If you are a federal retiree approaching age 65, your mailbox is likely full of Medicare flyers screaming about “permanent penalties” if you don’t sign up immediately. Throw them away.

Let’s take a look at FEHB and Medicare Part B…

As a federal retiree with FEHB (Federal Employees Health Benefits), you possess a “Golden Ticket” that most Americans do not: Creditable Coverage.

This means the standard rules of engagement do not apply to you. Because FEHB is considered creditable coverage, you have flexibility; your penalty exposure depends on whether you have current employment coverage and SEP timing. Details and exceptions below.

The real question isn’t can you delay, but should you?

Meet Dan (a CSRS Retiree) and Susan (a FERS Retiree). I’ve reviewed hundreds of federal retirement plans like theirs. I often see retirees keeping their expensive “High Option” FEHB plan and paying for Medicare Part B. They think they are being safe. In reality, they are paying two premiums for one set of benefits. Essentially donating $2,400+ a year to the government for coverage they rarely use.

Here is the contrarian math on when to take Part B, when to skip it, and the specific “FEHB Switch” strategy that can eliminate your out-of-pocket medical costs entirely.

⚡ Key Takeaways

- The Safety Net: FEHB is creditable coverage, meaning you can delay Medicare Part B without incurring the 10% lifelong penalty if you follow the Special Enrollment Period (SEP) rules correctly.

- The Waste: If you keep a High Option FEHB plan and add Part B, you are likely over-insured and wasting money.

- The Strategy: Part B only makes sense if you switch to a “Medicare-coordinated” FEHB plan that waives deductibles and copays.

- The Trap: High-income Feds (CSRS/FERS + TSP) often trigger IRMAA, making Part B significantly more expensive than the standard premium.

FEHB vs Medicare Part B: The Core Conflict

To make this decision, you must understand Coordination of Benefits. Who pays first.

- While you are still working:

- FEHB is the Primary Payer.

- Medicare is Secondary.

- Once you retire:

- Medicare Part B becomes the Primary Payer.

- FEHB becomes the Secondary Payer.

When you sign up for Part B, you agree to pay the standard monthly premium ($202.90 for 2026). (Source: CMS).

In exchange, Medicare pays 80% of your doctor/outpatient bills.

Your FEHB plan then picks up the remaining 20%.

The Problem:

Your FEHB plan already covers that 20% (minus a small copay). So, if you pay $202.90/month for Part B just to save a $25 copay at the doctor, the math doesn’t work.

You are spending dollars to save pennies.

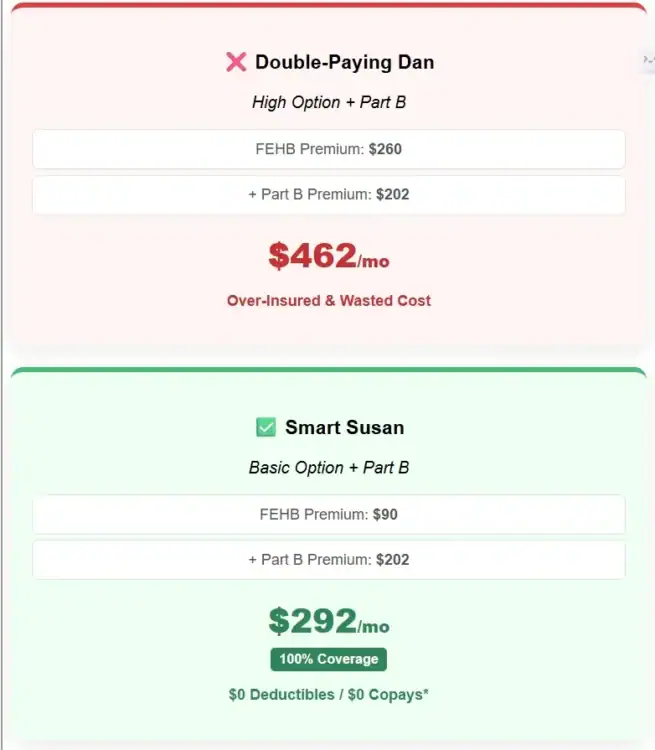

The “Double-Paying Dan” Disaster

Let’s look at a real scenario. “Dan,” a CSRS retiree, kept his Blue Cross Blue Shield (BCBS) High Option plan because “it’s the best.”

He also signed up for Medicare Part B because his neighbor told him he had to.

- FEHB Premium (High Option): ~$260/month (Dan’s share).

- Medicare Part B Premium: $202.90/month.

- Total Cost: $462.90/month.

Dan rarely goes to the doctor. The High Option plan alone would have covered him excellently.

