Retirees frequently encounter confusion regarding the Income-Related Monthly Adjustment Amount (IRMAA). Official government notices often provide only data tables, failing to address complex scenarios such as

- the tax implications of widowhood

- the sale of rental real estate

- or the financial consequences of exceeding the income threshold by a single dollar.

That’s why I decided to put together this guide to help answer the most common Medicare IRMAA questions. This guide compiles the most urgent, misunderstood inquiries regarding Medicare surcharges. Learn how one retiree eliminated her IRMAA penalty. And how you can too.

These answers utilize the official guidelines from the Centers for Medicare & Medicaid Services (CMS) and the Social Security Administration (SSA) to provide definitive clarity.

⚡ Key Takeaways: The IRMAA Snapshot

- The Recalculation Cycle: The Medicare Part B surcharge is not permanent; Medicare recalculates it every calendar year using your Modified Adjusted Gross Income (MAGI) from your IRS tax return filed two years earlier (for 2026 premiums, SSA generally uses your 2024 tax return).

- The Municipal Bond Trap: Tax-exempt municipal bond interest is added to AGI when calculating Medicare MAGI for IRMAA, so it can push you into a higher premium bracket even though it is not subject to federal income tax.

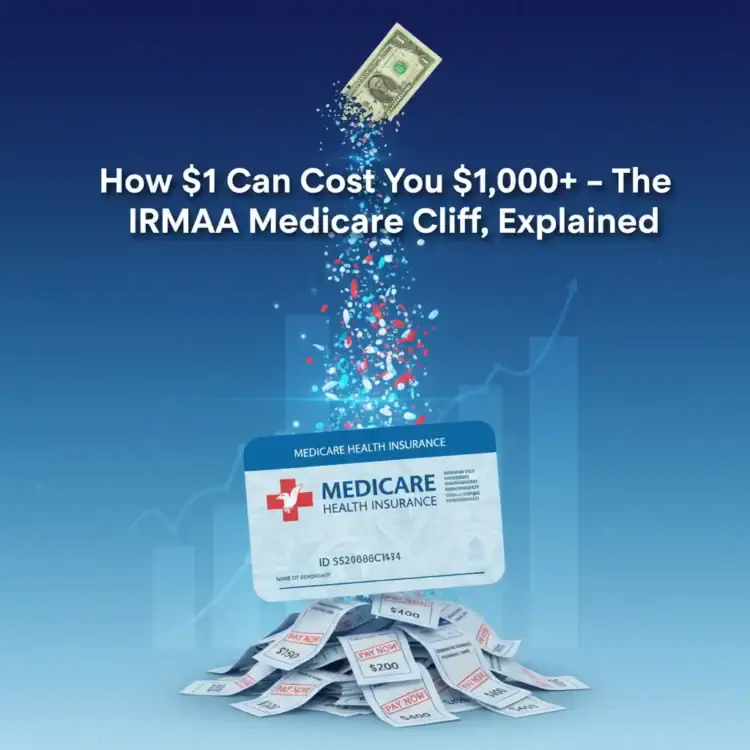

- The Marginal Tax Cliff: Exceeding an IRMAA income bracket by $1 triggers the full surcharge for that tier for the entire calendar year; in 2026, moving from just below to just above a bracket can add hundreds to over $1,000 per person in annual Part B and Part D premiums.

- The Appeal Limitations: The SSA generally grants a Request for Reconsideration only when you qualify for a recognized Life-Changing Event (LCE) or when the tax data is wrong, not simply because you had a one-time capital gain or other voluntary income event.

- The Roth Trade-off: A Roth conversion increases current-year MAGI, potentially elevating future Medicare premiums, creating a strategic tax-planning conflict.

Key Takeaways Ahead

The “What Counts?” Questions (MAGI Calculation)

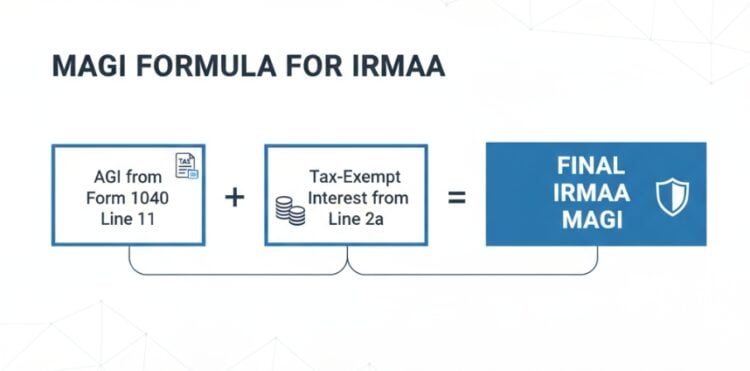

1. What exactly is MAGI for IRMAA purposes?

The Social Security Administration calculates the surcharge using a specific formula, distinct from the calculations used for Roth IRA eligibility or the Net Investment Income Tax.

