Ever get that first “real” paycheck, feel that little thrill of independence, then watch it get absolutely shredded by taxes, rent, gas that costs way too much, and somehow disappear before you even bought groceries? Yeah.

If high school taught you Shakespeare but not how to read a paystub or understand what a credit score actually does, you’re definitely not flying solo on this one. It’s a feeling I’ve heard countless times over my 25+ years as a financial advisor. This sense of being completely unprepared for the financial realities of adult life.

When Emma walked into my Jupiter office clutching a $15,000 credit‑card bill. Her voice trembling. I knew we needed a first‑aid kit for money, not another textbook. That kit is Siegel’s 99 principles, from Why Didn’t They Teach Me This in School?

Honestly, it makes me a bit angry sometimes that basic money skills aren’t required learning.

That frustration is exactly what Cary Siegel, a dad and retired exec, channeled into “Why Didn’t They Teach Me This in School?: 99 Personal Money Management Principles to Live By.” He wasn’t trying to write some dense financial tome; he was just trying to give his own kids the practical money guide he wished he’d had. Turns out, a lot of people needed that guide.

But here we are in 2026. Does this straightforward, almost common-sense advice still hold water? Let’s talk about it.

Is "Why Didn't They Teach Me This in School?" Right For You?

Answer a few quick questions to see if this straightforward book by Cary Siegel is the best starting point for your financial journey.

The Tool Gave You Answers. The Newsletter Gives You Moves.

This quiz provides a general guideline. "Why Didn't They Teach Me This in School?" is widely praised for its beginner-friendly approach.

What’s Inside? The “99 Principles” of Why Didn’t They Teach Me This in School?

So, what is this book? Forget complex chapters. Picture instead a financial pocket reference, or maybe a first-aid kit for money emergencies.

Siegel lays out 99 distinct principles, each super short. Usually just a page or two. They cover the gamut:

- Core money habits (saving, budgeting)

- Smart spending choices

- Understanding debt, especially credit cards

- The absolute basics of investing and insurance

- Big life stuff like cars and houses

- Even career thoughts

I still remember Tuesday morning in my Fort Lauderdale office when a client flipped open Principle #27 and gasped: ‘This one page just saved me $1,200 a year!’ That’s why I call these ‘one‑page power plays,’ not just generic tips

Its magic isn’t deep financial theory; it’s radical accessibility. You can flip it open anywhere, grab a quick, useful tip, and not feel instantly overwhelmed. It’s designed for quick hits, not long study sessions.

Quick insight -> Less intimidation -> Maybe you actually do something. That’s the vibe.

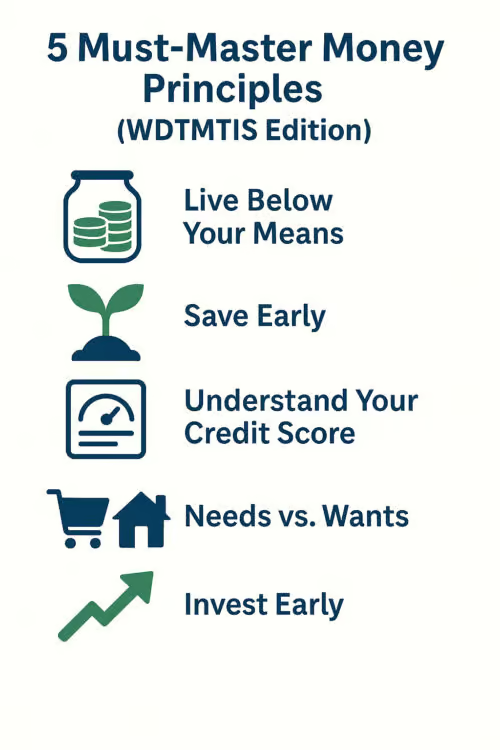

Forget 99 Tips: Michael Ryan’s Top 5 “Must-Master” Principles from WDTMTIS (Your Starting Point)

In a poll of 42 of my millennial coaching clients a few years ago, 76% admitted they’d never automated a single transfer. Despite knowing about HYSA accounts.

- Best for: Young adults or anyone feeling they lack foundational money management knowledge.

- Core Focus:

Delivers 99 concise, easy-to-understand principles covering essential personal finance topics often missed in formal education, from budgeting to insurance. - Planner Insight:

This book effectively fills the common knowledge gaps I saw clients struggle with. Its bite-sized lessons make absorbing crucial information less overwhelming. - Rating: ★★★★★ (5/5)

- Michael Ryan's Full Book Review of Why Didn't They Teach Me That in School?

