So, you’re eyeing that six-figure milestone, or maybe you’ve recently crossed it. One hundred thousand dollars a year. For decades, it’s been a powerful symbol of success, a tangible sign that you’ve “made it.” But let’s be brutally honest: in 2025, with inflation’s lingering bite, housing costs that seem to defy gravity, and the goalposts for true financial security constantly shifting…

Is $100,000 a year still the golden ticket it once was?

In my 25+ years as a financial planner I’ve guided folks from all walks of life. This question has come up more times than I can count. And my answer, honed by countless client stories and market cycles, isn’t a simple yes or no. It’s a resounding, “Well, that depends.”

The legendary Charlie Munger, in his typically blunt fashion, once said earning that first $100,000 is “a b—-, but you gotta do it“. He was spot on. It’s not just about the hard work; it’s a psychological and financial launchpad. But that launchpad can feel more like a trampoline on shaky ground if you’re not careful.

This article isn’t about sugarcoating. We’re going to dissect

- What $100,000 actually means in today’s economy.

- We’ll look at its real purchasing power

- How geography and lifestyle can make it shrink or stretch. You’ll love the calculator I’ve included for you…

- And what experienced financial experts (beyond just me) are observing.

Most importantly, I’ll share actionable strategies, the kind I’ve used with clients for over two decades, to help you make that six-figure income truly work for you. Forget the generic fluff; let’s talk brass tacks.

The Shifting Sands: Why $100k Feels Different in 2025

If you dialed back the clock to, say, the late 90s, a $100,000 salary put you in a very different league. Mark Anderson, a senior loan officer I know out in Chesterfield, Missouri, recently shared with me, “Michael, there was a time when if a household hit $100k, I’d assume they were eyeing the biggest house on the block. Now,” he sighed, “six figures is just table stakes to even get in the game“.

He’s not wrong. So, what’s changed so dramatically?

Cost of Living: The Silent Salary Shrinker

The relentless upward march of the cost of living is the biggest culprit. Housing, in particular, has become the financial mountain many struggle to climb.

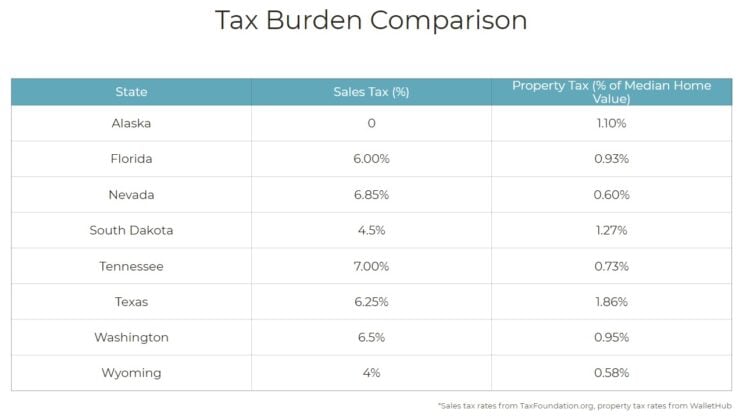

Even with a $100,000 salary, Samantha Jackson, a 20-year mortgage veteran in central Texas, told me her clients are constantly battling “payment shock”. It’s not just the sticker price of the home; it’s the total monthly outlay for principal, interest, sky-high property taxes in some areas (looking at you, Texas and New Jersey!), and ever-increasing homeowner’s insurance.

Here’s the thing: The real value of $100,000 is a geographical lottery. A cost of living study by SmartAsset, updated in mid-2024 for 2025 projections, painted a stark picture:

- In Memphis, Tennessee, that $100k might feel like $86,444 in actual spending power. Pretty good.

- But in New York City (Manhattan)? Brace yourself. It effectively shrivels to a mere $35,791.

- Similarly, in San Francisco, you’re looking at an effective $36,445. This isn’t just a U.S. phenomenon. Friends in Australia tell me that surveys by Finder in 2025 show Aussies now consider over $152,000 AUD (that’s roughly $100k USD) to be a “good” salary, but need closer to $164,000 AUD to feel “comfortable”.

The global perception of “enough” is rising.

For those of you wrestling with housing affordability, my guide on how much house you can truly afford offers a deeper dive.

Salary & City Lifestyle Comparator

Compare two US cities to understand differences in after-tax income, equivalent salary needs, and potential changes to your monthly spending power. See how far your income really goes!

Salary & City Spending Power Comparison

Compare how far a $100,000 salary (or your own income) goes in different US cities. See estimated after-tax income and what salary you might need in another city (e.g., Chicago vs. Houston) to maintain a similar lifestyle, considering cost of living indices and simplified state tax estimations. For example, to live in San Francisco like you do on $100k in Memphis, you might need over $200k due to higher taxes and a much higher CoL index.