By adding Part B without changing his FEHB plan, he added $2,434.80/year in fixed costs to his budget with almost zero tangible benefit.

When Part B is a “Gold Mine” (The Waiver Strategy)

So, why do many federal retirees eventually take Part B? Because of the Cost-Sharing Waiver.

Certain FEHB plans (typically “Basic” or “Standard” options) have a special provision in Section 9 of their brochure: If Medicare Part B is your primary payer, they waive all deductibles, copays, and coinsurance.

This turns your health coverage into a 100% coverage solution. No copays for doctors. No bills for surgeries. No deductible to meet. (Note: The Medicare Part B annual deductible of $283 for 2026 still applies, but many wrap-around FEHB plans cover this too. (Source: CMS). Check your specific brochure).

🔍 See Plan Brochure Quotes

From the BCBS Service Benefit Plan (Section 9): “We waive specified cost-sharing when Medicare Part B is primary for covered in-network services.”

Critical Note: BCBS Basic has limited out-of-network benefits compared to Standard. Always confirm network fit before switching. View 2026 Plan Brochures at OPM.gov.

The “Smart Susan” Strategy

Susan, a FERS retiree, did the math using official 2026 numbers.

- She enrolled in Medicare Part B ($202.90/mo).

- She downgraded her FEHB plan from High Option to Basic Option (saving ~$90/mo in premiums).

- The Result: Her total monthly premium went up slightly (net +$112.90), BUT she eliminated all out-of-pocket medical costs.

Because she expects knee surgery next year, this strategy saves her thousands in deductibles and coinsurance percentages.

She paid a predictable premium to eliminate unpredictable medical bills.

The IRMAA Wealth Trap: Why Feds Are Targeted

There is a massive caveat for federal employees that civilians often miss: Your pension counts as income.

Medicare Part B premiums are means-tested. This is called IRMAA (Income-Related Monthly Adjustment Amount). If your Modified Adjusted Gross Income (MAGI) from 2024 exceeds certain official 2026 thresholds ($109,000 Single / $218,000 Married), you don’t pay $202.90. (Source: Medicare.gov).

You pay more.

The Federal Retiree Trap:

Between your FERS/CSRS pension, Social Security (which is often taxable), and RMDs from your TSP, it is very easy for federal households to breach these limits. This specific income stack creates a unique IRMAA trap for federal retirees that civilian planning often misses.

If you trigger IRMAA Tier 2 or 3, your total Part B premium could jump to $405.80 or $527.50 per month per person in 2026. (Source: CMS).

Example of The Math Shift:

At $202.90/month, the “Smart Susan” strategy (Part B + FEHB Basic) works beautifully.

At $400+/month (due to IRMAA), the math collapses. It is rarely worth paying an extra $200+ per month just to waive copays. In this case, sticking with FEHB Only is almost always the superior financial move.

You can verify exactly where you fall on the 2026 IRMAA brackets to see if the premium jump makes Part B financially unviable.

📊 The “Fed-Check” Calculation

Before signing up for Part B, check your Tax Return from two years ago (Line 11). For 2026, look at your 2024 MAGI. (Source: SSA). Is it over $218,000 (Married)?

- If YES: You will likely pay an IRMAA surcharge. Calculate the total Part B cost. It likely outweighs the benefits of “wrapping” your FEHB plan.

- If NO: The standard Part B premium is likely a good value if you switch to a lower-cost FEHB plan.

See 2026 IRMAA Brackets & Premiums →

When Can You Delay? (SEP Rules)

You are not forced to make this decision at age 65 if you are still working.

- Still Working (You or Spouse):

- If you are covered by “current employment” insurance (FEHB while working), you can delay Part B without penalty.

- Retired (Annuitant):

- Once you retire, your FEHB is “retiree coverage.” You generally have an 8-month Special Enrollment Period (SEP) starting the month after employment ends to sign up for Part B without penalty. (Source: CMS).

Myth Buster: “I can sign up later if I get sick.”

Reality: Yes, but if you miss your SEP, you will pay a 10% late enrollment penalty for every 12-month period you were eligible but didn’t sign up. AND, you can only sign up during the General Enrollment Period (GEP) (Jan-March), with coverage starting the month after you sign up.

🚀 Enrollment Windows & Forms

Still working? You qualify for a Special Enrollment Period (SEP). When you eventually retire and want Part B, bring Form CMS-L564 (Request for Employment Information) to Social Security to prove you had coverage and avoid the penalty.

The FEHB vs. Medicare Decision Matrix

Use this table to find your strategy based on your health and income profile (Official 2026 Data).

