“Michael, I think I messed up. I need to know about a Roth IRA Recharacterization ASAP“

It’s a call I get every year. In March 2026, a diligent saver, let’s call her “Megan”, contacted me in a panic. She had contributed the maximum $7,500 to her Roth IRA in January, but an unexpected 2025 year-end bonus pushed her income over the MAGI limit. She was staring down a potential $420 IRS penalty (6% for excess contributions) and thought her only option was a complex withdrawal.

My answer was simple: “Don’t panic. There’s an official ‘undo button’ for this.”

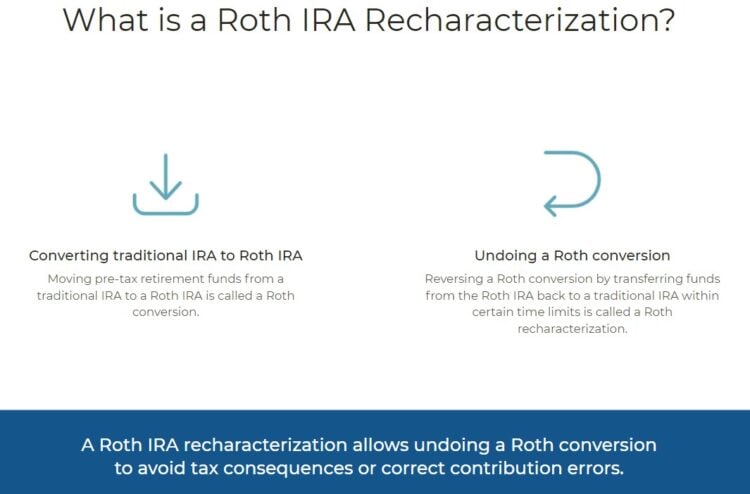

That undo button is called a Roth IRA Recharacterization. It’s a simple, penalty-free process that lets you treat your original Roth IRA contribution as if you’d made it to a Traditional IRA from the very beginning.

I’m going to walk you through exactly what a recharacterization is, when you should use it, how to do it step-by-step, and the common mistakes to avoid. I’ve been helping people fix these situations for nearly 30 years.

What You’ll Learn

What Is an IRA Recharacterization? (And Why Is It Your Best Friend After a Contribution Mistake?)

An IRA recharacterization is an IRS-approved method to redesignate a contribution from one type of IRA to another.

In plain English, you’re telling your brokerage, “Oops, I put money into my Roth IRA, but I meant to put it in my Traditional IRA instead.”

The brokerage then moves your original contribution, plus or minus any earnings or losses it generated, from the Roth to the Traditional IRA. For tax purposes, the IRS treats it as if the contribution was made to the correct account all along.

💡 Michael Ryan Money Tip

Think of it like putting the wrong type of fuel in your car. A recharacterization lets your mechanic (the brokerage) cleanly swap it for the right fuel without having to rebuild the engine (a major taxable event). It’s a simple fix for a common mistake.

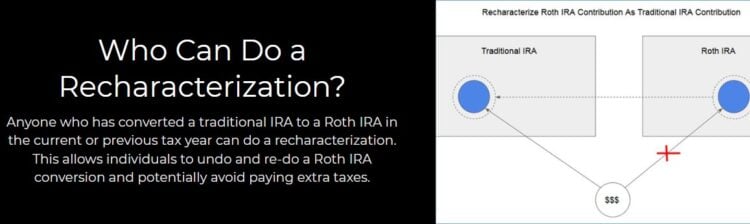

The primary reason people do this is to correct an excess contribution. If your Modified Adjusted Gross Income (MAGI) is too high to contribute to a Roth IRA, a recharacterization is your go-to tool to avoid the 6% per year penalty.

According to IRS Publication 590‑A (2026), Roth IRA contribution eligibility phases out at a modified AGI of $$168,000for single filers and $$252,000for married filers.

Traditional IRA deductibility also phases out between $81,000–$91,000 (single) or $129,000–$149,000 (married, workplace plan). These thresholds matter because exceeding them can trigger excess contribution issues. Know your numbers before recharacterizing. IRS

You can find the current Roth IRA income and contribution limits here.

