Ever stared at your credit score and felt like it’s some mystical number decided by a secret society? You think you’re alone? After 25 years as a financial planner, I’ve seen countless brilliant people, from “Credit Builder Caseys” just starting out, to “Debt Juggler Danas” managing multiple cards. And even savvy “Financial Planner Phils” get tripped up by one of the most influential yet often misunderstood factors: Credit Utilization.

Forget the complex algorithms for a moment. Your credit utilization ratio is, at its heart, a simple measure of how much of your available revolving credit (think credit cards, lines of credit) you’re actually using.

It accounts for a whopping 30% of your FICO score. Second only to payment history!

Why should you care? Because lenders see your credit utilization ratio as a direct indicator of your financial stress and responsibility.

High utilization screams “risk,” while low utilization whispers “savvy borrower.”

Today, we’re not just defining it. We’re controlling it. We’re giving you the tools, an interactive credit utilization calculator AND a downloadable worksheet, to finally get a grip on this. And I’ll share some hard-won insights from my financial planning career that can help you turn this number into your credit score’s secret weapon.

Credit Utilization 101: Your Score’s Secret Engine (Quick Video & Why It’s Non-Negotiable)

Alright, let’s cut straight to the chase. You’re here because you want to understand Credit Utilization Ratio, right?

Simply put, it’s the percentage of your available revolving credit (think credit cards, lines of credit) that you’re currently using. If you have a total credit limit of $10,000 across all cards and your current combined balance is $3,000

Your credit utilization ratio is 30($3,000 is 30% of $10,000).

Why do you need to understand this right now?

Because this single number is a financial heavyweight, powerfully influencing:

- Your Credit Score (Big Time!): It makes up about 30% of your FICO score A high ratio can drag your score down significantly, while a low one can be a major credit score booster. Or if you have have ever wondered where your credit score starts as well.

- Loan Approvals & Interest Rates: Lenders scrutinize this ratio. A high utilization signals you might be overextended and thus a higher risk. This can lead to outright loan denials or, if approved, much higher interest rates on mortgages, car loans, and new credit cards, costing you thousands.

- Your Overall Financial Health Picture: It’s a key vital sign. Consistently high utilization can indicate budgeting challenges or that you’re relying too heavily on credit to manage expenses.

Think of it like the oil in your car’s engine. You might not check it daily, but if it gets too low (or in this case, the utilization percentage gets too high), major problems are just around the corner. Understanding your credit utilization ratio now gives you the power to proactively manage it, improve your creditworthiness, and ultimately, save a boatload of money.

Now, while that video gives you the basics, I strongly suggest you keep reading.

I’m about to share my 25+ years of real-world experience, including insider perspectives on what truly moves the needle with this ratio, common (and costly!) mistakes I see people make, and exactly how to fix a less-than-ideal situation.

Plus, I’ve got a downloadable Credit Utilization Worksheet and an interactive Credit Utilization Calculator further down to make all of this incredibly practical for you. Ready to become a credit utilization pro? Let’s dive deeper.

So, Michael, What’s This Credit Utilization Thing REALLY Costing Me (Or Saving Me)?

Imagine two people, both with a $10,000 total credit limit.

- Casey has balances totaling $8,000.

Her utilization? A sky-high 80%. - Dana has balances totaling $1,000.

Her utilization? A stellar 10%.

Who do you think gets the better mortgage rate, the lower car insurance premium, or the coveted travel rewards card? Dana, every single time.

High utilization can mean paying thousands more in interest over the life of a loan. It can be the difference between approval and denial. This isn’t just a number; it’s money in your pocket or money needlessly flying out.

A Common Myth I Constantly Battle:

Michael, I always pay on time, isn’t that enough? Paying on time is crucial, yes, it’s 35% of your FICO score!

But if you’re consistently using 90% of your credit limit, even with on-time payments, your score will suffer. It’s like acing one part of an exam but failing another, you won’t get the top grade.

The Credit Utilization Formula & Why Per-Card Matters Too!

The basic credit utilizaation formula is simple:

Credit Utilization Ratio = (Total Outstanding Balances on Revolving Credit / Total Credit Limits on Revolving Credit) x 100

So, if you have $5,000 in balances across all your cards and a total credit limit of $20,000. Then your overall utilization is ($5,000 / $20,000) x 100 = 25%.

BUT HERE’S THE INSIDER KICKER many miss: Lenders and credit scoring models also look at the utilization on each individual card.

Maxing out one card, even if your overall utilization is low because other cards are empty, can still be a red flag.

Think of it like a teacher looking at your overall GPA and your grade in each subject.

