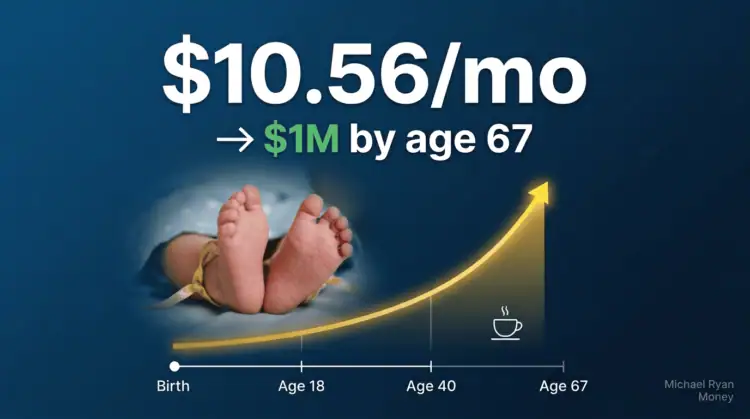

Looking at investing for a newborn? Here’s a number that will stop you mid-scroll: $10.56. That’s the monthly contribution needed to potentially build a million-dollar investment account for your child by retirement.

That’s all it takes. Per month, invested from birth, at a 10% historical market average… For your newborn to retire a millionaire at 67. Not $500. Not $1,000. Less than two Starbucks lattes.

Now ask yourself: Why isn’t everyone doing this?

Because the obvious question parents ask is the wrong one. Everything you need to know about the secrets for how to start investing money for a newborn. And how compound interest for kids really works.

Investing For a Newborn Key Takeaways

Why Parents Ask the Wrong Question About Investing Money for Children

Wondering how to start investing money for your newborn child? Most parents just ask: “How do I save enough for my kid’s future?”

The answer isn’t just saving. It’s opening a custodial investment account for your child that leverages compound growth over decades.

That’s the first obvious approach, a savings mindset.

The second obvious approach is the college fund framing:

“How do I get my child though college without debt?”

The third, counter-intuitive perspective?

Your child doesn’t need you to save for them. They need you to invest time on their behalf. Time is the asset. Money is just the trigger.

Starting investing for children early dramatically reduces the monthly contribution needed to reach $1 million by retirement. This compound interest projection shows how each decade of delay more than triples your required investment—making “start now” the most powerful financial decision for your Gen Alpha child’s future.

| Starting Age | Years to Grow | Monthly Needed | Total Invested | Cost Multiplier |

|---|---|---|---|---|

| Birth | 67 | +$10.56 | $54.83 | ✓ 1.0x (baseline) |

| Age 5 | 62 | +$17.39 | $78.04 | ↑ 1.6x |

| Age 10 | 57 | +$28.65 | $111.26 | ↑ 2.7x |

| Age 18 | 49 | +$63.81 | $197.27 | ↑ 6.0x |

| Age 25 | 42 | +$129.13 | $328.55 | ↑ 12.2x |

| Age 35 | 32 | +$359.05 | $700.08 | ↑ 34.0x |

Key takeaway: Waiting just 10 years to start investing for your child increases your required monthly contribution by nearly 3x—start with a custodial Roth IRA or UGMA account today to lock in the compounding advantage.

Source: Calculations based on S&P 500 historical average returns. Past performance does not guarantee future results. Consult a financial advisor before opening a child investment account.