Feel free to watch this quick slideshow as well for a quick rundown and explanation of IRA Recharacterizations:

Should I Recharacterize My Roth IRA Contribution? Key Scenarios

While fixing an over-contribution is the most common reason, there are other strategic times to consider using this tool.

Scenario 1: You Earned Too Much (The “Megan” Problem)

This is the classic case. Your income exceeded the MAGI limit, making your Roth IRA contribution ineligible.

- Action:

Recharacterize the contribution to a non-deductible Traditional IRA to avoid penalties.

This is often the first step in a Backdoor Roth IRA strategy.

Scenario 2: You Need a Tax Deduction

You contributed to a Roth IRA, but at tax time, you realize you need a deduction to lower your taxable income.

- Action:

If you qualify to deduct Traditional IRA contributions, you can recharacterize your Roth contribution to a Traditional IRA to get the tax break.

📘 A Planner’s War Story: Emily’s Savvy Tax Move

A client, “Emily,” contributed to her Roth IRA in early 2024. During the market decline later that year, her investment lost value. We recharacterized her Roth contribution to a Traditional IRA, which allowed her to claim a tax deduction on the full pre-loss amount. Later, she converted the smaller, post-loss amount back to a Roth, effectively paying tax on less while getting the full initial deduction—a savvy move that maximized her tax situation.

How To: Your Step-by-Step Guide to Recharacterizing an IRA Contribution

This process is surprisingly simple and is handled almost entirely by your IRA custodian (your brokerage firm).

1. Contact Your Brokerage (Before the Deadline!)

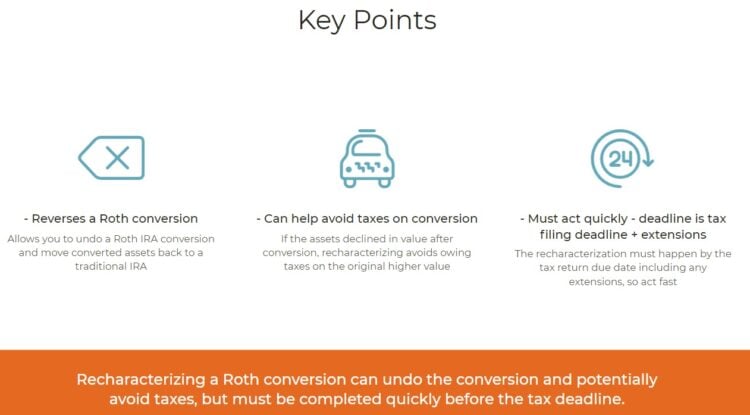

The deadline to recharacterize a prior year’s contribution is your tax filing deadline for that year, including extensions (typically October 15th).

If you miss the deadline, IRS Revenue Procedure 2000‑39 (updated via Rev. Proc. 2024‑X) allows eligible taxpayers up to 6 months post-deadline (Oct 15 for extended returns) to file a private letter ruling or EP corrective submission, amend the return, and still recharacterize. Avoiding penalties.

Call your brokerage’s customer service line.

2. State Your Intent Clearly

Use a simple script: “Hello, I need to recharacterize my Roth IRA contribution of $[Amount] for the [Year] tax year to a Traditional IRA.”

They will know exactly what you mean.

3. Let the Brokerage Handle the Math

You must move the original contribution and any associated earnings or losses, a figure known as the Net Income Attributable (NIA). Your brokerage will calculate this for you, often following the IRS’s suggested method in Notice 2000-39.

For instance: Drew put $2,600 into a Traditional IRA in December; by April, the value grew to $7,600. The gain attributable to the contribution was $150, so you’d recharacterized $2,750 (contribution + NIA).

That formula applies in full or partial recharacterizations under IRS rules.

Another Example:

If you contributed $7,000 and it lost $200, the brokerage must move exactly $6,800.

If it gained $500, they must move $7,500.

4. Report it on Your Tax Return

You do not get a specific tax form for a recharacterization, but you must report it. According to the IRS, you should attach a statement to your tax return explaining it.

You must also report the non-deductible contribution on IRS Form 8606.

Roth IRA Recharacterization vs. Roth Conversion: What’s The Difference?

