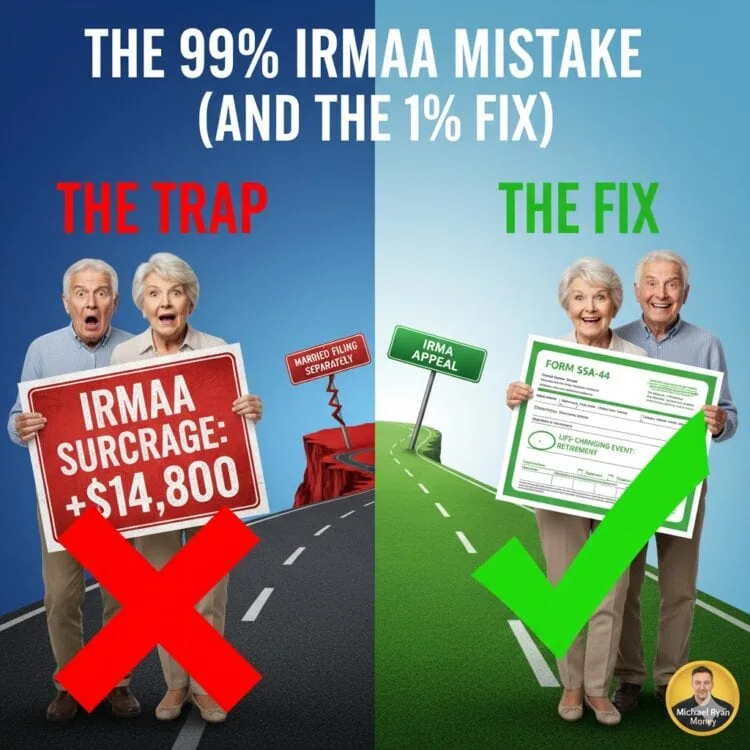

Got that shocking IRMAA determination letter? Before you do anything else, read this.

Every year, thousands of retirees see that massive Medicare premium surcharge and makehttps://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles a panic-driven, and costly, mistake. They immediately assume it’s a tax problem and turn to a seemingly clever strategy: IRMAA Married Filing Separately (MFS).

$$202.90

This is the 99% mistake. It’s an irreversible tax decision that often costs more than the penalty it’s trying to fix.

The correct solution isn’t a drastic tax change; it’s a simple administrative fix. For 99% of retirees, the answer is the “1% Fix”: a Life-Changing Event (LCE) appeal using Form SSA-44.

Here’s the difference between the 99% mistake and the 1% fix—and how to know exactly which path to take.

Key Takeaways Ahead

Before we dive into the text, you can watch the full breakdown of this costly IRMAA mistake, and the simple fix, in this video.

Now, let’s walk through the exact numbers to see how this trap snaps shut.