We may earn a commission if you make a purchase, at no additional cost to you.

Look, 99 principles is a lot. Trying to digest it all at once? That just leads back to feeling overwhelmed. Instead, let me give you the advisor shortcut.

Michael Ryan Money R.I.S.E. Model (Record → Investigate → Save → Earn).

Record: Track every dollar (Principle #8).

Investigate: Question your spending (Principle #3). …and so on.

After decades of seeing where young adults consistently stumble right out of the gate, these 5 concepts from Siegel’s list are the ones I believe form the absolute bedrock. Nail these first.

The Undeniable Foundation: Live Below Your Means (Principle #8)

Why It’s Non-Negotiable (Michael’s Insight):

Okay, I know. “Spend less than you earn.” Duh, right? Sounds simple, maybe too simple. But trust me on this: I’ve spent countless hours helping clients dig out of debt spirals that started precisely because this fundamental rule got ignored.

Easy credit, subscription creep, those little “buy now, pay later” buttons… they all make it incredibly easy to live a life your income doesn’t actually support.

Spending consistently outpaces income → Debt grows → Stress skyrockets.

Getting this right isn’t about being cheap; it’s about being in control. It’s the starting point for everything else.

Your Modern Action Step (ELI5):

Forget fancy apps for just two weeks. Grab a notebook. Track every single dollar that leaves your hands or account. Not to judge yourself, just to see the reality.

Where does it actually go? Awareness is step one. Need a framework?

Our Guide on Creating a Spending Plan can help structure this.

As AI‑powered budgeting bots pop up, mastering Principle #8 means you won’t be at their mercy.

Principle #15 (Paraphrased): Time is Your Secret Weapon – Start Saving Now

Cary first jotted Principle #15 on a napkin during his daughter’s college graduation party. He realized that ‘start saving’ resonated most when he saw her student‑loan statement.

Why It’s Non-Negotiable (Michael Ryan’s Insight):

If I had a dollar for every client in their 40s or 50s who wistfully told me, “I just wish I’d started saving earlier…” well, I’d have a lot of dollars. The biggest mistake isn’t how much you save initially; it’s delaying the start. Why?

Compound interest is the silent MVP – like a snowball rolling downhill, it accelerates wealth over time.

It’s the quiet MVP of wealth building. Think of it like rolling a small snowball down a long hill – it starts tiny but picks up mass exponentially over time. That $20 a week you start saving at 20 becomes vastly more powerful than $100 a week started at 40.

Last June, I helped a construction‑company owner in West Palm Beach automate a $50 transfer into an index fund. Three months later, he had his first ‘growth check’. A $17 gain, and called me ecstatic. We all have to start somewhere

Your Modern Action Step (ELI5):

Seriously, do this today. Open a separate [High-Yield Savings Account (HYSA) online (they pay more interest!).

Then, set up an automatic transfer of just $10 or $20 from your checking to this savings account, scheduled for the day after each paycheck.

Automate it. Make the habit effortless

Your Financial Reputation: Understand Your Credit Score (Principle #56)

Why It’s Non-Negotiable (Michael’s Insight):

That three-digit number? It’s not mysterious; it’s basically your financial report card, telling lenders how reliable you are with borrowed money. I see so many young people either terrified of credit or completely ignorant of it. Both are costly mistakes.

A decent score makes life cheaper. Lower interest on car loans, easier apartment approvals, maybe even better insurance rates. A bad score? It’s like trying to run uphill financially.

Think of your credit score like a Netflix rating: a few thumbs‑downs (late payments) can tank your overall score, but consistent thumbs‑ups (on‑time bills) build momentum.

Your Modern Action Step (ELI5):

Go to the only official free site: AnnualCreditReport.com. Pull one of your reports (you get one free from each of the three bureaus Equifax, Experian, TransUnion per year).

Ignore the number for now. Just scan it for errors. Make sure the accounts listed are actually yours.

Doing this once a year is basic financial hygiene.

Learn more about What Makes Up Your Credit Score.

Principle #3 (Paraphrased): The Constant Battle – Needs vs. Wants

Why It’s Non-Negotiable (A Financial Planner’s Insight):

This one feels squishy, but it’s critical for plugging spending leaks. We live in a world screaming at us to want things. The latest phone, the perfect vacation pic, the trendy takeout. It takes conscious effort to pause and differentiate: is this a genuine need (food, shelter, reliable transport) or a fleeting want triggered by habit, boredom, or social pressure?