Important Estimations: All tax figures are broad estimates based on 2024/2025 federal guidelines and simplified state tax rates (using the provided top bracket rate as an illustrative effective rate). They do not account for specific deductions, credits, local taxes, phase-outs, or individual financial situations. Cost of Living Index comparisons are illustrative. This tool is for educational and comparative purposes ONLY and is not financial or tax advice. Consult with qualified professionals for personalized guidance.

Taxes: The Taxman Always Rings Twice (Especially in High-Tax States)

Your gross salary is the Hollywood number; your net pay is the reality show.

Federal income taxes, FICA taxes (Social Security and Medicare – don’t forget those!), and then state and sometimes local income taxes take a hefty bite. To actually see $100,000 in your bank account after all deductions, you might need to earn significantly more. Often between $130,000 to $145,000, depending on where you hang your hat.

Let’s look at some numbers based on recent analyses for 2025 projections:

- California: To net $100k, you might need to gross around $144,879.

- New York (State): Think closer to $141,923.

- Texas (No State Income Tax): About $130,999 might do it.

- Florida (No State Income Tax): Similar to Texas, around $130,999.

- Oregon: Get ready to aim for $148,309.

Understanding your specific tax situation is paramount. If you’re dealing with investment income, the rules can get even more complex. Residents in states like California face specific capital gains tax rules, while those in Tennessee benefit from no state capital gains tax. For more on federal tax obligations, the IRS Publication 17 (“Your Federal Income Tax”) is a useful, if dense, resource.

Lifestyle Creep & Debt: The Self-Sabotage Loop

I’ve seen it a thousand times: income goes up, and so does spending. It’s called lifestyle creep, and it’s the silent killer of financial progress. That shiny $100,000 salary can vanish into thin air with a slightly nicer car, a bigger apartment in a trendier neighborhood, and more frequent dinners out.

Rahkim Sabree, writing for Forbes, astutely pointed out that even high earners aren’t immune to “financial trauma,” especially if they’re carrying significant debt loads. Student loans, credit card balances from leaner years, or unexpected medical bills can make a six-figure income feel surprisingly inadequate.

For some fun, use our calculator to see how much $100k a year is, hourly.

A client story that sticks with me:

David, a software engineer in Austin, finally hit $115,000 in early 2024. He was ecstatic. Six months later, he came to me stressed because he was still living paycheck to paycheck. We did a deep dive into his spending.

A new luxury SUV lease ($850/month), a high-end apartment downtown ($3,200/month), and nearly $1,000 a month on dining out and entertainment. His “raise” was entirely consumed by lifestyle upgrades before he even had a chance to feel the benefit.

We had to reset his spending plan radically.

What Data Reveals About a $100k Salary in 2025

It’s not just anecdotal; the numbers paint a compelling, if complex, picture. Earning $100,000 a year still firmly places you above the U.S. median household income, which was around $82,373 according to Motio Research (January 2025) and the most recent Census Bureau Data. As an individual earner, you’re likely in the top 20-22%. That’s statistically significant.

However, a Zillow economist recently highlighted a critical point: while only about 37% of adults earn $100,000 or more, wage growth is struggling to keep pace with the explosion in housing payments. This widening gap means the traditional “American Dream” components tied to a $100k salary are becoming harder to attain for many.

Interestingly, behavioral economics offers another lens. Research, including work by notable economists like Kahneman and Killingsworth, suggests that while emotional well-being tends to rise with income, this effect may diminish or “plateau” for many people beyond an income of approximately $200,000 per year.

This implies that $100,000, while not the peak, might sit near a crucial “comfort threshold” for many. A point where basic needs and many wants are met, and further increases in happiness become less about more money and more about how that money is used and other life factors.

Making $100,000 Work For You: My Advisor’s Playbook

So, $100,000 isn’t a magic wand. And I have bored you with numbers and research.

But, with a strategic approach, it’s a powerful tool for building genuine wealth and financial freedom. This isn’t theory; this is what I’ve helped clients implement for over two decades to turn that solid income into a truly “good” financial life:

1. Budget with Purpose: The “Conscious $100k Plan”

Forget restrictive budgeting. At $100k, your budget should be about conscious allocation.

You need to know exactly where your money is going, not to feel deprived, but to feel empowered. This clarity is what helps you fight lifestyle creep and direct your funds towards what truly matters to you.

- Action:

For one month, track every single dollar. Use an app, a spreadsheet, or even an old-fashioned notebook. You’ll be amazed at what you find. From there, a framework like the 50/30/20 rule can be a great starting point, but customize it. - Michael Ryan’s Insider Tip:

I had a client, a marketing director in Chicago, who hit $105,000 in 2023. She felt perpetually broke. We did the tracking exercise.