This is the single biggest point of confusion. They are not the same, and the rules are completely different.

| Feature | Recharacterization | Roth Conversion |

|---|---|---|

| Purpose | To “undo” or redesignate a contribution from the current or prior year. | To move pre-tax money from a Traditional IRA/401(k) to a Roth IRA. |

| Tax Impact | Generally not a taxable event. You are just correcting a contribution. | Is a taxable event. You must pay income tax on the amount converted. |

| When to Use It | When you contribute to the wrong type of IRA or exceed income limits. | When you want to pay taxes now to get tax-free growth and withdrawals later. |

| Can it be Undone? | Yes, you can recharacterize a contribution. | NO. Since the Tax Cuts and Jobs Act of 2017, a Roth conversion is permanent and irreversible. |

⚠️ Myth Busted

You can NOT undo a Roth conversion. Prior to 2018, you could recharacterize a conversion if the market went down to avoid paying taxes on a higher value. That loophole is now permanently closed. Once you convert, the decision is final.

The IRS imposes a 6% annual excise tax on excess IRA contributions that aren’t corrected timely. This penalty repeats each year the excess amount remains in your IRA. Filing Form 5329 is required to report and remove the penalty. Don’t delay.

🧠 Michael’s Rule of Thumb: I’ve seen procrastination driven by regret-aversion prevent timely recharacterizations. And clients often pay the penalty they were trying to avoid. Treat correcting it like sending a form. Not admitting a failure.

Act within the first two weeks of tax awareness.

Roth IRA Recharacterizations Frequently Asked Questions (FAQ)

What is the deadline for an IRA recharacterization?

The deadline is your tax filing deadline for the contribution year, including extensions. For a 2025 contribution, this would typically be October 15, 2026.

Is an IRA recharacterization a taxable event?

No, the recharacterization itself is not taxable. You are simply correcting the original contribution.

Can I undo a Roth conversion?

No. This was disallowed by the Tax Cuts and Jobs Act of 2017. All Roth conversions are now permanent and irreversible.

Ready to Take Action?

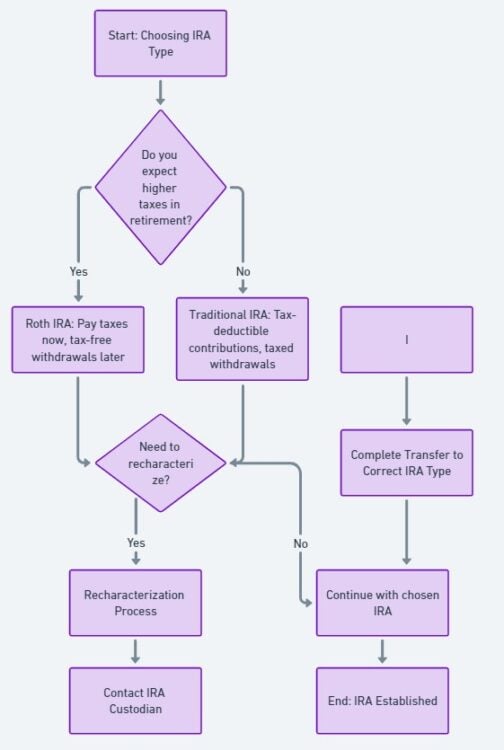

To make the process even simpler, download our Free Recharacterization Decision Checklist & Letter Template. It includes a flowchart to confirm if a recharacterization is your best move and provides a clear script to use when contacting your IRA custodian.

📝 IRA Recharacterization Decision Checklist

Purpose: Use this checklist to systematically evaluate whether IRA recharacterization is right for your situation and ensure you complete the process correctly.

Timeline: Most recharacterizations must be completed by your tax filing deadline (April 15) or extended deadline (October 15).

Key Benefit: Avoid the recurring 6% penalty on excess contributions while optimizing your tax strategy.

📂 How to Use This Checklist

- Print and Check Boxes: Use as a physical checklist to track your progress through each step

- Save for Records: Keep as documentation if you need to file late recharacterization under IRS relief provisions

- Share with Professionals: Provide to your tax advisor or financial planner for coordinated planning

- Prevention Tool: Use annually during tax planning to avoid future recharacterization needs

- Follow Sequentially: Complete steps in order—early steps inform later decisions

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.