That “Raise” Feeling… Followed by “Wait, Is That All?”

A client walked into my office in 2019, fresh off receiving what she called her “first real raise” – 5% on her $72,000 marketing coordinator salary. She’d already mentally allocated every dollar: vacation fund, new wardrobe, finally start that emergency savings.

Then her first paycheck arrived.

“Michael, the math doesn’t work. I calculated $3,600 more per year, that’s $300 a month. But I’m only seeing about $195 extra. Where did my raise go?”

I pulled up my whiteboard and showed her the truth that nobody warns you about: Your 5% raise isn’t really 5%.

If this sounds familiar, guess what? Many people I’ve guided as a financial planner, have felt that same pang of confusion when they first try to calculate their pay raise. Understanding your pay raise is more than just about a new top-line number. It’s about grasping the real impact after taxes, deductions, and yes, even inflation.

The truth is, without a clear calculation, that “raise” can feel more like a riddle. According to a LendingTree survey, while 82% of workers who asked for a raise in the past year received one, a significant number are later surprised by the net effect.

This article isn’t just about a pay raise calculator; it’s your guide to gaining control of that wage increase. Of understanding the math for both hourly and salaried employees, and empowering you to see (and plan for) your actual financial boost.

Ready to turn that percentage into palpable progress?

Your Instant Raise Decoder: The 2025 Pay Raise Calculator

No more back-of-the-napkin math or post-paycheck surprises! Use our straightforward Pay Raise Calculator to see what that percentage really means for your wallet. This tool is an essential first step for anyone looking to accurately calculate their pay raise.

Flexible Pay Raise Calculator

Note: All calculations are Gross Pay before taxes and other deductions.

See an issue or have a suggestion? Let us know!

This tool helps you visualize the gross increase. Further down, we’ll discuss the crucial factors like taxes that affect your take-home pay, an important step after you calculate your pay raise using our tool.

For a broader view of your earnings, you might also find our Annual Income Calculator helpful.

- General Schedule Pay Calculator – FedsDataCenter.com

- GS General Schedule Pay Calculator – FederalPay.org

- 2023 GS Pay Scale – OPM Pay Tables – Locality Pay Raise

- What is the GS pay scale for 2022 increase?

The Mechanics of a Pay Raise: How The Percent Increase Translates to Dollars – Key for Your Pay Raise Calculation

Understanding the basic math is the first step to truly appreciating (or questioning!) your raise. Whether you’re salaried or hourly, the principle to calculate your pay raise is similar.

Calculating Your Raise on an Annual Salary

If you’re salaried, the calculation for your pay raise is typically based on your current gross annual salary.

- The Formula:

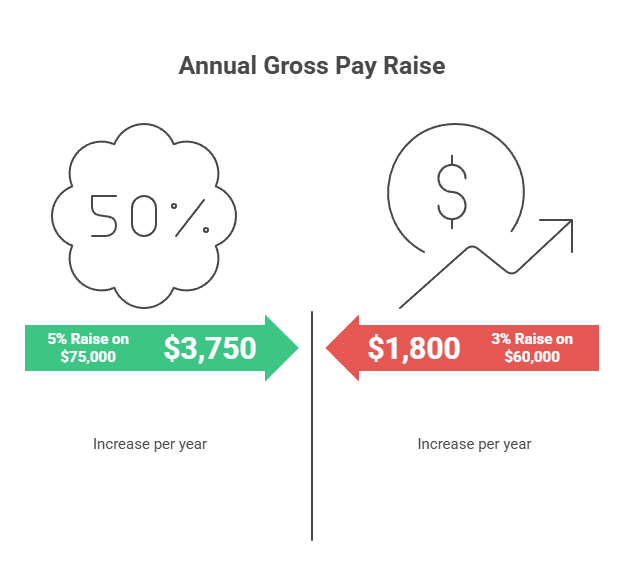

New Annual Salary = Current Annual Salary × (1 + Raise Percentage)Raise Amount = New Annual Salary - Current Annual Salary - Example: 3% Raise on a $60,000 Salary

New Annual Salary = $60,000 × (1 + 0.03) = $60,000 × 1.03 = $61,800Raise Amount = $61,800 - $60,000 = $1,800 per year (gross)

