Let’s stop guessing about your risk tolerance. After nearly 30 years of guiding clients through the euphoria of the dot-com bubble, the gut-wrenching panic of 2008, the wild swings of the 2020s, and most recently, the shocking April 2025 tariff crash that sent the VIX to 45 and markets into bear territory, I can tell you one thing with absolute certainty: Most investors have no idea what their true risk tolerance is until it’s too late.

Most investors have no idea what their true risk tolerance is until it’s too late.

They take a simple online risk tolerance quiz, get labeled “aggressive,” and pile into stocks, feeling invincible during a bull market. Then, the first 20% drawdown hits, and that paper-tiger courage evaporates. They panic-sell at the bottom, locking in devastating losses. I

I’ve seen it happen dozens of times. This isn’t just an article defining a term. This is a playbook forged from decades of real-world experience, designed to help you avoid that fate.

We’re going to dismantle the myths pushed by “finfluencers” and oversimplified quizzes. We’ll replace them with a professional framework—the same one I used with my clients. That aligns with regulator standards from the SEC and FINRA and is grounded in the hard truths of behavioral finance.

We will move beyond one-dimensional thinking and explore the three critical pillars of your investor profile:

- Risk Tolerance (Your Willingness)

- Risk Capacity (Your Ability)

- Risk Composure (Your Real-World Behavior)

By the end of this guide, you won’t just have a label; you’ll have a deep understanding of your financial DNA and a practical workflow to build an asset allocation you can actually stick with, in good times and bad.

Key Takeaways Ahead

The 3-D Risk Framework: Tolerance vs. Capacity vs. Composure

For years, the industry used “risk tolerance” as a catch all term. It’s dangerously incomplete. To build a durable portfolio, you must analyze your profile in three dimensions.

Take our free Risk Tolerance Questionnaire here

Client Story: When Investment Tolerance of Risk & Capacity Collide

I’ll never forget a client couple, David and Candace in early 2008. David, a surgeon with a high and stable income, had high risk capacity. A 30% drop in their portfolio wouldn’t change their lifestyle one bit. Candace, however, had watched her parents struggle after a business failure and had extremely low risk tolerance.

Their previous advisor had ignored Candace’s fears and put them in an aggressive 80% stock portfolio based on their high capacity.

When the market crashed, Candace was in my office every week, terrified. Even though they could afford the loss, she was emotionally unwilling to endure it. After they transferred the accounts to me, we had to sell some at a loss to help her sleep at night. This was a direct result of a portfolio that ignored the tolerance dimension.

This is why regulators like FINRA and the SEC mandate a suitability assessment it’s about aligning the math with the person.

Why You Don’t Know Your Risk Tolerance (And Neither Does a 5-Minute Quiz)

The biggest problem with determining risk tolerance is that our brains are wired to be terrible investors.

The most powerful bias is Loss Aversion. As their Nobel Prize-winning Prospect Theory explains, the psychological pain of losing $1,000 is about twice as powerful as the pleasure of gaining $1,000. This is why people who claim to be “aggressive” in a rising market suddenly become terrified conservatives the moment their portfolio turns red.

How to Actually Determine Your 3-D Risk Profile: A Regulator-Aligned Workflow

Professionals operating under a best interest standard (like Regulation Best Interest in the U.S. or MiFID II in the EU) can’t just rely on a simple quiz. We use a multi-step process to build a comprehensive client profile. Here’s how you can do it for yourself.

Step 1: Assess Your Risk Tolerance (Willingness)

Start with a quality investor questionnaire. The one from Investor.gov, an official SEC site, is a great, unbiased starting point. But I have a better tool for you in a minute…

Answer honestly. This gives you a baseline label: Conservative, Moderate, or Aggressive.

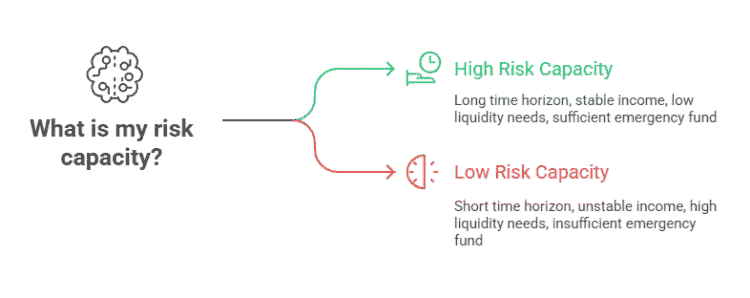

Step 2: Calculate Your Risk Capacity (Ability)

Now, ignore the quiz results and do the math. This is about your capacity for loss.

- Time Horizon:

How long until you need this money? More than 10 years gives you high capacity; less than 5 years is low. - Income Stability & Human Capital:

Is your job secure? A tenured professor has higher capacity than a freelance artist. - Liquidity Needs:

Do you have major expenses coming up (college, down payment)? This reduces your capacity. - Emergency Fund:

Do you have 3-6 months of living expenses in cash? If not, your capacity for investment risk is very low.