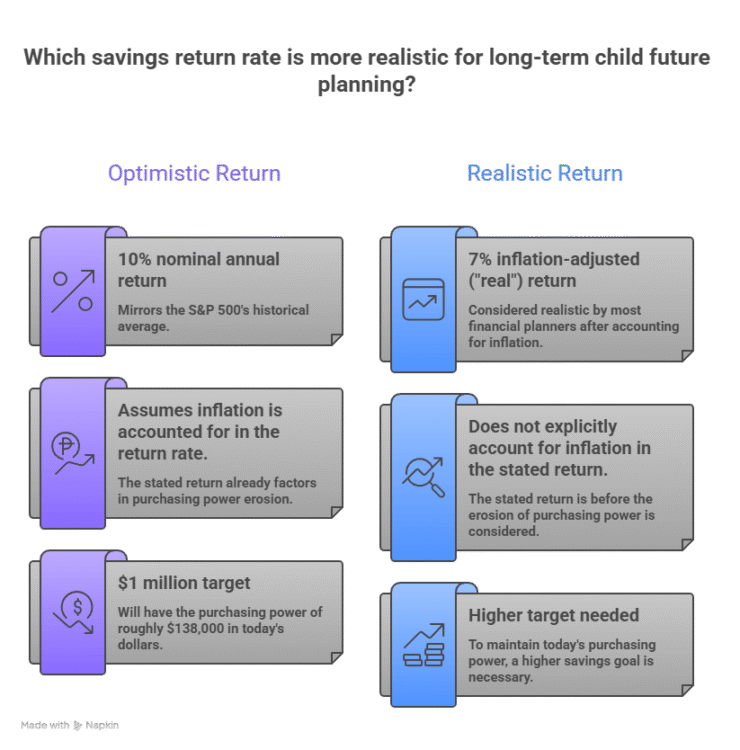

Realistic Return Assumptions for Child Investment Accounts: 7-10% Annual Return Explained

Let’s be brutally honest about the math. Because the fine print is where most financial content fails you.

The $10.56/month figure assumes a 10% nominal annual return, which mirrors the S&P 500’s historical average going back to 1957. That’s the optimistic scenario. The more sobering number uses a 7% inflation-adjusted (“real”) return, which is the figure most financial planners consider realistic after accounting for the ~3% annual erosion of purchasing power.

Three critical assumptions underpin every projection:

- Return rate: 7–10% annually, depending on inflation adjustment

- Time horizon: 49–67 years (the childhood starting-age advantage)

- Consistency: Monthly contributions that never stop, never pause, never “take a break during market downturns”

🔍 Explained Simply

Nominal returns (~10%) sound impressive but ignore inflation. Real returns (~7%) reflect actual purchasing power growth. Plan child investments using the 7% figure for realistic expectations.

And here’s the twist that I see most other articles skip. That nominal $1 million at age 67 will have the purchasing power of roughly $138,000 in today’s dollars. How assuming 3% annual inflation over 67 years. That’s not a reason to quit though. It’s a reason to aim higher than $1 million and to use accounts that compound tax-free.

The Childhood Savings Advantage Is Not What You Think

What if the biggest financial mistake parents make isn’t starting late. It’s starting with the wrong account?

Starting early matters enormously. Investing just $50/month at 7% from birth grows to over $21,000 by age 18. Wait until the child turns 10, and that same $50/month reaches only $6,400 — a third of the result, for the same dollar amount invested. The math doesn’t forgive a 10-year delay.

But here’s the counter-intuitive truth: a child who starts investing at birth in a taxable custodial account (UGMA/UTMA) will underperform a child who starts at 13 in a tax-advantaged custodial Roth IRA.

Best Investment Accounts for Children in 2026: Custodial Roth IRA vs 529 vs UGMA/UTMA Compared

Most parents default to a 529 plan. That’s the first obvious answer. The second obvious answer is a savings bond. The actual best answer depends on whether your child has earned income — because that changes everything.

💡 Michael Ryan Money Tip

Child has earned income? Prioritize a custodial Roth IRA for tax-free lifetime growth. No earned income? Use a UGMA/UTMA for flexibility or a 529 for education-specific goals.

Custodial Roth IRA for a Child (if earned income exists)

This is the crown jewel. Contributions grow tax-free for life for your child if invested in a Roth IRA. The 2026 Roth IRA contribution limit is $7,500 or the child’s total earned income, whichever is less.

A 15-year-old who mows lawns and earns $3,000 can stash all of it here. By retirement, that single teenage year of contributions could compound into six figures. Per IRS Publication 590-A, the 2026 Roth IRA contribution limit is $7,500 for individuals under 50.

UGMA/UTMA Custodial Accounts: No Income Requirement for Child Investing

No income requirement to save for your child in an UGMA or UTMA account. Parents open and manage them; the child takes full control at 18–21. These custodial brokerage accounts for minors allow investment in stocks, ETFs, and mutual funds with no earned income requirement.