- For “Debt Juggler Dana”:

You might have five cards with a $20,000 total limit and only $4,000 in total debt (20% overall – looks good!).

But if $3,500 of that debt is on one card with a $4,000 limit (nearly 88% utilization on that card), that one card is dragging you down. - Actionable Insight:

Aim to keep utilization low both overall AND on each individual card.

Generally, under 30% is good, under 10% is often seen as excellent by lenders.

The “Michael Ryan Money” Credit Utilization Toolkit: Calculate & Conquer!

Enough theory. Let’s get practical.

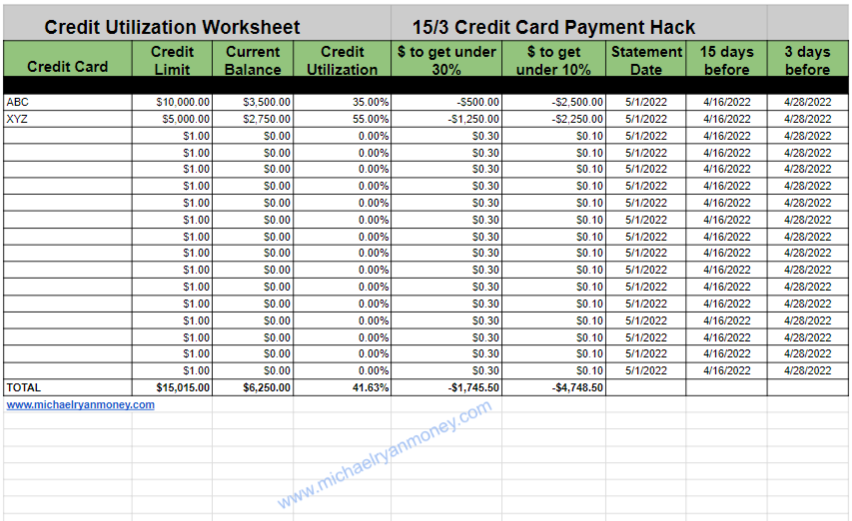

Tool #1: Your Downloadable 2026 Credit Utilization Worksheet (The Game Changer!)

While the calculator next is great for quick checks, the real power comes from tracking over time and seeing the impact of your actions. That’s where our Credit Utilization Worksheet (Google Sheet/Excel) comes in.

Here is an interactive credit utilization spreadsheet that will help you calculate everything. Download Your Free Credit Utilization Worksheet Here

If You Prefer to Download Your Free Copy Of The Credit Card Utilization Calculator – CLICK BELOW

Credit Utilization Worksheet

- Please be patient, I personally review & authorize each request. To avoid spam and other sites from stealing the tool.

Worksheet Sneak Peek & Instructions:

- Click the link above.

- Crucial Step: In Google Sheets, click FILE > MAKE A COPY. This saves it to your Google Drive so only you can see and edit your information. (If Excel, download and save).

- Enter Your Data: Fill in your card names, current balances, and credit limits. The formulas do the rest!

Why This Worksheet is Your New Best Friend (Especially for Dana & Phil!):

- List Every Card: Track balances and limits for each card individually.

- See Per-Card Utilization: Instantly identify problem cards.

- Calculates “Pay Down To” Targets: Shows you exactly how much to pay on each card to get below the crucial 30% and elite 10% thresholds.

This feature alone is gold! - Track Statement Dates: Crucial for timing payments (more on that later!).

- The “15/3 Hack” Dates Calculated: If you’re using my 15/3 Credit Card Payment Hack (opens in new window), this worksheet calculates those key payment dates for you.

- Overall Totals: See your total credit limit, total balance, and total utilization at a glance.

Tool #2: The Instant Credit Utilization Calculator

No spreadsheets needed for a quick check! Just plug in your numbers below:

Credit Utilization Calculator and Paydown Planner

Calculate overall and per-card utilization, test upcoming activity, and see how a payment could be distributed across your highest-utilization cards.

Your Utilization Analysis

Overall utilization and the highest individual-card ratio can tell different stories, so both are shown.

Current overall utilization

— —Projected overall utilization

— —Card-by-card analysis

| Card | Balance | Limit | Current utilization | Projected balance | Projected utilization | Payment to target |

|---|

Suggested payment allocation

This allocation attempts to reduce the highest individual-card utilization first. It is not an interest-cost payoff strategy.

| Card | Suggested payment | Balance after payment and charges | Projected utilization |

|---|

Your biggest utilization takeaway

Complete the worksheet to generate an explanation.

No score prediction: This calculator estimates utilization ratios only. It cannot predict whether a score will change, how many points it may change, or when a lender or scoring service will update a score.