Step 3: Test Your Risk Composure (Behavior)

This is the step that separates amateurs from serious investors. This is the step that separates amateurs from serious investors, focusing on what financial planner Michael Kitces has termed risk composure.

- The -30% Stress Test:

Open your latest investment statement. Multiply the total by 0.70.

Write that number down. Imagine that is your new balance tomorrow.

How does that physically feel? Be honest. If your stomach churns, your composure is lower than you think. - What did you do in March 2020? Or in 2008? Most tellingly, what about April 2025 when Trump’s tariffs sent the market down 20% into bear territory, with the VIX spiking to 45.31—only to see a historic 9.5% single-day rebound just nine days later? Did you sell at the bottom and miss the recovery, or did you hold (or even buy more)? Your past actions are the best predictor of your future behavior. It will at least rhyme…

How to Determine Your True Risk Tolerance (An Interactive Analysis)

You can determine your true risk tolerance by analyzing three distinct dimensions of your investor profile: your emotional willingness to take risks (Tolerance), your financial ability to withstand losses (Capacity), and your likely behavior during a market crash (Composure). This professional 3-step analysis prevents the #1 mistake I’ve seen in my career: overestimating your courage and panic-selling at the worst possible time.

The interactive tool below will guide you through this process:

- The Gut Check: You’ll answer two questions to establish your baseline emotional comfort with market volatility.

- The Reality Check: You’ll use sliders to calculate your financial capacity based on your time horizon, emergency fund, and income stability.

- The Fire Drill: You’ll face a crisis scenario to test your behavioral composure and reveal how you’d likely act under extreme pressure.

Based on your inputs, the analyzer will generate your unique 3D Risk Profile, my personal “Advisor’s Take” on your results, and a suggested starting asset allocation. Begin the analysis below to get your personalized results in under 2 minutes.

The 3D Risk Profile Analyzer

Let's discover your personal risk profile across three critical dimensions: your willingness to take risk, your ability to take risk, and your emotional composure when markets get volatile.

Dimension 1: Risk Tolerance (Your Mindset)

Which scenario sounds most like you when you think about your investment portfolio?

Building a Portfolio You Can Stick With

Once you have your 3-D profile, you can build an asset allocation that fits. This involves diversification across different asset classes.

- Conservative Profile:

Often 20-40% stocks, 60-80% bonds and cash. Focus is on wealth preservation and avoiding volatility. - Moderate Profile:

Typically a 50/50 or 60/40 mix of stocks and bonds. A balance between growth and stability. - Aggressive Profile:

80-100% in stocks. For investors with high tolerance, high capacity, and proven composure over a long time horizon.

Related Reading You Might Enjoy

My Personal Portfolio: Walking the Talk in 2026

It’s easy to preach about risk tolerance from the ivory tower of theory. Let me show you what I actually do with my own money, because the best advisors eat their own cooking.

My current allocation is 70% equities / 30% fixed income. That puts me solidly in the “Moderately Aggressive” category. But here’s the key: this allocation stayed exactly the same through April 2025 when my portfolio dropped 15% in two weeks. I didn’t sell a single share. In fact, I rebalanced… buying stocks when they were down 20% to bring my equity allocation back to target.

Why could I do that? Because I followed my own 3-D framework:

Tolerance:

I’ve been through 2000, 2008, and March 2020. I know my emotional limits and I’m comfortable with 15-20% drawdowns.

Capacity:

I have (hopefully) 40+ years until retirement ends. A 12-month emergency fund, and no immediate liquidity needs. Mathematically, I can handle the volatility.

Composure:

My past behavior proves it. I’ve never panic-sold during a crash. I’ve always rebalanced into weakness. This isn’t theory, it’s documented history.

That’s the power of knowing your true risk tolerance. When April 2025 hit, I didn’t need to make an emotional decision in the moment. I already had a plan built on a foundation of self-knowledge. The 9.5% rebound that followed rewarded that discipline.

Your Risk Tolerance Next Steps: From Guesswork to a Bulletproof Financial Plan

Understanding your risk profile is the most important step in your investment journey. It’s more critical than picking the hot stock of the day and more impactful than timing the market. It is the foundation upon which your entire financial plan rests.

By moving beyond a simple quiz and embracing the 3-D framework of Tolerance, Capacity, and Composure, you stop being a passenger in your financial life and become the pilot. You create an Investment Policy Statement (IPS), a personal set of rules, that guides your decisions not based on fear or greed, but on a deep, honest assessment of who you are and what you can handle.

This is how you build a portfolio that lets you sleep at night. This is how you stay the course during the next inevitable market storm—whether it’s driven by tariffs, AI disruption, or geopolitical shocks. As we navigate 2026 with continued uncertainty around interest rates, inflation, and policy volatility, the investors who win won’t be the ones with the highest risk tolerance on paper. They’ll be the ones who combined honest self-assessment with the discipline to stick to their plan when everyone else is panicking. This is how you win.

Now, try searching for: asset allocation models, how to start investing, or Roth IRA guide.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.

Take our FREE Risk tolerance questionnaire and let us know where you stand?