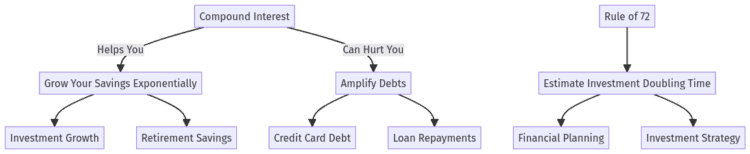

The straight answer: Compound interest is the interest you earn on both your original principal and the accumulated interest from previous periods. The Rule of 72 is a simple formula to estimate how many years it will take for an investment to double.

While often called the “eighth wonder of the world,” compounding is a double-edged sword: it can build immense wealth over time or create an inescapable cycle of debt.

This guide moves beyond simple definitions. We will use historical S&P 500 data, detailed client case studies from my nearly 30 years as a financial planner, and interactive calculators to give you a masterclass in this powerful financial force.

Whether you’re a recent graduate starting with small savings or a homeowner battling credit card debt, you will leave this page with the financial literacy to make your money work for you, not against you.

Key Takeaways Ahead

Compound Interest Calculators

Below is the Michael Ryan Money compound interest calculator for you to choose from below. Just click on each tab, then enter your information and watch the math happen!

Albert Einstein is famously quoted as saying, “Compound interest is the most powerful force in the universe.”

Albert Einstein

Compound Interest Time Machine

Compare two saving and investing paths side by side. Change the starting amount, monthly contribution, return assumption, and years to see which factor matters most.

What the assumptions produce

Each result separates what you put in from the growth generated by the return assumption.

Scenario A

—- Total contributed

- —

- Assumed growth

- —

Scenario B

—- Total contributed

- —

- Assumed growth

- —

What the comparison shows

Understanding Compound Interest: A Key to Financial Growth

Compound interest works by earning interest on both your principal (the initial amount) and the interest that accumulates. It’s the engine of long-term wealth building.

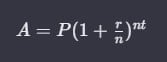

First, the formula for compound interest is: A = P(1 + r/n)^(nt)

- A is the future value of your investment

- P is the principal amount you invested

- r is the annual interest rate

- n is the number of times interest is compounded per year

- t is the number of years you invest

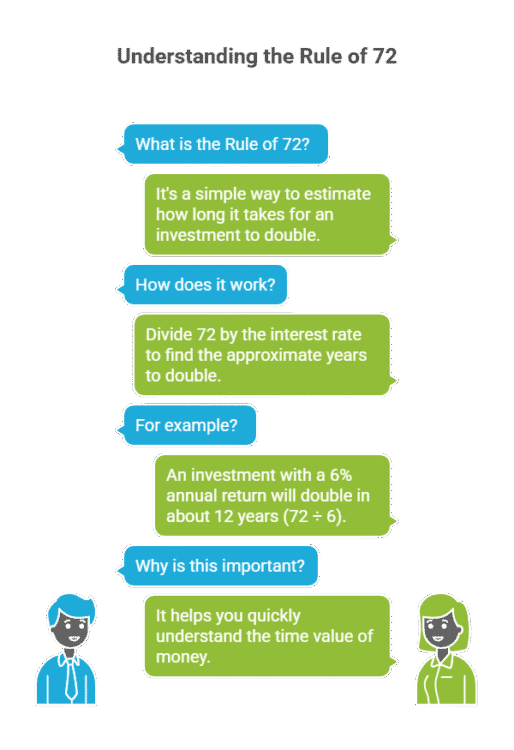

The Rule of 72: Your Mental Shortcut

The Rule of 72 is a simple way to estimate how long it will take for an investment to double.

Formula: 72 ÷ Interest Rate = Years to Double

For example, an investment with a 6% annual return will double in approximately 12 years (72 ÷ 6). This powerful shortcut helps you quickly grasp the time value of money without complex formulas.

An Example of Compounding in Action

You invest $1,000 at a 5% annual compound interest rate.

- Year 1: You earn $50 in interest. Total = $1,050.

- Year 2: You earn 5% on $1,050, which is $52.50. Total = $1,102.50.

- Year 10: Your investment grows to $1,628.89.

This exponential growth is what makes compounding a powerful ally.

The Three Levers of Your Compounding Machine

Think of your wealth as a machine with three critical levers. How you pull them determines your financial outcome.

Lever 1: Time (The Most Powerful Lever)

Starting early is the single most important factor. The “snowball effect” of compounding needs a long runway to work its magic.

The key insight?

The Teenage Saver who invested just $10,000 over 5 years ended up with nearly the same amount as the person who invested $80,000 over 40 years. The difference isn’t the money; it’s the time.

Lever 2: Compounding Frequency (The Engine’s Speed)

The more often interest is compounded, the faster your money grows.

- Daily Compounding: Fastest growth. Common in high-yield savings accounts.

- Monthly Compounding: Common for dividend reinvestment in stocks.

- Annual Compounding: Slowest growth.

With a $1,000 investment at 5% interest over 10 years:

- Daily compounding grows to $1,648.66.

- Monthly compounding grows to $1,647.01.

- Annually it grows to $1,628.89.

| Year | Principal | Interest Earned | Ending Balance |

|---|---|---|---|

| 1 | $1,000.00 | $50.00 | $1,050.00 |

| 2 | $1,050.00 | $52.50 | $1,102.50 |

| 3 | $1,102.50 | $55.13 | $1,157.63 |

| 4 | $1,157.63 | $57.88 | $1,215.51 |

| 5 | $1,215.51 | $60.78 | $1,276.29 |

| 6 | $1,276.29 | $63.81 | $1,340.10 |

| 7 | $1,340.10 | $67.00 | $1,407.10 |

| 8 | $1,407.10 | $70.36 | $1,477.46 |

| 9 | $1,477.46 | $73.87 | $1,551.33 |

| 10 | $1,551.33 | $77.57 | $1,628.90 |

Lever 3: Rate of Return (The Fuel’s Quality)

A higher rate of return dramatically accelerates growth. This is where moving from a simple savings account to diversified investments in a Roth IRA or 401(k) becomes critical.

The Dark Side: When Compound Interest is Your Enemy

Compounding is equally powerful when it works against you in the form of debt.

- Credit Card Debt:

A $5,000 balance at a 20% Annual Percentage Rate (APR) can take over a decade and cost thousands in interest if you only make minimum payments. - Student Loans:

Interest often compounds even during deferment, meaning your loan balance can be higher when you graduate than when you started. - Mortgages:

On a 30-year mortgage, it’s common to pay more than double the home’s purchase price over the life of the loan due to compounding.

The Hidden Enemies of Compounding

Beyond debt, three silent forces can erode your compound growth.

- Inflation:

The inflation impact on savings is critical. If your investments earn 7% but inflation is 3%, your real return is only 4%. You must outpace inflation to build real wealth. For the latest data, you can refer to the Bureau of Labor Statistics (BLS). - Fees:

A 1.5% annual management fee might seem small, but on a $100,000 portfolio, it can reduce your final nest egg by over $250,000 over 30 years compared to a 0.5% fee. - Taxes:

Compounding in a taxable brokerage account is less efficient than in a tax-advantaged account like a Roth IRA, where growth and withdrawals are tax-free.

We are audience supported - when you make a purchase through our site, we may earn an affiliate commission.