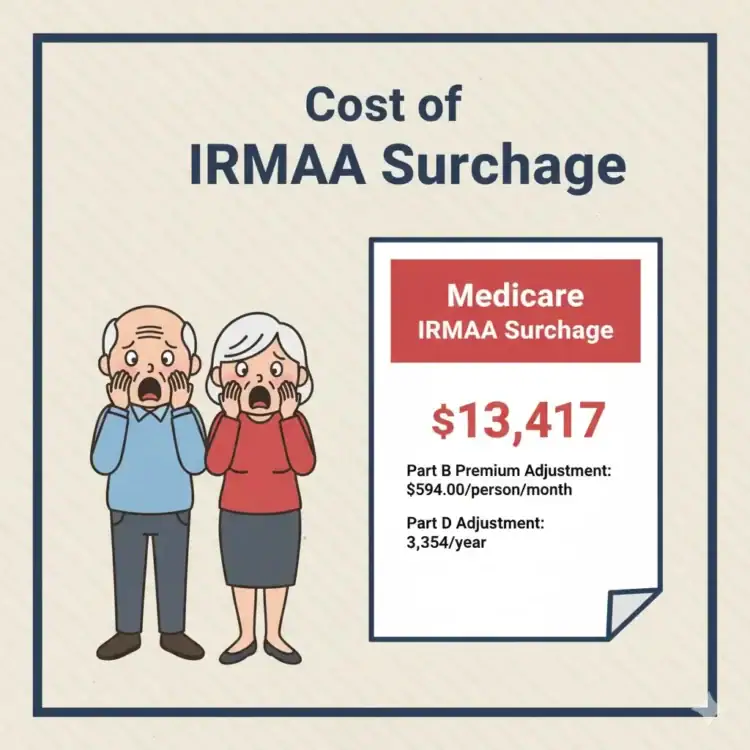

The Problem: A Sudden $15,000 Bill for Medicare

Let’s meet David and Sarah.

Two years ago, in their final year of work, their joint Modified Adjusted Gross Income (MAGI) was $700,000. David retired at the end of that year, and Sarah retired last year.

💡 Michael Ryan Money Tip

Medicare uses a 2-year “lookback” because the Social Security Administration (SSA) gets your income data from the IRS. It takes that long for the final, verified tax data to be shared. The “IRMAA Trap” is simply being charged today based on obsolete data from your peak earning years.

Now, their income has dropped to just $200,000 in retirement, sourced from pensions and IRA withdrawals.

But Medicare doesn’t look at their current income. It looks at their tax return from two years ago. Based on that $700,000 income, Social Security hits them with a determination letter placing them in the highest IRMAA bracket (Tier 6).

- Standard Part B Premium: $$202.90per person

- Their IRMAA-Adjusted Premium: $$689.90per person

- Total Monthly Surcharge (2 people): $$974.00

- Total Annual Surcharge: $$11,688.00

- Part D Surcharge (2 people): $$2,184

- Total 2026IRMAA Bill: $$13,872

They are being charged over $13,000 based on an income they no longer earn. This is the moment they fall into the trap.

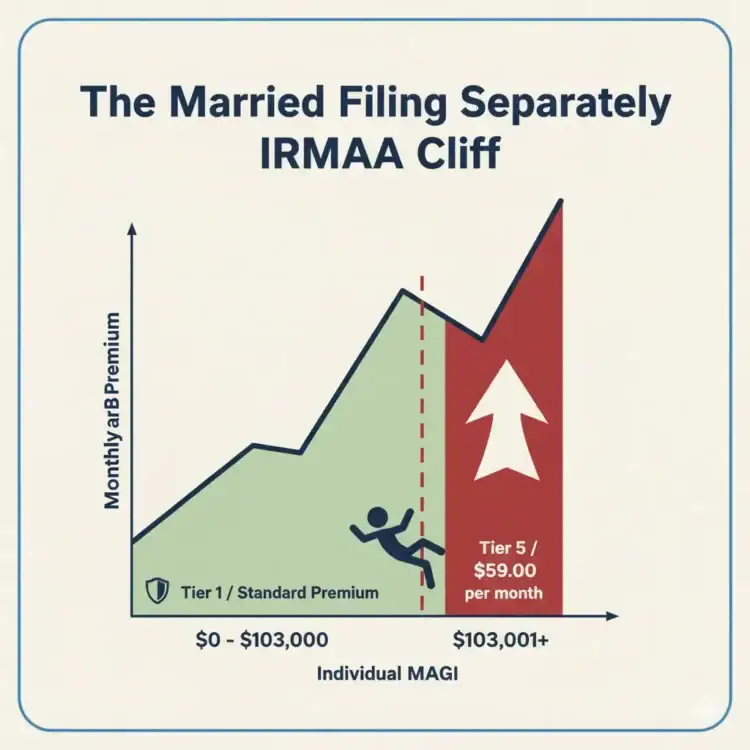

The 99% Mistake: Why ‘Married Filing Separately’ Is a Tax Trap

David does some research and finds a “clever” strategy. The IRMAA brackets for Married Filing Separately are different. If they file separately, maybe they can escape the surcharge.

