Did you know that the average American worker spends over a third of their life at work? That’s a staggering amount of time. Yet, when I ask new clients what their time is worth per hour, most salaried employees just shrug.

They know their annual salary, but they’ve never calculated their true hourly wage.

As a financial planner for over 25 years, I’ve seen people make six-figure career mistakes based on a misunderstanding of this simple calculation. This guide is here to change that.

We’ll walk you through the process of calculating your hourly wage from your annual salary step-by-step, explore the critical factors that impact your real take-home pay, and provide a powerful annual salary to hourly calculator to do the heavy lifting for you.

Key Takeaways Ahead

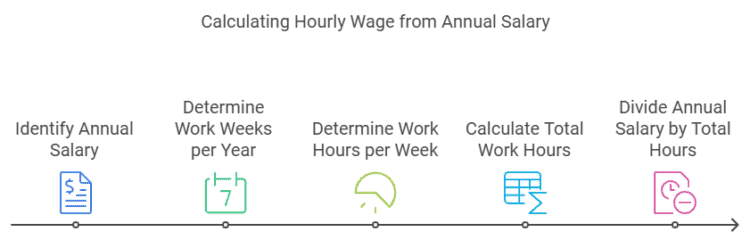

How to Calculate Your Hourly Wage from Your Annual Salary

To convert your annual salary into a gross hourly wage, we start with one key number: 2,080. This is the standard number of work hours in a year for a full-time employee (40 hours/week x 52 weeks/year).

The Basic Formula:

Hourly Wage = Annual Salary / 2,080

- Example: If your annual salary is $50,000, your gross hourly wage is:

$50,000 / 2,080 = $24.04 per hour

But as with most things in finance, this is just the starting point. Let’s use our interactive tool to move beyond the basics.

Your Interactive Annual Salary to Hourly Wage Calculator

To make these calculations easier, I’ve included an enhanced annual salary to hourly wage calculator. This tool allows you to input your specific salary and work schedule to get a precise gross hourly rate.

Annual Salary to Hourly Wage Calculator

See an issue or have a suggestion? Let us know!

Beyond the Basics: Calculating Your True Take-Home Hourly Rate

Your gross hourly wage is a useful number, but it’s not what you actually put in the bank. To understand your true hourly rate, you must account for unpaid overtime, taxes, and benefits.

The Salaried Employee Trap: How Unpaid Overtime Dilutes Your True Worth

I’ll never forget a client, ‘James,’ who was considering a new job with a $115k salary, a big jump from his current $95k. He was ready to accept until we did the math.

His current job was a strict 40 hours a week, making his true hourly rate about $45.67. The new job, he admitted, would require at least 55 hours a week.

That “higher” salary was actually a pay cut to about $39.86 per hour.

He would have been working an extra 15 hours a week for less pay per hour. This is the most common trap for salaried-exempt employees.

From Salary to Total Compensation

Before you calculate your hourly rate, you need to understand your Total Compensation.

This is your salary plus the annual value of your employee benefits, like a 401(k) match or employer-paid health premiums. A job with a lower salary but a fantastic benefits package can often be the better financial choice.

Factoring in Federal, State, and FICA Taxes

Your paycheck is subject to several types of taxes that will reduce your take-home pay. These include:

- Federal Income Tax: Based on the federal tax brackets for the current year.

- State and Local Taxes: These vary significantly depending on where you live.

- FICA Taxes: This is a flat 7.65% tax that covers Social Security and Medicare.

⚠️ Don’t Confuse Gross with Net

Your gross wage is your pay before any deductions. Your net wage is your actual take-home pay. I’ve seen clients make major budgeting errors by basing their spending on their gross income, only to find themselves short on cash after taxes and deductions.

The True Hourly Rate Calculator: Your Financial Planning Ally

Forget trying to calculate all those deductions yourself. I’ve developed a more powerful, multi-step calculator to do it for you. This tool will walk you through calculating your true take-home hourly rate.

- Step 1: Enter Your Annual Salary & Average Weekly Hours. Be honest about your overtime!

- Step 2: Enter Your Per-Paycheck Deductions. Look at your pay stub and enter your pre-tax deductions like health insurance premiums and 401(k) contributions.

- Step 3: Get Your True Hourly Rate. The tool will annualize your deductions, estimate your taxes, and calculate your net hourly wage.

Special Scenarios: Adapting the Calculation for Your Job

Not everyone works a standard 9-to-5. Here’s how to adjust the formula for different work situations.

For Part-Time Workers

If you work part-time, replace 2,080 with your actual annual hours.

- Example: You work 20 hours per week for 50 weeks a year (1,000 hours). On a $30,000 salary, your hourly wage is $30/hour ($30,000 / 1,000).

For Freelancers & Contractors

If you’re a freelancer, calculating your hourly rate from your target annual income is crucial for profitability. You must account for self-employment taxes and the cost of benefits you now pay for yourself.

💡 Michael Ryan Money Tip for Freelancers

I had a client, a graphic designer, who left a $100k job and was thrilled to bill at $50/hour, not realizing that after paying $7,650 in self-employment tax and $6,000 for a health plan, her $50/hour rate was actually a $13k pay cut. To find your target freelance rate, start with your desired annual salary, then add 25-30% to cover these new costs.

Frequently Asked Questions About Salary to Hourly Conversion

Q1: How do I account for overtime in my hourly wage calculation?

A: If you are an hourly employee eligible for overtime under the Fair Labor Standards Act (FLSA), you are typically paid 1.5 times your regular rate for any hours worked over 40 in a week. Salaried employees are often exempt from overtime.

Q2: What is the standard number of work hours in a year?

A: While 2,080 is the standard for a full-time, 40-hour/week job, your actual hours may vary. Always use the number of hours specific to your job for the most accurate calculation.

Q3: How often should I recalculate my hourly wage?

A: You should recalculate whenever you get a pay raise, change jobs, or experience a significant change in your tax situation or benefits deductions.

Conclusion: Empower Yourself with Your True Hourly Wage

Understanding your hourly wage from your annual salary is a vital step in mastering your personal finances. By using an annual salary to hourly calculator that accounts for all the real-world variables, you can make informed decisions about budgeting, job offers, and career planning.

Remember, your time is valuable. Understanding its worth is the first step toward achieving your goals.

Ready to compare a new job offer? Download our free “Job Offer Comparison Worksheet” to analyze salary, benefits, and other factors side-by-side, ensuring you make the best career move for your financial future.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.