Let’s talk straight. In times of financial stress, looking at your bank balance can make you ask a question that hits right in the gut: “Is my money truly safe?” You deserve to know not just the name of FDIC insurance but exactly how it protects you and what that protection really means for your savings.

For nearly three decades, I have sat across the table from people just like you. Hardworking individuals who saved diligently and then found themselves kept up at night by worrying headlines. I have heard the questions again and again: “Is my money safe in the bank?” “What if my bank is next to fail?” “I have all my accounts at one bank; is it all covered by FDIC?” “Is $250,000 really the absolute maximum insurance?”

This guide is not just another dry explanation. It was written for real people who want straightforward information. Here you will find clear answers, not financial jargon, so you can go from worry to confidence.

This is practical help for right now and for planning with confidence into 2026.

Here’s what you will learn in this guide:

- Why FDIC insurance is the foundation of your banking safety

- How the $250,000 rule actually works, with real examples

- A simple checklist of what is covered and what is not

- Ways to protect more than the standard limit if you need to

- How to think about your money in light of recent bank failures

By the time you finish reading, you will understand not just what FDIC insurance is, but how it applies to your own money and what steps you can take to make sure your savings are protected.

Key Takeaways Ahead

The FDIC guarantee isn’t just a policy; it’s a law. Since its creation in 1933, no depositor has ever lost a single penny of insured funds. This zero-loss history is the most powerful reason to have confidence in the banking system.

The FDIC guarantee isn’t just a policy; it’s a law. Since its creation in 1933, no depositor has ever lost a single penny of insured funds. This zero-loss history is the most powerful reason to have confidence in the banking system.

– The Ironclad Guarantee: FDIC insurance protects up to $250,000 per depositor, per insured bank, per ownership category. It is backed by the full faith and credit of the U.S. government.

– Coverage is Specific: It covers your deposits (checking, savings, CDs) but not your investments (stocks, crypto, mutual funds).

– The “Secret” to More Coverage: You can easily insure millions at a single bank by strategically using different “ownership categories” like joint accounts and beneficiaries.

– Verification is Simple: You can confirm your exact coverage in two minutes using the FDIC’s official tools.

– Coverage is Specific: It covers your deposits (checking, savings, CDs) but not your investments (stocks, crypto, mutual funds).

– The “Secret” to More Coverage: You can easily insure millions at a single bank by strategically using different “ownership categories” like joint accounts and beneficiaries.

– Verification is Simple: You can confirm your exact coverage in two minutes using the FDIC’s official tools.

Why FDIC Insurance Coverage is the Bedrock of Your Banking Safety

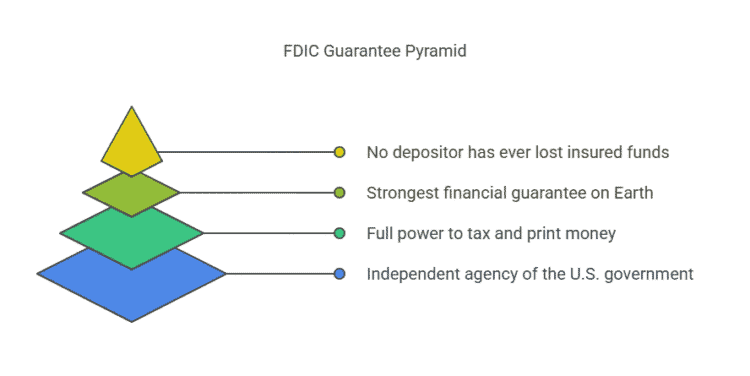

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government created by Congress in 1933 to promote public confidence and stability in the nation’s banking system. Its mission includes insuring deposits, supervising financial institutions for safety and soundness, and managing receiverships when banks fail. According to FDIC reporting, no depositor has ever lost insured funds since the agency was created.

FDIC insures deposits up to the applicable insurance limits and provides prompt access to insured funds if your bank fails. In most cases, the FDIC arranges for a healthy bank to assume the deposits or pays depositors directly up to the insured limit.

Think of it this way. I grew up hearing stories from my grandfather about the Great Depression. He saw shop owners, farmers, and his own neighbors lining up outside their bank only to find the doors locked forever and their life savings gone. It was more than a financial crisis. It was a crisis of trust.

The Full Faith and Credit Guarantee

Quick Stat: Following the regional bank failures of 2023, regulators highlighted that heavy reliance on uninsured deposits made several institutions more vulnerable to rapid withdrawals, which in turn contributed to instability in the banking system.