Here’s the problem: he’s confusing an IRMAA Strategy with an IRMAA Appeal.

How the MFS Strategy Backfires

The MFS bracket is notoriously punitive; it’s not a gentle tier system, it’s a cliff.

- MFS Bracket 1 (Income $0 – $$109,000): You pay the standard $$202.90.

- MFS Bracket 2 (Income $$109,001++): You are immediately launched into Tier 5 ($$649.20per month).

⚠️ Myth Busted

The myth is that MFS is a “secret loophole” for high-income couples. The reality? The IRS created the MFS tax tables specifically to penalize this status, removing deductions and creating harsher tax brackets. It’s a trap, not a loophole.

The only way this strategy works is if both spouses can get their individual MAGIs below the $$109,000cliff. This is the 1% “unicorn” scenario. It almost never happens.

Let’s see what happens to David and Sarah if they try this.

- David’s MFS Income: $100,000

- Sarah’s MFS Income: $100,000

Both are just under the $$109,000limit. They successfully avoid IRMAA! They save the full $$13,872.

But they forgot one crucial thing: the tax code is designed to punish MFS.

By filing separately, they lose access to dozens of deductions and credits, such as the student loan interest deduction, education credits, and often the ability to claim the standard deduction if one spouse itemizes. Their tax bill explodes.

- Taxes as MFJ: $22,200

- Taxes as MFS: $37,000

- Extra “MFS Tax Penalty”: $14,800

The Result:

They “saved” $$13,872on IRMAA but paid an extra $14,800 in income tax. Their “strategy” resulted in a net loss of $$928.

This is the trap. They traded a temporary Medicare problem for a permanent, more expensive tax problem.

💡 AVOID COSTLY TRAPS & GET THE 1% FIX

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Actionable retirement tax alerts

- → How to navigate Medicare “gotchas”

- → Simple guides to complex forms

The 99% Fix: Filing a ‘Life-Changing Event’ Appeal (Form SSA-44)

David and Sarah’s problem was never a tax problem. It was a timing problem.

They (and 99% of retirees in this situation) don’t need a clever strategy. They just need to file a simple, one-page form: Form SSA-44, also known as a Life-Changing Event (LCE) Appeal.

🚀 Next Steps

Received a high IRMAA letter? Don’t panic or call your accountant to change your filing status. Yourfirstaction is to download Form SSA-44. Check the list of “Life-Changing Events”—if you (or your spouse) retired, that’s your ticket. This form is the only tool designed to fix this specific problem.

This form essentially lets you raise your hand and tell Social Security, “Hey, the 2-year-old tax return you’re using is obsolete. My income is lower now because of a specific, approved event.”

What Qualifies as an Appealable Life-Changing Event?

Social Security is very specific. You can’t appeal just because you had a bad year in the market. You must meet one of these qualifying criteria:

- Work Stoppage (Retirement)

- Work Reduction (Cutting back hours)

- Marriage

- Divorce or Annulment

- Death of Your Spouse

- Loss of Pension Income

- Employer Settlement Payment

David and Sarah both experienced a “Work Stoppage.” This is the most common and clear-cut reason for an appeal.

What Does NOT Qualify? (The ‘Planning Problems’)

This is just as important. You cannot appeal if your income spike was from:

- A large Roth IRA conversion

- Selling a highly appreciated stock

- High capital gains from selling a rental property

- A large, one-time bonus (that wasn’t a settlement)

These are planning problems, not appealable events.