For Medicare purposes, Modified Adjusted Gross Income (MAGI) starts with your Adjusted Gross Income (AGI) on Form 1040, Line 11, and adds back tax-exempt interest (Form 1040, Line 2a); SSA uses this Medicare-specific MAGI to determine whether IRMAA applies. In plain terms, Medicare MAGI is “your taxable income plus any tax-exempt interest,” not including the non-taxable portion of your Social Security benefits.

➡️ Deep Dive: What Income Counts Toward IRMAA MAGI?

2. Does tax-exempt municipal bond interest really count?

Yes. While municipal bond interest remains free from federal income tax, Congress mandates the inclusion of this revenue stream in the Medicare means-testing formula.

High-net-worth retirees cannot utilize municipal bonds to shield income from the premium adjustment.

3. Does Social Security income count toward the surcharge?

Yes, but only the taxable portion included in the AGI. Since the IRMAA MAGI calculation begins with AGI, any Social Security benefits reported as taxable income on Form 1040 are automatically factored into the surcharge determination.

4. Do Roth IRA distributions trigger IRMAA?

No. Qualified distributions from a Roth IRA are tax-free and do not appear in the Adjusted Gross Income. Consequently, tax-free Roth withdrawals serve as a primary defense strategy for managing Medicare bracket exposure in later retirement years.

5. Do capital gains affect Medicare premiums?

Yes. The IRS treats both short-term and long-term capital gains as taxable income. Therefore, realizing significant portfolio gains directly increases MAGI, potentially pushing a beneficiary into a higher IRMAA tier.

➡️ Strategy Guide: How to Avoid IRMAA Surcharges with Asset Location

6. Does the sale of a primary home count?

The surcharge calculation includes only the capital gain exceeding the Section 121 exclusion ($250,000 for single filers; $500,000 for married couples). Furthermore, homeowners should adjust the cost basis by including documented capital improvements (e.g., renovations, new roofing) to reduce the reportable profit before the Medicare income assessment applies.

7. Does an inheritance trigger the surcharge?

Generally, the receipt of an inheritance does not constitute taxable income unless the assets originate from a pre-tax source, such as a Traditional IRA or 401(k). However, liquidating inherited assets or taking a large distribution from an Inherited IRA will spike AGI, potentially triggering a one-time IRMAA spike.

➡️ Read More: Managing an IRMAA One-Time Income Spike

The “Cliff” & The Two-Year Lookback

8. What happens if income exceeds the threshold by $1?

The beneficiary owes the full surcharge for that tier. The IRMAA bracket system functions as a “cliff,” not a progressive tax.

For example, in 2026 a married couple moving from just below the first IRMAA bracket to just above it would each pay an extra $81.20 per month in Part B premiums (plus any Part D IRMAA), or almost $1,950 more per year in combined Part B premiums alone.

➡️ See the Data: IRMAA Brackets & The Marginal Tax Cliff

9. Is the surcharge applied monthly or annually?

CMS applies the adjustment as a monthly addition to the Part B and Part D premiums; however, the beneficiary remains liable for the surcharge for the entire 12-month calendar year.

10. How does the 2-year lookback period work?

Medicare determines premiums based on the tax return from two years prior.

- 2024 Income Earned → Reported on 2025 Tax Return → Determines 2026 Medicare Premiums.

➡️ Timeline: The Full IRMAA Timeline Explained

11. When does Social Security notify beneficiaries of a surcharge?

The Social Security Administration mails an Initial Determination Notice in late November or December of the year preceding the coverage year.

Appeals & Form SSA-44 (Life-Changing Events)

12. Can a beneficiary appeal a one-time capital gain?

No. The SSA rejects appeals based solely on “unusual” income events like a portfolio rebalancing or lottery win. A valid Request for Reconsideration requires a specific regulatory exception.

13. What constitutes a valid Life-Changing Event (LCE)?

The SSA recognizes only eight specific LCEs for a MAGI reduction request. These include Marriage, Divorce/Annulment, Death of a Spouse, Work Stoppage (Retirement), Work Reduction, Loss of Income-Producing Property, Loss of Pension, and Employer Settlement Payment.