Here’s the most important fact you need to know: no depositor has ever lost a single penny of FDIC-insured funds. Ever. This is not a slogan. It is an officially recorded outcome over nearly a century of FDIC history.

FDIC insurance is not private coverage from an individual company that could go under. Your protection is backed by federal law and the FDIC’s Deposit Insurance Fund, which is supported by insurance premiums paid by member banks and by interest the fund earns on its investments.

What You Can Do Today

Stop thinking of FDIC insurance as just another policy. See it as a foundational feature of the U.S. banking system that protects your deposit accounts when a bank fails. To understand exactly how much of your money is covered, use the official Electronic Deposit Insurance Estimator (EDIE) from the FDIC. This tool shows how your accounts at a particular bank are insured and whether any portion might be uninsured.

Official FDIC Explanation

According to the FDIC’s own resources, FDIC deposit insurance protects the money you have in deposit accounts at FDIC-insured banks if the institution closes. It is automatic for deposits and does not require any enrollment from you. Deposits are covered up to at least $250,000 per depositor, per insured bank, per ownership category.

This protection has helped maintain trust in the banking system for nearly a century. When you see the FDIC sign at a bank, that means the institution participates in this system and deposits up to the insurance limits are protected.

Following the 2023 bank failures, the FDIC reported that nearly half of all deposits in domestic banks were uninsured. This staggering number highlights why understanding this checklist isn’t just an academic exercise—it’s a critical step to ensure your money isn’t part of that statistic.

FDIC Fact Sheet: What The Public Needs to Know

The $250,000 Rule: How FDIC Coverage Actually Works

You’ve already heard that FDIC insurance covers up to $250,000, but that description can be misleading on its own. The real rule is more specific and more useful once you understand it.

FDIC deposit insurance protects the money you keep in deposit accounts at an FDIC-insured bank if that bank fails. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. That means your coverage depends not just on how much you have, but how and in whose name the accounts are held.

That means you are insured up to $250,000 in each category of ownership at each bank. If you hold separate types of accounts that fall into different ownership categories, each category starts its own limit.

Here is how the common categories work:

- Single accounts are accounts in one person’s name. All of your single accounts at the same bank count together toward one $250,000 limit.

- Joint accounts are accounts owned by two or more people. Each co-owner of a joint account receives up to $250,000 of insurance for their share of the account.

- Certain retirement accounts, such as an IRA, are insured up to $250,000 per owner.

- Trust accounts may be insured based on beneficiary rules, and each unique beneficiary can expand your total coverage up to limits allowed by FDIC rules.

Think of FDIC insurance the way you think about groups of bags for travel. The airline limit (or the insurance cap) is $250,000 per bag type. But if you have multiple people traveling together, or different types of bags, you can bring more total value because each person or category has their own allowance.

Example of How This Insurance Protection Works in Real Life

If you and your spouse both have individual accounts at the same FDIC-insured bank, here’s how insurance can stack:

- Your own individual accounts add up and are insured up to $250,000 total.

- Your spouse’s individual accounts are also insured up to $250,000 total.

- A joint account you share is insured up to $250,000 for each of you in that joint ownership category.

That means just by using separate ownership categories, this one bank could insure up to $750,000 on behalf of your family, as long as all the accounts meet FDIC coverage rules.

You can check your exact coverage at any bank by using the FDIC’s Electronic Deposit Insurance Estimator (EDIE), which takes all your accounts and ownership categories into account and tells you what is and isn’t covered. (Link your EDIE tool earlier in the article if you like.)

Breaking Down the FDIC Insurance Rule in Everyday Language

There are three parts to remember:

- Per Depositor

This means you are treated separately from any other individual or owner on the title. - Per Insured Bank

If you spread money across different FDIC-insured banks, each bank gives you a new set of $250,000 limits for each ownership category. - Per Ownership Category

This is where savvy planning matters most. The same person can get coverage beyond $250,000 by using multiple ownership categories like single, joint, trust, and retirement accounts.

A simple first step is to write down who owns each account and in what form. That tells you (or a financial professional) exactly which FDIC categories you are using and how much is protected.