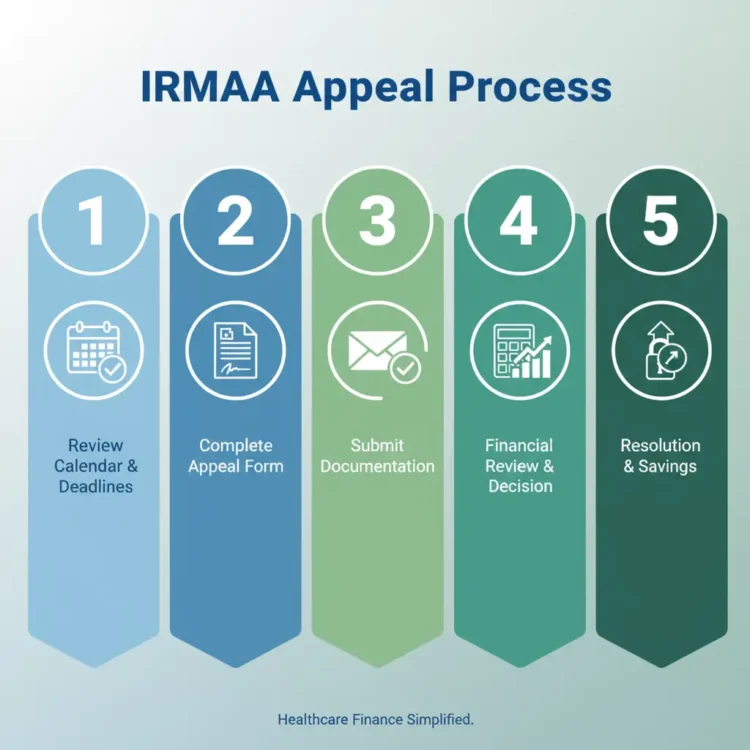

The Correct Path: A Simple 6-Step Appeal Process

Instead of changing their tax filing status, all they had to do was:

- Get their IRMAA letter.

- Download Form SSA-44 (PDF link).

- Check the “Work Stoppage” box.

- Provide proof: A retirement letter from an employer or a signed statement that they retired.

- Estimate their new, lower MAGI: They’ll state their income is now $200,000, not $700,000.

- Submit the form (following the SSA’s instructions).

Within a few weeks, Social Security will process the form, look at their new $200,000 income, and re-calculate their premium.

- New Bracket (MFJ, $200k): Tier 1

- New IRMAA-Adjusted Premium: $$202.90(the base amount)

- Total Annual Surcharge: $0

They save the entire $$13,872. And because they continue to file “Married Filing Jointly,” their tax bill remains low. They don’t pay a single dollar in MFS tax penalties.

🧠 Michael’s Take: The ‘Gotcha’ When Filing Form SSA-44

The appeal process is simple, but it isn’t magic. The #1 mistake I see? People file the SSA-44 but forget to provide proof.

Don’t just estimate your new income; prove the event. If you retired, attach a short, signed letter stating:

“I retired from [Company Name] on [Date].”

If you lost a pension, attach the letter from the pension administrator.

The SSA reviewer isn’t an investigator; they’re a processor. Make their job easy. Give them the form and the proof in one package, and your appeal will sail through. Make them hunt for info, and you’ll get a denial or a request for more information, delaying your refund by months.

💡 AVOID COSTLY TRAPS & GET THE 1% FIX

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Actionable retirement tax alerts

- → How to navigate Medicare “gotchas”

- → Simple guides to complex forms

The Final Verdict: Appeal, Don’t ‘Strategize’

Before you make an irreversible tax decision, ask yourself this one simple question:

“Is my income high today, or am I being penalized for an income that is already gone?”

📌 Key Takeaway

An IRMAA surcharge feels like a tax problem, but it’s anadministrative timing problem. Don’t use a complex tax tool (Married Filing Separately) to solve it. Use the simple administrative tool (Form SSA-44) that was literally designed to fix it.

- If your income is still high today, you may be the 1% “unicorn” who needs a complex (and risky) MFS strategy.

- But if, like the 99%, your income has already dropped due to retirement, you don’t need a strategy. You need an appeal.

Related Reading From Michael Ryan Money

- How to Avoid IRMAA Surcharges

- What Income Counts Toward Your IRMAA MAGI?

- IRMAA Brackets: A Full Guide

- A Deep Dive on the Form SSA-44 Appeal

- IRMAA Calculator

- How Do Roth Conversions Affect IRMAA?

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.