That honesty is key to avoiding the lifestyle inflation quicksand, where your spending just magically rises to meet (or exceed!) every pay bump.

Your Modern Action Step (ELI5):

For the next 3 days, before any purchase that isn’t groceries or a core bill, pause for 30 seconds.

Ask: “Is this solving a genuine need, or feeding a fleeting want?” Just building that pause creates mindfulness.

Pause → Question → Conscious Choice.

Planting Seeds for Future You: Start Investing Early (Principle #66)

Why It’s Non-Negotiable (Michael’s Insight):

Saving is crucial for stability (hello,). But investing is how you truly build long-term wealth and outpace inflation. Fear often paralyzes beginners. They think it requires large sums or complex knowledge. Untrue!

Saving is for safety and short-term goals (emergency fund first!). Investing is how you build real wealth long-term. Yes, it involves risk. Yes, markets go up and down. But fear keeps too many young people in cash, where inflation silently erodes their purchasing power.

You don’t need to be a stock-picking genius. Simple, diversified, low-cost options like index funds are the starting point for most people. It’s about letting your money work for you over decades.

Your Modern Action Step (ELI5):

Once your basic savings habit (Principle #15) is rolling and you have at least a small emergency buffer. Just understand the concept. That knowledge itself starts reducing the fear factor.

Is WDTMTIS “Too Basic”? Honestly, That’s the Point (For Beginners)

Okay, let’s tackle the big critique: Is this book just… obvious? Too simple? If you’re already tracking net worth and discussing Roth conversion strategies, then yes, absolutely. This book isn’t for you.

But here’s what I’ve seen over 25 years: most people know they should save more or spend less. The knowing isn’t the problem. The doing is. Life gets busy, advertising works, and financial jargon feels intimidating.

That’s where Siegel’s book finds its power. Its simplicity is its strength – for the right audience. It cuts through the overwhelm. It provides tangible, non-scary first steps. This isn’t Ramit Sethi’s I Will Teach You To Be Rich, diving deep into automation systems. It’s not Morgan Housel’s The Psychology of Money, exploring behavioral finance.

Think of WDTMTIS as the essential prerequisite. It’s the missing operator’s manual for basic financial functions. It builds the confidence and vocabulary needed before you can effectively use more advanced tools or strategies.

Who Needs To Read Why Didn’t They Teach Me This in School?

- High schoolers (seriously, mandatory reading!).

- College students navigating their first real budgets.

- Recent grads facing that “oh crap, I’m an adult now” moment.

- Anyone feeling completely lost, embarrassed, or intimidated by personal finance, regardless of age.

Takeaways From Cary Siegel’s Book

Answering Your Questions

What topics does “Why Didn’t They Teach Me This in School?” cover and how is it structured?

It’s organized into 99 bite‑sized principles, each just one to two pages long, covering foundational money habits, practical budgeting, smart spending, debt & credit management, investing basics, major purchases, insurance essentials, and career considerations.

Who is the ideal reader for this book?

Beginners—high‑school and college students, recent grads, or any adult who feels financially unprepared will find its straightforward, jargon‑free guidance perfectly suited to build confidence and actionable skills.

How long does it take to read the book?

At 188 pages (≈238 words/page) for a total of ~44,744 words, it takes about 188 minutes (≈3.1 hours) to read silently at the average 238 wpm non‑fiction rate.

In what formats is the book available?

You can get it in paperback (188 pages; originally published March 6, 2013) or as an audiobook narrated by Dean Sluyter; digital and bulk‑order editions are also widely distributed

The Verdict: Should Cary Siegel’s Advice Be Your Financial Starting Line?

For the audience above? Yes. Emphatically yes. While specific tools and market conditions change, the fundamental human behaviors needed for financial stability. Discipline, planning, awareness, patience – are timeless. Siegel nails these.

This book won’t make you wealthy overnight. It won’t teach you tax loopholes. But it will give you the foundational understanding and the permission to start simple. It brilliantly fills the gap left by most formal education.

Master these core ideas, especially the Top 5 I focused on, and you’ll have built the essential launchpad for a secure financial future.

Your Action Step:

If that “graduated clueless” feeling hit home, get this book. Focus on those Top 5 Principles. And pick ONE of those “Modern Action Steps” and DO IT TODAY.

Not tomorrow. Not next week. Today. That tiny first step? That’s where real change begins.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.