According to the “Kiddie Tax“, he first $1,350 of unearned income (2026) is tax-free; earnings above that are taxed at the child’s rate (typically much lower than parents). Downside: once the child reaches age of majority, the funds legally belong to them. They can spend it however they want.

529 College Savings Plan: Tax-Free Growth for Education Expenses (Now With Roth Rollover)

Tax-free growth only for qualified education expenses. Recent rule changes allow rolling unused 529 funds into a Roth IRA (subject to limits), making them more flexible than ever.

In 2026, you can gift up to $19,000 per beneficiary ($38,000 if married) without triggering gift tax. The lifetime gift/estate tax exemption is $15M (2026).

–> Learn how the SECURE Act 2.0 529 to Roth IRA rollover works in this article.

Youth Brokerage Accounts (Ages 13-17): Teaching Kids to Invest With Supervised Accounts

A supervised brokerage for ages 13–17 with a debit card. It’s less about maximizing returns and more about building the habit of investing before adulthood. Parents co-manage; the teen sees how their money grows in real-time.

For example, platforms such as Fidelity Youth Account and Charles Schwab Teen Investor Account offer parent supervised investing with debit cards.

Should You Fund Your Child’s Investment Account Before Your Retirement? The Oxygen-Mask Rule

Stop right here. Before you redirect a single dollar toward your kid’s account, answer this: Do you have a 3-month emergency fund? Are you capturing your full employer 401(k) match?

If the answer to either is no, prioritize your emergency fund and employer 401(k) match before opening a custodial account for your child.

This sounds harsh, but it’s actually protective. A parent who depletes their emergency fund to fund a custodial account and then has to liquidate investments during a market downturn teaches their child the most damaging financial lesson possible: that markets punish you.

The oxygen-mask rule applies to family finance. Secure yours first.

Once your financial foundation is solid, a layered approach works:

- Prioritize employer 401(k) match (it’s an instant 50–100% return)

- Fund your own Roth IRA if eligible

- Then direct surplus toward your child’s account

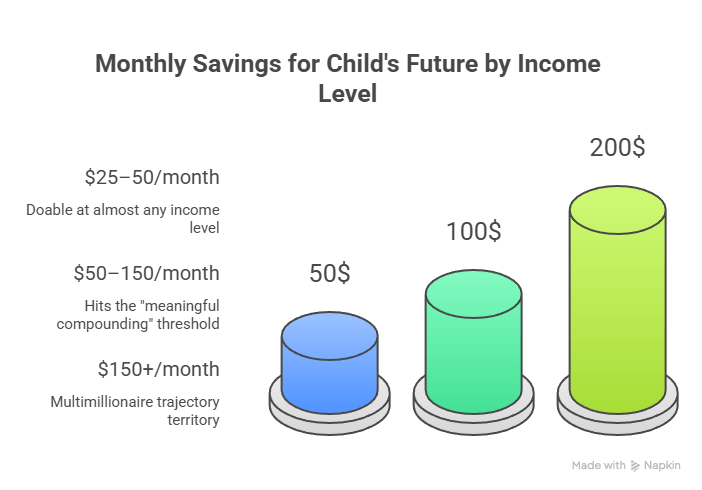

How Much to Invest Monthly for Your Child: $25-$150 Strategies for Middle-Income Families

Here’s the number most other financial content is too timid to say out loud: $50 to $100 per month is the sweet spot for middle-income families starting in childhood.

At $50/month with a 7% real return starting at birth, a child won’t retire with a million dollars in today’s purchasing power. But they’ll have a substantial head start that dramatically reduces their own savings burden in adulthood.

At $100/month from birth at 10% nominal returns, they’re looking at well over $2 million at 67.

The practical breakdown for a median-income household:

- $25–50/month:

Doable at almost any income level; open a no-fee UGMA custodial account at a firm like Fidelity or Vanguard (zero account minimums, fractional shares available) - $50–150/month:

Hits the “meaningful compounding” threshold; consider UGMA plus a custodial Roth if the child has earned income - $150+/month:

Multimillionaire trajectory territory, especially if started before your child turns age 10

Why Consistent Monthly Contributions Beat Large Lump Sums for Child Investment Accounts

Here’s the experiment nobody runs though… This is the “dollar-cost averaging for kids” paradox of compound interest: the first dollars invested have the most time to compound.