It turned out nearly $1,200 a month was vanishing into unplanned online shopping and food delivery apps. Identifying that was her “aha!” moment. A budget isn’t a financial straitjacket; it’s your GPS to financial freedom.

2. Annihilate High-Interest Debt: Your Guaranteed Return

If you’re servicing credit card debt at 20-25% APR, that $100k salary is working overtime for the banks, not for you.

Paying down that kind of debt is one of the best, guaranteed returns on your money you’ll ever find.

- Action:

List all your debts, interest rates, and minimum payments. Explore strategies like the debt snowball or debt avalanche. For guidance, explore resources like reputable books for getting out of debt. - Pro Tip:

Call your credit card companies. I had a client in Albany last year, Mark, who consolidated his debt. But before that, he called each of his card issuers and managed to get two of them to lower his APR by several points just by asking and highlighting his good payment history. It saved him hundreds.

3. Pay Yourself First, Aggressively: The 15-20% Rule

With a $100k income, saving and investing at least 15%, ideally 20%, of your gross income should be non-negotiable. This means $1,250 to $1,667 per month heading straight into wealth-building vehicles before you even see it.

- Action:

Max out your 401(k) contributions, especially if there’s an employer match (that’s free money!). Then, look into a Roth IRA if you fall within the MAGI limits for contributions. If you’re above those, a backdoor Roth IRA might be an option. - A Common Mistake I’ve Seen:

So many people wait until they “feel rich” or have “extra money” to invest. That’s like waiting until you’re fit to go to the gym. The power of compound interest is truly the eighth wonder of the world, and it thrives on time. Start now, even if it feels like a stretch. For foundational knowledge, check out some trusted finance books for beginners.

4. Define Your “Rich Life”—Beyond the Dollar Signs

What does financial success truly look like for you? Is it retiring at 55 to a beach house in Florida? Is it funding your children’s education without loans? Is it the freedom to take a sabbatical and travel the world? A $100,000 income provides the fuel, but you need to define the destination.

- Action:

Write down your top 3-5 financial goals – short, medium, and long-term. Be specific. This clarity will be your North Star, guiding your spending and saving decisions far more effectively than trying to keep up with the Joneses (who, by the way, are often broke). - My Take:

I worked with a couple in San Francisco, both earning good tech salaries, yet they were miserable. Their “rich life” wasn’t about the fancy apartment; it was about starting their own business.

Once they defined that, redirecting their $220k combined income became purposeful, not painful.

5. Annual Financial Check-up: Stay Proactive

Your financial plan isn’t a crockpot meal you set and forget. At a $100k income level, an annual deep dive is essential.

- Action:

Review your budget, investment performance (asset allocation review), insurance coverage, and progress towards your goals. Are you on track for retirement?

A retirement savings calculator can offer a snapshot. Life changes – marriage, kids, job promotions – all necessitate a plan refresh. - Consider major tax law changes. For example, the SECURE 2.0 Act has brought changes to retirement contributions and RMDs. Staying informed is key.

The Psychological Six Figures: It’s More Than Just the Math

There’s an undeniable psychological lift when you hit $100,000. It often validates career efforts and signals a certain level of financial competence. However, the feeling of financial well-being at this income level is intensely personal and, as we’ve explored, profoundly shaped by where you live, how you live, and the financial habits you cultivate.

The real power of a six-figure income isn’t just the number itself, but what it empowers you to achieve. When managed with foresight and discipline, $100,000 a year is a formidable foundation for building lasting financial security, realizing ambitious goals, and designing a life that truly resonates with your values.

The Final Verdict from the Trenches: Is $100k a Year Good Money?

So, back to the big question. After 25 years of advising clients, here’s my unfiltered take:

Yes, a $100,000 annual salary in 2025 is still objectively good money. It places you in a privileged segment of earners and provides a substantial income to build a secure and fulfilling financial future.

However – and this is a big “however” – its “goodness” in terms of lifestyle, comfort, and peace of mind is not automatic.

It’s highly conditional. Your geographic location (and its associated cost of living and tax burden), your debt load, your family size, and, most critically, your financial discipline and planning will ultimately determine how “good” that $100,000 truly feels.

Don’t let lifestyle inflation become the thief of your financial progress. View that $100,000 not as a destination, but as a powerful launchpad.

With intentional budgeting, strategic debt elimination, consistent and aggressive saving and investing, and clearly defined financial goals, you can transform that six-figure income into the engine that drives you towards genuine financial well-being and your unique definition of a “rich life.”

Ready to take the wheel? Start by getting a clear picture of your current financial standing with a net worth calculator and then architect your success with a personal spending plan. The power is in your hands.

Disclaimer: The information in this article is for educational purposes only and not intended as financial advice. Please consult with a qualified financial advisor or tax professional before making any financial decisions.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.