Yes, Earnin can work together with Chime. But there are critical catches.

If you’re reading this, you’re probably stressed. Maybe your transmission just blew and you need $800 by Tuesday. Or rent’s due Friday and you’re $200 short. Or you got slammed with an unexpected ER copay three days before payday. You need cash RIGHT NOW, and you’re wondering: will Earnin actually connect to your Chime account without throwing some garbage “error” message?

I’ve been a financial planner for almost 30 years. I’ve seen every version of this emergency. So I’m skipping the fluff.

Here’s the direct answer:

For most Chime users in 2026, the connection With Earnin Is unreliable and not officially supported.

Now, I’ll explain why it fails, give you a checklist to see if you have a fighting chance, and provide a crucial warning you won’t get from the app store.

Your Pre-Flight Checklist: Do This Before You Try to Connect Earnin With Chime

Don’t waste precious time on a connection that’s doomed to fail. Before you even open the Earnin app, run through this quick checklist. If you can’t say “yes” to all three, your odds of a successful connection are extremely low.

- ✅ The Single Source Rule:

Is at least 50% of your paycheck coming from a single, consistent employer via direct deposit into your Chime account?

Earnin gets confused by multiple income streams or split deposits. - ✅ The Proof of Work Test:

Do you have a fixed, physical work location or use a verifiable electronic timesheet system (like TSheets or ADP)?

Earnin needs to confirm you’re actually working the hours you claim. - ✅ The Regular Paycheck Mandate:

Is your direct deposit a regular, salaried, or hourly paycheck?

Earnin’s system is not designed for the variable payouts of most gig economy work like Uber or DoorDash.

If you didn’t pass that checklist, you can save yourself the headache and skip to the section on “Smarter Alternatives” below. If you did, you might be in the small test group that can make this work.

Key Takeaways Ahead

The Core Problem: Why Earnin and Chime Clash

So, why is this so difficult? It boils down to a fundamental conflict between Chime’s best feature and Earnin’s core requirement.

Think of it like this: Earnin is trying to tune an old FM radio to a station that’s broadcasting on a constantly shifting frequency. You might catch the signal for a second, but you’ll never get a clear song.

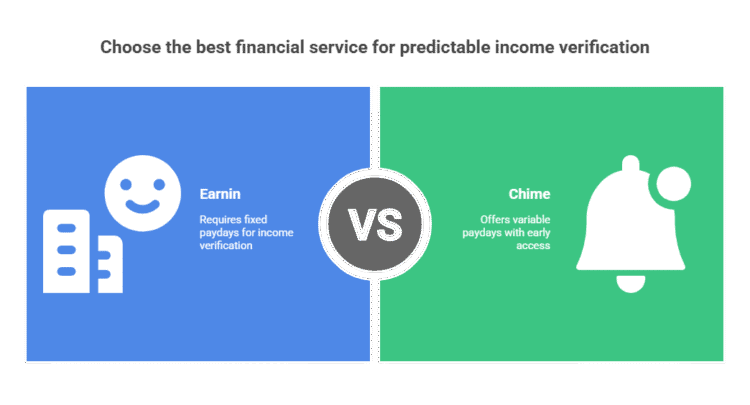

Earnin needs a fixed, predictable payday.

Its entire system is built on knowing your paycheck will arrive on the same day every pay period. This is how it verifies your income and schedules its automatic debit for repayment of a Cash Out.

Chime’s “Get Paid Early” feature creates a variable payday.

Chime gives you access to your money as soon as your employer’s bank. Which could be The Bancorp Bank, N.A. or Stride Bank, N.A. for Chime. They then send the payment file through the Federal Reserve’s ACH transfer system.

This means your “payday” could be a Tuesday one week and a Wednesday the next.

This variable schedule breaks Earnin’s predictive model.

The connection itself is handled by a third-party service called Plaid, which acts as a secure translator between the two apps. When Plaid shows Earnin your deposit history, Earnin’s system often can’t identify a fixed pattern and gives up.

This is why you get the “bank not supported” message or a connection that just spins forever, and it’s also why features like Lightning Speed often fail with Chime accounts.