The Official FDIC Insurance Checklist: What’s Covered vs. What’s at Risk

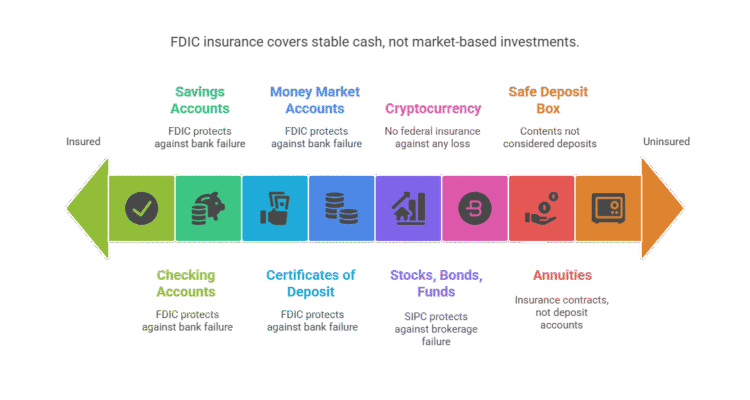

Here’s what FDIC deposit insurance actually covers when you place money in an FDIC-insured bank:

Insured Deposit Accounts

- Checking accounts

- Savings accounts

- Money Market Deposit Accounts (MMDAs)

- Certificates of Deposit (CDs)

- Cashier’s checks, money orders, and other official items issued by a bank

These accounts are protected up to the insurance limit as long as they meet the FDIC’s deposit definition. Coverage is automatic when you open an eligible deposit account at a bank that participates in FDIC insurance. :contentReference[oaicite:9]{index=9}

Here’s what FDIC insurance does not cover:

❌ Stocks, Bonds, and Mutual Funds (These are covered by Securities Investor Protection Corporation (SIPC) against brokerage failure, not market loss).

❌ Cryptocurrency Assets & Other Digital Assets (Bitcoin, Ethereum, etc., have no federal insurance).

❌ Annuities and Life Insurance Policies (These are insurance contracts).

❌ Contents of a Safe Deposit Box (Your baseball cards and grandma’s jewelry are not considered deposits).

❌ Municipal securities and similar investment products

Retirement accounts like a Roth IRA have their own specific contribution limits and tax advantages.

These are not deposit accounts under FDIC rules, even if you hold them at a bank. Other protections may apply (for example, SIPC may cover certain brokerage failures, but SIPC is not FDIC insurance).

The standard FDIC insurance amount is $250,000 per depositor, per FDIC-insured bank, for each account ownership category. This means you can increase total protection by using separate ownership categories at the same bank or by placing funds at different FDIC-insured banks.

Beyond $250k: How to Insure Every Dollar (The Smart Way)

You can protect far more than $250,000 at a single bank by strategically using different ownership categories to create multiple, separate buckets of insurance coverage.

The $250k limit isn’t a brick wall. It’s a doorway. Once you understand that, you can stop feeling anxious about being “over the limit” and start feeling smart about how you structure your accounts.

When naming beneficiaries on a Payable-on-Death (POD) account, the details matter. A single revocable trust account can also act as its own powerful ownership category, allowing you to insure millions for multiple beneficiaries at one institution. This is one of the most underused strategies for high-net-worth protection.

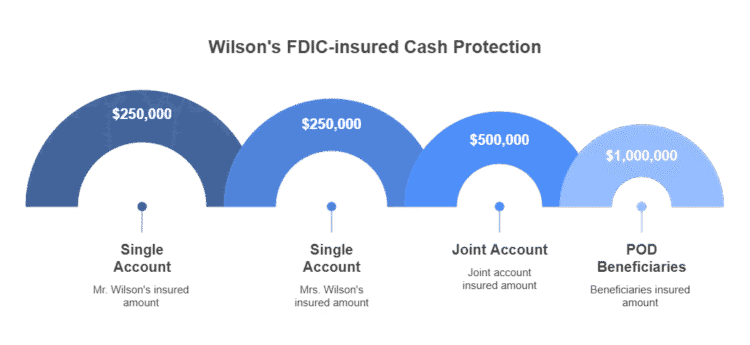

I had clients, the Wilsons, who came to me after selling their business. They had over $1.5 million in cash sitting in one account and were terrified. They were about to open accounts at six different banks across town. A logistical nightmare.

“Hold on,” I told them. “Let’s fix this right now, without leaving your kitchen table.“

The Power of Ownership Categories

We simply changed how their accounts were titled. By leveraging ownership categories, we made sure every penny was protected, all at their one trusted, local bank.

Here’s the exact math we used. It’s not magic; it’s just arithmetic.

