Let’s be honest: choosing a budgeting app feels overwhelming. The market is flooded with options, all promising financial clarity.

But I’ve learned from nearly 3 decades of financial planning that the best budgeting app isn’t the one with the most features. It’s the money tracking app that matches your money personality.

The wrong budgeting tool inevitably leads to burnout. In an informal poll of 50 of my former clients, the #1 reason they quit a budgeting app was “too much daily maintenance.” The tool didn’t fit their life.

It’s the reason so many high earners are ‘not rich yet,’ and why companies are increasingly offering financial wellness platforms as an employee benefit to help their teams reduce money stress.

That’s why this guide is different. I’ve personally tested dozens of apps, and I’ve structured this review to help you find the perfect fit for your specific goals and habits. We’ll find the app that sticks.

📌 In a Hurry? Here’s My Verdict:

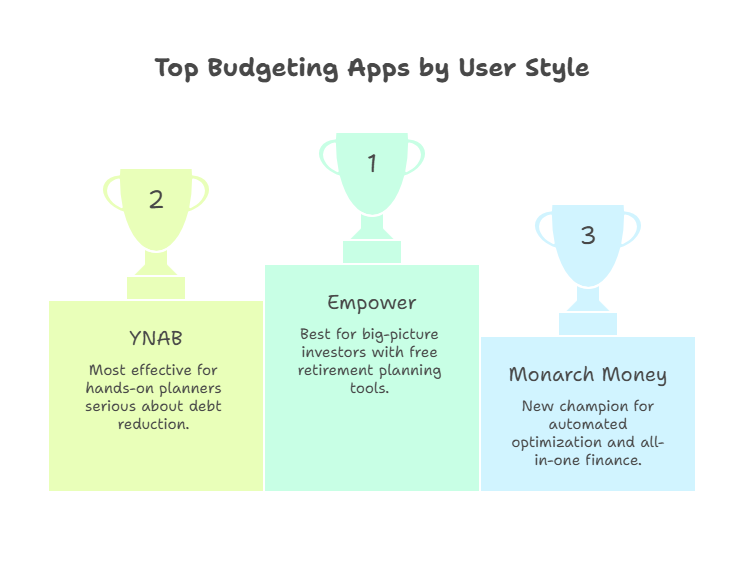

- ✔️ Best Free App: Empower is the best choice for tracking investments and net worth, for free.

- ✔️ Best Overall (paid): Monarch Money is the best Mint replacement for 90% of people, especially couples.

- ✔️ Best for Debt Payoff: YNAB is the undisputed champion if you’re serious about getting out of debt.

- ❌ App to Avoid: Rocket Money has too many user complaints lately about billing to be recommended.

Find Your Ideal Budgeting Co-Pilot

Answer these questions to see which budgeting approach and app might best suit your style and needs.

This tool provides general guidance. Your individual needs may vary. Always research thoroughly before making financial decisions.

Key Takeaways Ahead

What’s Your Money Personality? A Planner’s Framework for Choosing

Before you look at a single app, you need to know what kind of budgeter you are. I’ve found my clients generally fall into one of three categories

The Hands-On Planner:

You crave control and are willing to be actively involved. You feel empowered by categorizing every transaction and creating a forward-looking plan.

For you, the power of a tool like YNAB lies in leveraging the behavioral principle of proactive choice, shifting you from a reactive consumer to an intentional planner.

The Automated Optimizer:

You’re busy and want insights without the daily effort.

You need a tool that works silently in the background, automatically tracking your accounts and alerting you only when something needs your attention.

The Big-Picture Investor:

Your primary goal isn’t just managing monthly cash flow; it’s growing your net worth. You need a powerful dashboard that tracks all your assets—investments, real estate, and savings in one place.

Seeing your net worth trend line gamifies wealth-building and makes future goals feel tangible.

The Best Budgeting Apps by Money Personality

Now, let’s match the best tools to your style.

For “The Big-Picture Investor”: Empower

This is my personal favorite for most users. Especially the Big Picture Investor!

If your main goal is a 30,000-foot view of your entire financial life, Empower (formerly Personal Capital) is the undisputed king, and it’s completely free.