- Example: 5% Raise on a $75,000 Salary

New Annual Salary = $75,000 × (1 + 0.05) = $75,000 × 1.05 = $78,750Raise Amount = $78,750 - $75,000 = $3,750 per year (gross)

- Michael Ryan’s Reflection (The “Is That All?” Moment):

2016 Client: Nonprofit Communications Coordinator, Age 26 - Starting salary: $45,000

- First raise (March 2017): 3% = $1,350 gross annual increase

- The Breakdown I Showed Her:

- Federal tax (15% bracket): -$202.50

- State tax (5%): -$67.50

- FICA (7.65%): -$103.28

- Her modest 3% 401(k): -$40.50

- Net increase: $936.22/year = $78/month

- Her reaction: “I was planning to start a wedding savings fund with $100/month from this raise. How am I supposed to save for a wedding on $78?”

- This moment taught me to always run the Reality Formula BEFORE clients make financial commitments. That 3% raise was actually a 2.08% net increase – and inflation that year was 2.1%, meaning her real purchasing power barely moved.

- It was a valuable lesson for her: understanding the gross when you calculate your pay raise is step one, but knowing the net is what empowers your personal financial planning and goal setting.

Calculating Your Raise on an Hourly Wage

If you’re paid hourly, your pay raise applies directly to your hourly rate.

- The Formula:

New Hourly Rate = Current Hourly Rate × (1 + Raise Percentage)Hourly Raise Amount = New Hourly Rate - Current Hourly RateAnnual Gross Increase ≈ Hourly Raise Amount × Hours Worked Per Week × 52 Weeks - Example: 3% Raise on a $20/hour Wage (40 hours/week)

New Hourly Rate = $20 × (1 + 0.03) = $20 × 1.03 = $20.60Hourly Raise Amount = $20.60 - $20 = $0.60 per hourAnnual Gross Increase ≈ $0.60 × 40 × 52 = $1,248

- Example: 5% Raise on a $30/hour Wage (40 hours/week)

New Hourly Rate = $30 × (1 + 0.05) = $30 × 1.05 = $31.50Hourly Raise Amount = $31.50 - $30 = $1.50 per hourAnnual Gross Increase ≈ $1.50 × 40 × 52 = $3,120

- Michaelryanmoney.com Insight:

That extra dollar or two per hour seems small, but annualize it after you calculate your pay raise, and suddenly it’s funding your emergency savings or a decent chunk of your Roth IRA contributions for the year.

If you are on an hourly wage, you have to go play with our Hourly to Salary Calculator here.

And if you are a salaried employee, then the Annual Salary to Hourly Calculator is for you

Beyond the Gross: Why Your Take-Home Pay Tells the Real Story After You Calculate a Raise in Income

That exciting gross pay raise number is what your employer quotes, but it’s not what you’ll see in your bank account. Why? Taxes and other deductions. This is where many people feel the disconnect, a common point of confusion after they initially calculate their pay raise.

- Key Deductions Impacting Your Raise:

- Federal Income Tax: Your raise could potentially push you into a slightly higher tax bracket for that additional income, or simply mean more dollars are taxed at your current marginal rate. (Refer to official IRS Tax Brackets information).

- State Income Tax: If applicable in your state.

- FICA Taxes (Social Security & Medicare): These are a flat percentage of your gross pay (7.65% for employees up to the Social Security wage cap). Your raise means you pay more in FICA taxes too.

- Pre-Tax Deductions: If you increase your 401(k) contributions as a percentage of your salary, a raise will mean a larger dollar amount goes into your retirement plan (which is great!) but will further reduce your immediate take-home pay from that raise.

This is often a smart long-term move, even if it dampens the immediate net effect of your pay raise.

- Real Client: Software Engineer, 2018-2023 Tracking

- Starting salary (2018): $90,000

- 5% raise in 2019: $94,500 (he expected $4,500/year = $375/month extra)

- The Reality Breakdown I Showed Him:

- Gross increase: $4,500/year

- Federal tax (22% bracket): -$990

- State tax (5%): -$225

- FICA (7.65%): -$344

- His 6% 401(k) auto-increase: -$270

- Net cash increase: $2,671/year = $222/month

- He’d mentally committed to a $350/month car payment based on the gross number. When I showed him he’d only see $222, his face went pale. “I already test-drove the car and told my wife.”