Take two parents.

- Parent A invests $200/month for 10 years starting at the child’s birth, then stops completely.

- Parent B invests $100/month starting when the child is 10, and never stops until retirement.

Parent A wins by a landslide, despite investing for half as long and stopping entirely. This is the “early quitter beats the disciplined late starter” paradox of compound interest when investing money for your young child.

The first dollars in are the most powerful dollars that will ever enter your kid’s savings account. Each month you delay isn’t just a month of your child’s missed investment contributions. It’s a month of lost compounding interest on every future contribution of savings for your kid.

Consistency matters most when stock markets are down. The parents who paused monthly savings contributions in 2020 or 2022 cost their children tens of thousands of dollars in future value. Not because of the missed contributions, but because they missed buying assets at a discount.

–> Learn more about how time in the market beats market timing in this article

5 Common Mistakes Parents Make When Investing for Children (And How to Avoid Them)

After the math checks out, human behavior is where the wealth evaporates. The most common parent investing mistakes:

- Mistake #1: Choosing High-Yield Savings Accounts Over Brokerage Accounts for Long-Term Child Investing

A high-yield savings account earning 4–5% feels safe but loses to inflation over 50+ year periods. Kids need equity exposure, not cash-equivalent returns. - Mistake #2: Stopping Contributions During Market Downturns—The Most Expensive Error in Custodial Accounts

This is the single most expensive mistake. Selling low and pausing contributions during downturns permanently impairs compound growth. - Mistake #3: Over-Concentrating in 529 Plans Without Diversifying to Custodial Roth IRAs

Parents who fund only 529 accounts and have children who don’t attend college can face penalties and restrictions. Diversify account types. - Mistake #4: Waiting for “The Right Amount” Instead of Starting Small With Child Investment Accounts

$25/month invested today outperforms $200/month invested three years from now. Imperfect action now beats perfect planning later. - Mistake #5: Treating UGMA/UTMA Accounts as Family Emergency Funds (Legal Warning)

UGMA accounts, once established, belong to the child. Many parents forget this and mentally earmark the funds for family emergencies.

How to Teach Financial Literacy to Gen Alpha While Building Their Investment Portfolio

What if the best investment isn’t in the account, but in the child’s brain?

Financial education for children compounds just like money. And platforms like Next Gen Money or Greenlight can help automate the lesson.

A child who understands why $10.56/month becomes $1 million is a child who will never make the catastrophic financial mistakes that wipe out adult wealth. The impulse car purchase financed at 24%, the credit card balance carried for years, the 401(k) cashed out during a job transition.

Practical ways to build financial literacy alongside the portfolio:

- Show your child the account. Log in together monthly. Let them watch the number grow. This activates the same reward circuitry that makes video games addictive. But for saving.

- Let your kids earn contributions. For children with custodial Roth IRAs, earned income is required anyway. Making them earn (and then “invest” their earnings with a parent match) creates skin in the game.

- Use real market events as teachable moments. A market drop isn’t a crisis — it’s a lesson in staying the course. The parent who reacts calmly in 2030 when markets dip 20% will have a child who doesn’t panic-sell in 2050.

- Introduce the “future self” framework. Research shows humans are more likely to save for retirement when they feel emotionally connected to their future self. Show your 10-year-old an age-progression photo of themselves. Sounds gimmicky; works remarkably well.

Why Boring Index Fund Investing Beats Crypto for Gen Alpha Wealth Building

The generation that grew up watching TikTok millionaires and crypto influencers has a dangerous misconception: that wealth is built through big bets and viral moments.

The actual data says something entirely different. A child whose parents invested $50/month from birth in a boring S&P 500 index fund will almost certainly outperform the adult who tries to “catch up” with aggressive trading in their 30s.

Gen Alpha doesn’t need a hot stock tip. They need a Fidelity custodial account, a $50 monthly auto-transfer, and a parent patient enough to never touch it.

The boring path is the wealth path. Start today, not when you have “enough” to invest. The compounding clock doesn’t wait for perfect financial conditions. And neither should you.

Key Resources

- Using a Roth IRA to Pay For College

- Everything to Know About 529 Plans

- Types of College Savings Accounts

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.