A Word of Warning From Michael Ryan Money

In a true, one-time emergency, a cash advance is certainly better than a predatory payday loan with a 400% APR. But I need to be brutally honest with you:

If you find yourself needing a paycheck advance month after month, the app isn’t the solution; it’s a symptom of a cash flow problem.

Take Marcus, a 28-year-old graphic designer I worked with in spring 2025. Started with one $50 Earnin advance to cover a gap between invoices. Fast forward six months: he was trapped in what I call the “advance treadmill.” Each time his paycheck hit, he’d immediately need another advance just to cover the previous one. The amounts crept up from $50 to $100 to eventually maxing out his daily limit.

By early 2026, Marcus was basically giving Earnin first dibs on every paycheck. He couldn’t build any buffer because the cycle kept repeating. We had to do a complete financial reset (budgeting from zero, cutting expenses, building a small emergency fund) just to break free.

We had to do a full “financial detox” and build a budget from scratch to break the cycle. A cash advance app is a bandage, not a cure. The only goal should be to fix the underlying issue so you can fire these apps for good.

Smarter Alternatives That Actually Work With Chime When Earnin Can’t

Instead of fighting with an unreliable connection, consider these options that are built to work with Chime’s ecosystem.

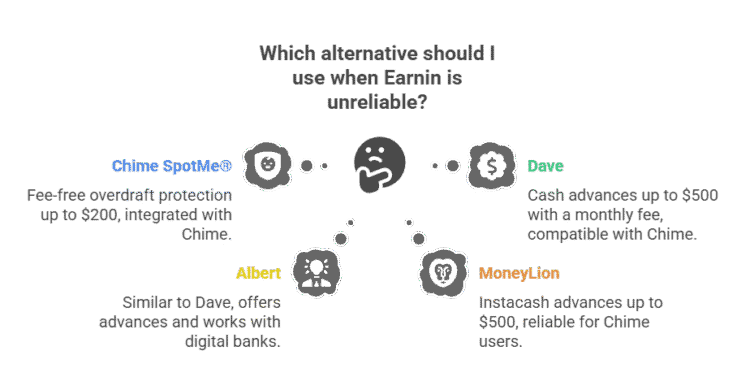

- Chime SpotMe®:

Your absolute first move. SpotMe isn’t a cash advance, it’s fee-free overdraft protection built directly into your Chime checking account. As of 2026, eligible members can overdraw on debit purchases up to $200 (no ATM withdrawals) without fees or interest. The limit starts at $20 for new users and increases based on your direct deposit history and account activity. When your next paycheck hits, Chime automatically deducts what you borrowed. No tipping, no subscription fees, completely integrated. This is hands down the safest option if you’re already a Chime user. - Dave:

Dave has built a solid reputation for Chime compatibility. In 2026, it offers ExtraCash advances up to $500, though most users start with a $100-$250 limit that grows with consistent repayment. There’s a $1 monthly membership fee, plus optional expedited funding fees ($1.99-$5.99) and tips. The big advantage over Earnin: Dave uses its own deposit verification system that plays nicely with Chime’s infrastructure. You connect your Chime account, verify your income, and usually get approved within minutes. - Albert:

Albert’s Instant feature works with Chime and most digital banks, offering advances up to $250 depending on your account activity and income verification. As of 2026, Albert charges a $14.99/month Genius membership for access to Instant (plus budgeting tools and investment features). The advance itself has no interest, but you’re locked into that monthly subscription. Best for people who want the full Albert financial suite, not just occasional cash access. - MoneyLion:

MoneyLion’s Instacash gives you up to $500 in advances (though most new users start at $100-$250). Works smoothly with Chime accounts. In 2026, there’s no mandatory fee, but they use a “turbo fee” model if you want instant access ($3.99-$8.99 depending on amount). Otherwise, advances arrive in 12-48 hours for free. No credit check required. The catch: to access higher limits and faster funding, you’ll likely want their Core membership ($19.99/month), which also includes credit building and investment features.

Your First Action Step

Before you download another app, open your Chime account and check your SpotMe limit. This built-in feature might be all you need to cover your shortfall without the hassle or risk of a third-party service. It’s the smartest, most cost-effective first move.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.