The planning bands shown by this tool are educational reference ranges, not official FICO or VantageScore ratings. There is no universal utilization percentage that guarantees a particular score or approval result.

The balance visible in an issuer’s app may differ from the balance currently reported to a credit bureau. Payments and purchases affect a credit score calculation only after the relevant account information is reported and incorporated into the credit report used by that scoring model.

The payment-allocation feature focuses on utilization, not interest expense. A debt-payoff strategy may instead prioritize minimum payments, delinquent accounts, promotional-rate deadlines, or the highest annual percentage rate.

This tool provides educational estimates and does not provide personalized credit, lending, debt-management, legal, tax, or financial advice.

How to Use the Interactive Credit Utilization Ration Calculator:

- Gather your latest credit card statements or log in to your online accounts.

- For each card, find the Current Balance and the Credit Limit.

- Enter these into the calculator. It will show your per-card and overall utilization instantly!

Client Story (The “Worksheet Revelation”):

I had a client, ‘Financial Planner Phil,’ who thought his credit was impeccable. His overall utilization was always around 15%. But the worksheet highlighted one Amex he used for business expenses that frequently hit 70% utilization right before the statement date.

We adjusted his payment timing on that one card, and his score jumped 15 points, getting him a significantly better rate on a business line of credit. He was floored by such a small tweak yielding big results.

Beyond 30%: Unlocking Elite Credit with Smart Utilization Strategies

Okay, so under 30% is the baseline. But what if you want to play in the big leagues (think 760+ scores)?

- The 10% Rule:

As mentioned, consistently staying under 10% utilization (overall and per card) is often where the magic happens for top-tier credit. - Statement Closing Date vs. Due Date – The Billion Dollar Secret:

Most people focus on the payment due date. Smart money focuses on the statement closing date. Your issuer reports your balance to the credit bureaus around your statement closing date.- If you make a large payment before your statement closes, the balance reported will be lower, thus your utilization for that month will be lower, even if you paid the minimum by the due date. This is the core of the 15/3 Hack.

- Requesting Credit Limit Increases (Strategically!):

- How it helps: If your limit goes up but your balance stays the same, your utilization percentage drops.

- When to do it: When you have a good payment history and your income can support it.

- Caution: Don’t request increases if you’ll be tempted to spend more! And be aware some issuers do a “hard pull” on your credit, which can temporarily dip your score slightly. Ask first!

The Myth of “Closing Old Cards”:

Financial Builder Casey might think closing unused cards is good. Often, it’s not!

Closing a card reduces your overall available credit, which can increase your utilization ratio if you have balances elsewhere. It also shortens your average age of credit.

Unless a card has a high annual fee you can’t downgrade, often it’s better to keep it open and use it lightly once every few months to keep it active.

- Michaelryanmoney.com Expert Insight: According to Experian, one of the major credit bureaus, average age of accounts and credit utilization are significant factors. Closing long-held accounts can negatively impact both.

What If My Utilization Rate is High? Your Action Plan to Tame the Beast.

Seeing a high number can be a shock. Don’t panic – act!

- Stop Adding to Balances: Put the credit cards on ice for new purchases, especially on high-utilization cards. Switch to debit or cash temporarily.

- Prioritize Payments: Use the “Avalanche” (highest interest rate first) or “Snowball” (smallest balance first for psychological wins) method to aggressively pay down balances. Our worksheet helps you see which cards need attention most urgently from a utilization perspective.

- Consider a Balance Transfer (Carefully!): A 0% APR balance transfer card can provide breathing room, but be aware of transfer fees and the rate after the promotional period ends.

- Can You Increase Income or Cut Expenses? Even a small extra amount thrown at credit card debt regularly makes a big difference. Check out our Kakeibo Method Budgeting Guide

- Track, Track, Track: Use your worksheet monthly. Seeing the numbers go down is incredibly motivating!

Need a Nudge:

Is that daily $7 latte worth the extra 2% interest on your mortgage because your credit score is lagging? Small habits have big financial echoes.

Tying It All Together From Credit Score Victim to Credit Utilization Victor

Understanding and actively managing your credit utilization isn’t just about pleasing lenders; it’s about taking profound control over your financial well-being. It’s about unlocking better opportunities, saving serious money on interest, and reducing financial stress.

Whether you’re Casey building from scratch, Dana juggling multiple debts, or Phil fine-tuning for perfection, the principles are the same: know your numbers, understand the game, and take consistent, smart action.

The calculator and worksheet are your allies. The strategies are your playbook. Your improved credit score and financial peace of mind? That’s the victory.

What’s the first step you’ll take today to master your credit utilization?

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.