➡️ The Guide: IRMAA Appeal Guide: Divorce & Death of Spouse

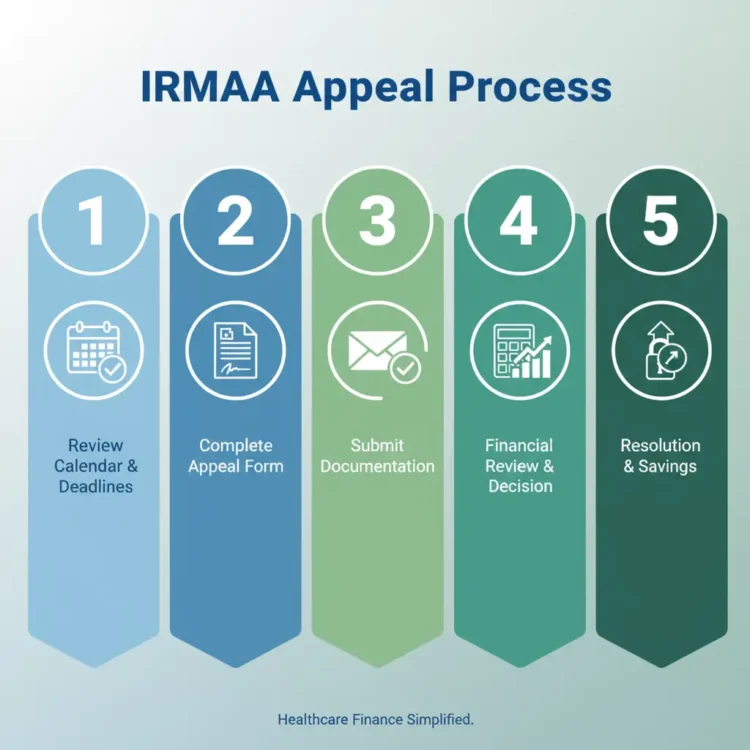

14. How does one file an IRMAA appeal?

The beneficiary must complete Form SSA-44 (Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event) and submit the document to a local Social Security office with supporting evidence. Pro Tip: Submit via Certified Mail with Return Receipt to establish a paper trail.

➡️ Step-by-Step: The Complete Form SSA-44 Guide

15. What occurs if the estimated income on the appeal is incorrect?

If the actual MAGI reported to the IRS exceeds the estimate provided on Form SSA-44, Medicare will retroactively bill the beneficiary for the unpaid premiums.

Advanced Medicare/IRMAA Strategies & Loopholes

16. Does “Married Filing Separately” reduce the surcharge?

Rarely. The Married Filing Separately (MFS) IRMAA brackets are punitive. For 2026 IRMAA determinations, the Married Filing Separately brackets are much tighter: the surcharge applies once Medicare MAGI exceeds $109,000, and the top bracket begins at $391,000, so filing separately usually increases rather than reduces your Medicare premiums.

➡️ Warning: The IRMAA Married Filing Separately Penalty

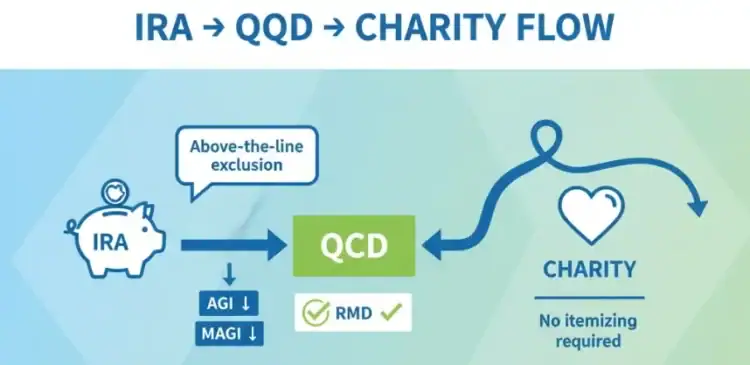

17. Can a Qualified Charitable Distribution (QCD) avoid IRMAA?

Yes. A Qualified Charitable Distribution satisfies the Required Minimum Distribution (RMD) rules while excluding the funds from Adjusted Gross Income. This exclusion directly lowers MAGI, serving as a precise tool for staying below a premium surcharge tier.

➡️ Tactic: Using QCDs to Lower IRMAA Exposure

18. Can Tax-Loss Harvesting offset the Medicare surcharge?

Yes. Tax-loss harvesting allows investors to offset unlimited capital gains and up to $3,000 of ordinary income. Reducing the net capital gain reported on the tax return directly suppresses the MAGI figure used for the Medicare premium calculation.

➡️ Strategy: Tax-Loss Harvesting for IRMAA Reduction

19. Is the IRMAA surcharge mandatory?

Yes. Failure to pay the assessed Part B or Part D adjustment results in the termination of Medicare coverage. The federal government creates no opt-out mechanism for high-income beneficiaries other than income reduction.

20. Does the surcharge apply to Medicare Advantage plans?

Yes. The Part B IRMAA is a federal assessment. Even beneficiaries enrolled in private Medicare Advantage (Part C) plans must remit the Part B premium and any applicable income adjustments to the government.

21. How do Roth conversions impact the surcharge?

Roth conversions generate taxable income in the year of execution, which raises MAGI and may trigger a temporary IRMAA spike two years later. Planners must weigh the short-term premium cost against the long-term tax-free growth benefits.

➡️ Analysis: The Roth Conversion vs. IRMAA Trade-off

📚 Related Reading & Resources

- The Calculator: Run Your Numbers with the 2026 IRMAA Calculator

- The Timeline: Understanding the 2-Year Lookback Rule

- The Mistake: Common IRMAA Mistakes to Avoid

The Bottom Line on Medicare Surcharges

IRMAA functions as a “shadow tax” on retirement success. While beneficiaries cannot alter the CMS statutory regulations, they can control the Modified Adjusted Gross Income that dictates the penalty. Whether through QCDs, Tax-Loss Harvesting, or strategic Roth Conversions, proactive income management remains the only effective defense against the Medicare cliff.

Need to check your specific bracket?

Use the Free IRMAA Surcharge Calculator

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.