🚀 The Coverage Maximizer Worksheet

- Step 1: Mr. Wilson’s Single Account = $250,000

- Step 2: Mrs. Wilson’s Single Account = $250,000

- Step 3: Their Joint Account = $500,000

- Step 4: Add their two kids as Payable-on-Death (POD) beneficiaries to the Joint Account. This adds a new category worth $250k per owner, per beneficiary. (2 owners x 2 kids x $250k) = $1,000,000

- Their New Total Insured at One Bank = $2,000,000

- By leveraging ownership categories, like a revocable trust account, we made sure every penny was protected…

Advanced Strategies & Nuances for High-Value Accounts

For those with more complex finances, understanding the finer points of deposit insurance is crucial. Here are key areas where savvy savers and business owners should pay close attention.

- For those with even larger cash positions, there are services that do this work for you. Cash Sweep Programs and the IntraFi Network are services offered by many banks that take a large deposit and automatically spread it across a network of other FDIC-insured institutions, ensuring every dollar stays under the limit at each one.

- Distinguishing FDIC vs. SIPC: Cash held in a bank deposit account is protected by the FDIC. Cash and securities held in a brokerage account are protected by the Securities Investor Protection Corporation (SIPC) against the brokerage firm’s failure—not against market losses. Be clear on which protection applies to which account.

- Business Account Coverage: FDIC coverage extends to business accounts (like checking or savings) just as it does for personal accounts. The FDIC insured limit applies per depositor (the business entity) per insured bank.

- Cash Management Accounts (CMAs): Many brokerage firms and FinTechs offer CMAs that “sweep” your cash into a network of multiple FDIC-insured banks. This is a legitimate way to get millions of dollars in FDIC protection while managing it all from one account.

- Irrevocable Trusts: The rules for irrevocable trusts are highly complex and depend on the specific terms of the trust document. Unlike simple POD accounts, coverage is not always guaranteed on a per-beneficiary basis. If you use trusts for estate planning, consult a financial planner to verify your specific FDIC coverage.

For those managing significant assets, this is a key part of understanding your overall net worth statement.

Trust Accounts and FDIC Coverage:

Trust accounts, including payable-on-death (POD) or other revocable trust accounts, are insured based on the number of unique eligible beneficiaries named in the account records. Under FDIC rules, a trust with five or more unique beneficiaries may be eligible for up to 1,250,000 US dollars of coverage for a single owner at the same insured bank, though specific conditions must be met.

Depositors should ensure beneficiary names are clearly recorded by the bank to receive this coverage.

Bank Failure Data and Uninsured Deposit Trends:

From 2001 through 2026, there have been 570 FDIC-insured bank failures in the United States. This demonstrates that depositor risk is real and why deposit insurance exists.

Uninsured deposits — amounts above the FDIC insurance limits — have grown significantly in recent years. When a bank experiences rapid withdrawals of uninsured funds, it can increase liquidity stress and contribute to failure.

When an FDIC-insured bank fails, the FDIC typically arranges for another insured institution to assume the deposits or directly returns insured funds to depositors, usually within a few business days of failure.

The Future of Your Money: What to Watch for into 2026

While the core FDIC rules are stable, the lessons from the 2023 banking crisis are prompting ongoing policy debates and regulatory changes that will shape the financial landscape.

As your retired planner, this is the stuff I’m telling my former clients to keep an eye on—not to worry about, but to be aware of. You don’t need to follow the daily news, but understanding the trends is smart.

Lessons from the 2023 Bank Failures

The key takeaway from the turmoil was that large amounts of uninsured deposits (money held over the key Bottom lineinsured limit) can create instability. This sparked a huge debate in Washington about whether the limit should be raised.

While a broad increase is unlikely due to concerns about encouraging risky bank behavior (what economists call moral hazard), you should expect to see targeted proposals discussed.

As FDIC Chairman Travis Hill noted, a system of unlimited insurance could have “unintended consequences.”

💡 The 2026 FDIC Watchlist

- The Health of the Insurance Fund: The FDIC is in the middle of a multi-year plan to replenish its insurance fund (the DIF), paid for by special fees on larger banks, not depositors. I am monitoring its progress toward its legally required funding level, and it remains strong and on track.

- Potential for Targeted Reform: Watch for discussions about increasing coverage for specific account types, like business payroll accounts. This was a major pain point in 2023 and is a logical area for a modest increase.