Empower’s account aggregation services provide the best free dashboard for tracking your net worth.

The psychological impact of seeing your net worth chart tick up daily cannot be overstated. It creates a positive feedback loop that gamifies wealth-building, making a distant goal like retirement feel immediate and tangible.

Its budgeting tools are more basic, but its retirement planner and investment checkup tools are best-in-class.

For “The Hands-On Planner”: YNAB (You Need A Budget)

For the Hands-On Planner who wants to command every dollar, YNAB is the undisputed champion. This is the most effective tool I’ve seen for people who are serious about getting out of debt, and it integrates powerful debt management tools, like target payoff dates, directly into its system.

YNAB is more than just an app; it’s a financial philosophy. It uses the zero-based budgeting method, forcing you to give every single dollar a “job.”

The power of YNAB’s zero-based method is rooted in behavioral finance. By forcing you to make a proactive choice for every dollar, it creates a sense of scarcity and intentionality that short-circuits the reactive, emotional spending that derails most budgets.

It’s not for the passive user, but as YNAB users report, the results are life-changing, with users saving an average of $600 in their first two months.

For “The Automated Optimizer”: Monarch Money

Since Mint shut down, Monarch Money has become the new champion of all-in-one personal finance.

It expertly blends powerful personal finance management (PFM) tools, investment tracking, and goal setting into a clean, intuitive interface. Its “Rules” feature is a lifesaver; I created a rule to automatically categorize any transaction from ‘Amazon Marketplace’ over $100 as ‘Household Goods’ instead of ‘Shopping,’ which helped fine-tune my budget effortlessly.

📘 A Planner’s War Story: The Power of a Free Tool

A client was convinced his investments were “fine.” I had him link his accounts to Empower. The free ‘Investment Checkup’ tool immediately flagged that he was paying over 1.5% in fees in an old mutual fund. A “fee leak” that was costing him over $2,250 a year. That one insight, from a free tool, could be worth over $75,000 more by retirement thanks to compounding.

Budgeting App Showdown: A Feature-by-Feature Comparison

Here’s how my top picks stack up on the features that matter most.

| App Name | Price | Best For (Money Personality) | Key Feature |

|---|---|---|---|

| Monarch Money | $14.99/mo or $99.99/yr | The Automated Optimizer / The Family CFO | Excellent couples/family sharing features. |

| YNAB | $14.99/mo or $99/yr | The Hands-On Planner | Powerful zero-based budgeting methodology. |

| Empower | Free | The Big-Picture Investor | Best-in-class investment & net worth tracking. |

| Honeydue | Free | The Family CFO (Couples) | Designed for collaborative partner budgeting. |

| Copilot Money | $13/mo or $95/yr | The Automated Optimizer (Apple Users) | Slickest user interface and AI categorization. |

The Apps to Be Cautious Of: A Note on Trust and Safety

A budgeting app is only useful if you can trust it with your data. Reputable apps use bank-level, 256-bit encryption and connect to your accounts via trusted aggregators like Plaid, which use tokens and don’t store your bank login credentials. However, not all apps have a stellar track record.

⚠️ Red Flag: Rocket Money

While Rocket Money offers useful features, significant trust issues persist. The Better Business Bureau reports 273 complaints in the past three years with users citing unauthorized charges and major difficulty canceling subscriptions—an ironic twist from an app meant to simplify your money.

Frequently Asked Questions About Budget Tracking Apps

What is the best free alternative to the Mint app?

For users who loved Mint’s comprehensive financial dashboard and net worth tracking, Empower is the best free alternative. For those who want more hands-on budgeting, the free version of Goodbudget is an excellent choice.

Is paying for a budgeting app like YNAB or Monarch Money worth it?

A paid app is worth it if it helps you change your behavior. If a $99/year subscription to Monarch Money helps you identify and cut $20/month in wasteful spending and build a plan to pay down high-interest debt, the return on your investment is massive.

Your Next Steps: From Choosing to Committing

Choosing the right budgeting app is a powerful step toward financial control. Remember, the goal isn’t just to track your expenses; it’s to build a system that empowers you to achieve your long-term goals.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.