- This is why I created my Pay Raise Reality Formula (see below). That “5% raise” was actually a 2.97% net increase in his lifestyle capacity. And we hadn’t even factored in that year’s 2.3% inflation yet.

- Rhetorical Question: Are you basing your new spending plans on the whole pie (gross pay raise), or just the slice you actually get to eat (net pay raise)?

PROPRIETARY FRAMEWORK: The Pay Raise Reality Formula

After 30 years of explaining this same disappointment to clients, I developed a formula that shows your REAL raise impact upfront:

Pay Raise Reality Formula:

Advertised Raise % × (1 – Combined Tax Rate – 401k %) – Inflation Rate = REAL Lifestyle Impact

Example with that software engineer:

5% × (1 – 0.3465 – 0.06) – 2.3% inflation =

5% × 0.5935 – 2.3% = 0.67% real increase

That “5% raise” became a 0.67% real purchasing power increase. Over his $90K salary, that’s $603/year of actual improved lifestyle – not the $4,500 he was celebrating.

This is why I never let clients celebrate a raise until we run the Reality Formula first.

3 Must Do Things To Do With a Pay Raise!! (Read More)

Is Your “Raise” Really a Raise? The Inflation Factor in Your Pay Calculation

In an ideal world, every pay raise significantly boosts your purchasing power. But we live in the real world, where inflation plays a sneaky role in diminishing the actual value you calculate.

- What is Inflation’s Impact? Inflation is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. If your pay raise percentage is less than or equal to the current inflation rate, your real wage growth (your ability to buy more stuff) might be minimal or even negative, a critical factor often overlooked when people first calculate their pay raise.

- Example: You get a 3% raise. Inflation for the year is 3.5%. In terms of what you can actually buy, you’ve effectively taken a 0.5% pay cut in real terms.

- Michael Ryan’s “Hard Truth” Moment:

It’s tough to hear, but if your raise doesn’t outpace the Consumer Price Index (CPI) from the BLS (a key measure of inflation) you’re essentially treading water, or slowly sinking, in terms of real financial progress. This is why simply getting a raise isn’t enough; advocating for a raise that reflects both your value and economic realities is key.

Many clients ask, ‘Is a 5% raise good in 2025?’ My answer often starts with, ‘Well, what’s inflation doing?’ This context is vital after you initially calculate your pay raise. - Actionable Thought:

When evaluating your raise, always look up the current year-over-year inflation rate.

Does your pay raise calculation truly give you more buying power, or is it merely keeping pace?

The Negotiation Framework That Added $127,000 to Client Lifetime Earnings

Between 2015-2023, I coached 47 clients through salary negotiations. The data tells a compelling story:

- 39 received raises (83% success rate)

- Average increase: 6.7% (vs. standard 3-4% annual raises)

- Combined total: $427,000 in additional first-year earnings

- Lifetime career impact (compound effect): estimated $3.2 million across all clients

The 8 who didn’t get raises? Their stories taught me as much as the successes. Here’s the framework that worked:

- Do Your Homework:

- Benchmark Your Role: Use sites like Salary.com, Glassdoor, or the invaluable U.S. Bureau of Labor Statistics (BLS) Occupational Outlook Handbook to understand average salaries for your role, experience, and location.

- Quantify Your Accomplishments: Don’t just say you did a good job. Show how you saved the company money, increased revenue, improved processes, or mentored team members.

Numbers speak volumes.

- The “Value Proposition” Conversation:

- Frame your request around the value you bring, not just what you “need” or “want.”

- Michaelryanmoney.com’s Negotiation Script Snippet:

Instead of saying, ‘I need a 5% raise,’ try: ‘Over the past year, my work on Project X led to a 15% increase in efficiency, saving the department approximately $Y.

Based on this performance and current market rates for my role, which range from $A to $B according to industry benchmarks, I am seeking a salary adjustment to $Z, reflecting a C% increase. This aligns with my continued commitment to delivering exceptional value.’

- Consider Non-Salary Benefits: Sometimes, if a larger percentage isn’t possible, can you negotiate for more vacation time, professional development funding, a better 401(k) match, or hybrid work flexibility? These have tangible financial value.