Deciding between FEHB and Medicare Part B requires analyzing your specific health needs and income level. This comparison outlines the three most common federal retiree scenarios to help you determine if the cost-sharing waiver is worth the extra premium or if IRMAA surcharges make it a bad deal.

| Retiree Profile | Strategy | Why? |

|---|---|---|

| Low Usage / High Income (IRMAA) | FEHB Only | Part B premiums + IRMAA surcharges cost far more than your occasional copays. |

| High Usage / Standard Income | FEHB Basic + Part B | Paying the Part B premium ($202.90) eliminates the unpredictable 15-20% coinsurance on surgeries/therapies. |

| Snowbird / Travel Heavily | FEHB Standard + Part B | Basic plans often lack out-of-network coverage. Standard + Part B gives you nationwide access with reduced costs. |

Review your specific FEHB plan brochure (Section 9) to confirm waiver details before making a final enrollment decision.

🔀 15-Second Decision Tree

1. Do you have high income (IRMAA)?

(MAGI > $109,000 Single / $218,000 Married)

👉 YES: Keep FEHB Only. (Part B is too expensive)

👉 NO: Go to question 2.

2. Do you want 100% predictable costs?

(No copays, no coinsurance on surgery)

👉 YES: Enroll in Part B + Switch to FEHB Basic.

👉 NO: Keep FEHB Standard Only. (Pay small copays to save premiums)

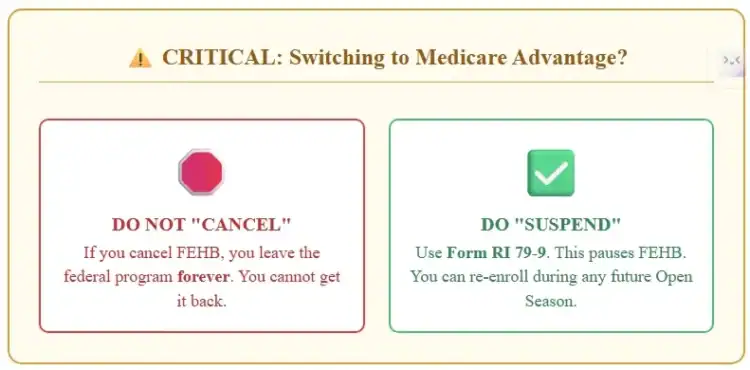

A Note on “Suspending” vs. “Canceling”

If you decide to try a Medicare Advantage plan (which some carriers offer specifically for Feds), NEVER cancel your FEHB coverage. You must SUSPEND it using form RI 79-9.

- Cancel: You leave the federal program forever. You cannot get it back.

- Suspend: You pause FEHB to use Medicare Advantage. You can re-enroll during any future Open Season.

Frequent Reader Questions About FEHB And Medicare

Is FEHB considered creditable coverage for Medicare?

Yes. FEHB plans are considered creditable coverage for both Medicare Part B and Part D. This means you can delay enrollment in Medicare past age 65 without incurring the permanent late enrollment penalty, as long as you maintain your FEHB coverage.

Does Medicare Part B replace FEHB?

No. Medicare Part B works as the primary payer, and FEHB becomes the secondary payer. You can suspend your FEHB to pay only for Medicare, or keep both. If you keep both, many FEHB plans waive deductibles and copays, providing near 100% coverage.

Should federal retirees sign up for Medicare Part B?

It depends. If you switch to a lower-cost FEHB plan that waives cost-sharing, Part B can provide comprehensive coverage for a similar total cost. However, if you are subject to high IRMAA surcharges due to your pension income, staying with FEHB-only is often the better financial decision.

The Bottom Line: FEHB and Medicare Part B

For federal retirees, Medicare Part B is not a requirement; it is a purchase decision.

Take Part B If:

- You crave 100% coverage and predictable costs.

- You switch to an FEHB plan that waives cost-sharing (e.g., BCBS Basic, GEHA Standard).

- You do not have high enough income to trigger massive IRMAA surcharges.

Skip Part B (FEHB Only) If:

- You are a high earner subject to significant IRMAA surcharges.

- You are happy with your current FEHB plan and don’t mind paying small copays.

- You want to avoid the hassle of coordinating two insurance cards.

Your Next Steps

- Check your 2024 Tax Return to forecast your 2026 IRMAA bracket. (Source: Medicare.gov).

- Download your FEHB Brochure and read Section 9. Does it waive costs?

- Run the numbers: (Part B Premium x 12) vs. (Your Annual Deductibles + Copays). If the Premium is higher, think twice.

- If you are on the edge of a tier, look into income reduction strategies to keep your MAGI below the surcharge cliff.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.