- Clarity for FinTech: Expect the Consumer Financial Protection Bureau (CFPB) to continue to push for clearer rules on how FinTech apps must advertise their FDIC insurance. This is a big win for you, the consumer.

Action Step:

Don’t get lost in the debate. Focus on what you can control. The strategies in the section above work right now and will continue to work regardless of any future changes.

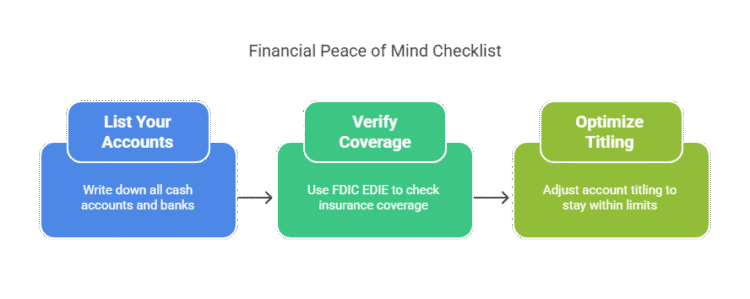

Your 3-Step Action Plan to Your Financial Security

You now have the knowledge to move from anxiety to complete confidence. Here is your simple, three-step plan to ensure every dollar of your hard-earned savings is safe.

Your Financial Peace of Mind Checklist

- List Your Accounts:

On a piece of paper, list every cash account you have (checking, savings, CDs) and the bank where it’s held. This is the foundational first step of any effective personal spending plan. - Verify Your Coverage with the Official FDIC Calculator: (takes 2 minutes)

Do not guess. Go to the official FDIC Electronic Deposit Insurance Estimator (EDIE). This is the only FDIC insurance calculator that matters. Enter your accounts as you listed them, and it will give you a definitive answer on your coverage in minutes. - Optimize Your Account Titling:

If the calculator shows you are over the limit at any bank, call them. Ask for the form to either add a joint owner (like a spouse) or designate Payable-on-Death (POD) beneficiaries (like your children or a trust). This is the simplest way to multiply your coverage.

Knowledge is useless without action. Here is your simple, three-step plan to go from reading this article to achieving total peace of mind. The infographic below explpains it very straightforward. You can do this in the next 15 minutes.

Your Top Questions Answered

Key FDIC Tools & Resources

- Use the FDIC Electronic Deposit Insurance Estimator (EDIE) to calculate how much of your deposits are protected by FDIC insurance.

- Check whether a bank is FDIC-insured with the FDIC BankFind Suite.

How do I verify a bank is FDIC insured in 2026?

Use the official FDIC’s BankFind Suite. If the bank isn’t on this list, it’s not FDIC insured. Period.

What Happens to Your Deposits When a Bank Fails?

When an FDIC-insured bank fails, the FDIC either arranges for another institution to assume your accounts or pays insured deposits directly, typically within a few business days. This process preserves access to your insured funds and minimizes disruption.

Is it safer to spread my money across multiple banks?

It is a perfectly valid strategy, but as you saw with the Wilsons, it’s not always necessary. Using ownership categories correctly is often far easier than juggling multiple bank logins and statements.

What About Uninsured Funds & Recent Bank Failures?

FDIC insurance does not protect amounts above the insurance limit. For example, in major failures like Silicon Valley Bank, more than 85% of deposits were uninsured. Highlighting the importance of strategic account structuring

Does FDIC Insurance Cover Funds Held Through FinTech or Third-Party Apps?

FDIC insurance only applies to money held in actual deposit accounts at FDIC-insured banks. Third-party apps and fintech platforms do not themselves carry FDIC insurance; instead, coverage depends on whether the funds are placed into insured accounts and are traceable to you as the depositor.

In some cases, services can arrange pass-through FDIC insurance when they place deposits at participating banks and maintain the records that link those deposits back to individual customers.

Risk Context: Why FDIC Insurance Matters?

The FDIC was created during the Great Depression to restore faith in the U.S. banking system and prevent bank runs. Today, depositors in FDIC-insured banks can be confident that their insured deposits are backed by the full faith and credit of the United States government up to applicable limits.

However, FDIC insurance does not protect investment losses, identity theft, or losses caused by fraud. It strictly covers the bank failure risk associated with eligible deposit accounts.

And with that, you are the captain of your financial ship. You know how it’s built, you know what it can handle, and now you know exactly how to secure every last compartment to ensure it can weather any storm and stay on the path to financial freedom.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.