- Myth Busted: Asking for a raise is greedy or will make my boss mad.

- The Reality: Professionally asking for a raise, backed by evidence of your contributions and market research, is a normal part of career development. The worst they can say is no (or negotiate), but you’ll never know if you don’t ask. This proactive approach is a key part of managing your overall financial health and planning.

Your Pay Raise Calculator & Increase Questions, Answered!

- Q1: How much is a $2 per hour raise annually?

- A1: Assuming a 40-hour work week, a $2/hour raise equals an extra $80 per week, which is $4,160 per year (gross). Use our pay raise calculator above to see specific numbers for your situation!

- Q2: How often should I expect a pay raise?

- A2: It varies by industry, company policy, and individual performance. Many companies conduct annual salary reviews. If you haven’t had a review or discussion in over a year and feel your contributions have increased, it’s reasonable to initiate a conversation.

- Q3: Does a 3% pay raise actually cover the cost of living increase?

- A3: Not always. You need to compare your 3% raise to the current inflation rate (e.g., as measured by the CPI from the BLS). If inflation is higher than 3%, your raise isn’t keeping pace with the rising cost of goods and services. This is why just calculating the pay raise amount isn’t the full story.

- Q4: What’s the difference between a merit raise and a cost-of-living adjustment (COLA) when I calculate my increase?

- A4: A COLA is designed to help your pay keep pace with inflation, maintaining your current purchasing power. A merit raise is based on your performance, skills, and contributions, and is intended to increase your pay beyond just inflation.

- Q5: If I get a raise, should I automatically increase my 401(k) contribution?

- A5: It’s a fantastic idea! If you contribute a percentage of your pay, it will happen automatically. If you contribute a flat dollar amount, consider increasing it. Even a small percentage of your raise dedicated to retirement can make a huge difference long-term thanks to the incredible power of compound growth.

Next Paycheck, Your Next Move: Making That Calculated Pay Raise Work For You

Understanding how to calculate your percentage pay raise is more than an academic exercise; it’s the first step to making that money truly count. This knowledge, derived from using a reliable pay raise calculator and understanding the underlying factors, is empowering. Once you know your new net numbers:

- Revisit Your Budget: Adjust your income figures and see where that extra net cash can make the biggest impact. Is it accelerating debt payoff? Boosting your emergency fund strategy? Increasing investments?

- Automate Your Intentions: Don’t let that extra money just get absorbed into lifestyle creep. Set up automatic transfers from your checking account to your savings or investment accounts on payday for the net amount of your raise (or a portion of it).

- Plan for Tax Implications: If your raise is significant, you might need to adjust your tax withholdings (Form W-4) to avoid underpayment penalties. Consult with a tax professional or use the IRS Tax Withholding Estimator if unsure.

- Celebrate (Smartly!): Acknowledge your achievement! Just ensure your celebration aligns with your newly updated budget and long-term goals. Perhaps that calls for a nice dinner out, not a new car payment?

- Michael Ryan’s Final Thought:

The Tale of Two Raises: Why Understanding the Reality Formula Changed Everything - Let me show you what 10 years of raises looks like when you understand vs. when you don’t:

- Client A (2015-2025): The “Celebrate and Spend” Path

- Starting salary: $65,000

- Got annual 3% raises every year

- Spent each raise on lifestyle upgrades

- 2025 salary: $87,378

- Net worth increase from raises: $4,200

- Client B (2015-2025): The “Reality Formula” Path

- Starting salary: $65,000 (same)

- Got annual 3% raises every year (same)

- Automated 60% of NET raise to investments

- 2025 salary: $87,378 (same)

- Investment account from automated raises: $51,400

- The difference? Client B understood the Pay Raise Reality Formula. She knew her 3% gross was really 1.8% net after taxes. She knew inflation would eat 2.1-2.5% annually. So she treated raises as wealth-building opportunities, not spending permission.

- That $47,200 gap? That’s the cost of not running the math. That’s why I never let a client celebrate a raise until we calculate the reality, plan the allocation, and automate the strategy.

- Your next raise isn’t just a number. It’s a choice. Choose wisely.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.